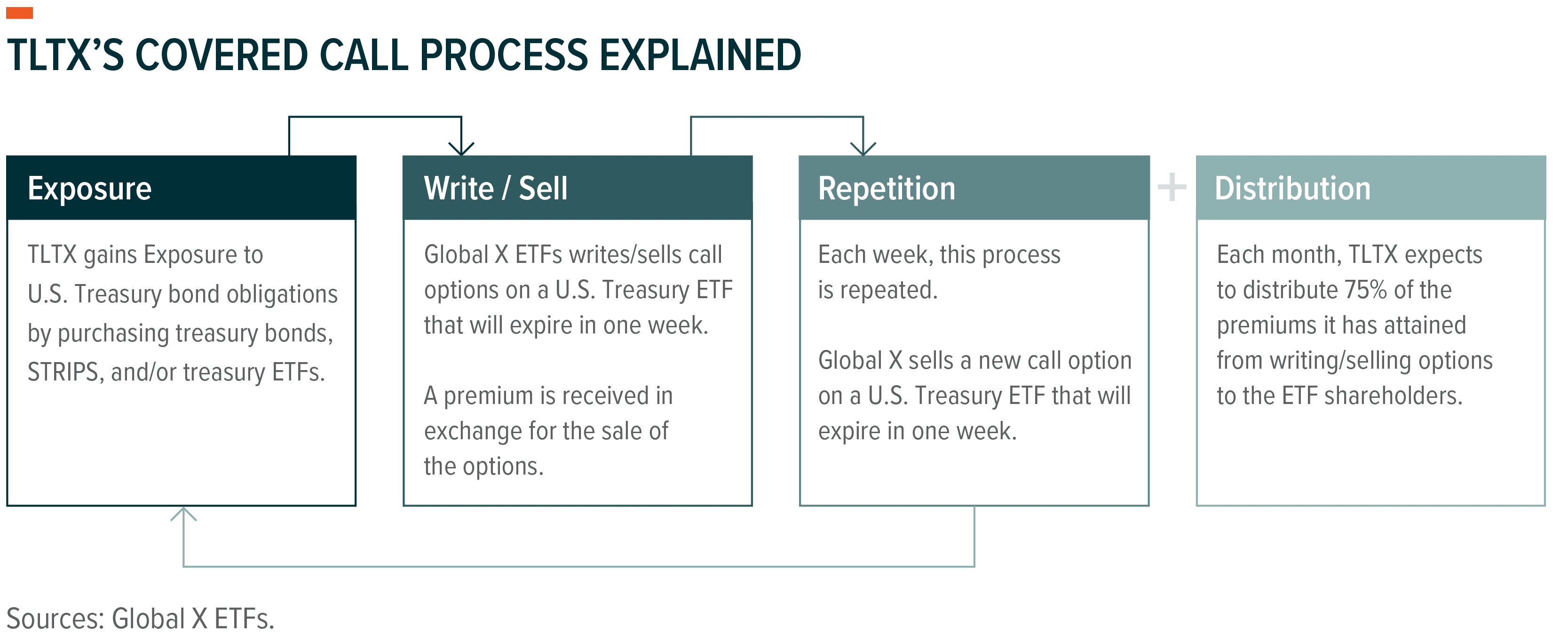

On July 16, 2025, we listed the Global X Treasury Bond Enhanced Income ETF (TLTX) on the Cboe BZX exchange. TLTX seeks to offer investors exposure to the long end of the treasury yield curve while writing weekly call options on long-duration treasury ETFs. The fund aims at writing call options at a value equal to a portion of its notional holdings, in an attempt to provide access to a portion of the price appreciation potential of long-duration treasuries. Meanwhile, it is designed to harvest option premiums as a potential source of income.

Investors have long sought to incorporate treasury exposure into their portfolios. It offers a perceived means of safety being backed by the full faith and credit of the U.S. government, a tax-efficient source of income with exemptions common at state and local levels, and yield potential, which, as of late, has risen to levels not seen for the better part of the last decade. Historically, when investors have looked to enhance the yield associated with these positions, they’ve sought to increase bond duration by moving further out on the yield curve. While longer-duration Treasuries can offer this enhanced yield potential, they also have the potential to carry higher volatility, given their heightened sensitivity to moving interest rates.

The Global X Treasury Bond Enhanced Income ETF seeks to allow investors to maintain exposure to this higher-yielding segment of the curve, while potentially mitigating associated volatility through monthly distributions.

Key Takeaways

- The Global X Treasury Bond Enhanced Income ETF is a systematic active strategy that offers access to a portfolio of treasury securities while writing weekly call options to pursue premium distributions and manage interest-rate sensitivity.

- The measure of volatility that long-duration treasury securities tend to display may be a deterrent for some investors. TLTX seeks to monetize this volatility by engaging in call option writing.

- TLTX’s active management team writes weekly call options and maintains discretion over particular functions of the options roll process to seek superior premiums.

TLTX Aims to Address Challenges Facing Income Investors Through a Covered Call Strategy

Within treasury markets - where most instruments share similarly high credit ratings - the positive relationship between yield and duration is evident (i.e., longer durations generally produce higher yields). The relationship holds true across other fixed income asset classes, as well, but when looking at the broader bond market, investors generally have two options when they want to boost yield potential: increase duration or invest further down on the credit-quality spectrum.

Each approach presents distinct trade-offs. Extending duration may expose investors to greater volatility through heightened interest rate sensitivity. Conversely, accepting lower credit quality may result in less volatility relative to long-duration instruments, but it introduces higher default risk as credit quality deteriorates. The Global X Treasury Bond Enhanced Income ETF (TLTX) seeks to address this challenge by allowing investors to take share in the long end of the treasury yield curve, while seeking to mitigate interest rate sensitivity through the writing of weekly call options. The fund employs a systematic active strategy, but at large it will see the fund hold long positions in a basket of treasury securities with an approximate 20-year duration target, while writing weekly call options, in succession, in an effort to manage volatility associated with the position by cushioning downside price movements with option premiums. The fund is expected to perform monthly distributions, valued at approximately 75% of the weekly premiums it collects. Returns generated by the fund may also be enhanced by the underlying treasury securities that it fund holds.

Long-Duration Treasury Volatility Creates Opportunity to Source Better Premiums

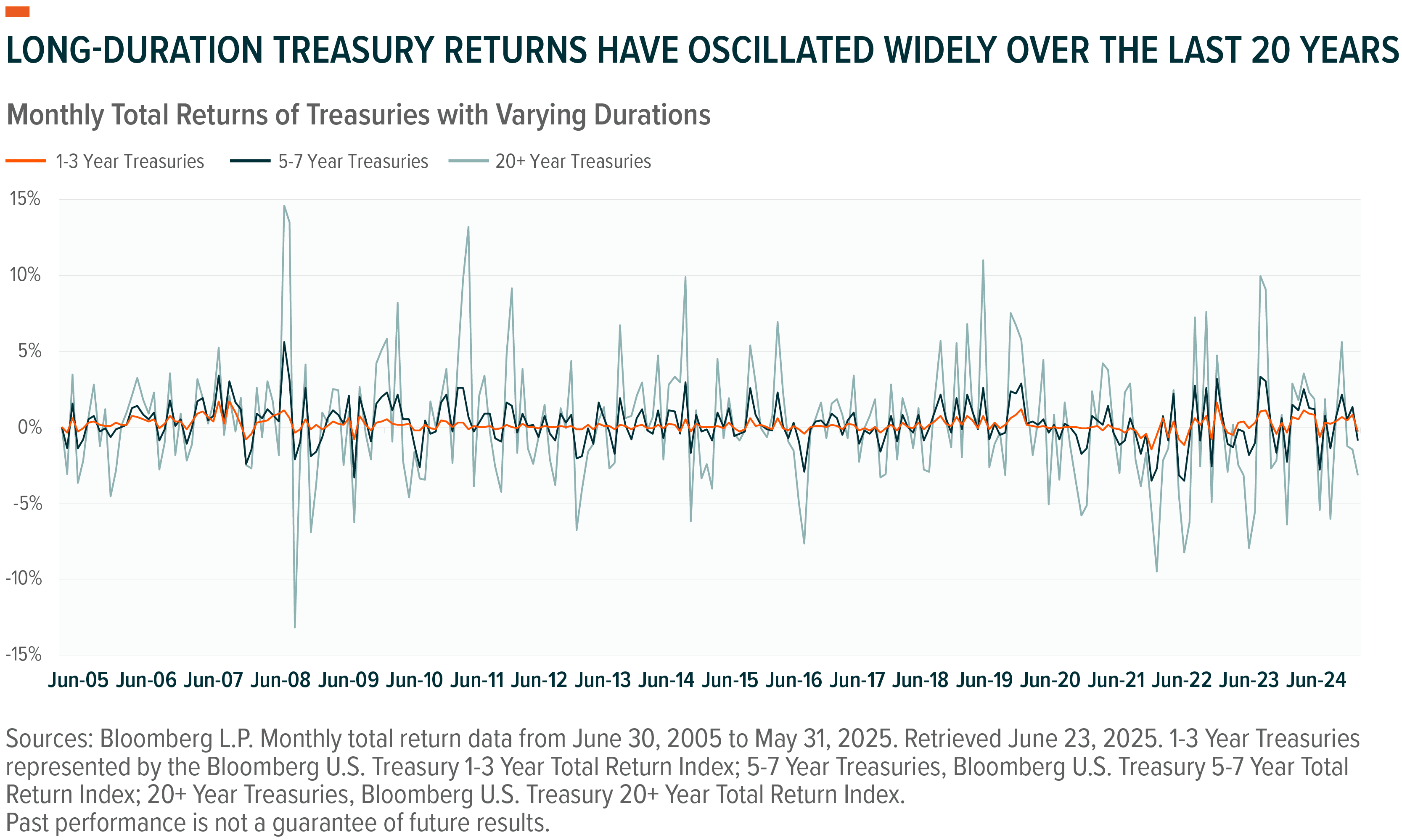

Interest rates and economic uncertainty have the potential to influence the value of treasury securities, and their impact can be even more emphatic at the long end of the curve. This stems from the understanding that bond values are derived from the present value of their future cash flows. Meaning that if the market growth is expected to be healthy for the foreseeable future, the value of a bond’s predetermined coupon payments may prove less impactful than if the market was assuming a weak or negative growth trajectory. That type of environment would likely result in more spending power to the coupon payments provided by the bond. And because long-tenored bonds offer more coupon payments, and more of those payments take place much further out into the future, the influence of interest rates and economic uncertainty tend to have a stronger effect on these longer-dated securities. The level of sensitivity that these long-duration instruments have to changes in the market outlook, among other factors, can be examined by looking at the deviations between monthly total returns provided by 20+ year treasuries over the last 20 years, relative to shorter-duration instruments.

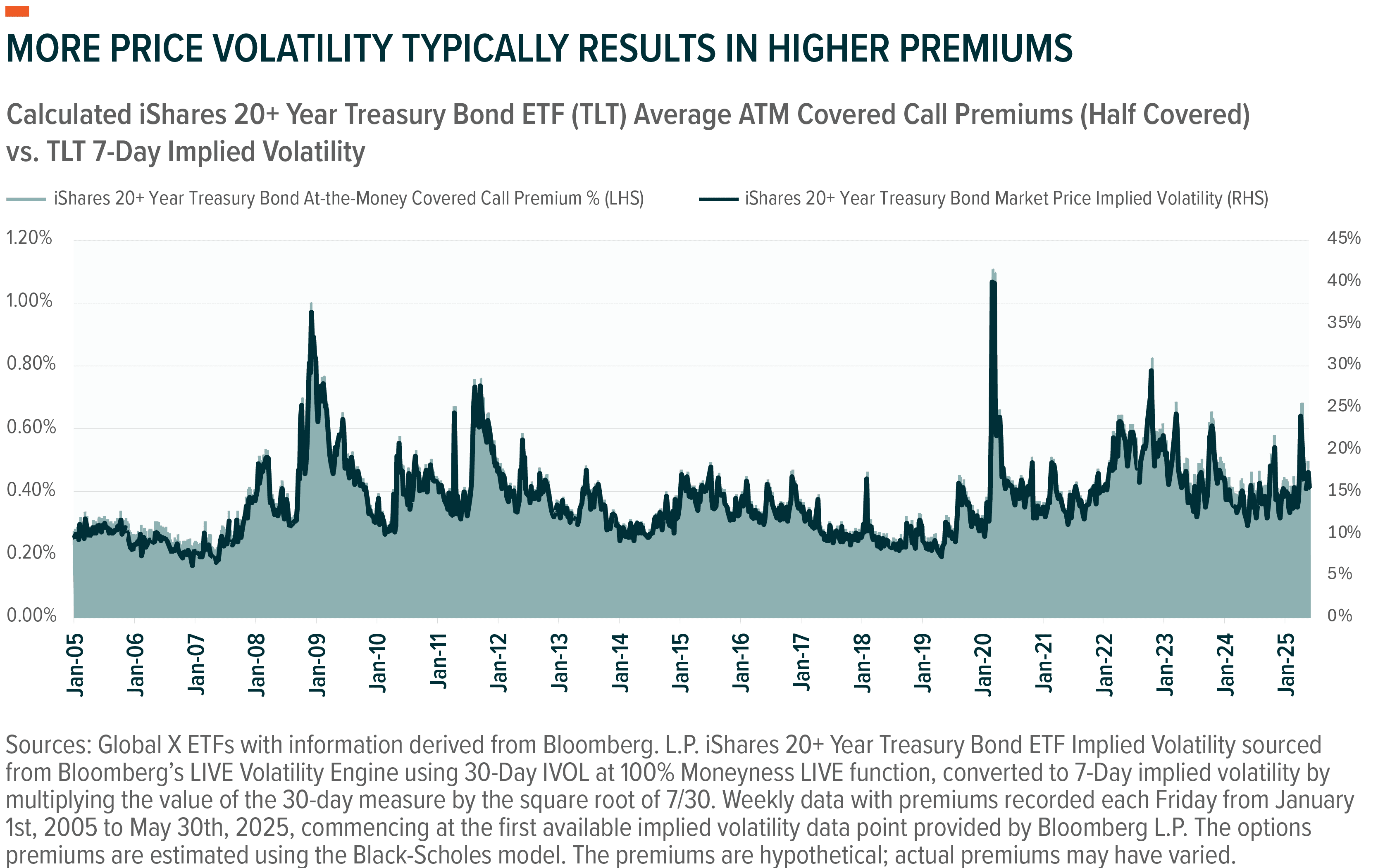

This volatility dynamic creates an interesting opportunity, as volatility typically correlates positively with option premiums. To examine this relationship further, the chart below uses a Black-Scholes1 option pricing model using a weekly call writing strategy on the iShares 20+ Year Treasury Bond ETF (TLT). The analysis clearly demonstrates that higher asset volatility generates correspondingly higher option premiums.

The Global X Treasury Bond Enhanced Income ETF leans into this relationship and the elevated volatility characteristic of long-duration treasury instruments. It also seeks to keep a portion of its portfolio unencumbered by the influence of written call options to retain price appreciation potential should the value of its underlying treasuries rise. When operating a covered call strategy, the strike price at which the call option can be exercised sets a cap on the upside potential that can be realized by holding the underlying security. By writing the call on only a portion of its portfolio, however, TLTX keeps a measure of the portfolio’s upside uncapped, making the fund a potential total return solution.

A critical consideration by TLTX is that notional option coverage is not determined by the fund's total asset value, but rather by a strategic coverage ratio. The fund typically maintains notional coverage equivalent to approximately half its duration exposure. Since bond prices typically share a negative relationship with interest rates, we expect writing call options at a notional value that represent half the fund’s duration will capture roughly half the upside potential of its Treasury holdings when interest rates are on the decline while collecting option premiums. On the other hand, when interest rates are on the rise, the fund remains exposed to the full downside of its Treasury positions, with option premiums providing a partial offset.

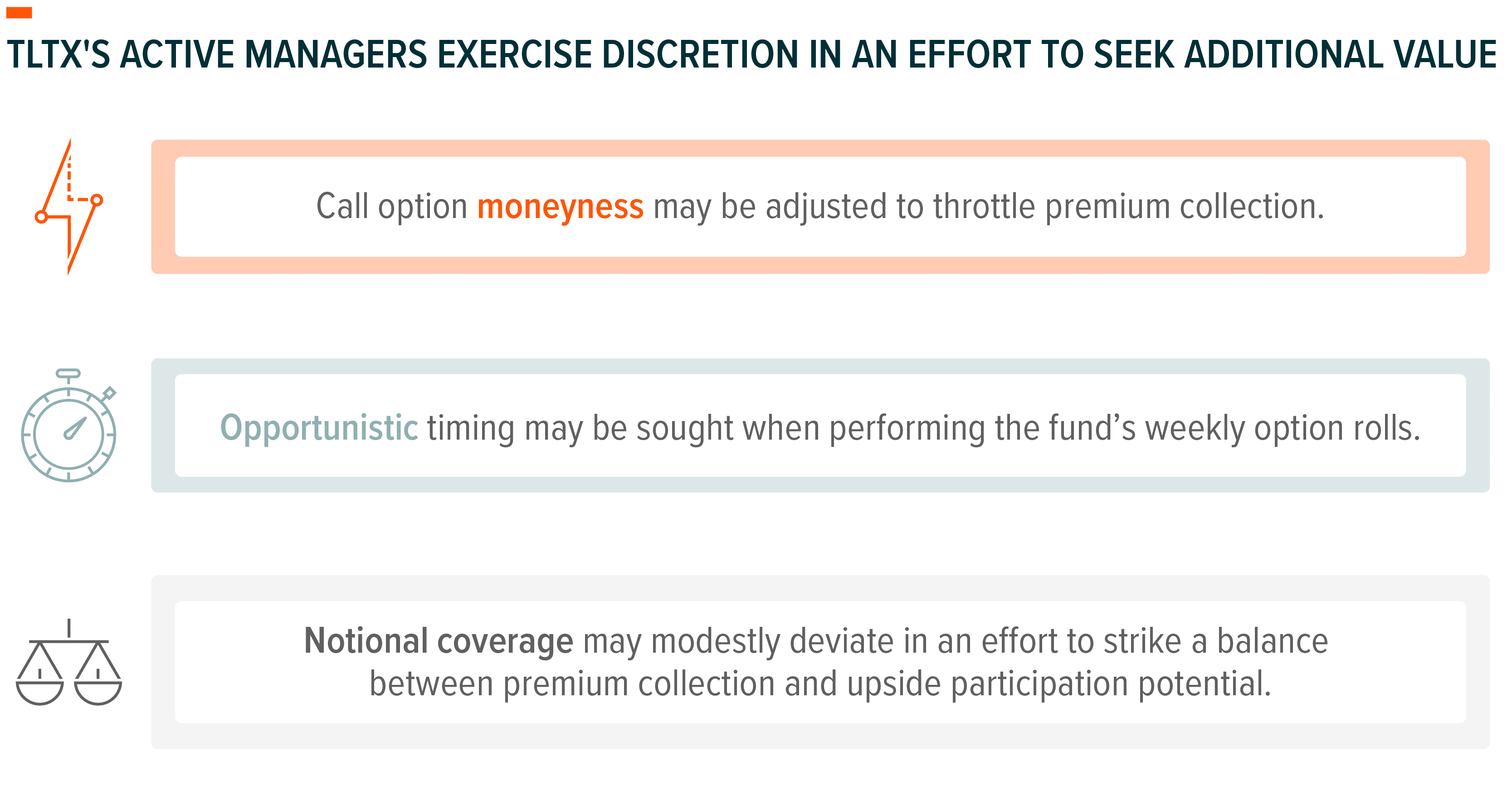

TLTX’s Active Management Team Has Discretion to Seek Opportunistic Pricing and Coverage

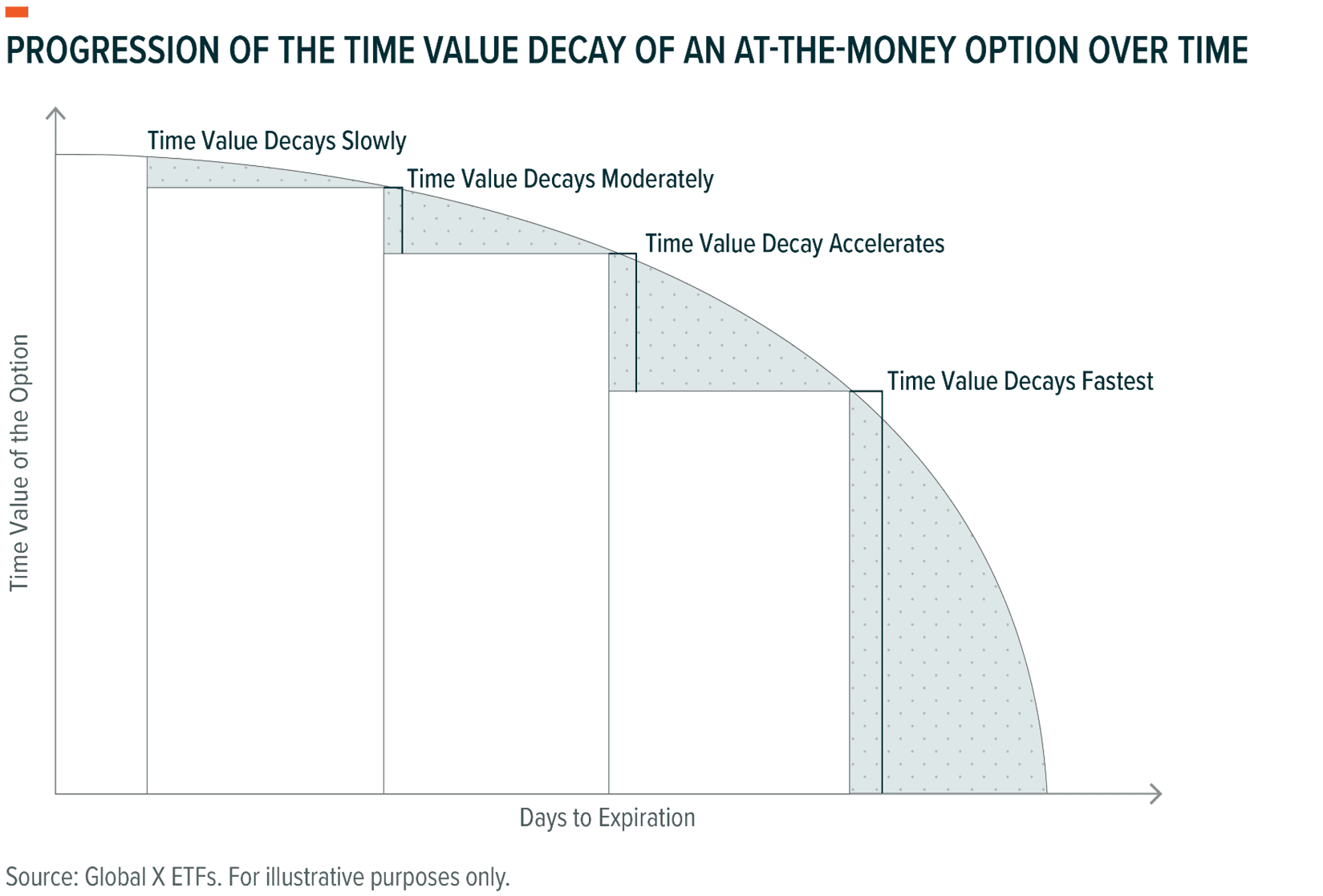

Many of the functions of TLTX’s investment strategy could be deemed deliberate and systematic. For instance, the fund seeks to utilize weekly call options with consistency as opposed to longer-dated options in an effort to attract higher annualized premiums. This rationale stems from option contracts typically losing value more rapidly the closer that they get to expiration. As a function of this more-rapid time value decay, the seller is typically afforded more generous premium compensation when transacting the trade. Thus, by selling short-term weekly options in succession rather than longer-term options the fund can potentially capture this accelerated decrease in value more efficiently.

Outside these systematic functions, however, the fund’s active portfolio managers are granted the flexibility to perform their trades utilizing varying levels of moneyness and notional coverage, while seeking opportunistic timing in an effort to manage risk and seek out advantageous pricing. The call options that are being written by TLTX are expected to have strike prices that are only slightly out of the money, and the degree of notional that is covered is expected to remain relatively consistent at around half the portfolio’s duration. However, having the flexibility to actively govern these factors may open up the opportunity to enhance returns.

Conclusion: TLTX May Enhance Income Potential Associated with Long-Duration Treasuries

Treasury investment returns fundamentally depend on the interest rates investors can capture from these instruments. The Global X Treasury Bond Enhanced Income ETF seeks to enhance this income potential by systematically writing call options. The premiums received from writing the options can help buffer against capital losses in environments when interest rates rise, or act as a supplement to the returns of a basket of long-duration treasury securities when the rate environment is static. The fund has the potential to be utilized as a single source of distributions, or as a pairing with a broader basket of treasuries to help manage volatility and maintain upside potential.

Related ETFs

TLTX – Global X Treasury Bond Enhanced Income ETF (TLTX)

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.