Rohan Reddy

Rohan ReddyThe Global X Income Outlook for Q1 2021 can be viewed here. This report seeks to provide macro-level data and insights across several income-oriented asset classes and strategies.

Key Takeaways:

- Inflation expectations are rising alongside economic acceleration, resulting in selloffs in longer dated bonds. While inflation may continue to rise in the near term, it appears unlikely to reach unusually elevated levels. Energy, materials, and industrials typically perform well in this type of reflationary environment.

- Income-oriented investors may be wise to reduce the duration and instead focus on credit-like instruments like preferreds, or gaining exposure to high yielding Energy investments.

- The Nasdaq 100 faces a mixed return outlook in the midst of a rotation from growth to value, so a covered call strategy is a potential alternative for income and tech exposure.

Inflation Expectations Rising, But Likely to Peak in 2021

Inflation numbers in February came in at their highest levels since the pre-pandemic period, with the Consumer Price Index (CPI) reading 1.7% year-over-year. There are reasons to believe inflation could continue to rise from here. In fact, the market expects this. 10-year Treasury breakeven numbers were pricing in 2.37% inflation at the end of Q1, its highest level since April 2013.1 The Fed’s commitment to low rates amid elevated unemployment, increased consumer spending with the re-opening economy and fiscal stimulus, and a supply chain that can’t keep up with accelerating demand could jolt inflation beyond the 2% marker in Q2. Biden’s proposed $2.25 trillion infrastructure plan could further push inflation above 2% for an extended period if it is passed by Congress in 2021. For context, the US GDP is $21.5 trillion, so the infrastructure package is a meaningful source of stimulus.2

Breakeven rate is the difference between the nominal yields and the inflation protected bonds of the same maturity.

But while inflation may further increase from here, we believe it’s unlikely we’ll see prolonged periods of high inflation like the 70’s and 80’s. One reason is that labor markets tend to not move as fast in recoveries as they do during downturns. U-6 unemployment stands at 10.7% today, an improvement from the 22.9% peak figure in April 2020, but still well-above the February 2020 pre-pandemic number of 7.0%.3 This means there is still substantial slack in the labor market, which is a headwind for inflation. In addition, the US government recently passed its third round of stimulus, but how consumers are using their stimulus checks should give inflation mega-bulls pause. 52% of those receiving stimulus checks from February 17th to March 1st used it mostly to pay down debt, and another 19% mostly saved it. Only 28% spent their stimulus checks, according to the US Census Bureau. Therefore, stimulus checks are not creating the surge in consumption that headline numbers suggested.

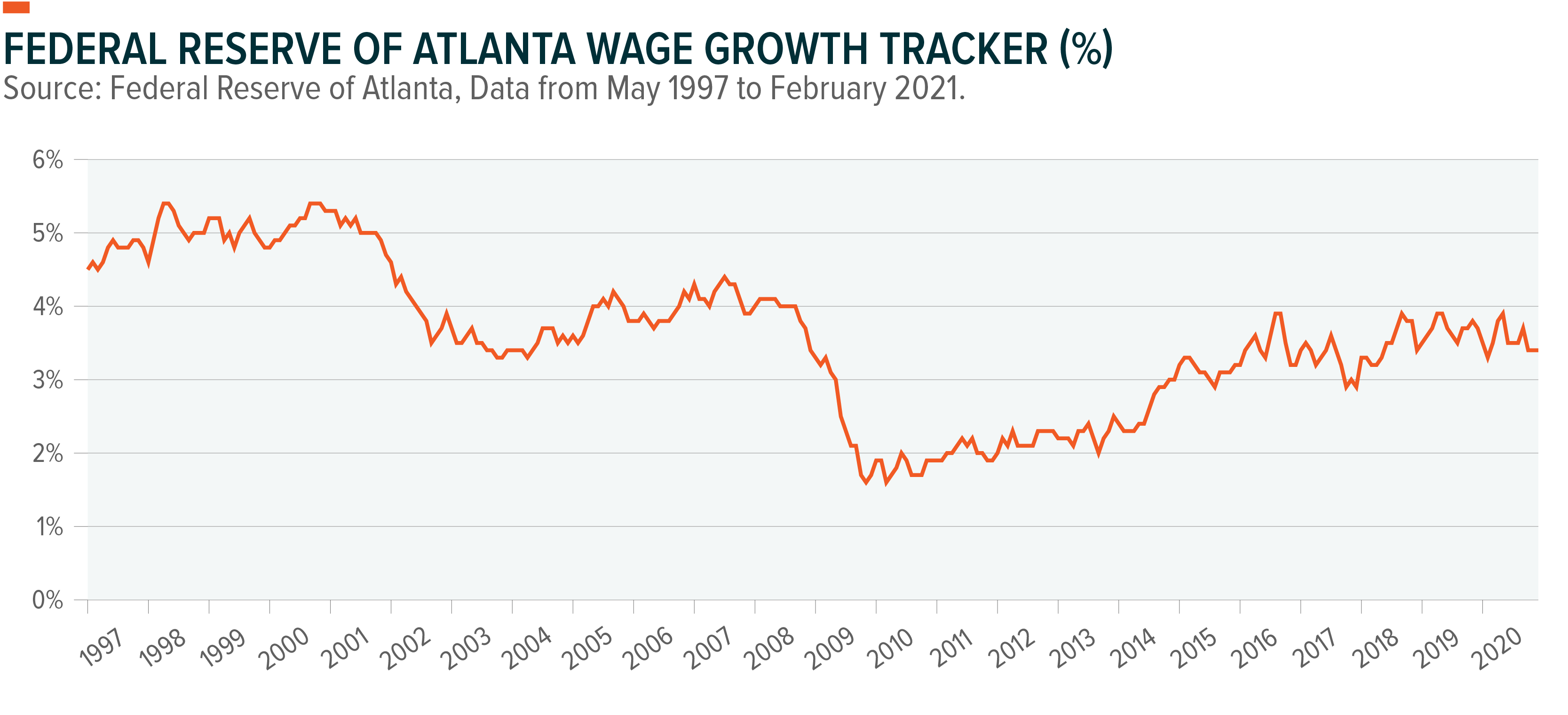

Wage growth even over longer periods hasn’t changed much either, which might explain some of the consumer behavior explained previously. The Federal Reserve of Atlanta’s wage growth tracker shows inflation has stayed fairly range-bound over the better part of the last five years. Wage growth rose since the financial crisis, but hasn’t reached levels seen in prior cycles partly due to technological innovations. The Biden administration’s proposal to raise the corporate tax rate from 21% to 28%, and closing corporate tax loopholes may add to these labor market pressures further. Considering consumption represents 68% of GDP, a much stronger labor market would be needed to push significant inflation into the system.4

Fed Chair, Jerome Powell, believes inflation could be higher, but not uncontrolled, as well. In March, Powell stated the Fed expects inflation to hit 2.4% in 2021, but for the move to be “transient”. Hence why the Fed is in no rush to raise interest rates through 2023. Their 2021 GDP growth expectations rose from 4.2% in December to 6.5% in March, but growth globally is still playing catch up. China has set its 2021 GDP growth target at 6%, at the low end of its 6-6.5% target from previous years. Europe stands in stark contrast to the rest of the world in its COVID-19 progress. France just entered its third national lockdown, and most of Western Europe is either in lockdown or restrictive activity mode. This implies that inflation should remain muted as consumer spending remains reigned amid continued lockdown measures.

Overall, we believe inflation is likely to rise above recent norms, but not enough to cause a hyperinflationary environment. Investors should prepare themselves instead for a reflationary period where elevated inflation is coupled with strong economic growth.

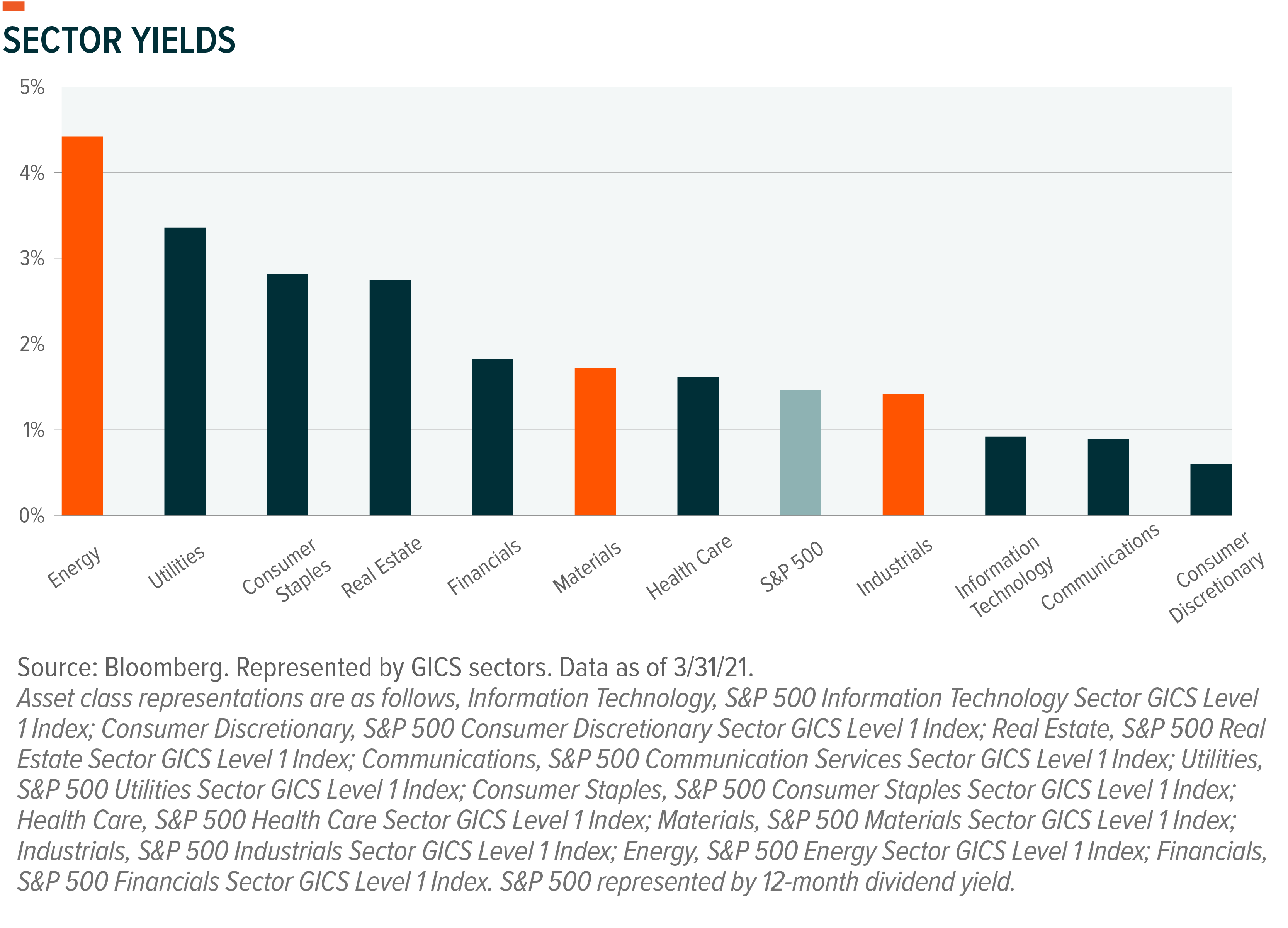

90% of Americans will be eligible for vaccines by mid-April according to President Biden, a landmark announcement. Current projections show all adults in the US will be vaccinated by July 4th. With widespread vaccinations, offices, businesses and schools can fully re-open, and consumers can resume in-person activities like dining out, travel, and attending events. Cyclical sectors like Energy, Materials, and Industrials are among the best positioned for this development. Energy prices are already rising as the re-opening economy takes effect and demand for oil increases. Materials stocks should get a boost from rising input costs, increased industrial activity, and more importantly Biden’s potential $2.25 trillion infrastructure bill. Materials and Industrials companies, like construction and engineering firms, would be direct beneficiaries of this proposed package. These companies typically don’t offer high yields like the Energy sector, but offer investors a total return strategy with market-level yield potential.

Favoring Credit Over Duration Amid Reflation

Longer-dated bond yields rose materially in Q1 with 10-year treasury yields rising 83 basis points, and we expect choppiness in the yield curve to continue this year. For investors, the risk of rising inflation makes duration-sensitive assets like long term bonds a difficult proposition. Instead, we favor overweighting credit risk versus duration in this type of reflationary environment. Credit spreads are likely to remain tight with supportive Fed policy and an expanding economy.

Preferred stock is one way to implement this tilt. Preferreds offer a duration of 4.6 years and the average credit rating of the ICE BofA Diversified Core U.S. Preferred Securities Index is BBB-, putting them just inside the investment grade realm.5 Preferred issuers are also 61% weighted towards financial institutions, which should benefit from rising rate environments.6 This could potentially offset some of the duration sensitivity in the actual preferreds themselves. Preferreds were only down -0.27% in Q1 compared to -3.37% for the broader bond market, and -4.65% for investment grade corporate bonds.7 Variable rate preferreds are another option to gain exposure to credit but potentially reduce duration further. Variable rate preferreds offer a duration of 2.5 compared to 4.6 at the broader preferred level.8

Technology Sector Positioning

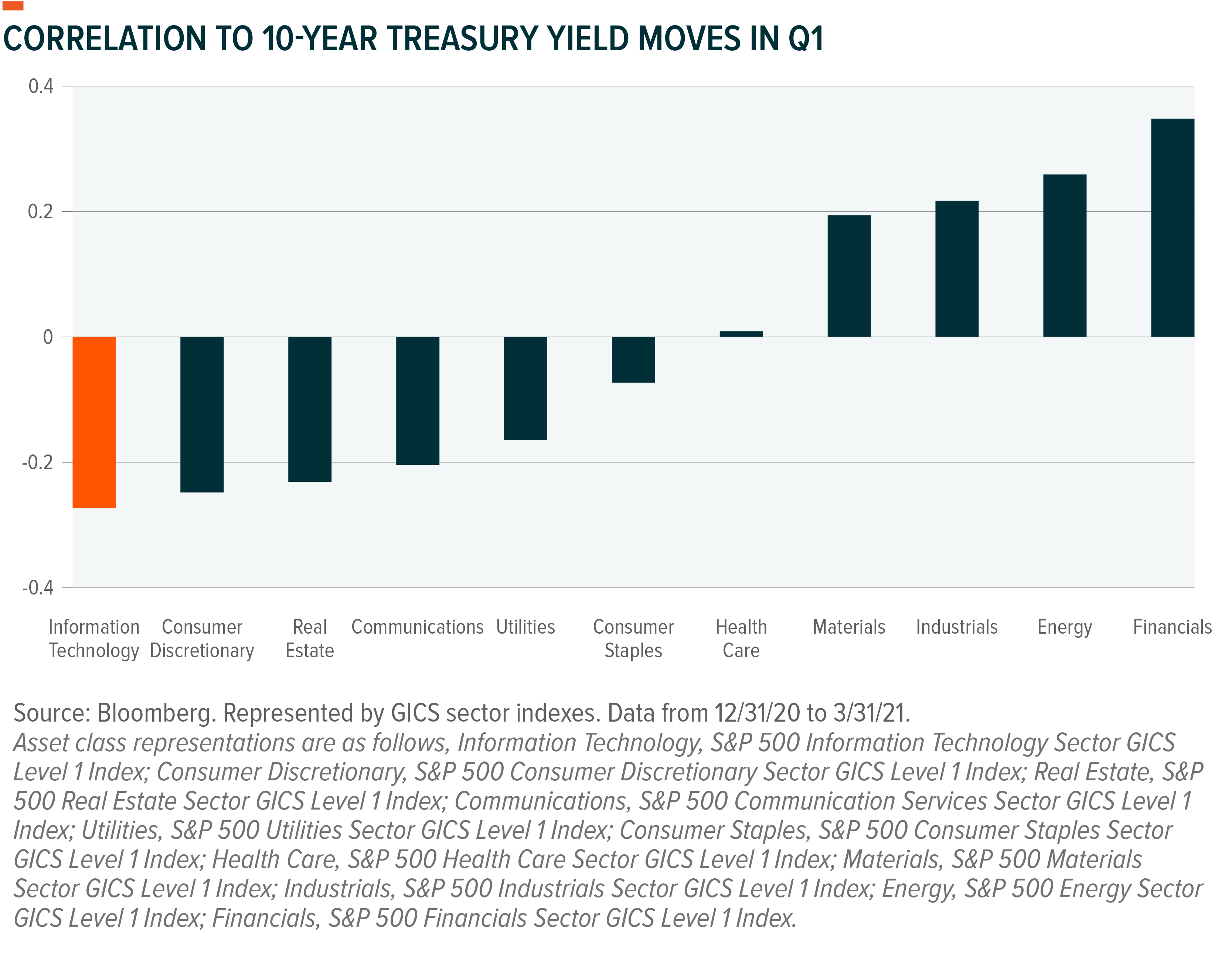

2021 is proving to be more challenging for the Information Technology sector than in the recent past. The sector’s returns flirted between negative and flat for most of Q1. Profit-taking, the re-opening economy, and rising bond yields are all presenting headwinds for the sector following a phenomenal 2020. The IT sector this year has displayed an acutely negative correlation to bond yield moves. IT’s correlation to daily 10-year bond yield moves in Q1 was -0.27.9

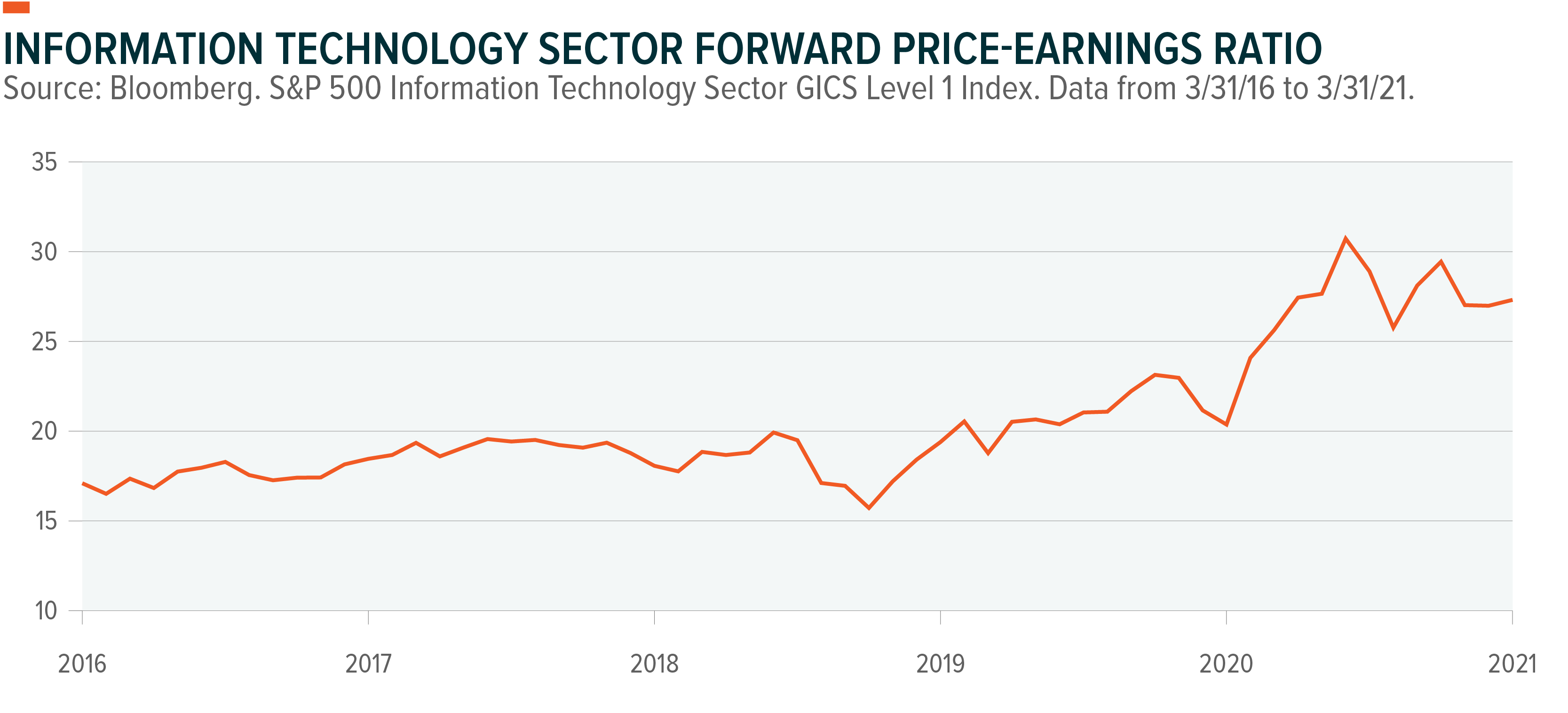

Recent weak IT performance is in spite of the fact that valuations are comparable to the second half of 2020, if not cheaper, indicating profit-taking and/or rotation trades.

Should the shift from growth to value continue and Tech names remain choppy, selling call options on the Nasdaq 100 could help monetize the sector’s sideways returns. Covered call strategies on the Nasdaq also add another source of potential returns to income portfolios, which traditionally are underweight the Information Technology sector.

Conclusion

The global economy is on a stronger footing, and the effects of the pandemic are beginning to subside, but income investors need to be careful with their exposures. Inflation is rising moderately and that is having a substantial impact on longer dated bonds. Cyclicals and small caps are faring well, but fixed income and Tech may need more nuanced approaches. Hybrid securities like preferreds, options strategies like covered calls, and inflation-insulated sectors like Energy should all be considered for income portfolios today.