Global X Research Team

Global X Research TeamThe Global X research team updated the Scientific Beta Factor Report for Q3 2018, analyzing the performance and characteristics of factors in the US and international markets. The full Q3 Factor Report can be read here.

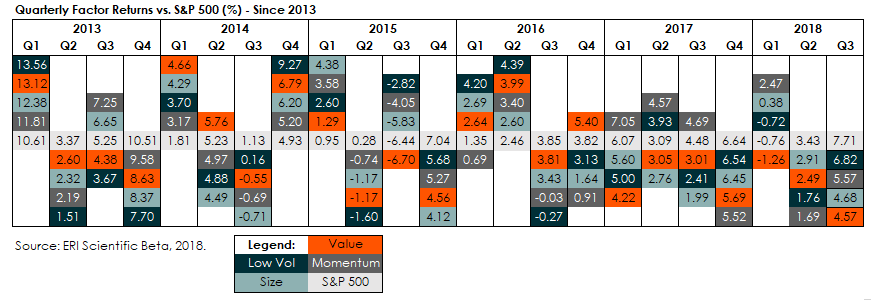

United States: Muted Factor Returns

In Q3 2018, factors generally lagged the S&P 500 after a tough period of factor performance in Q2. Despite all factors having positive performance for the quarter, each underperformed the S&P 500 by an average of 230 basis points (bps).

The Technology-heavy S&P 500 outperformed the Global X Scientific Beta US ETF (SCIU) for the quarter. The Technology sector has been the largest driver of returns for the S&P 500 this year, which has negatively affected SCIU given its 6% underweight to the sector relative to the S&P 500.

Value index represented by the Scientific Beta United States Value Diversified Multi-Strategy Index. Momentum represented by the Scientific Beta United States High-Momentum Diversified Multi-Strategy Index. Size Index represented by the Scientific Beta United States Mid-Cap Diversified Multi-Strategy Index. Low Volatility represented by the Scientific Beta United States Low-Volatility Diversified Multi-Strategy Index.

International: Factors Outperform in Europe & Asia Ex-Japan

In the international markets, factor performance remained mixed. The Asia ex-Japan region had better success amid its down market, with three of the four factors outperforming their broad market benchmark, the MSCI Pacific ex-Japan Index. Europe and Japan saw factor performance become more split, with two of the four factors underperforming in Europe and three of the four underperforming in Japan.

In Asia ex-Japan, three of the four factors outperformed the benchmark MSCI Pacific ex-Japan Index. Low Volatility had the largest outperformance by 331 bps, Value outperformed by 89 bps, and Size outperformed by 47 bps. Momentum was the lone underperformer by 76 bps.

In Europe, Momentum and Low Volatility outperformed the STOXX Europe 600 Index. Low Volatility outperformed by 102 bps and Momentum outperformed by 41 bps, while Size underperformed by 148 bps and Value underperformed by 55 bps.

In Japan, all factors except Value underperformed the MSCI Japan Index. Value outperformed by 98 bps, while Size underperformed by 216 bps, Low Volatility underperformed by 195 bps, and Momentum underperformed by 102 bps.

For Fund performance, please click on the fund ticker: SCIU, SCID, SCIX, SCIJ