Pedro Palandrani

Pedro PalandraniOften originating from tech-at-core companies residing outside of the traditional banking sector, FinTech firms are using their unique capabilities to enhance or transform financial services as we know it. Areas such as mobile payments, crowd-funding, blockchain and crypto currencies, peer-to-peer (P2P) and marketplace lending, finance and insurance software, and wealthtech, are many of the new applications for technology to disrupt the financial services space. In this piece, we explore some of the key drivers and developments in the FinTech space that are propelling this disruptive theme.

Key Points:

- Despite strong growth, overall penetration of FinTech remains low, leaving a large market to be disrupted

- FinTech M&A is on the rise, including four large deals valued above $10 billion just in 20191

- Global consumers have grown less reliant on cash, enhancing the growth profile of mobile payments firms

How Much has FinTech Grown?

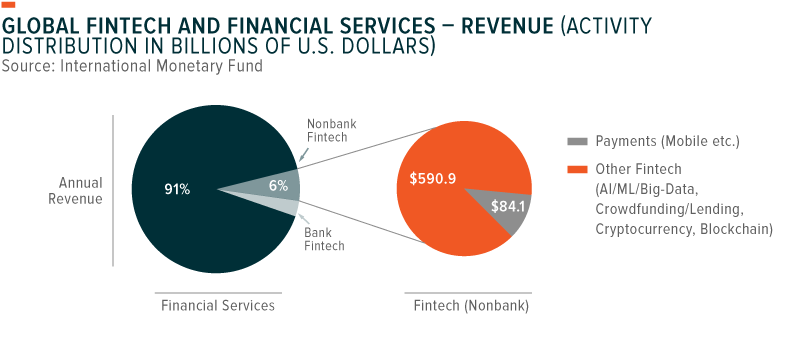

Currently, FinTech represents just 6%, or approximately $675 billion, of the total global estimated annual revenue for the financial services industry.2 In addition, a recent Global X survey of consumer adoption of disruptive technologies revealed that just 11% of consumers indicated that they use mobile wallets on at least a weekly basis, compared to 84% use of credit cards.3 This low penetration rate leads us to believe that this disruption should continue to exhibit long term secular growth over the coming decade as FinTechs continue to take market share from traditional financial services firms.

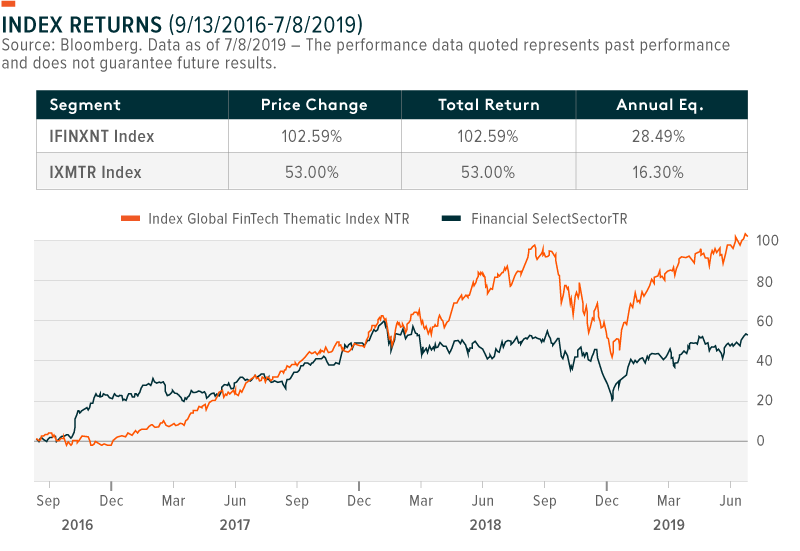

Despite the nascent nature of FinTech, many of these firms are experiencing significantly faster growth than their traditional financial services peers. This has been reflected in the performance of FinTech companies tracked by the Indxx Global Fintech Thematic Index, the underlying index for the Global X FinTech ETF (FINX), relative to the Financial Select Sector Index.

Since 09/13/2016, the date of inception of Global X FinTech ETF (FINX), until 07/08/2019, the Indxx Global Fintech Thematic Index has outperformed the Financial Select Sector Index by 49.59%. Also, a zero percent overlap between the two indices and a correlation of 0.572 suggests a weak relationship between the old and new financial firms.4

While such outperformance may indicate a speculative bubble, financial results reveal high quality earnings for financial firms embracing technology. Return on equity (ROE) for traditional banks tends to be around 19%, while the ROE for digital-focused banks tends to be around 27%, given the scalability of tech-enabled platforms.5

M&A is on the rise

Gartner recently reported that by 2030, 80% of legacy financial firms could go out of business as a result of the high degree of digital transformation.6 As established financial service providers move quickly to defend their businesses from the FinTech insurrection, many are either establishing partnerships or buying FinTech companies outright. According to one analysis, almost 80% of financial institutions are engaging with FinTech companies.7 M&A has been the preferred option for many, with traditional firms opting to pay high premiums to participate in FinTech’s growth, which ultimately benefits the shareholders of these FinTech firms.

Since 2018, the M&A landscape for FinTech deals has been quite active. Just in 2019, deals have totaled over $97 billion, including four large deals valued above $10 billion.8 A few major transactions include Fiserv acquiring First Data Corp, Global Payments closing a transaction with Total System Services and Fidelity National Information Services buying Worldpay. Unsurprisingly, venture and private equity firms have also been aggressively deploying capital to invest with or acquire leading FinTech firms.

Many factors could continue to drive increased investments and M&A in FinTech, including:

- M&A is a key component of traditional financial services growth strategies – Banks have learned the hard way that the inertia of large organizations can stall organic progress. Jamie Dimon, JP Morgan Chase’s CEO, commented in his latest annual report that “…there are many capable financial technology (FinTech) companies in the United States and around the world – technology always creates opportunities for disruption. We have acknowledged that companies like Square and PayPal have done things that we could have done but did not. They looked at clients’ problems, improved straight through processing, added data and analytics to products, and moved quickly.”9 This acknowledgement, which is broadly shared by the traditional services industry, has resulted in aggressive investments from major financial services firm in FinTech companies.

- FinTech players targeting new clients – Technology has allowed FinTech companies to offer solutions to the needs of the unbanked and underserved populations. Companies like Square in the US and PagSeguro in Brazil, to name a few, have been able to provide affordable hardware that enables micro, small, and medium size sellers to turn mobile and computer devices into payment and point-of-sale (POS) solutions. On the other hand, free investing apps and robo-advisors have helped bring wealth management to those with small account balances. For a long time, banks ignored these populations, failing to see their growth and developing a scalable business to serve them. Today, banks could be on the hunt to acquire FinTech targets that have succeeded in reaching the underserved as traditional firms look for new avenues of growth.

- Younger generations will continue to push for more appealing financial products and services – Millennials and the Gen Z generation are opting for financial services that offer them convenience via tech-enabled platforms. They want companies that allow them to open an account in minutes and access its services with just one click. Many FinTech companies have already reached these generations, which are usually identified as being innovators or early adopters. Thus, traditional financial services firms looking to gain next generation clients may acquire them via FinTech investments.

Global consumers are growing less reliant on cash

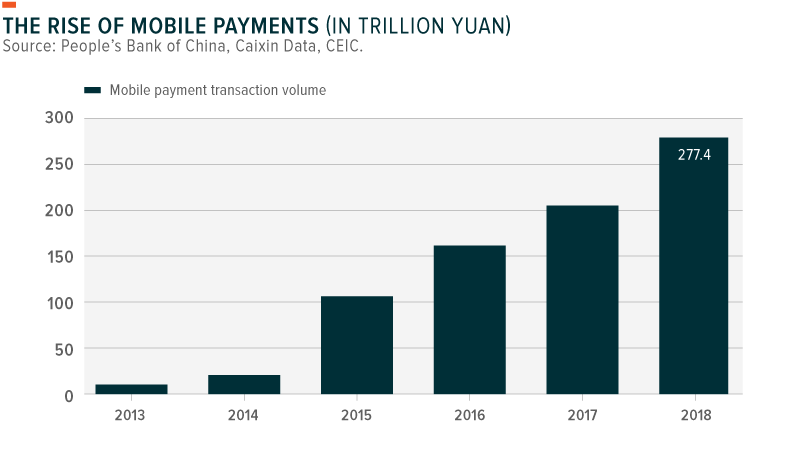

Global consumers have grown less reliant on cash, resulting in fast growth of the mobile payments space. In 2018, China alone processed $41.51 trillion dollar in mobile transaction volume.10 That’s more than three times China’s GDP. Consumers are often drawn to the convenience of mobile payments, as well as the access to greater spending data and often targeted rewards from certain merchants.

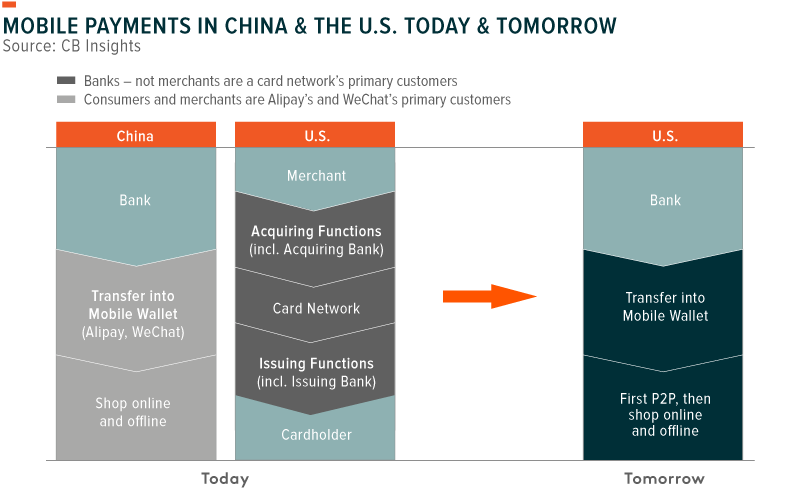

Despite this early growth, mobile payments still have significant room to grow. For example, in the US, merchants and sellers have to pay high fees to participate in bank-backed, open loop card networks.11 Given these fees, in a $100 transaction between a merchant and a cardholder, on average only $97.30 goes to the merchant.12 On the other hand, in China, mobile payments using mobile apps such as Alipay/WeChat Pay a merchant receives ¥99.30 per ¥100 transaction.13

Given high fees, sidestepping banks and card networks has been a long-term goal of retailers and merchants as they seek to improve profitability. FinTech companies such as PayPal, Square, Stripe, Intuit, working together with Google, Apple, and Amazon formed the advocacy group, Financial Innovation Now (FIN). FIN is working with policymakers and other stakeholders to ensure that legislative and regulatory initiatives encourage the growth and adoption of new financial services technologies and products.14

Another approach is for companies like Starbucks to use their mobile apps to facilitate payments and disintermediate credit cards. The Starbucks app allows consumers to transfer money from their bank account or credit card to a mobile wallet, which is then used to pay for a coffee or food item. This method reduces the credit card transaction volumes and therefore fees for the merchant. Yet, future expectations aim to replicate the model of Chinese payment leaders, in which consumers and merchants are their primary customers rather than current banks and card networks.15

Conclusion

FinTech has evolved significantly over the last few years, yet the penetration rates of its various technologies still remain low, indicating the early nature of this theme. While M&A is helping companies achieve synergies and grow their market position, ultimately increased overall adoption of mobile payments, enterprise software, and P2P lending will be the main driver of FinTech’s long term growth.

We believe that complementing a portfolio’s Financial sector exposure with Fintech can improve growth characteristics, while diversifying holdings and mitigating the potential disruption risks associated with traditional financial services companies.

Related ETFs

FINX: The Global X FinTech ETF seeks to invest in companies on the leading edge of the emerging financial technology sector, which encompasses a range of innovations helping to transform established industries like insurance, investing, fundraising, and third-party lending through unique mobile and digital solutions.

Please click the fund name above for standard performance information.