Global X Research Team

Global X Research TeamGreece exited its largest ever bailout program just over 18 months ago, sparking a market rally that led the country to finish 2019 as one of the best performing emerging markets. Yet COVID-19 and the ensuing collapse in trade, tourism, and oil prices introduced new obstacles in the way of Greece’s long recovery, shaking the economic foundation Greece carefully rebuilt over years of painful austerity measures. While the pandemic may be far from over, Greece appears better equipped to combat COVID-19 than other Emerging Markets, given Europe’s strong public health systems, ECB monetary stimulus, and support for the most vulnerable industries like tourism, shipping, and banking.

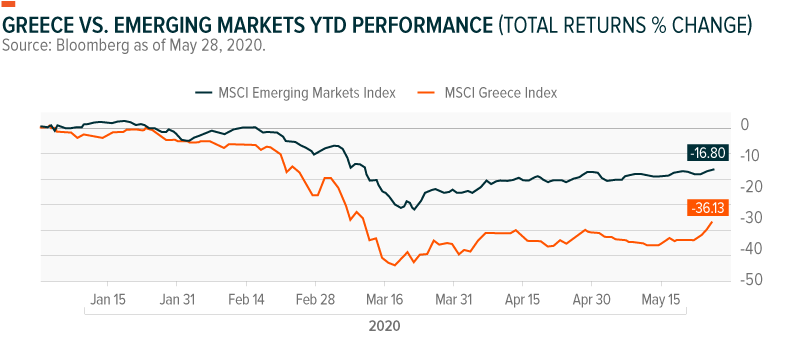

Greek Recovery Halted by COVID-19

Greece’s fragile economic recovery is suddenly facing strong headwinds. From August 2018 to the end of 2019, as Greece enjoyed strong equity market performance as the country exited the IMF bailout program, GDP expanded, unemployment fell, and the country returned to global capital markets issuing relatively inexpensive debt. Yet COVID-19 threw a wrench in those recovery plans. Consequently, Greek markets have suffered this year, significantly more so than the broad MSCI Emerging Markets Indexes.

Year-to-date, Greece is one of the worst performers among EMs with negative returns of -36.13%.1 This is worse than regional peers like Portugal, which has lost -17.17% so far in 2020. It is also worse than other EMs globally, including Turkey, Brazil, and Indonesia, as well as oil exporting Saudi Arabia and Russia.

Adjusting to a New Normal

While Italy and Spain were hit hardest by the health consequences of COVID-19, Greece and Portugal received praise for the success of its early and aggressive lockdown measures. As a result of Greece’s successful containment efforts, and a desire to avoid more economic pain, the country plans to reopen between mid-June and early July to tourists. A safe reopening may be difficult to plan but will be critical to restoring economic growth as nearly 25% of GDP is derived from tourism.

Yet despite successful containment efforts, Greece’s economy weakened under shutdown orders, as tourism, trade, and general economic activity plummeted. Greece’s Financials sector was among the most severely impacted as the banks were called on to renegotiate loans with individuals and businesses. Greece, however, has more monetary support than the average emerging market. In response to widespread liquidity issues across Europe, the European Central Bank (ECB) announced an increase to its quantitative easing (QE) program and activated a powerful €750 bn bond-buying program, called the Pandemic Emergency Purchase Program (PEPP). PEPP is specifically designed for addressing the pandemic, and for the first time ever, includes Greek sovereign debt. This crucial ECB support did prompt Greek bonds to rally and Financial stocks to recover somewhat from their extreme lows. With the more recent deceleration in new COVID-19 cases and the announcement of EU policy support, gains extended across nearly every sector in Greece, except the still embittered Energy space.

Broad EU Policy Support

Despite the challenges noted above, Greece may be better-positioned than most EMs to recover during post-COVID normalization. We attribute our optimism to the country’s robust support from the EU, a unique monetary and fiscal backstop that most EMs cannot rely on. Greece is eligible to receive aid and may benefit from the rollback of restrictions in EU funding agreements, which previously constrained spending. Supportive EU measures include:

- EU Responsiveness: Approved by the European Parliament, the “Coronavirus Response Investment Initiative” frees up €37 bn of European public investment, as a liquidity buffer for member states and sectors most affected. It reduces spending constraints on prior funding to allow for greater spending flexibility. EU member states and companies can access the EU Solidarity Fund, which provides additional cushion per member state of up to €800 million.

- EU Member State Coordination: EU Members ramped up their efforts towards the end of March, and by mid-April enacted discretionary fiscal measures amounting to 3% of EU GDP, in addition to automatic stabilizer measures. Public guarantee schemes and deferred tax payments also expanded, reaching 16% of EU GDP to provide buffers to vulnerable industries, including tourism and travel, which is critical for Greece.

- Aiding a Corporate Recovery: The European Investment Bank (EIB) is coordinating its policy response across EU institutions, allocating €1 billion from the EU budget to act as a “guarantee to the European Investment Fund (EIF)”. The EIF is in turn incentivizing banks to provide liquidity to SMEs and mid-caps, unlocking a total of €8 billion of working capital to support over 100,000 SMEs and small mid-cap companies in the EU.

Conclusion

Greek markets sold off aggressively in March compared to other Emerging Markets. Greece’s trade and tourism-dependent economy and weak financial system makes it particularly vulnerable to the spread of COVID-19. But a robust domestic response and regional support allowing businesses to reopen and tourism to resume may trigger a faster than expected recovery. Early actions halting the spread of COVID-19 domestically and earned Greek leaders praise from the international community. In addition, ECB and EU monetary and fiscal support is an envious backstop unique to Greece among emerging market countries. The outlook for recovery from COVID-19 is still highly uncertain, with global markets facing a host of unknown economic, political, and social issues. And while the road to recovery may be bumpy, with unpredictable timelines for fully reopening the global economy to trade and tourism, Greece may be well positioned to retake recent losses and resume its multi-year path to sustainable economic growth.

Related ETFs

GREK: The Global X MSCI Greece ETF (GREK) invests in among the largest and most liquid companies in Greece.