Global X Research Team

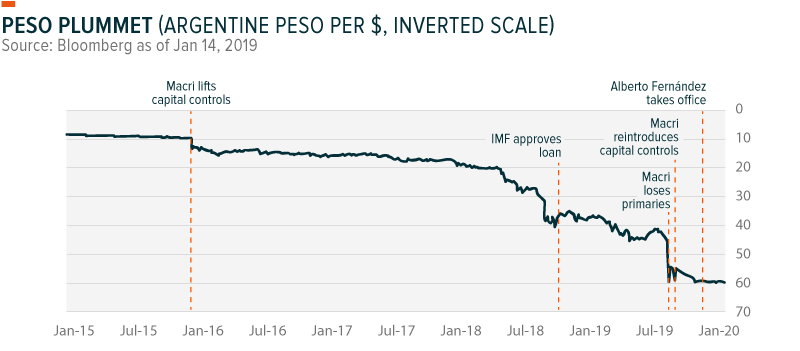

Global X Research TeamLast year, Argentine markets performed well until August, when former President Mauricio Macri’s poor results in the presidential primaries sparked a sharp sell off. The results correctly anticipated his loss in October and presaged the election of Alberto Fernández. The primary results sparked fears of a reversion to a populist regime under Fernández – igniting worsening economic conditions, a market rout, and a weakened peso.

Now it is up to Fernández to prove that he and his administration can reverse the economic recession, tame inflation, and steer Argentina clear of its ninth sovereign default.

This piece delves into challenges the Fernández administration will inherit, highlights policies his government is expected to prioritize, and provides a market outlook for investors with exposure to Argentina.

Fernández is not CFK 2.0

Following the primaries, concerns that Fernández would be a puppet figure for his running mate, former President Cristina Fernández de Kirchner (CFK), became prevalent. Serving as President before Macri, CFK imposed tight capital controls and populist policies, including the imposition of capital controls, export control on agriculture, and the infamous nationalization of Argentina’s largest oil and gas company, YPF.

Although Fernández served under CFK in the past, his ultimate resignation from her cabinet allowed him to join a more centrist faction of the Peronist party, where he openly criticized her policies. Fernández’s break with CFK, as well as his career and policy experience, suggests that markets may have overreacted, overestimating CFK’s influence on Fernández, and underestimating his more pragmatic approach. As Fernández strengthens his political alliances and forms a clear policy framework, investor sentiment may normalize.

Inheriting an Economic Crisis

Following his October 2015 election, the first half of Macri’s presidential term was met with exuberance as markets rallied to reach an all-time high in market capitalization by the end of 2017. But in 2018, Argentina suffered a severe drought, prompting a currency rout and an economic contraction, which pummeled markets, losing nearly a third of their value.

In 2019, a recovery seemed inevitable thanks to a record harvest season, strong domestic infrastructure investment, and higher global oil prices. Argentina also received its third installment of an IMF bailout, providing a buffer for the country to meet payments on maturing debt as it faced higher refinancing costs. Data from July showed a strong improvement in inflation and consumer confidence in 2019. Yet rather than building on these tailwinds, the election cycle reversed any progress as Macri fought to save his re-election campaign and Fernandez’s polling numbers reflected the inevitable election of a populist candidate.

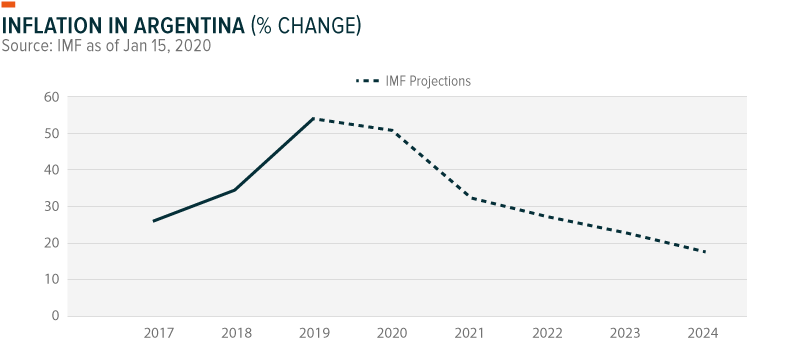

Now Fernández steps into office to preside over an economy that is expected to contract for a third consecutive year.1 Immediately, his administration and the country’s central bank must stimulate growth and reverse the recession, which has led to persistently high unemployment, inflation that’s still above 50%, and a severely weakened peso.

While the economy is fragile and sensitive to politics, a strong policy framework from Fernández could help to stabilize sentiment and bring the economy back on its trajectory prior to the elections.

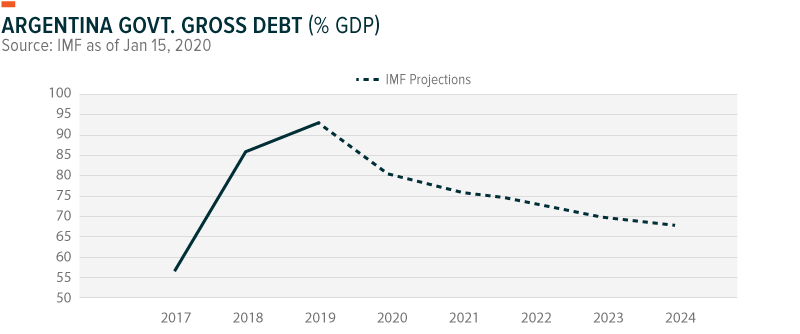

Some are already counting on it. The IMF projects that Argentina will return to positive 1.4% growth in 2021.2 Likewise, they project that sovereign debt as a percentage of GDP will fall towards the end of 2020.3 And they expect that employment to improve over the coming years, projecting that it will fall below 10% by 2022.4 But many of these projections are ultimately dependent on a variety of factors, with the efficacy of Fernández’s economic policies at the top of the list.

Fernández could score immediate creditability, particularly among international investors, by helping Argentina to meet $60 bn of debt payments due in 2020. In the same month Fernández took office, rating agencies Fitch and S&P downgraded Argentina’s sovereign debt to “restricted default” and “selective default” from CC and CCC-, after the country postponed payments on $9 bn of dollar-denominated debt. This was the second delay in five months and pushes payments out until next August. Martín Guzmán, the new Economy Minister, proposed further delaying payments, by as much as two years, to give Argentina ample time to restructure its debt while it manages debt loads that are expected to rise through 2021.

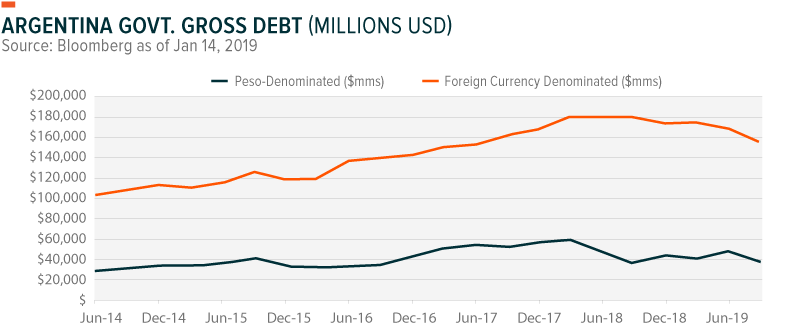

Over the course of his tenure, Fernández must guide Argentina away from its ninth sovereign default and oversee efforts by Guzmán, an academic specializing in debt negotiation, to manage Argentina’s credit and restructure Argentina’s roughly $332 bn of debt – including $101 bn of foreign currency denominated debt ($57 bn of which is from the IMF).

Breaking the Cycle of Inflation

To address Argentina’s runaway inflation, the Fernández team needs to use a combination of fiscal stimulus and responsive monetary policy that will require close coordination with the central bank and congress. So far, the administration has maintained price controls on staples, previously implemented by Macri’s government, and raised fixed-rates for pensioners and government employees.

Policy introduced in Argentina’s lower house focuses on encouraging production to tame prices, keep wages relatively stable, and break the cycle of inflation. It is unclear whether the proposal will pass through Congress, but the plan – which has roots in a similar policy from the 1970s – is described as a “social pact” between government, business and labor unions to control the inertia effect of inflation by encouraging production rather than raising salaries and price levels.

In December, the lower house also passed an emergency economic bill (“The Social Solidarity and Production Reactivation Plan”) aimed at raising more funds. The bill has yet to be voted on in the upper house, but in its current form would raise export taxes on grains, apply a 30% tax on purchases made abroad, and introduce taxes on property and assets held abroad by Argentines. The possibility of export controls may be disconcerting for the agricultural sector, given its history with and skepticism towards ‘temporary’ export controls. But if appropriately and only temporarily used, such controls could help bring down inflation and stabilize the peso.

Meanwhile, efforts from the central bank are focused on maintaining market stability, encouraging inflows of foreign capital, and expanding production capacity in key sectors. Aside from a focused intent on regulating the peso, the central bank announced that it expects to continue lowering rates to induce economic growth after higher rates under Macri proved ineffective at taming inflation.

Coordinated Efforts to Grow the Energy Sector Could Spur Growth

Concerted efforts from the central bank and judiciary may provide upside for the Energy sector. Since his time on the campaign trail, Fernández has been adamant about expanding production capacity and incubating growth in Vaca Muerta, which is home to the world’s second largest shale gas reserves.6 Miguel Pesce, the new central bank president, expressed support for such efforts and suggested that investors in Argentina’s energy sector may even receive favorable treatment, with energy firms potentially receiving exceptions from capital controls that would allow them to send dividends abroad. (Following policy introduced at the end of Macri’s term, firms must request permission to distribute dividends abroad.) Further progress is needed to develop Argentina’s broader Energy sector, but policy coordination could give Argentine energy firms the support they need to become more competitive.

Building a Pragmatic Cabinet

Fernández’s cabinet is an eclectic, but pragmatically-selected group, ranging from academics to career politicians, from CFK’s allies on the far-left, to her harshest critics closer to the center. Selecting cabinet members like Carlos Zannini or Eduardo de Pedro, who are on the far-left, could be a way for Fernández to ensure he has critical support of the large Kirchnerista camp. By balancing his cabinet with more centrist politicians and academics, like Matías Kulfas, who is an outspoken critic of CFK, Fernández may bridge gaps within the fractured Peronist party, and across party lines.

And although it is still too early to judge which policies Fernández will most aggressively pursue, his cabinet makeup suggests he uses a pragmatic and consensus-based approach to politics and policy, both of which are critical to enact the reforms that will spur an economic recovery.

Finding Growth Opportunities

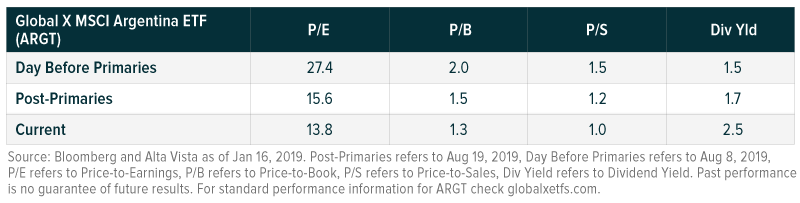

Valuations in Argentina continued to fall from pre-primary levels based on price-to-earnings, price-to-book, and price-to-sales metrics, resulting in significantly lower multiples. An economic recovery in Argentina could be a meaningful catalyst to push equity prices higher as valuations normalize to pre-primary levels.

Source: Bloomberg and Alta Vista as of Jan 16, 2019. Post-Primaries refers to Aug 19, 2019, Day Before Primaries refers to Aug 8, 2019, P/E refers to Price-to-Earnings, P/B refers to Price-to-Book, P/S refers to Price-to-Sales, Div Yield refers to Dividend Yield.

Past performance is no guarantee of future results. For standard performance information for ARGT please click here.

Conclusion

With Fernández now in office, surrounded by a carefully selected cabinet, a prudent and pro-growth policy framework must be put into place to stimulate Argentina’s economic recovery. Likewise, negotiations with the IMF and Argentina’s creditors must ensure that it meets its obligations to the international community. Markets may be reassured by the administration’s commitments to expand the Energy sector or its efforts to solidify trade deals with key partners in the EU and US. Investors should be attentive to Fernández’s approach to politics, but ought to form their longer-term outlook on the success of his policies to stimulate growth and incubate a sustainable recovery.

Related ETFs:

ARGT: The Global X MSCI Argentina ETF invests in among the largest and most liquid securities with exposure to Argentina.