Global X Research Team

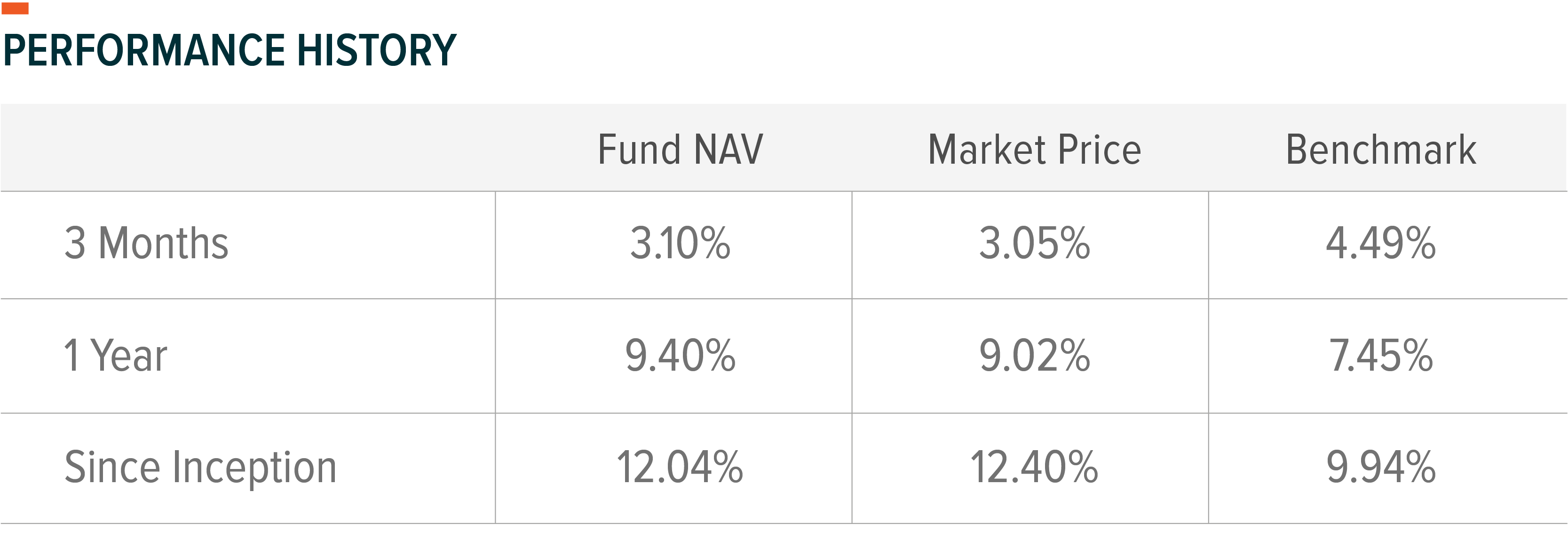

Global X Research TeamDuring Q2 2021, EMBD posted a total return of +3.10%. This compares to a gain of +4.49% for the JP Morgan EMBI Global Core Index, the fund’s benchmark, over the same period. The benchmark index tracks liquid, US dollar emerging market (EM) fixed and floating-rate debt instruments issued by sovereign and quasi-sovereign entities.

The performance data quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance data current to the most recent month end, please click here. Total Expense ratio: 0.39%.

Cumulative return is the aggregate amount that an investment has gained or lost over time. Annualized return is the average return gained or lost by an investment each year over a given time period.

General Market Review

Following a powerful risk-on sentiment in the first quarter, the market’s global reflation narrative stalled in the second quarter. 10-year US treasury yields, which rose 82 basis points to 1.74% at the end of Q1, started to move lower during Q2 and ended the quarter at 1.47% despite stronger US employment data and higher inflation prints. Several factors drove bond yields lower in Q2: 1) strong overseas demand for US bonds, which was absent in Q1; 2) additional liquidity of about $1 trillion injected into the system due to the US Treasury’s decision to withdraw General Accounts at the Fed and therefore less issuance; and 3) the continued spread of the COVID-19 Delta variant. Nevertheless, the lower bond yields observed in Q2 cast doubt on investors’ global reflation narratives.

Other factors were important drivers in Q2 as well. First, a surge in global consumption collided with significant supply chain bottlenecks. Dwindled corporate inventories, production shortages, and aggressive purchasing habits led to surges in inflation during the re-opening period. Second, the Fed, which maintained a dovish stance in Q1 by emphasizing a flexible 2% average inflation target, turned surprisingly hawkish at the June FOMC meeting. The 2023 median dot plot showed 2 hikes compared to previous guidance of zero rate hikes in 2023. And finally, concerns over the more infectious COVID-19 Delta variant impacted risk-asset sentiments as EM economies with low vaccination rates reintroduced restrictive lockdown measures to contain the spread. The inflation narrative certainly changed in Q2, but central banks like the Fed moved ahead with more hawkish policy stances.

While developed markets (DM) progressively opened up their economies in Q2 as vaccination rates improved, numerous EM countries were unable to secure vaccines and experienced a coinciding third wave of COVID-19 cases due to the more infectious Delta variant. With low vaccination rates, the new spread forced some EM countries to adopt restrictive social-distancing measures to prevent a deterioration of their health care systems. These actions inevitably pared growth expectations. The growth divergence between EM (excluding China) and DM shifted from +6.5% in Q1 to -11.9% in Q2, as Latin America and EM Asian economies shrank during the quarter. Vaccine shortfalls, limited fiscal buffers, and rising prices of basic goods fostered social unrest and political instability as well. As a result, EM investors faced mounting risks in Q2.

The Chinese government also continued its policy normalization in Q2. Officials viewed excess corporate debt levels and rising real estate prices as high priority issues. The government’s tightening measures on the housing market and its lending to the sector started to affect the domestic economy as PMI numbers declined during the period from 51.9 in March to 50.9 in June.

However, the most critical driver for financial asset prices in Q2 was the relentless supply of liquidity by global central banks. When Europe’s vaccination program got off to a slow start relative to the US, the European Central Bank (ECB) quickly announced a plan to accelerate the pace of its bond-buying program to inject more liquidity into the financial system. The Fed’s $120 billion per month quantitative easing program continued to flood the system with excess reserves even as US personal consumption expenditure (PCE) figures accelerated by 3.4% in May YoY. Ultimately, supportive liquidity measures drove EM asset gains during Q2, despite a more challenging macro environment and talks of tightening policy.

During the quarter, the emerging sovereign debt market returned +4.49% led by the high-yield sector with a return of +6.05%. The investment-grade sector, which benefited from the 10-year US government yield declining by 27 basis points, also posted a gain of +3.28% for the period. The key investment story for EM debt during Q2 was the major outperformance of issuers with idiosyncratic risks that performed poorly in 2020, such as Ecuador (+48.7%), Lebanon (+9.1%), Angola (+10.8%), Zambia (+11.8%) and Sri Lanka (+8.7%). The victory by a conservative businessman, Guillermo Lasso, in Ecuador’s run-off presidential election in April over favored left-wing economist Andres Arauz was the major surprise for EM investors as sovereign Ecuador bonds rallied over +45% following the election. However, other distressed issuers did not have noteworthy developments to support positive price actions, except that these issuers were not going to tap the new issue market and were less sensitive to rate volatility.

In contrast to Ecuador, Peru and Chile surprised the market negatively as far-left candidate Castillo won Peru’s run-off election and progressives and left-wing representatives aim to lead Chile’s constitutional reform. Sub-Saharan Africa was the best performing region up +6.1% during the period driven by strong commodity prices, limited new issuances, and positive developments related to forthcoming Special Drawing Rights (SDR) allocations. The worst performing country was El Salvador which posted a loss of -3.9% as President Bukele ousted Attorney General and Supreme Court judges to consolidate his power rather than working with the IMF to secure $1 billion in financing to plug budget gaps.

The emerging corporate debt market, which outperformed the sovereign debt market in Q1, posted a moderate return of +2.2% for the period. Similar to the emerging sovereign debt sector, the high-yield sector outperformed the investment-grade sector driven by the strong performance of energy and mining issuers on the back of high commodity prices. The only sector that generated weak performance was China’s high-yield sector, as regulators continued tightening policy to reign in the excess in China’s real estate market.

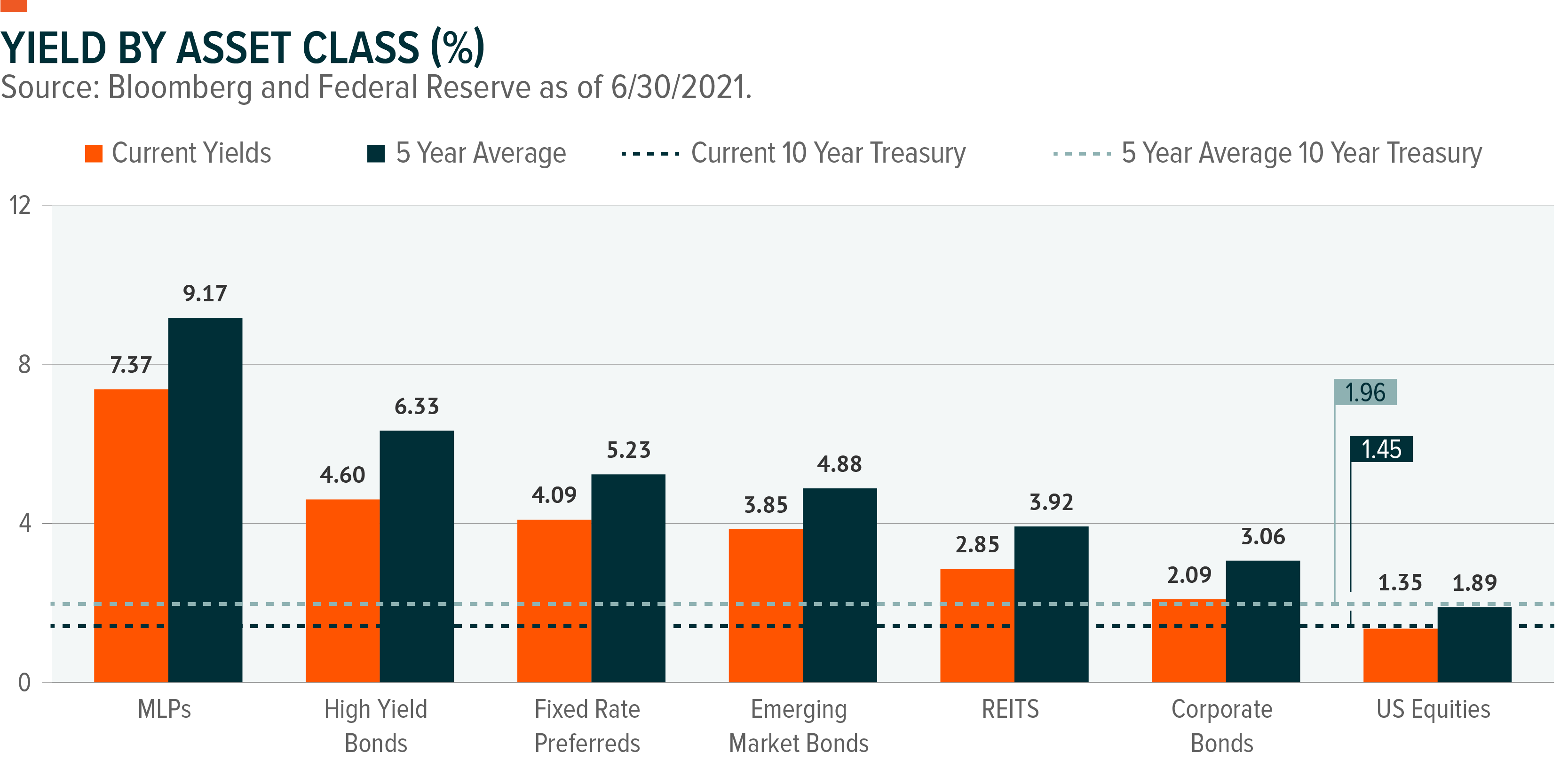

Note: Asset class representations are as follows, MLPs, S&P MLP Index; High Yield Bonds, Bloomberg Barclays US Corporate High Yield Total Return Index; Emerging Market (EM) Bonds, Bloomberg Barclays EM USD Aggregate Total Return Index; Corporate Bonds, Bloomberg Barclays US Corporate Total Return Index; REITs, FTSE NAREIT All Equity REITS Index; Equities, S&P 500 Index; and Fixed Rate Preferreds, ICE BofA Merrill Lynch Fixed Rate Preferred Securities Index. The performance data quoted represents past performance and does not guarantee future results.

EMBD Portfolio Attribution

During the quarter, EMBD underperformed its benchmark by 139 basis points. EMBD’s lower duration relative to the index was a main detractor to performance as US treasuries rallied during the period. Heading into Q2, the fund maintained its underweight duration exposure due to the thesis that the passage of a US infrastructure bill would require higher Treasury issuances amidst the strong growth recovery, which is expected to drive the government yields higher. Therefore, the fund maintained underweight positions to high-quality long-duration countries such as Malaysia, the Philippines, Indonesia and Uruguay. The underweight to Ecuador sovereign bonds was a leading detractor to performance as Ecuador bonds rallied +43% following the market-friendly election outcome. On the other hand, our selection of corporate and quasi-sovereign bonds in Peru contributed positively to performance.

Outlook & Strategy

We expect the EM-DM growth differences to narrow in the second half of 2021 as the vaccination-led recovery begins to positively impact EM. With vaccine rates plateauing in DM countries and vaccine production ramping up, we expect the EM countries to gain access to vaccines and follow the path of the DM vaccination roll-out. For those EM countries currently in the lockdown stage due to the COVID-19 Delta variant, our assumption is that economic activity could start to improve as early as Q3 with the easing of restrictions. That being said, vaccination campaigns will be uneven even within EM, hence the economic recovery will vary across EM.

Recent concerns of growth slowing down in DMs due to a rise in COVID-19 cases from the highly transmissible Delta variant may not lead to the reintroduction of lockdown measures in DM as vaccines show a high degree of efficacy against hospitalization and death. Therefore, even if COVID-19 Delta cases rise in the US or Europe in the second half of the year, we do not expect the growth trajectory to deviate from the current path. More importantly, we do not expect the Fed to alter its policy normalization shift due to the new wave of infections in the US.

Despite growing concerns that current inflation prints may not be as transitory as the Fed suggested, we do not expect the Fed to initiate the tapering process, nor bring forward its first hike date much sooner than what is priced in the market. The reason is that many uncertainties are impacting the current inflation prints beyond the base and transitory effects. For example, the Fed may want to understand the impact of the recent surge in commodity prices on inflation expectations. Given that the US is ahead of other economies in terms of the recovery cycle, we do not expect the Fed to push forward with hawkish monetary policy as its policy response will likely knock the global recovery off course. Consequently, our view is that the market will view the Fed as dovish.

We expect the Fed to officially announce the tapering policy either in Jackson Hole or September’s FOMC meeting, with actual tapering beginning in December 2021 or early 2022. Our view is that this announcement will cause the 10-year Treasury yield to move gradually higher helped by a rise in real yields. However, the speed at which government yield increases will be a much more measured pace than what the market observed in Q1, given that the market will only tolerate higher yields to the extent that the global recovery in Europe and EM are maintained.

Even though we are past the peak liquidity cycle, driven by the additional $1 trillion dollars of reserves pumped into the financial system with the drawdown of the US Treasury’s General Account at the Fed, we expect the abundance of liquidity in the financial system to support growth and carry assets as the Fed and ECB continue their QE program. As a result, we expect investors to consider EM credit assets which should benefit from the global recovery (i.e. rising commodity prices) while offering carry income in a rising volatile rate environment.

We maintain our view that global bond yields will move higher in the second half of the year, with EM credit spreads absorbing much of the rate moves. Therefore, we favor high-yielding assets over the investment-grade sector, given that there are more spread buffers to absorb in the high-yield sovereign bonds. Also, the SDR allocations in the second half of the year will bring much-needed liquidity support for higher-yielding sovereign issuers. That said, we believe credit differentiation driven by idiosyncratic developments and the progress in vaccine roll-outs will continue to be the central theme for EM assets. We find the EM corporate sector offers attractive investment opportunities as corporate fundamentals continue to improve with the global recovery while management teams have generally maintained conservative strategies to strengthen balance sheets. Also, we find particular corporate issuers such as Colombian utilities and Peruvian corporates attractively priced as the sovereign downgrade (i.e. Colombia) and political instability (i.e. Peru) put pressures on corporate issuers. We anticipate that market volatility will remain elevated as the Fed’s tapering discussions, COVID-19 variant concerns, and the Biden administration’s Infrastructure Plan may alter either growth trajectory or policy directions.

Related ETFs

EMBD: The Global X Emerging Markets Bond ETF (EMBD) is an actively managed fund sub-advised by Mirae Asset Global Investments that seeks a high level of total return, consisting of both income and capital appreciation, by investing in emerging market debt.