Rohan Reddy

Rohan ReddyThe Global X Income Monitor for Q4 2020 can be viewed here. This report seeks to provide broad, macro level insights into the income characteristics of various asset classes and strategies.

Key Takeaways:

- While high inflation hasn’t materialized in the economy yet, inflation expectations are increasing due to a greater likelihood of continued multi-trillion-dollar stimulus efforts

- Amid a backdrop of a low interest rate environment, investors may be wise to allocate towards asset classes and strategies that feature high yield with low duration

- Variable rate preferreds, high dividend stocks, and MLPs are a few areas that could be well positioned in an inflationary environment.

Rising inflation expectations are becoming a key discussion point in 2021. Rates were already on an upward trajectory in Q4, but recent developments fast-tracked those concerns in the new year. The market’s expectations of a more hawkish Fed policy is beginning to materialize despite the Fed’s commitment to not raise interest rates through 2023. Fed chair, Jerome Powell, later batted down those rumors, but the market is somewhat discounting his response. According to the New York Fed’s Primary Dealer Survey in December, the market believes the Fed’s net purchases of treasuries could begin to taper by the first half of 2022. Janet Yellen was also selected by President-elect Joe Biden to serve as Treasury Secretary for his administration in November. Ms. Yellen’s role would be different from her previous government position as Fed chair, but her recent comments supported more aggressive stimulus packages and an aversion to a weaker dollar.

Fiscal developments also contributed to rising concerns around inflation. In early January, the Democrats won control of the US Senate, and thus Congress, after the Georgia Senate runoff. This enables Democrats to pursue more ambitious fiscal stimulus efforts with less resistance from Republican lawmakers. A potential third round of stimulus is the highest profile example to date. Biden’s $1.9 trillion economic aid package includes a proposed additional $1,400 payment to individuals, on top of the $600 already agreed upon in the $900 billion package passed in December. The Democrats margin of control in Congress is extremely tight, so there are no guarantees of future stimulus bills passing, but the tide is now in their favor.

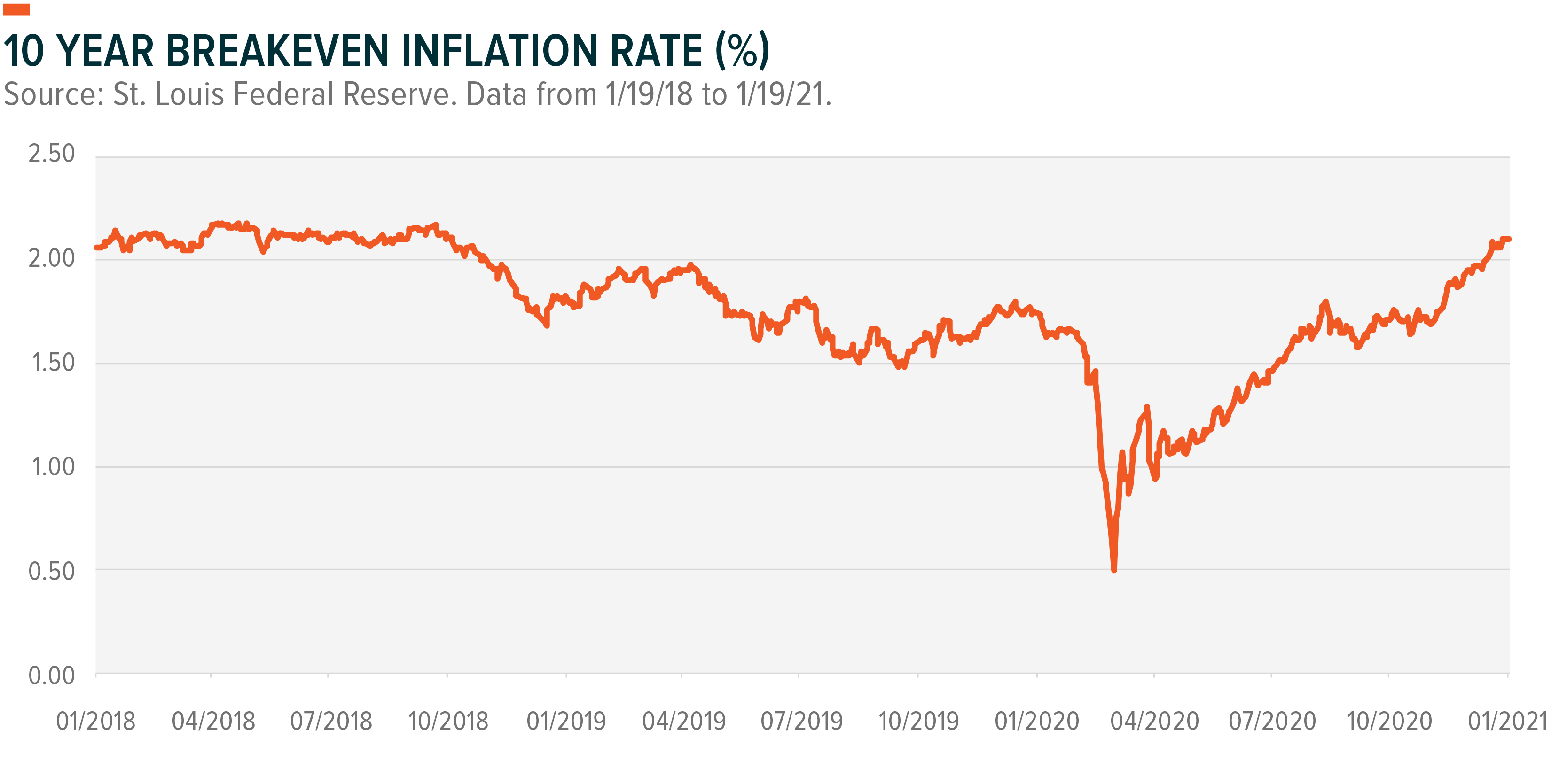

For investors, the key question is whether rising inflation expectations actually materialize in the economy. Looking at the current 10-Year Breakeven Inflation Rate, which compares nominal yields versus inflation protected bonds of the same maturity, we can see inflation expectations are accelerating from their nadir during the pandemic. But common inflation measures like the Consumer Price Index (CPI) are not indicating inflation has accelerated beyond pre-pandemic levels.

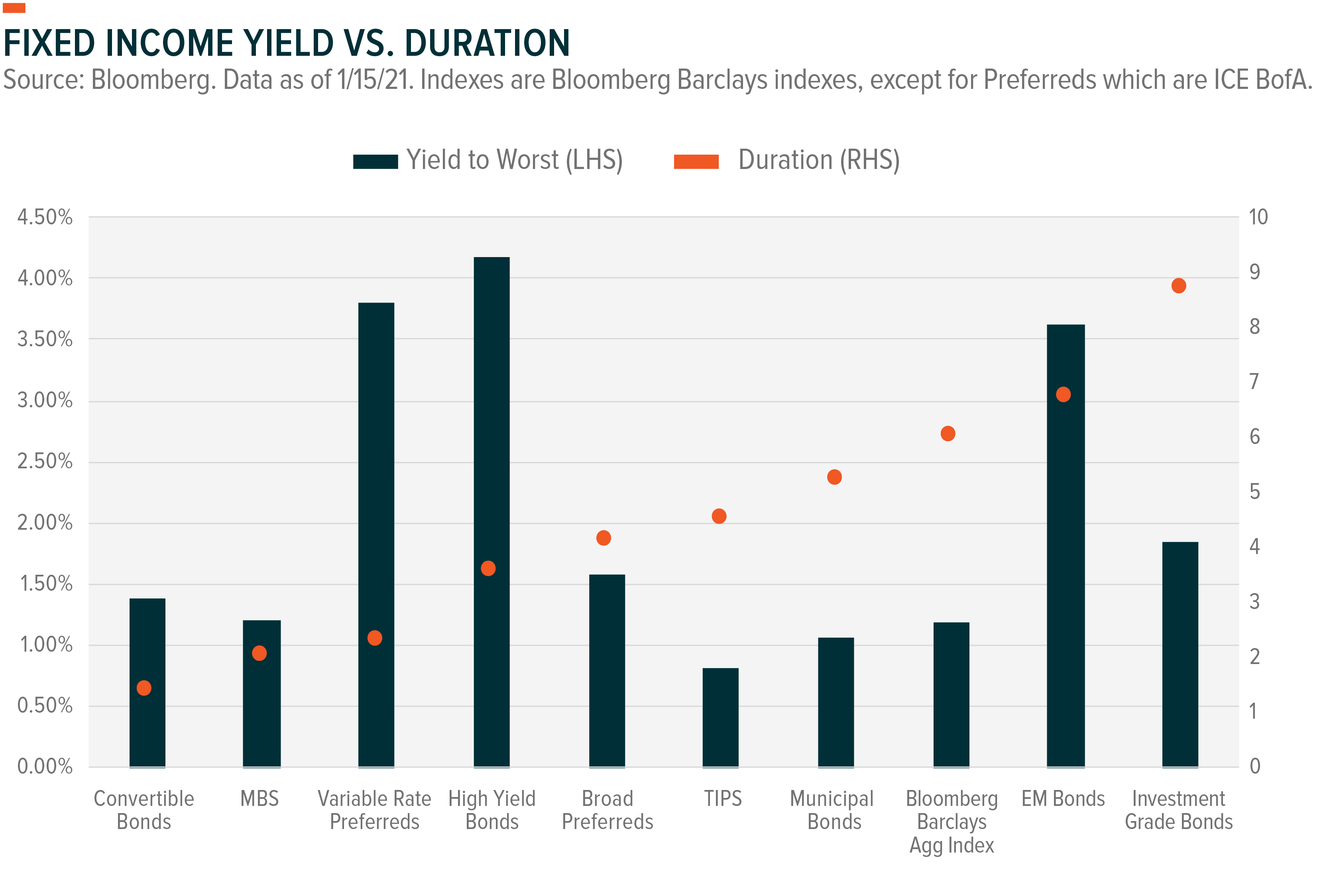

If inflation were to materialize, it could have a significantly negative impact on fixed income investments by lowering real returns. Investors concerned about inflation risk in the near future may want to prepare by reducing their portfolio’s duration, or interest rate risk. However, in the near term, there is typically a tradeoff between duration and yield, meaning reducing duration can also reduce a portfolio’s yield. This presents a challenge for investors living off their portfolio income amid an already historically low yield environment.

The sweet spot may be in allocating to asset classes that feature both low duration and high yield. Currently, variable rate preferreds and high yield bonds offer an attractive balance of lower duration and higher yield in the fixed income space. Variable rate preferreds typically pay a fixed coupon for the first 5 to 10 years of the preferred’s lifecycle before paying a floating rate based on the London Interbank Offering Rate (LIBOR) plus a pre-determined credit spread. Therefore, as rates increase, their coupons adjust higher. High yield bonds tend to pay fixed coupons, but they are largely issued with intermediate (such as 5 year) maturities.

We favor variable rate preferreds due to extremely tight credit spreads on high yield bonds. High yield spreads ended 2020 at the same level they started 2020, 3.27%, despite substantially greater risks in the economy.1 Variable rate preferreds, on the other hand, have higher overall credit quality than high yield bonds, with a BBB- rating at the index level compared to a B+ rating for high yield bonds – four notches higher.2 With the real economy is still on shaky footing, reaching too far into high yield credit could be costly.

Income-paying equities is another area that could be well positioned if inflation increases. Value stocks and cyclical sectors like Energy and Financials are examples of that. Greater fiscal stimulus could trigger reflation, but it would support higher economic growth. Small cap stocks also tend to benefit because of higher domestic exposure and the direct effect of a strengthening economy. High dividend stocks, which often have factor exposures to Size and Value, could be primed for a rebound in an inflationary period. Master limited partnerships (MLPs) also stand to potentially gain from increasing energy production through an inflationary oil price environment.

While inflation remains uncertain, we believe the odds of greater fiscal stimulus and economic activity could lead to rising interest rates sooner, rather than later, and investors would be wise to begin positioning their portfolios for this potential environment.