Today, we launched the Global X Russell 2000 Covered Call ETF (RYLD), adding a third fund to our covered call suite, which also consists of the Nasdaq 100 Covered Call ETF (QYLD) and the S&P 500 Covered Call ETF (HSPX). The Global X covered call suite recently crossed $500 million in assets, highlighting strong investor interest in these strategies, which can generate both yield and mitigate the risk of rising volatility.

The launch of RYLD brings an at-the-money covered call-writing strategy to the US small cap space. The fund gains exposure to the stocks in the Russell 2000 and simultaneously sells a call option on the Russell 2000 index. The fund collects the premium received from selling this option in exchange for forfeiting the upside appreciation of the Russell 2000.

RYLD follows a similar approach to the Nasdaq 100 Covered Call ETF (QYLD), which writes at-the-money covered calls on the Nasdaq 100 Index. Both RYLD and QYLD sell monthly index options that are written at-the-money, and rolled over each month.

To give a refresher on index options, which can be quite different from single stock options, below is a brief summary of their important characteristics.

Below is a description of how RYLD’s covered call-writing process works:

- RYLD sells Russell 2000 Index options (RTY) to a counterparty that will expire in one month

- A premium is received in exchange for the sale of the index options

- At the end of the month, RYLD seeks to distribute a portion of the income from writing/selling the RTY index option to the ETF shareholders

- At the beginning of each new month this process is repeated

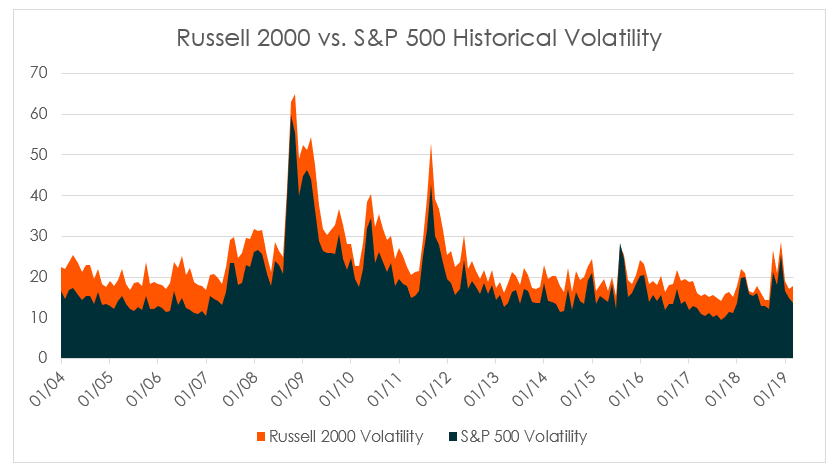

In option pricing, many factors determine the value of the premium received from selling a call option, such as the time to expiration, the strike price, the security’s current price, the risk free rate, and the security’s volatility. Since RYLD is writing at-the-money covered call options on a monthly basis, the time to expiration is one month, and the strike price is equal to the current price of the index, meaning these factors have little variation on a monthly basis in determining the option premium received. In addition, the risk free rate, particularly in the current interest rate environment, tends to be fairly stable. Therefore, the major source of variation in the value of an at-the-money option premium is volatility. The higher the volatility, typically the greater the option premium received from selling a call option. Historically, small caps, such as those tracked by the Russell 2000, have displayed greater volatility than their large cap counterparts, tracked by the S&P 500. All else equal, this implies that the option premiums for writing calls on a small cap index is expected to be higher over time than writing calls on a large cap index.

Source: Bloomberg. Measured by CBOE volatility indexes for Russell 2000 and S&P 500. Data from 1/31/04 to 3/31/19. 1/31/04 is the start of the CBOE Russell 2000 Volatility Index.

The volatility that small cap stocks display relative to the broader equity markets may lead to potentially higher option premiums, generating greater income for investors during periods of heightened volatility.

Covered call strategies can serve dual purposes in an investor’s portfolio. Alongside traditional US small cap equity exposure, covered calls can provide a measure of downside risk as the income on call writing tends to increase with higher volatility. We also believe RYLD can help investors diversify the sources of income in their portfolio. Traditionally, income portfolios, particularly on the equity side, tend to be concentrated in large caps, with tilts towards traditionally higher yielding sectors like Utilities and Real Estate. By using a Russell 2000 covered call strategy, investors can gain exposure to the small cap space as well as sectors like Information Technology and Health Care that may be underrepresented in many income-oriented strategies.

For investors looking to pare back on riskier fixed income exposures like High Yield bonds or Levered Loans, covered calls can serve as a potential replacement. One potential advantage of covered calls is that the strategy generates income primarily from volatility, meaning it has a very low duration risk.

We believe the multi-faceted uses of a Russell 2000 covered call strategy warrant a look as an alternative approach to generating income and diversifying exposure in an environment where market volatility is expected to pick up in the future.

Related ETFs:

RYLD: The Global X Russell 2000 Covered Call ETF (RYLD) follows a “covered call” or “buy-write” strategy, in which the Fund buys exposure to the stocks in the Russell 2000 Index and “writes” or “sells” corresponding call options on the same index.