Evolving supply and demand drivers helped to push copper prices to all-time highs in 2025, despite trade related volatility and weak demand from traditional, cyclical sources. Looking at 2026, we see a strong fundamental backdrop for the metal, with macro tailwinds likely aligning with the structural copper story. Against this backdrop, copper, and particularly copper miners, could be an effective allocation to capitalize on the long-term benefits of portfolio diversification that commodities have historically provided.

Key Takeaways

- Copper’s evolving supply and demand drivers helped propel the metal to all-time highs in 2025.1

- Copper prices proved resilient in 2025 despite the trade policy related volatility.2

- Both macro and structural factors underpin our bullish outlook as we begin 2026.

Copper’s Evolving Investment Thesis on Display in 2025

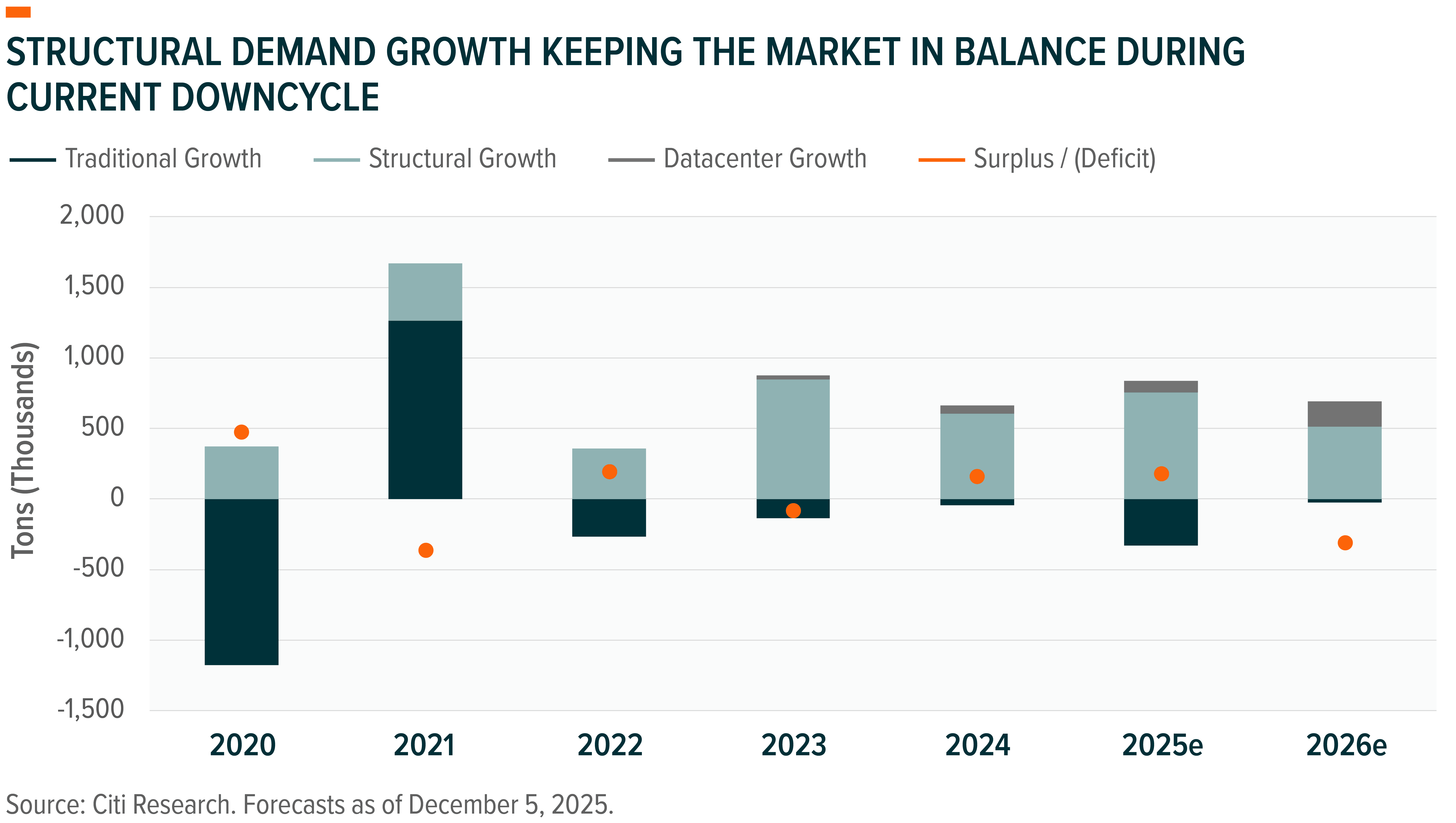

Copper’s performance in 2025 reinforced the strength of the metal’s changing investment thesis: even as traditional cyclical demand remained weak, copper’s increasing importance in enabling global structural megatrends and the deteriorating supply outlook helped keep the market firmly supported. High interest rates, a weaker fiscal impulse, and trade policy uncertainty have all weighed on global industrial and manufacturing activity since the post-covid boom, evidenced by traditional, more-cyclical demand for copper being flat since 2021.3 However, prices have remained well above the cost of production throughout this economic cycle, coming in contrast to both copper’s history and the present reality of other industrial metals, such as nickel. This is due to more forward-looking demand absorbing all incremental mine supply. This dynamic illustrates copper’s evolving investment thesis, placing both the metal and its producers in a unique position in the traditional commodity space.

We see copper demand becoming increasingly structural over time, with consumption from megatrends, such as electrification and artificial intelligence, set to continue growing strongly. These structural forces should therefore account for a larger share of total copper consumption, potentially helping offset the impact of stagnation in cyclical sectors and offering copper prices a layer of downside protection. At the same time, supply remains constrained: delays in new project ramp-ups, aging assets, declining grades, underinvestment, rising jurisdictional risks, and weather-related disruptions continue to limit production growth. This evolving supply dynamic presents a compelling long-term trend that could support higher prices. However, we don’t expect copper to fully detach from the economic cycle, given that over 80% of total demand remains tied to more traditional and cyclical sectors.4 Rather, we see copper’s trading range moving higher, with the metal likely to remain above the cost curve throughout a normalized business cycle. This dynamic is very beneficial for current producers of the metal. Miners are positioned to not only generate higher levels of cash on an absolute level, but we also expect them to be profitable throughout a normalized business cycle, which should support capital allocation budgets, limit balance sheet risks and, in our view, warrant higher multiples.

Trade Policy Created Short-Term Volatility in 2025

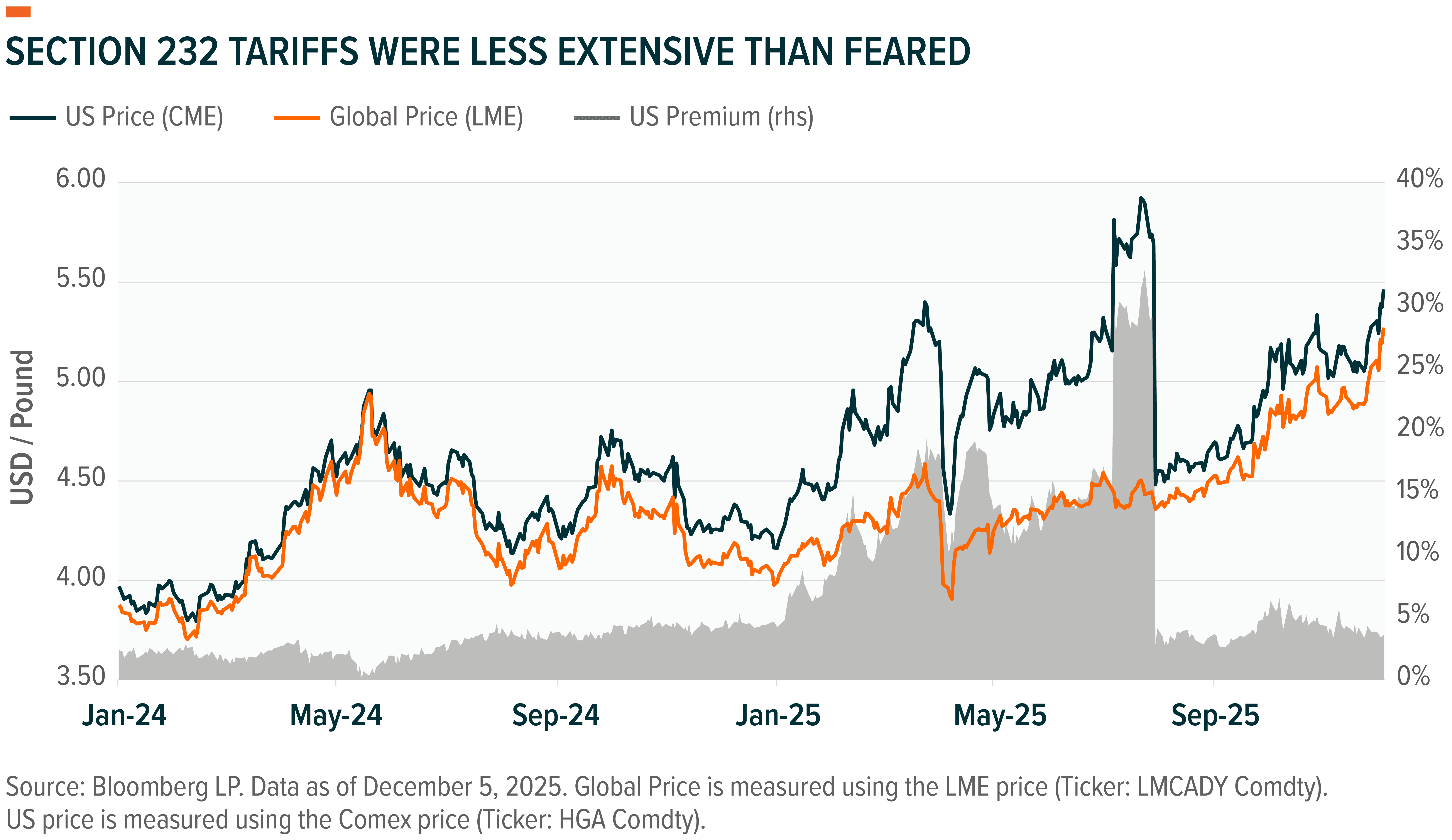

Tariffs greatly impacted the copper market in 2025, creating a more volatile and complex trading environment while also supporting prices during a period of weaker economic growth. The first impact came with the April tariff announcement, which weighed on U.S. and global growth expectations. Although ultimately proving incorrect, these heightened recession fears weighed on investor sentiment towards more cyclically tied assets, including Dr. Copper. The uncertainty around the Section 232 tariffs also had an impact on markets, not only causing the U.S. price to trade at a large premium to the global benchmark, but it also supported the global market itself, with inventories in LME (London Metal Exchange) and Chinese warehouses declining as U.S. buyers stockpiled the metal. This market dynamic resulted in the COMEX premium rising to a high of 33% versus the global benchmark price (LME), implying that all copper imports would be subject to a significant tariff like steel and aluminum.5 However, the Section 232 investigation proved far less rigorous than the market expected, causing the COMEX price to effectively erase its entire premium to the LME price in one trading day, with the U.S. price falling 27% on July 31st alone.6 Global copper prices remained resilient despite this shock, with fears over the reversal of flows overblown as U.S. stockpiles proved stickier than expected after the U.S. Government reclassified the metal as a Critical Mineral. The U.S. copper price premium and still elevated U.S. inventories reflect speculation that further levees could emerge. However, the small size of the premium limits our perception of the potential risk in the short term. We find it notable that despite this market volatility, copper’s price rose over 30% on the year to all-time highs, underscoring the metal’s increasing resilience in the face of macroeconomic headwinds.

Fundamentals Keep Us Positive Heading into 2026

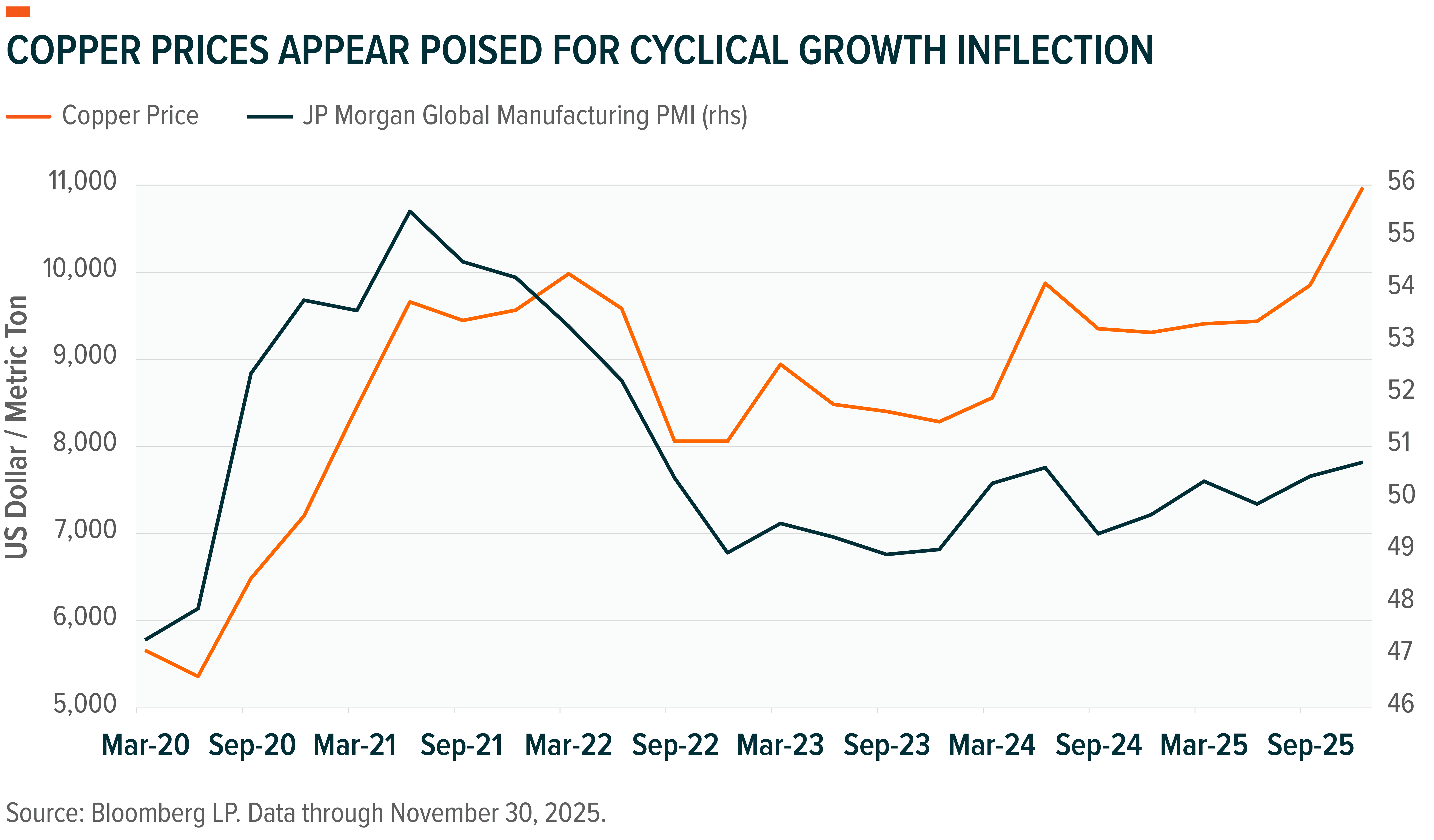

Despite copper prices rising to all-time highs in 2025, we see a strong fundamental backdrop heading into 2026, with macro tailwinds aligning with the structural copper story. We see the macro backdrop as favorable for copper and hard assets in general, with easier monetary policy from the Federal Reserve and a positive fiscal impulse helping support the demand growth outlook. A more dovish FOMC could also add to the U.S. dollar weakness seen in 2025, potentially benefitting hard assets like copper while also providing global central banks more room to ease monetary policy in order to boost domestic growth. Beyond these macro tailwinds, we expect demand for electrification to remain robust, with the artificial intelligence datacenter buildout continuing to grow very quickly as AI becomes an important force driving incremental demand. Copper mine supply growth should also remain low in 2026, with limited new projects expected to come online during the year, while Cobre Panama and Grasberg volumes remain either offline or well below previous estimates. All in all, we don’t expect to see a robust demand recovery like in 2021. Rather, we see the potential for a modest recovery pushing the copper market into deficit, which should in turn support copper prices.

Conclusion: An Increasingly Structural Thesis Meets a Cyclical Opportunity

We believe copper’s investment thesis has materially changed, with the evolving supply-demand dynamics likely pushing the metal’s trading range structurally higher over time, which would greatly benefit current producers of the metal. Copper’s rise to all-time highs in 2025 showcased the metal’s increasing resilience, with quickly growing structural demand and weak mine supply growth offsetting cyclical demand stagnation. Looking ahead in 2026, we see a mix of fundamental and macro factors driving the market into a modest deficit, which could potentially further support prices. Beyond copper, we see persistent inflation, rising sovereign debt levels, and worsening demographics highlighting the important role hard assets, such as commodities, play within a portfolio. Yet not all commodities are the same, underscoring the need to allocate to goods with more favorable long-term backdrops. In this context, copper and particularly copper miners, stand out to us as an effective allocation to capitalize on the long-term benefits of portfolio diversification that commodities have historically provided.