Rohan Reddy

Rohan ReddyOn February 22, 2023, we listed the Nasdaq 100 ESG Covered Call ETF (QYLE) and the S&P 500 ESG Covered Call ETF (XYLE). QYLE and XYLE are the latest additions to Global X’s covered call suite and are designed to offer investors the potential to achieve multiple goals. One goal an investor may have for their portfolio is to take Environmental, Social, Governance (ESG) considerations into account in which both ETFs are designed to invest in the equities of large-cap companies who display positive ESG characteristics by tracking an index that employs an ESG screening process. The second goal is that of an income investor, seeking to increase income potential via a covered call strategy that sells call options. These two ETFs are our first covered call related ESG offerings whose portfolios implement this two-pronged ESG and income-oriented strategy.

Key Takeaways

- Investment mandates that make Environmental, Social, & Governance (ESG) the focal point of their component selection processes have increased in popularity over the past decade. This trend may continue as investor bases change over time.

- Investor influence has continued to grow in the U.S. over the past few decades. U.S.-listed, passive ESG funds represent a $70 Billion1 opportunity to induce shifts in corporate behavior due to the exclusion and weighting criteria based on ESG metrics.

- Covered call strategies utilizing index options are a powerful solution for investors to potentially generate income and monetize volatility in an effort to achieve an extra source of income.

The Growing Focus on ESG for Companies

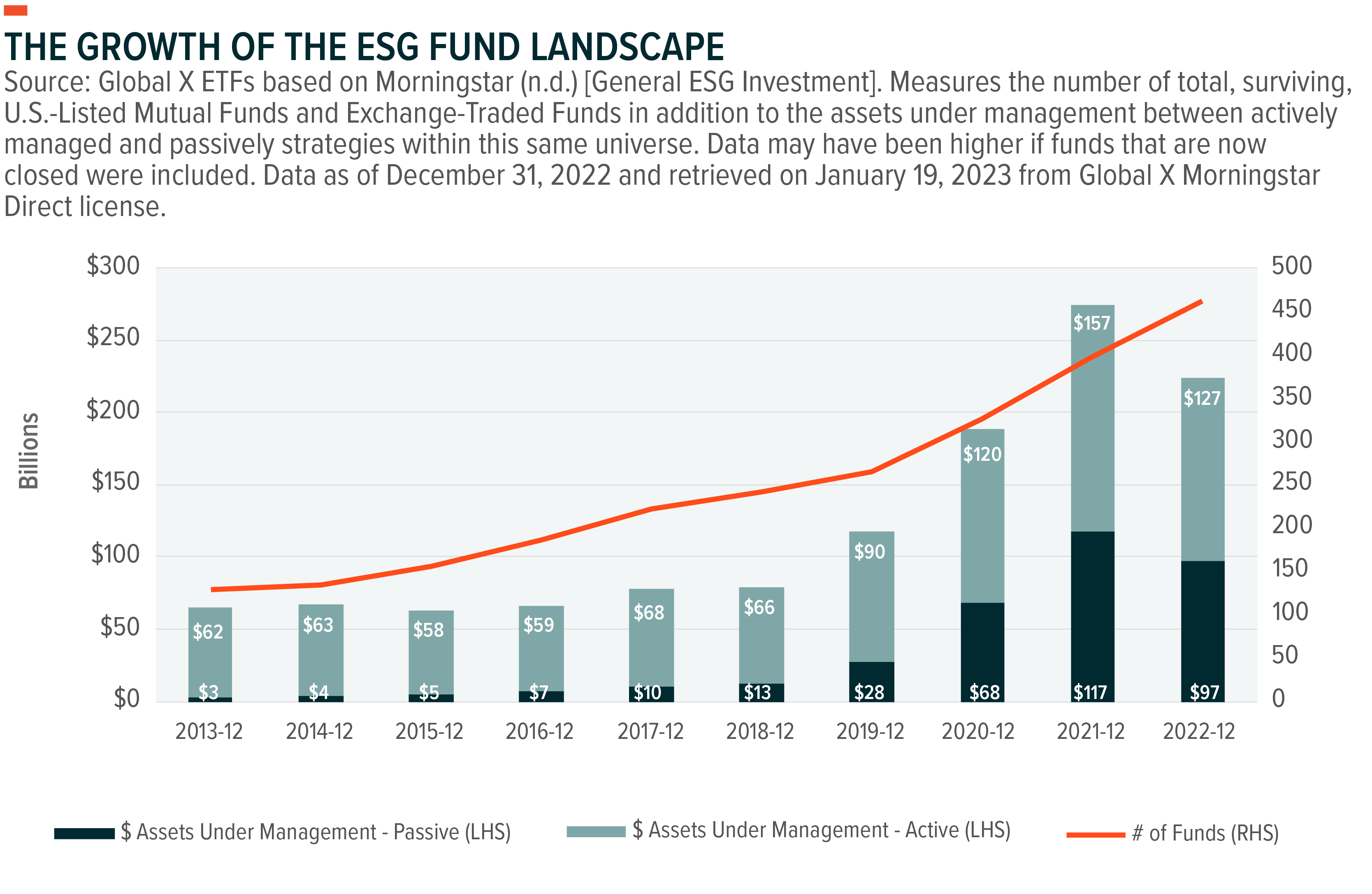

The demand for ESG investing is being driven by investor interest globally and PricewaterhouseCoopers (PwC) estimates that by 2026, ESG investing assets, globally, could reach $33.9 trillion, representing over one-fifth of total assets under management.2 Within the United States, in particular, the growing popularity of ESG investing is two-fold; size and scope of the asset base as well as the number of strategies currently being offered amongst open-ended mutual funds and ETFs. This is even more pronounced amongst the universe of passive ESG index funds. In fact, at the end of December 2013, amongst all surviving, U.S.-listed mutual funds & ETFs with ESG criteria as a central part of their investment strategy, only 3.33% sought to track an index.3 Fast forward to the end of December 2022 and this same segment now comprised 43.14% of the U.S.-listed, ESG fund landscape.4

ESG Screening Properties

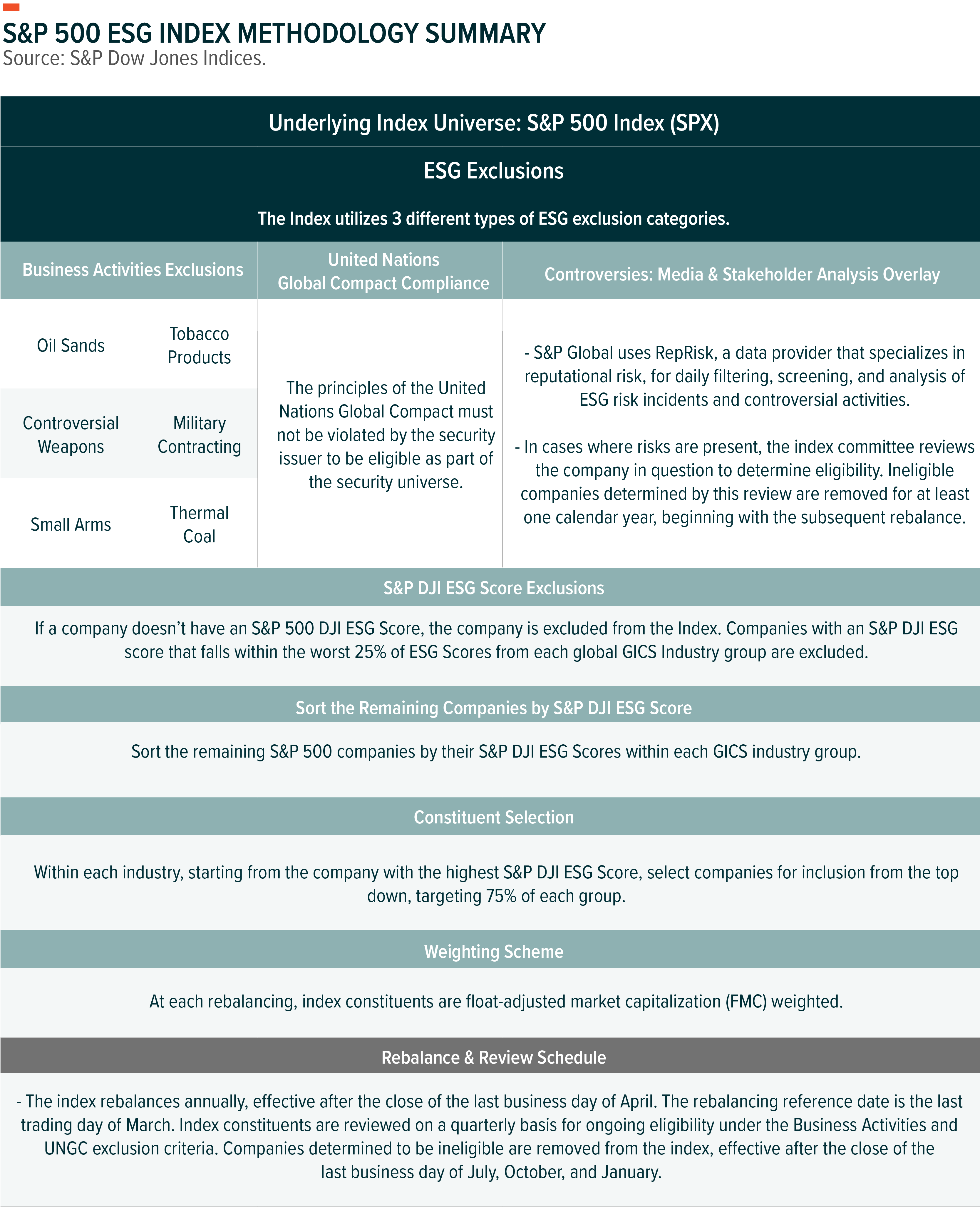

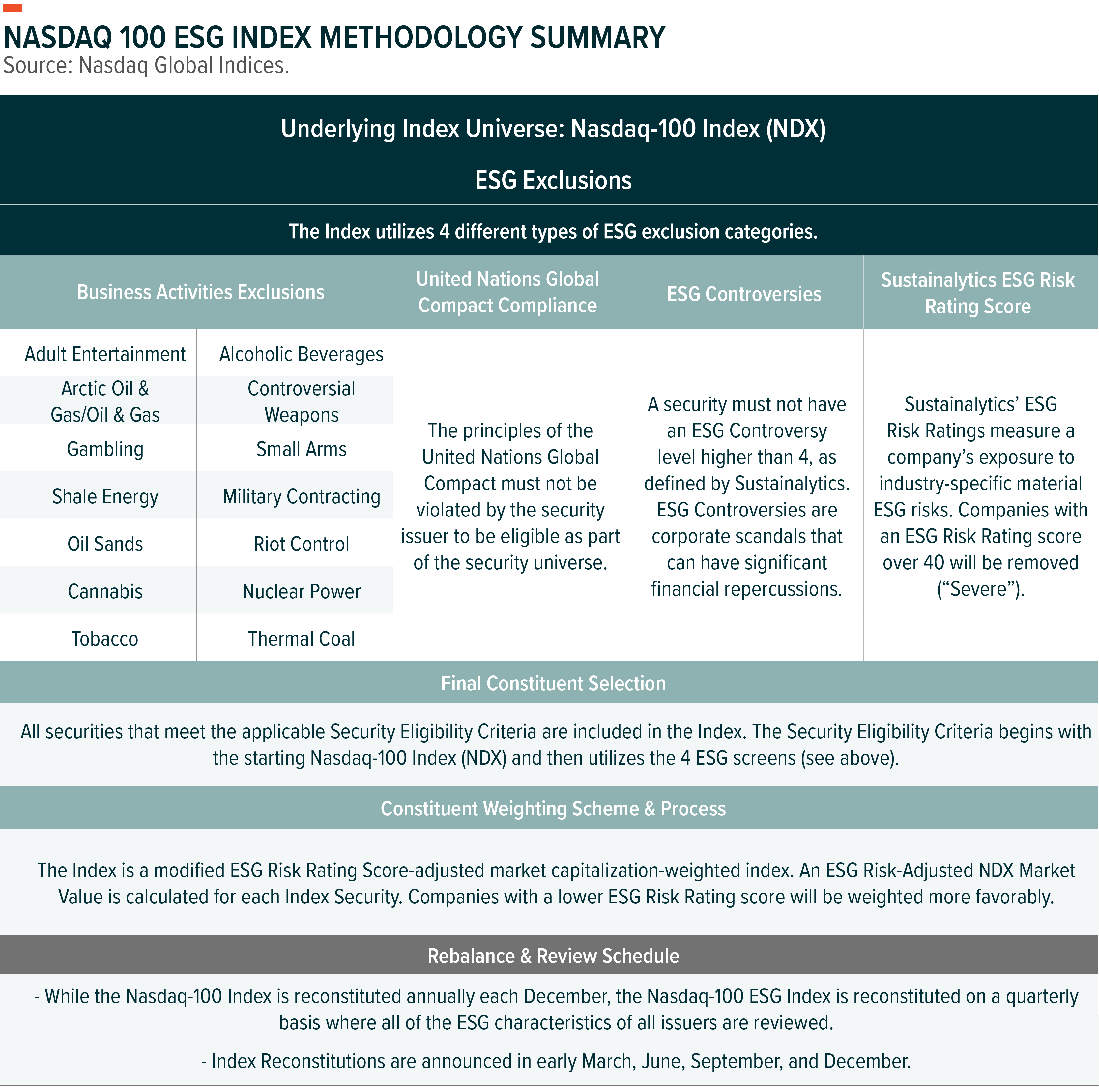

Two passive equity indices that implement ESG screening criteria include the Nasdaq 100 ESG Index and S&P 500 ESG Index. Each index starts with an initial universe of their respective parent equity indices, the Nasdaq 100 Index and the S&P 500 Index. Both, then, incorporate ESG investment screens through the use of ESG scores and exclusions related to controversial business activities, United Nations (UN) Global Compact compliance, and ESG Controversies. The ESG scores utilize a multitude of data points across a company’s business operations including issues such as environmental supply chain, employee management, human rights, board diversity and independence. The final score is a reflection of data aggregated across these multiple ESG considerations and controversial business activities may be excluded if they are seen as non-beneficial to society or actively working against climate change.

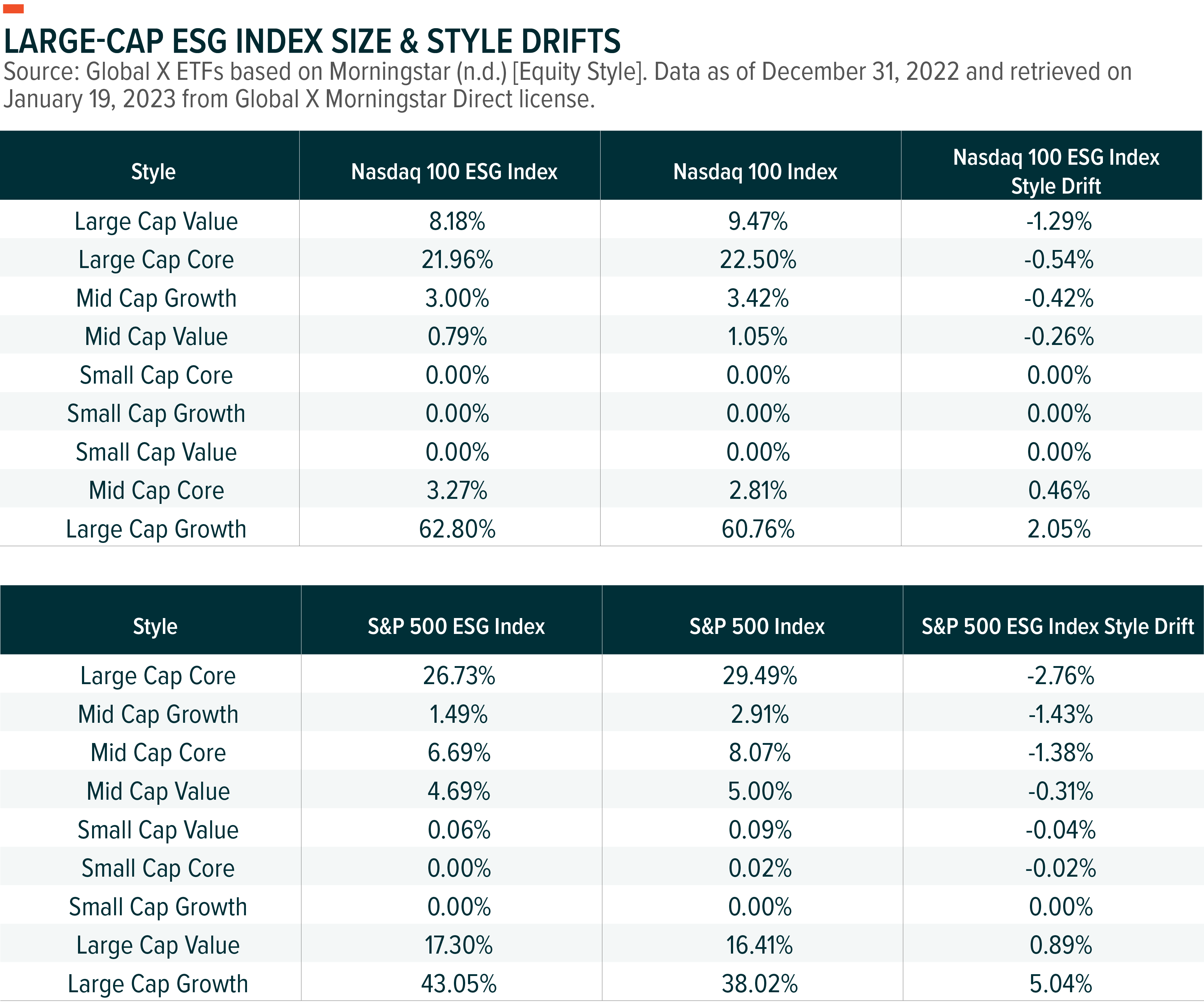

The Effects of an ESG Screen on Equity Exposure

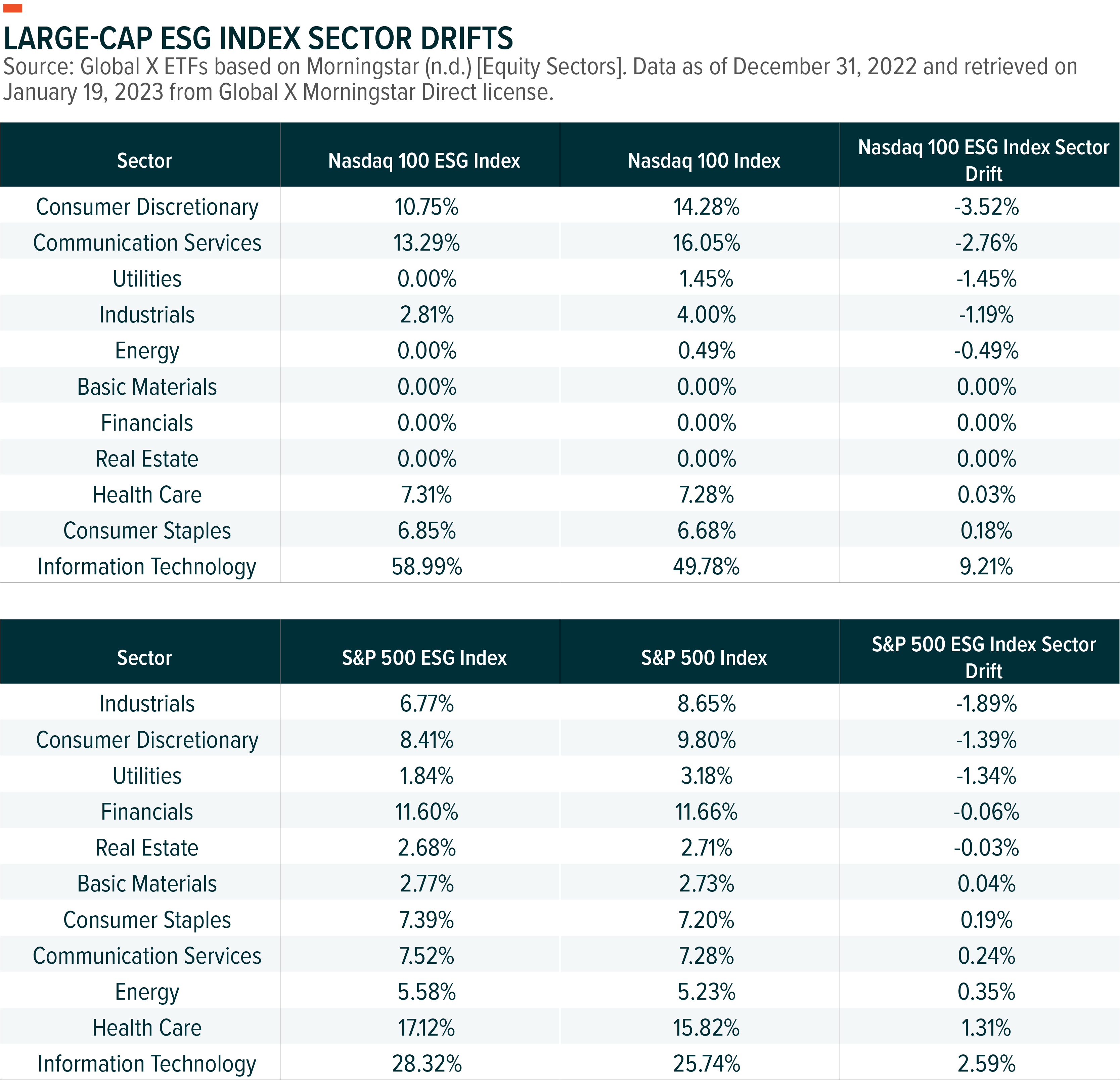

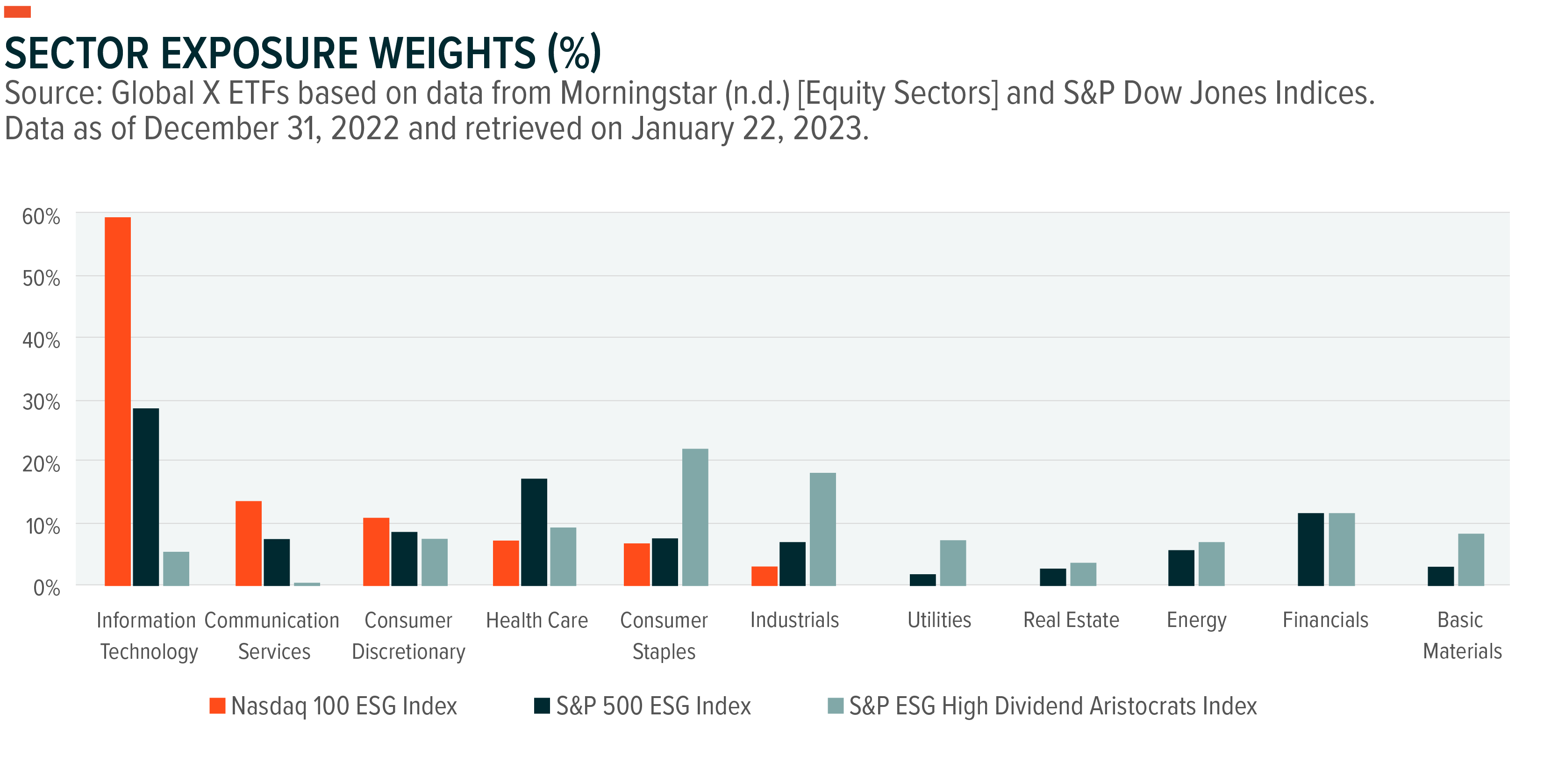

As a result of an ESG screening process, the final exposures within an ESG index relative to its parent index are expected to have a level of differences. For example, as of its last rebalance in April 2022, the S&P 500 ESG Index removed 196 companies from its initial universe, the S&P 500.5 This can potentially skew final sector and style exposures within the final portfolio and some sectors & styles may be impacted more so than others. As of the end of December 2022, both the Nasdaq 100 ESG Index and S&P 500 ESG Index were overweight information technology equities relative to their parent indices. On the other hand, we can see how the real estate sector was largely unaffected by their respective screening processes. When analyzing style allocations, these same indices were overweight the large-cap growth style while being underweight mid-cap equities.

An ESG Covered Call Strategy Can Potentially Thrive in Volatile Markets

Due to the sector & style differences across the Nasdaq 100 ESG Index and the S&P 500 ESG Index, the macro drivers between the two indexes are likely to be different, both in the long term and the short term. This can lead to contrasting levels of performance and volatility from one another.

The Income Potential

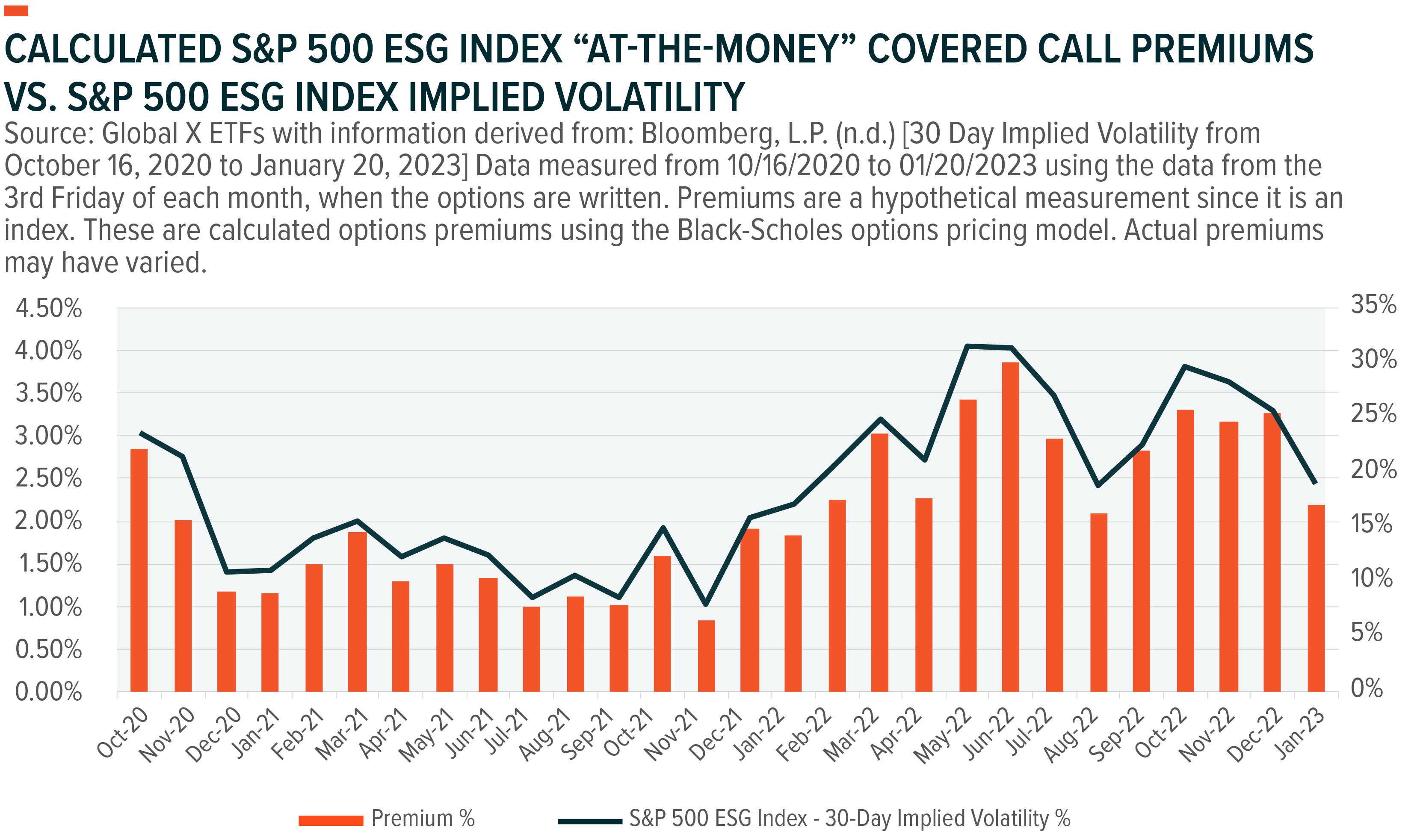

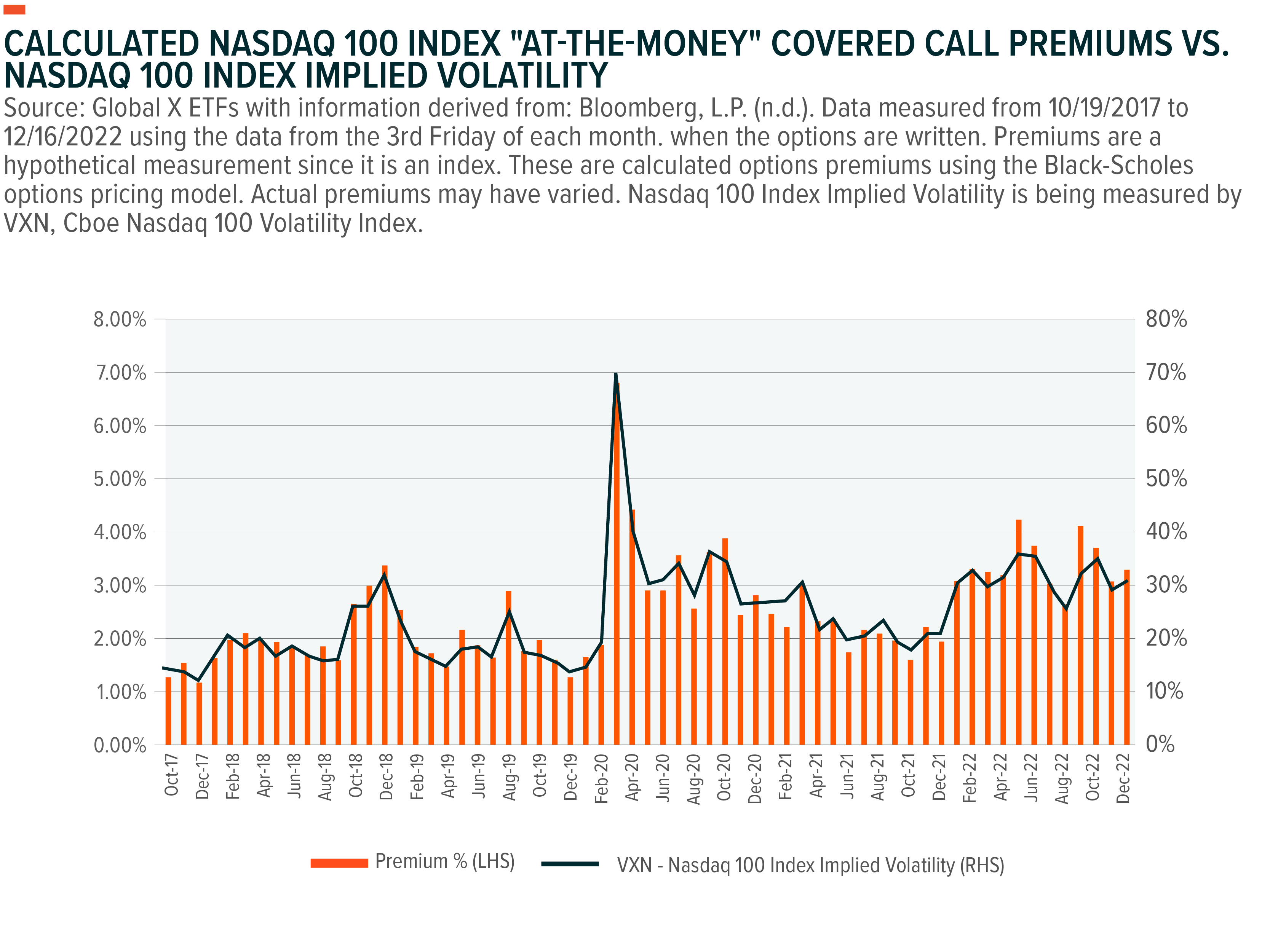

One way to harness perceived volatility is through an options writing strategy, such as covered calls. By writing covered calls, the option “seller” or “writer” forfeits a portion of or all upside potential in an underlying asset he/she already owns, in exchange for a premium. Typically, the closer the strike price of the contract sold is to the price level of the asset upon contract initiation, the higher the potential is for a higher premium. In addition to this, higher options premiums also tend to be correlated with the implied volatility of the underlying asset. Therefore, the higher the implied volatility, the higher the anticipated option premium. As an example of the income potential from writing index options, utilizing the Black-Scholes pricing model below, we visualize the calculated premiums that can potentially be received from writing call options on the S&P 500 ESG Index. Since index options on the Nasdaq 100 ESG index do not exist, we calculated premiums utilizing the Nasdaq 100 index using the same pricing model.

The Diversification Potential

By receiving income by writing calls on an index, income investors can potentially diversify their equity income portfolios to equity sectors that are typically un-aligned with other equity income strategies. One example is that of an ESG equity dividend strategy. These types of dividend-focused strategies tend to have sector leanings towards cyclical and defensive sectors, making them less diversified from this standpoint. Through pairing a strategy like this with an ESG covered call strategy, the higher the diversification opportunity is.

The Volatility Reduction Potential

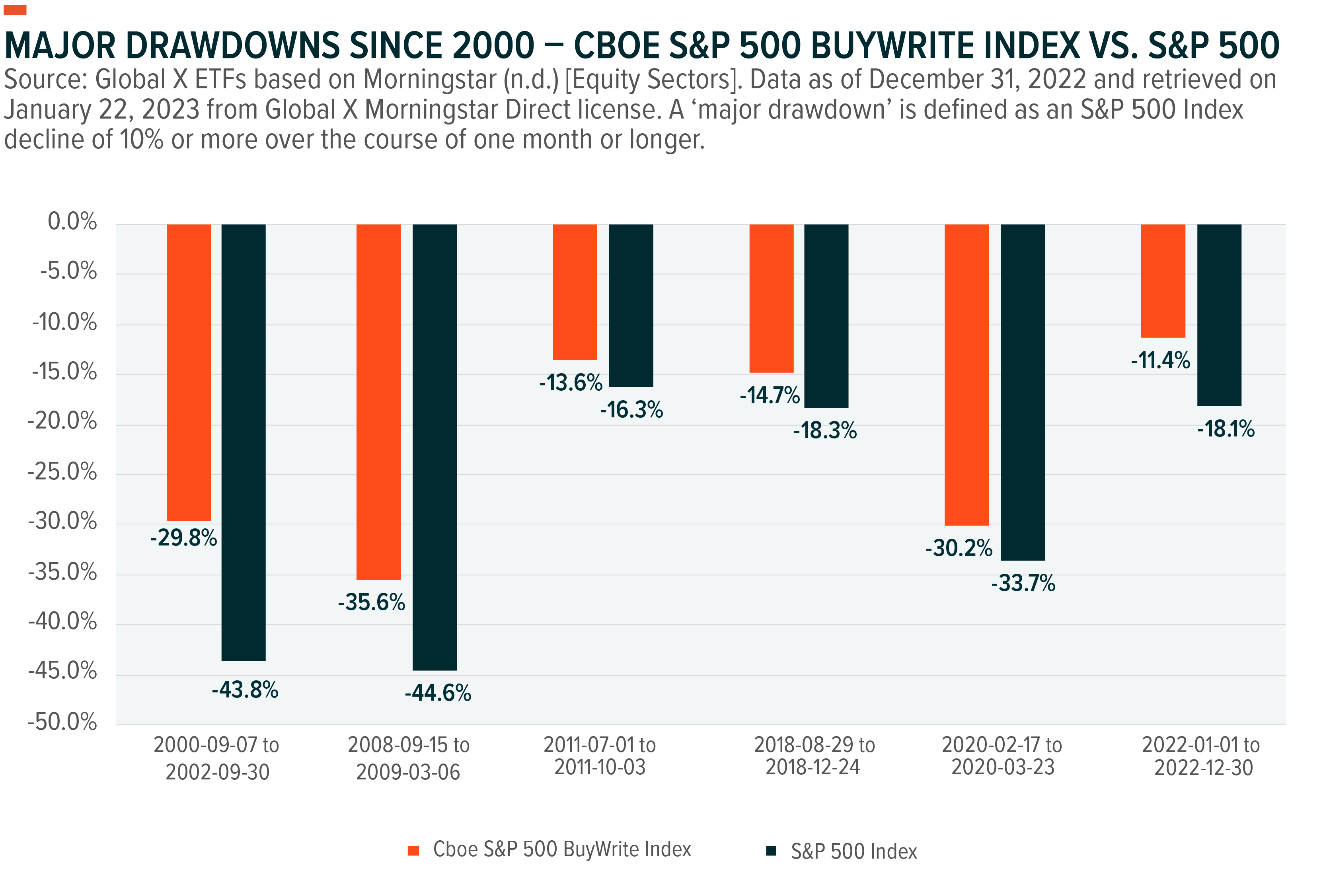

Covered call strategies also have the potential to provide a level of volatility reduction with a portfolio. Although this type of options overlay maintains an upside cap, the premiums received can help provide a level of volatility mitigation during significant equity market downturns. Also, as discussed earlier, options premiums tend to increase in events of market stress due to higher levels of implied volatility. Due to this dynamic, options premiums have the potential to be higher. The end result, for a covered call strategy, has been lower betas relative to the equity benchmark. For example, from the beginning of 2000 through the end of 2022, the Cboe S&P 500 BuyWrite Index has demonstrated a beta of 0.66 relative to the S&P 500 index.6

How an ESG Covered Call Strategy Works

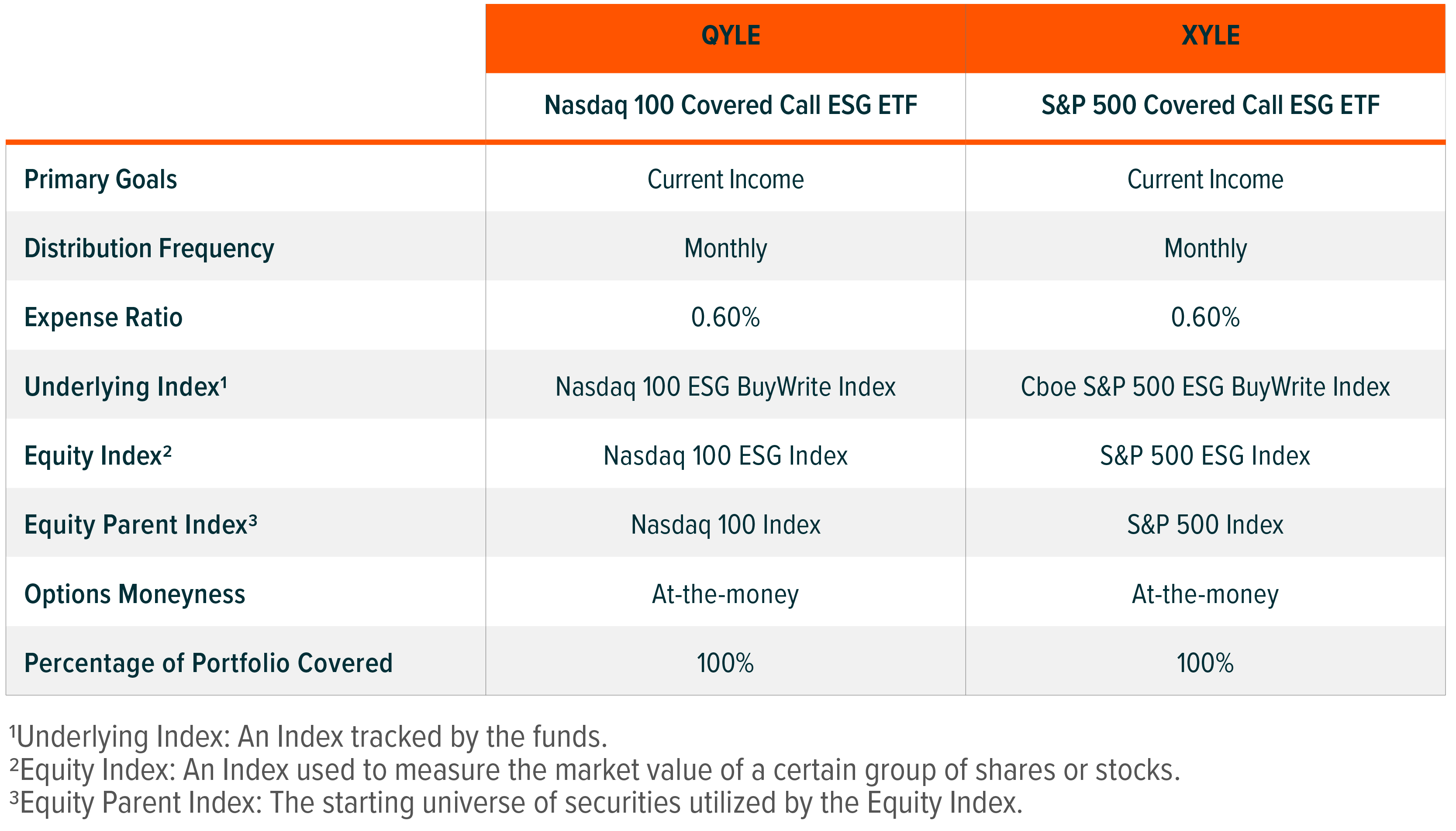

QYLE and XYLE offer investors the potential of high income while simultaneously offering the ability to suffice an ESG mandate. Similar to Global X’s other covered call ETFs, QYLE & XYLE are structured to track an index by implementing a systematic, buy/write strategy. Both ETFs are expected to purchase the securities within their equity index while seeking to generate monthly income through “at-the-money”, covered call writing on 100% of the notional exposure of the portfolios. However, both ETFs implement their call writing in a different manner.

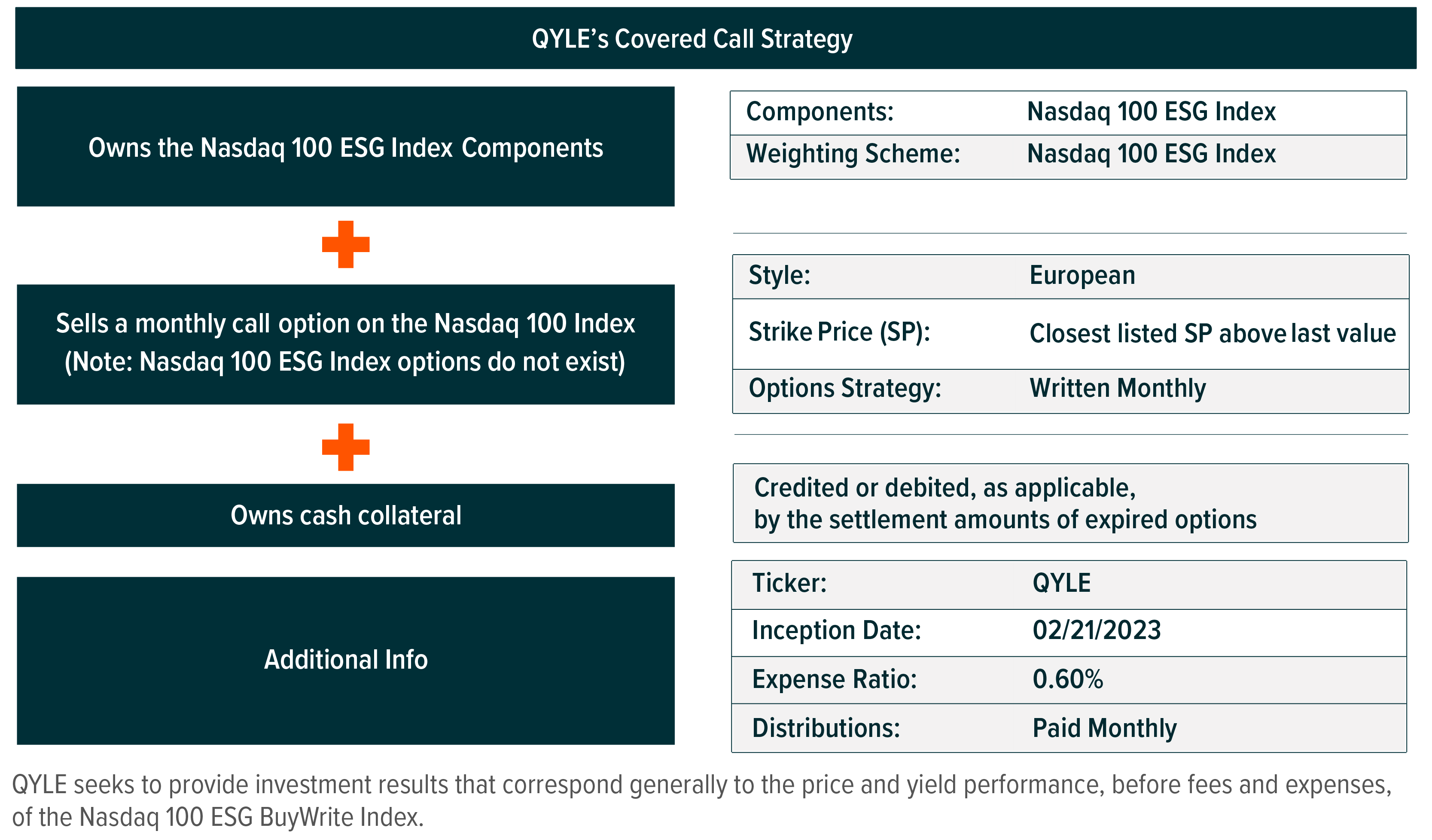

QYLE implements its strategy through the implementation of 3 primary positions:

Step 1) Purchases the underlying constituents in the Nasdaq 100 ESG Index.

Step 2) Sells an “at-the-money”, Nasdaq 100 Index (NDX) covered call option on 100% of the notional exposure of the portfolio. Utilizing European style options, the covered calls written cannot be exercised until expiration date and are settled with cash.

Step 3) Holds a collateral account holding cash and/or cash equivalents. This is needed since the options are written on a different index than the stock exposure being held “long”. The key reason for the utilization of Nasdaq 100 Index (NDX) options is that Nasdaq 100 ESG index options do not exist.

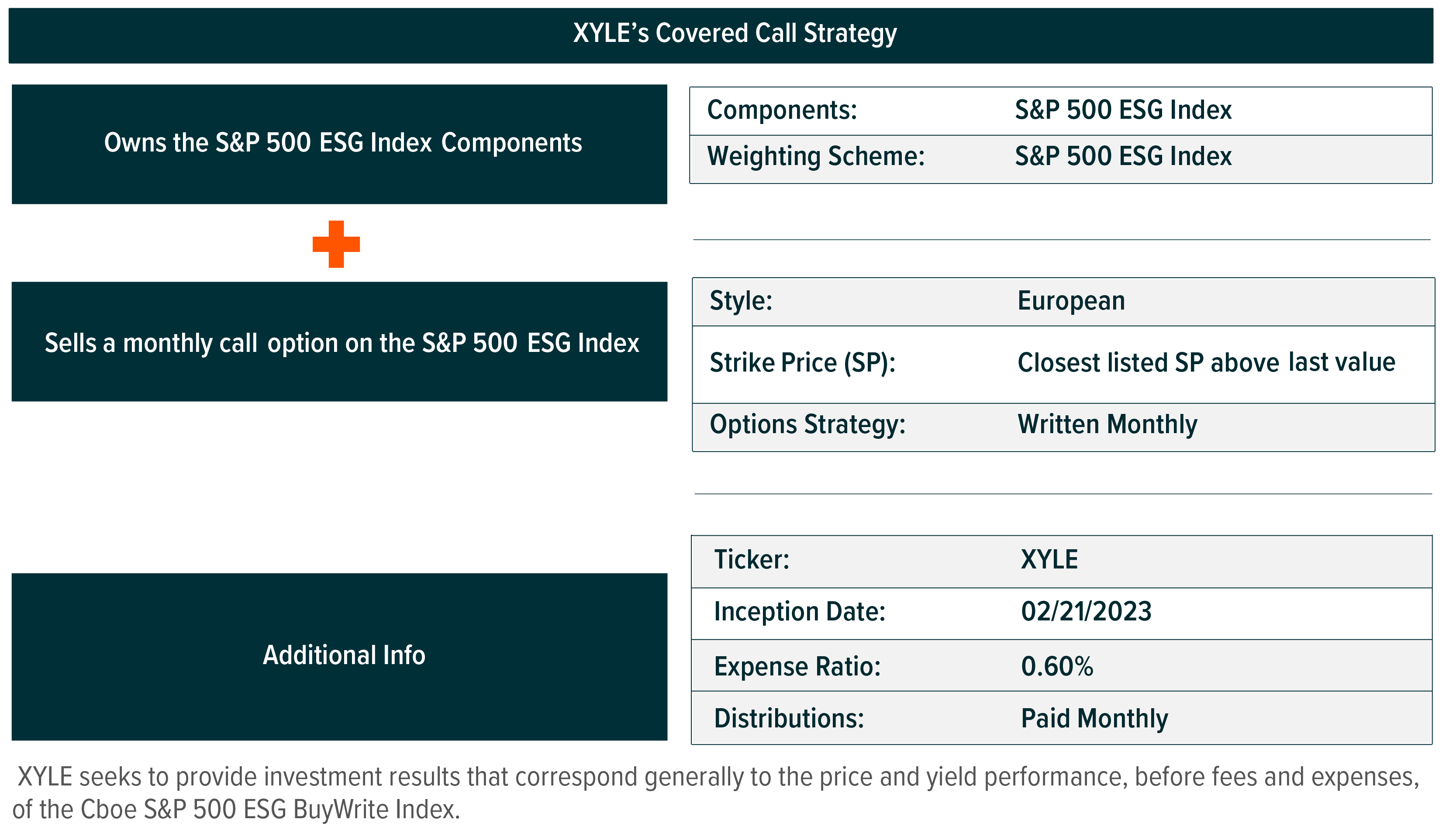

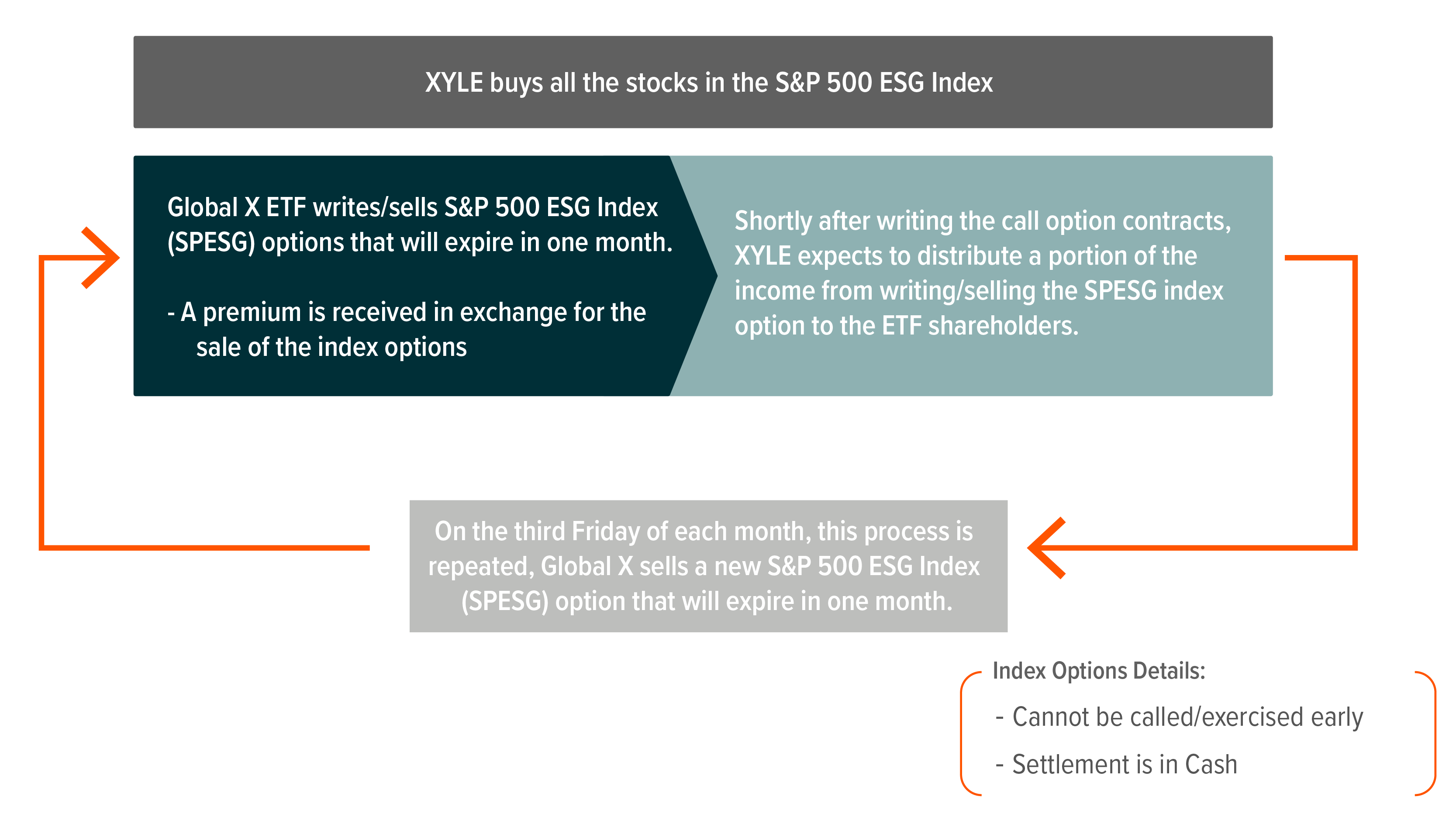

XYLE, however, implements its strategy through the implementation of 2 primary positions:

Step 1) Purchases the underlying constituents in the S&P 500 ESG (SPESG) index.

Step 2) Sells an “at-the-money”, S&P 500 ESG Index (SPESG) covered call option on 100% of the notional exposure of the reference index. Utilizing European style options, the covered calls written cannot be exercised until expiration date and are settled with cash.

Each fund accesses the index options market and are structured to roll their covered call exposures on the 3rd Friday of every month. Shortly after receipt of the monthly premium, both QYLE & XYLE are expected to conduct monthly distributions which are to be capped at half of premiums received or 1% of each fund’s NAV, similar to other Global X covered call strategies. In addition, any excess premium is anticipated to be reinvested back in each fund.

Implementing an ESG Covered Call Strategy

Implementing an ESG Covered Call Strategy

Despite strong returns over the past decade, the market is at a bit of a crossroads. If interest rates and credit spreads continue to rise, it could provide headwinds for traditional sources of income. Also, investor appetite towards ESG-aligned, index-based investments has continued to increase.

For the last decade, income investors have struggled to find diversified sources of income for their portfolios. Fast forward to today, in this current rising rate environment, traditional sources of income like dividend paying equities and fixed income solutions present additional risks that investors may be seeking to minimize or avoid all together. For investors considering how to add to a portfolio, investors could consider an ESG covered call ETF as a partial replacement to ESG-aligned equity and fixed income strategies. ESG-aligned, dividend equity strategies might have equity sector concentration that can potentially be minimized by the equity exposures offered by an ESG covered call ETF.

For ESG investors who are seeking to lower their equity portfolio beta, a buy/write strategy on a ESG equity index can potentially provide a lower level of volatility as opposed to obtaining exposure to the same stock index outright.

As investors are increasingly looking to diversify their portfolios across different asset classes with unique investment mandates, our launch of ESG covered call ETFs looks to provide investors the potential of both high income paired with managing ESG risks.

Related ETFs

QYLE – Global X Nasdaq 100 ESG Covered Call ETF

XYLE – Global X S&P 500 ESG Covered Call ETF

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.