Preview

Editor’s Note: Please see the glossary at the end for all terms highlighted in sea green found in the order that they appear.

In 2022, gold price volatility is higher than it’s been the last few years due to the shifting economic environment and global macro uncertainty. Given the contrasting forces of hawkish monetary policy against persistent inflation, for most of the year we have noted a decoupling of gold from its historical main driver: real (inflation-adjusted) rates. Against this backdrop, we investigate gold’s potential role as a portfolio diversifier and its potential for outperformance amid high geopolitical tensions and renewed central bank gold purchases. In our view, the yellow metal’s characteristics make a compelling case for long-term investment.

Key Takeaways

- Despite the Federal Reserve’s (Fed) aggressive tightening cycle, gold is holding up better than expected in 2022, supported by persistent inflationary pressure and geopolitical tensions.

- We expect central banks’ demand for gold to remain high as geopolitical unrest continues to encourage central banks to buy gold. On the production side, after rebounding from COVID-induced delays, miners with healthy balance sheets should be able to continue investing in exploration.

- Although gold can experience contagion risk in short term periods of volatility, its thesis has held true over the long term. Gold has a lower long-term correlation to other risky assets and thus remains an attractive potential portfolio diversifier. It has a solid track record of being a stable asset with a low or negative correlation to traditional asset classes such as treasury bonds, equities, and the U.S. dollar.

Gold Holding Up Better than Expected in Turbulent Market Conditions

Over the last five years, amid mounting macroeconomic and geopolitical headwinds and the pandemic, gold performed well, registering highs of $2,063/oz in August 2020 following the COVID outbreak and $2,050/oz in March 2022 following Russia’s invasion of Ukraine.1 Year over year, gold’s underperformance compared to the S&P 500 is still a better-than-expected result considering hawkish U.S. monetary policy.2 Typically, higher interest rates raise the opportunity cost of gold and reduce its investment appeal. Even if gold hasn’t generated gains in 2022, it has managed to dodge the losses that equities have not.

Gold’s price swings this year are due to the uncertainty in the global economy. In fact, in the first three quarters of 2022, gold volatility was 8% higher than its five-year average.3 On one side, the Russia-Ukraine conflict heightened fears of supply chain disruptions and sustained inflation, bolstering gold's attractiveness as a potential inflation hedge. On the other hand, the Fed's increased hawkishness, a strengthening dollar, and a broader market sell-off across all assets sparked price corrections in gold.

Inflows and outflows into the Bloomberg Total Known Holdings of Gold ETFs Index track the amount of gold held by the ETFs underlying the index in troy ounce and its changes tend to correspond to changes in the gold’s price. Inflows totaled 7.8 million t oz in Q1 2022 as gold’s price increased by 6% during the quarter. Thereafter, outflows amounted to -1.3 million t oz when the gold price decreased by 7% in the second quarter and -7.3 million t oz when the gold price decreased by 8% in the third quarter. 4,5

With the Fed’s rate changes forecasted to slowdown beyond December, the US Dollar and 10-year real rates are expected to begin falling by 2023. Amid persistent market volatility and geopolitical risk, gold might be due for a rebound. Indeed, most major investment banks predict that gold prices will rise beyond $1,800 per ounce in the near future.6,7,8

Physical Gold Market Supply and Demand Rebounded Well from 2020

Physical supply and demand rebounded in 2021 mostly due to the recovery in consumer confidence as economies started to normalize. COVID-related interruptions subsided, and global mine output increased 3% year-over-year (YoY) to 3,581t.9 Most mines ran at full capacity, though China’s output fell due to work stoppages at its Shandong mine. With the mine back online, China's output is expected to rebound and help global supply to grow by 2% in 2022.10

In 2021, exploration activities increased significantly as governments relaxed mining regulations and gold prices remained high. The number of exploratory reports, such as drilling updates or planned exploration announcements, increased by 25% YoY. Australia, Canada, and the U.S. continued to draw the highest interest in exploration, given their geological potential and political stability.11 As long as gold prices remain high and miners have healthy balance sheets, they should be able to continue investing in exploration in 2022.12

Importantly, when macroeconomic risks and market volatility rise, investors often turn to gold due to its status as a store of value. According to the World Gold Council, if every ounce of the world’s above-ground stock of gold were placed next to each other “the resulting cube of pure gold would only measure around 22 meters on each side." For investors, this scarcity is gold’s charm.

Demand for physical gold was robust in 2021, with gains across the jewelry industry, the largest source of annual demand for gold, which accounts for 46% of total demand.13 Global jewelry production returned to pre-pandemic levels at 905t, a 68% YoY increase.14 India, the world’s largest consumer gold market, accounted for over half of the increase globally, helped by the return of weddings.15

In 2022, jewelry demand from China, the second largest consumer of gold, is projected to decline due to the country’s zero-COVID policies and economic slowdown. However, industrial demand is expected to remain strong after it returned to 2019 levels by increasing by 9% in 2021.16 In particular, after declining for two straight years, demand for gold in the electronics industry increased due to a robust rebound in electronics sales owing to “working from home” economies.17 Demand for electronics is projected to continue its upward trajectory in 2022.18

Looking beyond this and next year, the worldwide jewelry market size is predicted to reach USD 518.90 billion by 2030, according to a new analysis by Grand View Research, Inc. Its compound annual growth rate (CAGR) from 2022 to 2030 would be 8.5%.19 The gold jewelry category is expected to expand the most.

Late Cycle Dynamics and Inflation Pressure Expected to Keep Gold Prices High

Currently, macro factors signal we are likely in a late-cycle economic environment, with persistently high inflation across the global economy. When economic expansions are close to their peak, gold prices often increase. Gold’s biggest gains typically occur in the final stages of expansions because gold’s long-term price dynamics are cyclical given its appeal as a store of value.20

Since 2021 began, global living costs have risen faster than in the previous five years.21 Both developed and emerging markets are affected by rampant inflation.22 Inflation in the U.S. continued around 1982 highs, September's Consumer Price Index (CPI) YoY print was 8.2%, down from June's 9.1%. In the UK, September's inflation was 10.1%, up from 9.9% in August but equal to July’s level. Despite signs of inflation peaking, high CPI prints might endure through 2023 owing to supply disruptions, a tight labor market, and high energy costs, which can be good news for gold bullion due to its positive association with inflation.

In fact, gold is considered a potential inflation hedge because of its track record of great performance amid high inflation, such as in the late 1970s into the 1980s. Gold returns were best when U.S. headline CPI is above the Fed’s target level of 2%. Historically, when inflation between 2% and 5%, gold’s price increased 7% on average. And in years when U.S. CPI averages more than 5%, the price of gold increased nearly 22% on average.23

Decoupling from U.S. Real Yields, a Key Gold Performance Driver

Historically, U.S. real yields are one of the main factors that affect the dollar-denominated gold price. Real interest rates are interest rates that account for the impacts of inflation; they are determined by deducting the expected inflation rate from the nominal yield of a bond. Because gold is a yield-free asset, rising real Treasury rates increase the opportunity cost of holding gold, which reduces its investment appeal. U.S. real yields accounted for most of the fluctuation in the USD gold price over the past 25 years.

Performing a regression analysis to approximate the relationship between gold and real yields, we found with an R^2 of 0.85, that over the last 10 years, a roughly $3 per ounce (oz) decrease in gold prices followed a 1-basis point (bp) increase in U.S. 10-year real yields.

By comparing the actual value of gold to the value resulting from the mentioned fair value model, we can notice the discrepancy over time. One limitation of regression analysis is that it tries to find the “best fit” assuming a linear cause and effect between the two factors; many times, the data does not actually fall on the line. At the end of Q3 2022, the actual real rate level was about 1.66 bps, and the resulting model implied gold value was around $872/oz while the actual gold was trading at $1,660/oz, i.e., at about 788$/oz premium to its fair value.24

The 25-years historical average premium to fair value is 10 $/oz thus the recent premiums data points (595$/oz as of Q2, 788$/oz as of Q3) show that gold held up much better than expected to real rates rise and hawkish monetary policy. The substantial premium over the real rates’ implied fair value has persisted over the past year, indicating a decoupling from the 10-year real yield.25 While we do not know if this decoupling will continue, negative pressure on gold from the Fed's tightening cycle has been and could continue to be less severe than would normally be expected based on the discussed regression analysis. At the same time, concerns about high inflation persisting and upward threats to energy costs may lead to more significant investment flows into gold.

Over the next year, markets expect a less hawkish path for Fed policy which suggests real rates may start to lose some ground in 2023. As of writing, the futures curve implies a federal funds policy rate peak of approximately 5.081 % by May 2023 to then start to decrease to 5.076% by June 2023.26 Looking forward, lower interest rates should strengthen the profitability of gold investments and support a case for gold to break out higher because of a lower opportunity cost of holding gold.

Demand for Gold High as Central Banks Seek Protection Against Risks

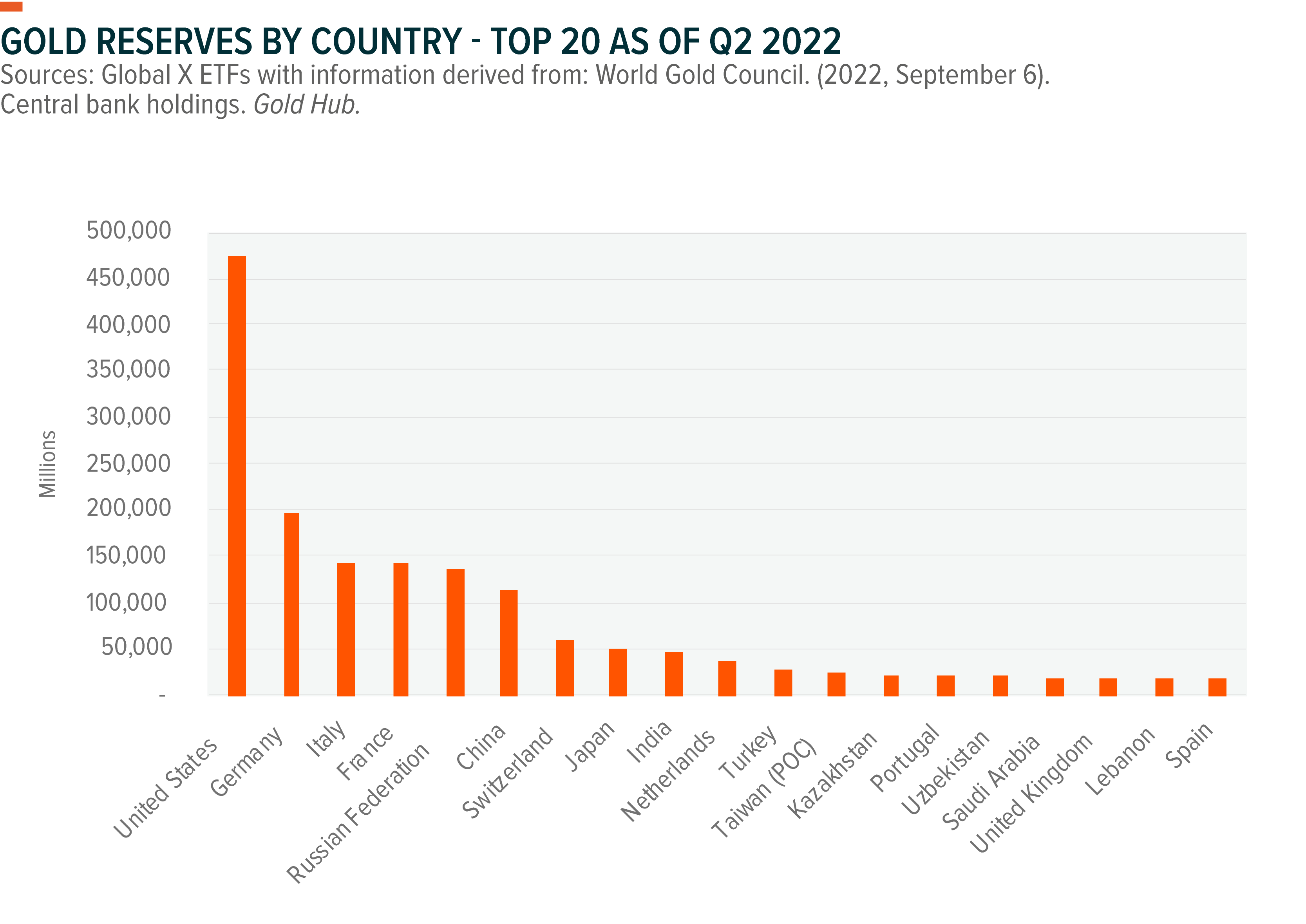

Gold plays a key role in central banks' decision-making as it is still crucial to the functioning of the global monetary system. Before gold started to trade freely in the global financial markets, bullion was used as cash worldwide when paper money wasn't invented yet, while by the late 19th century, major currencies were tied to gold in various forms for about a century. Nowadays, central banks hold reserves in gold in an effort to safeguard their financial systems and hedge against other currencies. We expect geopolitical tensions around the world will continue to encourage central banks to buy gold, especially countries where gold holdings are low relative to total reserves.

Net official gold sector purchases rose by a significant 79% year over year to 455 tons (t) in 2021.27 In addition to regular buyers like India and Commonwealth of Independent States (CIS), several countries resumed purchases. Among them, Thailand, India, Hungary, and Brazil were the biggest buyers.28 Strategic gold purchases by developed markets like Singapore and Ireland were particularly notable and may indicate a shift in public sector buying behavior. Developed markets hold the majority of gold reserves, but over the last decade or so, emerging market countries accounted for most of the gross purchases.

According to the latest World Gold Council Central Bank Gold Reserves (CBGR) survey, 25% of central banks plan to increase their gold reserves in the next 12 months, up from 21% in 2021 as bullion can backstop domestic banking systems and cushion against balance of payments (BOP) problems, where the BOP refers to all transactions between entities in one country and the rest of the world Survey respondents predict that gold and the Chinese yuan will play more significant roles in the international monetary system in the next five years, perhaps at the expense of the U.S. dollar and the euro.29

Respondents from emerging economies were less confident in the dollar’s status as a reserve currency and more worried about shifts in global economic power than their developed market peers. Historically, central bankers in emerging and developing economies view gold as more crucial to their reserve management strategy, given their challenges in maintaining stable currencies and keeping capital flows orderly.

The survey also underlined that the sanctions against Russia enhanced gold demand and led to central banks holding more gold as a reserve asset in an effort to protect against currency risks. Among the restrictions enacted in response to Russia’s invasion of Ukraine, the G7, the European Union, and traditionally neutral Switzerland banned imports of Russian gold in an effort to deprive the Putin administration of financing.30,31 Also, the London Bullion Market Association, which sets standards for the market, removed Russian gold refiners from its Good Delivery accredited list.

We anticipate part of the expected rebound in net global gold purchases to come from the Central Bank of Russia (CBR). The CBR is expected to absorb most of the country’s domestic mine production because of the ban on Russian bullion. And those purchases are significant, as Russia is the world’s second-largest producer of gold, producing roughly 300t per year and contributing about 9.3% of worldwide output.32 Russia also is the world’s fourth-largest exporter of gold.33 Still, the impact of the import bans on Russian gold should be limited, as bullion typically trades more on macro dynamics than supply and demand dynamics. Plus, Russian gold can find a home in other markets, including India and China.

Gold Remains an Attractive Potential Portfolio Diversifier

Portfolio diversifiers that can perform during market turbulence are in demand in 2022, and gold has a solid track record of being a stable asset. For the 5-year period from 30th September 2017 to 30th September 2022, gold’s 30-day historical volatility average of around 13 was lower than the S&P 500’s at around 17.34

Gold’s volatility has been trending downwards for quite some time; it only heightened during severe bearish market conditions such as in the COVID-19 pandemic. Over the past 5 years, gold historical volatility was clearly lower than many other asset classes such as oil, copper, 10-year treasury, and S&P 500 as shown below.

Gold’s low correlation to several asset classes stands out. Its correlation with S&P 500 from September 30th, 1997, to September 30t 2022 is -0.09. In the last 5 and 10 years, gold’s inverse relationship with the dollar (correlation of -0.5) was significant.

Gold’s more recent negative correlation with the dollar is a notable diversification feature. The Fed's tightening in the current environment has kept the dollar strong, but when it begins to fall from multi-year highs, we anticipate it will drive more investors into gold. With U.S. manufacturing activity declining to a more than two-year low in October 2022, the central bank is expected to ease its monetary tightening at some point in 2023.35 Upon that easing, should dovish forward-looking policy views from the Fed undercut the dollar's strength, we would expect prices to climb and gold ETF flows to increase.

Multiple Ways to Get Exposure to Gold, Including the Global X Gold Explorers ETF

Investors can buy physical commodities like gold if they are willing and able to handle storage and the associated storage costs. Investors can also gain exposure to physical gold through physical gold ETFs or through the futures and options markets, by bearing the associated costs. Alternatively, it is possible to indirectly get exposure to gold by purchasing gold mining stocks, which also means exposure to idiosyncratic company risks. Finally, an ETF on gold miners and explorers can be a compelling option because investors get exposure to the broader gold mining sector linked to the commodity’s underlying fundamentals. Overall, the share prices of gold mining companies are strongly correlated with the underlying commodity and typically produce higher levels of volatility than their underlying commodities; indeed, they are considered a leveraged play on gold.

For example, the Global X Gold Explorers ETF (GOEX) provides investors access to a range of companies involved in the broader gold supply chain, including exploration, extraction, mining and refining. Also, accessing the industry through a broad basket of gold industry stocks such as an ETF can help mitigate exposure to individual company risks.

Companies that engage in exploration activities are sometimes equated with venture capital, in that investments in them are early stage with high risk but high potential reward.

Explorers’ economic success depends on their capacity to identify commercially viable gold ores. Once gold is found, explorers can engage in M&A with a mining company or mine it themselves. Junior Miners are smaller firms engaging in exploration, development, or mining. Size makes them more nimble and able to pursue smaller opportunities than larger mining enterprises. While large miners can reduce costs via economies of scale and operational efficiency, they often acquire new mining operations to boost output thus ultimately depending on explorers and junior miner to expand.

Gold miners have historically beaten bullion in bullish markets because they employ operating leverage to improve earnings and share prices. This is partly attributable to profit expansion, since miners may sell appreciating gold rapidly, preventing a price decrease, while their own operational expenses increase slowly.36

Conclusion: Validity of Gold's Traits Remains.

We expect this backdrop to encourage many investors to diversify into gold, mainly if its price corrects and dip-buying becomes more popular. Amid weakening industrial activity, central banks may moderate monetary tightening in 2023. After that, we anticipate a rise in flows to gold and gold related ETFs as dovish forward-looking policy views from the Fed could weaken the dollar.

In our view, gold remains a solid potential hedge against inflation and store of value in times of economic downturns and geopolitical unrest. And year to date, despite the Fed’s aggressive tightening cycle, gold has outperformed its suggested fair value based of regression analysis compared to the 10-year real yield. We expect macroeconomic conditions and persistent geopolitical risks, such as the lingering war in Ukraine, to keep gold in demand. Risks like these are why we believe gold, given its negative correlations with other assets, remains a desirable portfolio diversifier.

Related ETFs

GOEX: The Global X Gold Explorers ETF provides investors access to a broad range of companies involved in the exploration of gold deposits.

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.