Global X ETF Model Portfolio Team

Global X ETF Model Portfolio Team

Editor’s Note: Conversational Alpha® (CA) is a vehicle we use for deeper and more relatable discussions about portfolio construction. In that sense, it represents both a journey and destination. This report is a periodic look at journeys and destinations that investors may want to consider.

After some days in the market, stashing money under the proverbial mattress can seem like the better bet. Many investors and companies with cash in Silicon Valley Bank (SVB) likely felt the same at one point or another in the panicked 48-hour run that led to its failure on Friday, March 10. The risk of exceeding the $250,000 Federal Deposit Insurance Corporation (FDIC) limit became acute as companies with millions in payroll were on the cusp of not being able to access their funds. But by Sunday, March 12, financial regulators stepped in to ensure depositors had access to their deposits, calming anxious markets.

Of all the angles to take with this still-developing story in these turbulent conditions, my focus here is mindset and diversification. Even as I write this piece, we get news of an emergency loan for Credit Suisse and the cash infusion to First Republic by a consortium of banks, so it can be difficult for investors to keep up with the rapid news flow and the potential investment implications. My view is that investors can find comfort in the long-term, big-picture view and the knowledge that they do have safe return options that don’t include hiding under a rock.

Conversation Starters

- Market crises are part of the investing deal, so diversification should be too.

- It’s been 15 years since investors have had such meaningful opportunities in cash.

- Equity markets typically struggle early in hiking cycles, so today’s cash option is a plus.

- Moving On…Let’s Chart: U.S. consumer credit card debt a worrying trend.

- To Wrap It Up: Portfolio considerations.

SVB Just the Latest Uncertainty

The past few years have been marked by a series of extraordinary events, including the pandemic, significant fiscal and monetary policy interventions, inflation, and the transition away from easy monetary policy. The regional bank crisis is yet another challenge. The fallout will likely continue in the coming days, weeks, and months, but the broader banking system remains healthy, and risks seem contained. Notably the banks that were saved by the government during the Global Financial Crisis, seem to be helping manage the contagion.

Now, we can’t forget the inflation angle. The market seemingly found some clarity in the Fed’s near-term path from the February CPI print, which confirmed that inflation is still high and sticky. However, it largely came in as expected. Core inflation is stickier than headline inflation, with food and services remaining high. But the market reacted positively to the prints.

In my opinion, all signs point to the Fed increasing the federal funds rate by 25 basis points at the March 21–22 meeting despite the concerns in the banking sector. This relative certainty shouldn’t be underestimated amid all the uncertainty because Fed rate hikes in this environment provide investors options.

Near 5% Short-Term Yields Are an Option

It’s understandable why a black swan event like a bank’s sudden collapse can catch investors off guard, but with a diversified portfolio, panic doesn’t have to be their default reaction when it happens. One of the reasons why this volatile period differs from others in recent memory is that investors can diversify their portfolios with cash or a cash equivalent that pays varied interest depending on the selected maturity date. The real rate may still be below inflation, but a roughly 4.8% instrument that provides a solid nominal rate as an alternative to long-term bonds and stocks doesn’t seem like a bad place to be.

I would not fault any investor for waiting in cash right now. What I cannot do is predict when they should jump back or go deeper into equities. Timing the market is a fool’s errand. Only a few get it right, and those who do are likely lucky. That’s why I am a big believer in diversification; it helps me sleep at night when markets are turbulent, and even when they’re not.

With that said, while the S&P 500 is unlikely to outperform cash in the near term, it is very likely to over the long term. The S&P’s annualized return from 1970 to March 9, 2023, is 7.3%1, demonstrating the benefit of staying invested with a diversified approach over a range of time. For the long term, I prefer equities to long duration bonds, but it doesn’t mean that long bonds should not be part of the mix. Don’t forget, with inflation around ~6%2, a nearly 5% treasury locks in a real loss of about ~1%3.

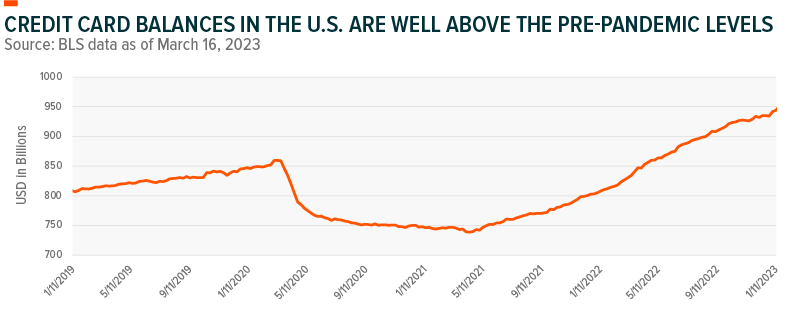

Let’s Chart: U.S. Consumer Credit Card Debt a Worrying Trend

More and more people are relying on credit cards to cover essential expenses like rent and groceries. According to TransUnion’s latest quarterly report, U.S. credit card debt hit an all-time high of $930.6 billion at the end of 2022, an 18.5% year-over-year (YoY) increase.4 The average balance per person is $5,805, a 13.2% YoY increase.5 Adding to the problem is that credit card interest rates are higher, and inflation is eroding savings that people may have accumulated during the pandemic.

The accompanying surge in delinquencies is another worrying trend. Historically low unemployment increases the financial stability of households, but inflation and interest rates are testing some borrowers’ ability to repay their debts. If unemployment rises and delinquencies rise further, it could indicate a more significant long-term issue that the Fed must consider.

To Wrap It Up: Portfolio Considerations

Markets are in transition given the end of the extraordinarily low rates era that fueled higher stock prices for years. Quite simply, higher rates now require an adjustment period. Returns, and where they come from, will likely look different in this rates environment. For example, this period may include the 60/40 portfolio’s return to relevance, assuming duration is calibrated appropriately. Investing isn’t a static exercise. It requires continued dexterity based on risk profile, time horizon, and a host of investor-specific factors. Keep that in mind, and volatility can be kept in perspective.