A fund with over 25% of its assets invested in Master Limited Partnerships (MLPs) does not qualify as a Regulated Investment Company (RIC) and instead, is structured as a ‘C-Corporation’ (C-Corp). As a result, these funds, which include ETFs, Mutual Funds, and Closed End Funds, must accrue corporate level taxes on the appreciation of the fund’s holdings. As the fund accrues a ‘tax liability’ in a bull market, the performance of the investment vehicle will lag its underlying components.

Hypothetical Performance of MLP Index vs. MLP Index Fund in Bull Market

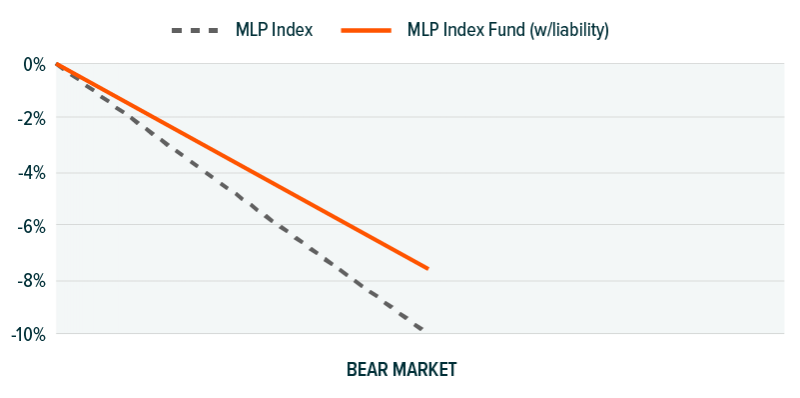

Should the market turn negative after a bull market, a fund can use its tax liability to offset future losses in the fund, providing a buffer on the way down. The buffer only works, however, if the fund has already accrued a tax liability from prior market appreciation.

Hypothetical Performance of MLP Index vs. MLP Index Fund in Bear Market after Bull Market

If the fund is new, or has already exhausted its tax liability from a sustained bear market, the fund’s performance will begin to trade in-line with its index on the way down. Because the fund’s future performance is influenced by whether or not it has previously accrued a tax liability, returns are considered path dependent.

Hypothetical Performance of MLP Index vs. MLP Index Fund with Tax Liability in a Bear Market

If the fund does not have a tax liability and continues to fall, it will accrue a ‘tax asset’ which can be used to offset future gains until the asset is exhausted. This means that the fund will trade in-line with the index on downward movements, and in-line on upward movements, until the tax asset reaches zero. Beyond this ‘zero’ point, upwards movements will result in the fund accruing a tax liability, and the fund will experience tax drag.

Hypothetical Performance of MLP Index vs. MLP Fund in Bull Market after Bear Market

Conclusion

Future performance of an MLP fund can depend on its previous price movements, which determine whether it has a tax asset, a tax liability, or is at its ‘zero’ point.

- A fund with a tax asset will closely replicate its underlying index in a bear, as well as a bull market until it reaches its ‘zero’ point. Further upward movements beyond this point will result in the fund accruing a tax liability and it will lag the index.

- A fund with a tax liability will lag the index in a bull market, but fall by less than the index in a bear market until it reaches its ‘zero’ point. Downward movements beyond its zero point will be in-line with the index and the fund will accrue a tax asset.

- A fund at its ‘zero’ point will accrue a tax liability in a bull market and lag the index, or accrue a tax asset in a bear market and trade in line with the index.

All else being equal, an investor that is bullish on the MLP space would prefer to own an MLP index fund with a greater tax asset as a percentage of the fund’s total assets. A greater tax asset results in higher upside potential in a future bull market compared to a fund with a lesser tax asset, a fund at its zero point, or a fund with a tax liability.