Rohan Reddy

Rohan ReddyDespite generally positive attitudes towards the global economy heading into Q1 2020, the quarter unraveled due to an unprecedented black swan event. The Covid-19 global pandemic shocked the world, disrupting our personal and professional lives, and paralyzing the global economy. The full repercussions of the virus are still unknown as the central banks and governments around the world scramble to contain its spread, maintain order in financial markets, and support affected businesses and individuals.

While seemingly only tangentially related to a viral outbreak, a confluence of plummeting demand and state-led decisions to flood the world with oil supply has made the Energy sector one of the most affected areas in the investing world. In this piece, we discuss the performance drivers of the Energy and midstream space. We also provide a tentative outlook for energy infrastructure, considering this new and rapidly changing environment.

- The Macro Picture: How Did We End Up Here?

- The Impact on MLPs & Midstream Companies

- Implications for MLP Distributions & E&P Credit Risk Assessment

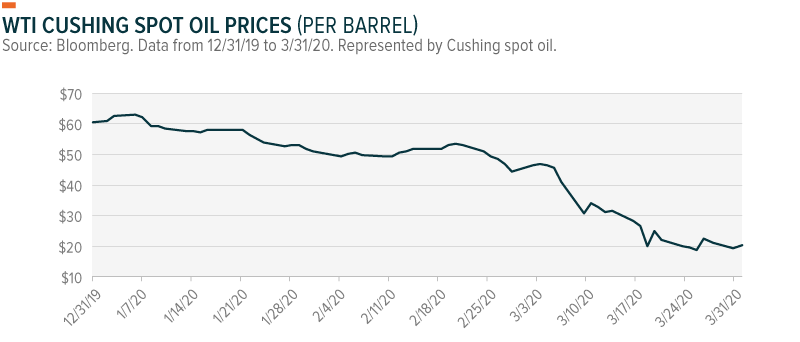

Oil Began on Weak Footing

Oil began the year on weak footing given uncertain demand amidst a weak global economic backdrop. Production quotas put in place by OPEC+ (whose members include OPEC leaders like Saudi Arabia and other large non-OPEC members like Russia) helped keep just enough of a lid on supply to support oil prices in the $50-60/barrel range. Additionally, the phase one trade deal between China and the US and the completion of Brexit provided some guidance to the markets about the direction of global trade.

Yet as the novel Coronavirus began to spread in China in January, Beijing limited travel and shut down factories to prevent further infections; a move that resulted in an estimated 4 million barrels per day (bpd) plummet in oil demand. This demand shock put further pressure on OPEC+ to extend and increase production limits to avoid oversupplying the global oil markets.

OPEC+ Fallout – Nothing Holding Back Supply

OPEC+ held a meeting on March 6th that failed to produce an agreement to extend or increase existing supply cuts. While Saudi Arabia proposed an extension of the existing 2.1m bpd supply cuts, plus an additional 1.5m bpd cut, the Russian delegation refused to participate. Saudi Arabia became furious with Russia’s unwillingness to collaborate and initiated an all-out price war. The Saudis marketed oil at a significant discount to prevailing crude prices, evoking techniques employed back in 2014-2016 when the oil market fell from over $100 per barrel to below $30. This time around, the move has been even more devastating to oil prices. By the end of March 2020, oil prices hovered near $20/barrel, their lowest level in 17 years.

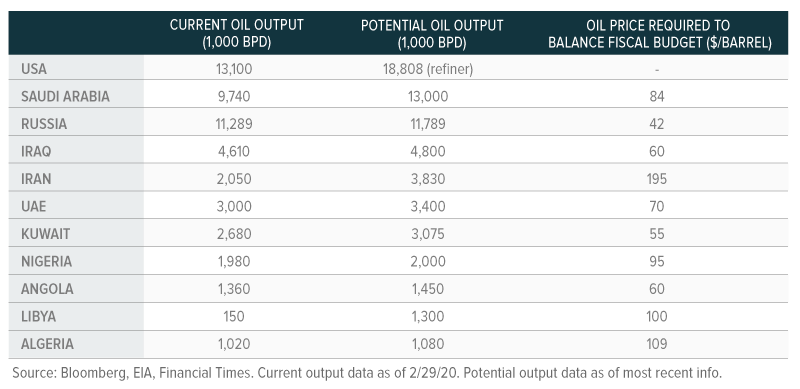

Output within Saudi Arabia is ramping up, with the kingdom able to add more than 3m bpd to its previous output levels. Other large producers like the UAE, Kuwait, and Iraq could add 1m barrels total between them. And Russia can add around 500,000 barrels. Due to the inelasticity of much oil demand, an oversupplied market can dramatically reduce prices without tempting much increase in demand.

A War of Attrition

Some think Saudi Arabia grew tired of leading efforts to limit supply among the OPEC+ group and wanted to flex their muscles. Others believe Russia wanted to induce a price war to retaliate against US efforts to block their Nord-stream 2 pipeline to Germany. Other theories hold that the Saudis and Russians both wanted to squeeze US oil & gas producers, who became the largest source of output in the world as a result of the shale revolution.

Regardless of the motivations, as oil supply floods the global market, the ensuing low prices will damage government and corporate budgets and induce a war of attrition. The question is who can survive the longest. The Russian economy may be more resilient to low oil prices, despite 60% of exports and 30% of GDP coming from oil and gas. Saudi Arabia, for comparison, generates 50% of its GDP from oil and petroleum accounts for 85% of its government budget that funds various domestic social programs. But both countries have low breakeven costs and may be compelled to prolong the price war to force the hands of US shale producers that rely heavily on external capital to stay afloat.

How does this impact the Energy Sector and Midstream MLPs & Energy Infrastructure Companies?

With oil’s fall to nearly $20/barrel, upstream producers sold off aggressively, as they have the most exposure to spot oil prices. The Exploration & Production Index is down -65% year to date, while the midstream segment has fallen -59%, and refiners are down -40%.1 Upstream firms are capital-intensive businesses which rely heavily on debt financing to build rigs and produce oil and gas, which is then sold at spot prices. While some E&Ps may hedge their commodity exposure, those with higher breakeven costs will likely not survive extremely low prices for an extended period given their debt burdens.

Midstream MLPs and energy infrastructure companies (EICs) transport and process the oil & gas produced by the E&Ps. They are compensated based on volume, which insulates them from the day-to-day movements in commodity prices. Yet at the extremes, such as when low energy prices threaten the going concern of E&Ps, MLP volumes can be at risk. Historically, this has resulted in MLPs exhibiting higher correlation with energy stocks when oil prices are at lower levels.

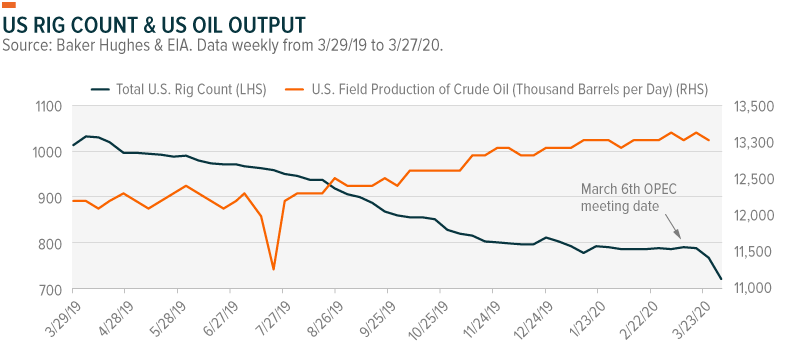

Going forward, the key question for MLPs and EICs is how much oil output declines in the US, and for how long. This could come in the form of temporarily idling rigs until energy prices recover, or more disruptively, bankruptcies of upstream firms, which could have longer-term ramifications.

Recent drawdowns in MLP and EIC indexes indicate that the market increasingly fears midstream revenues will decline as a result of an upstream production downturn. This risk is more pronounced among MLPs with a more concentrated customer base (ex: dropdown MLPs or single customer MLPs). In addition, more indebted companies could be at greater risk because historically capital markets have ceased equity and debt issuance for Energy firms in similar stressed environments.

Where Does Oil Go From Here & What Are The Key Factors?

- Supply Side – OPEC+ Relations: While the results of the recent OPEC+ meeting signal damaged relations between the two of the three largest oil producers in the world, OPEC+ holds the keys to ending the oil price war. Should Saudi Arabia and Russia renegotiate a production quota to support higher oil prices, the market could normalize quickly. In addition, other producers around the world may find it uneconomical in this low price environment to produce oil and voluntarily cut back operations, supporting higher prices.

- Demand Side – Covid-19 Recovery: Oil demand remains under substantial strain as commuters stay home and travelers avoid airports. In the US, approximately 45% of oil demand comes from motor gasoline and another 8% from air travel.2 Should the spread of the novel coronavirus slow due to containment efforts, weather changes, or other factors, the global economy can begin to ramp up and consume more oil. China’s recent partial resumption of economic activity could provide insights into a potential timeline for how soon North America and Europe can expect a return to normalcy.

- Energy Prices – How Low, for How Long: The supply and demand factors named above will ultimately play a decisive role in dictating oil prices. If prices remain below $40 per barrel, US producers will struggle to meet their breakeven costs. The longer prices remain at these levels, the more severe E&P production cuts will be. If prices remain low for long enough, supply could be forced out of the market through E&P bankruptcies.

From 2014-2016 when OPEC adopted a similar approach, it didn’t end well for many countries or heavily indebted private producers. Yet at the same time, US oil production grew its overall market share at the expense of OPEC’s. This demonstrated that the US is one of the world’s lower cost producers and may be able to weather the storm longer than higher cost producers like Iran, Nigeria, and Algeria, whose fiscal budgets rely heavily on elevated oil prices.

MLP Valuations & Fundamentals

MLPs, at the end of the day, are transport and storage-based businesses paid on volume. While oil production could be cut in the near future, the US’s energy independence remains a long-term strategic priority and many producers in the US are competitive at a global level. Therefore, we believe midstream energy is likely to survive this downturn either via competitive market forces or under extreme stress, with government support.

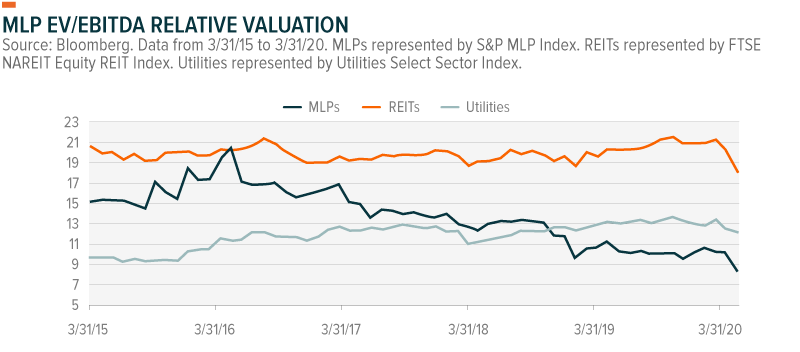

Currently, many MLPs feature double digit yields and are trading at an Enterprise Value to Earnings Before Interest, Taxes, Depreciation, Taxes, & Amortization (EV/EBITDA) of 7x, which is lower than in February 2016 when oil prices were at similar levels. Such valuations may prove to be an attractive entry point as any positive catalysts could spur strong valuation expansion.

It’s also important to remember that the MLP model is different, and more sustainable today than in 2014-2016. At that time, MLPs financed projects externally, taking on substantial debt burdens and returning virtually all cash flow to investors. Nowadays, MLPs retain more cash flow to self-fund capex and reduce debt, improving overall balance sheet quality. This could be why we are seeing significant insider buying form MLP management teams; a positive indication that they view units as being undervalued by the broader markets.

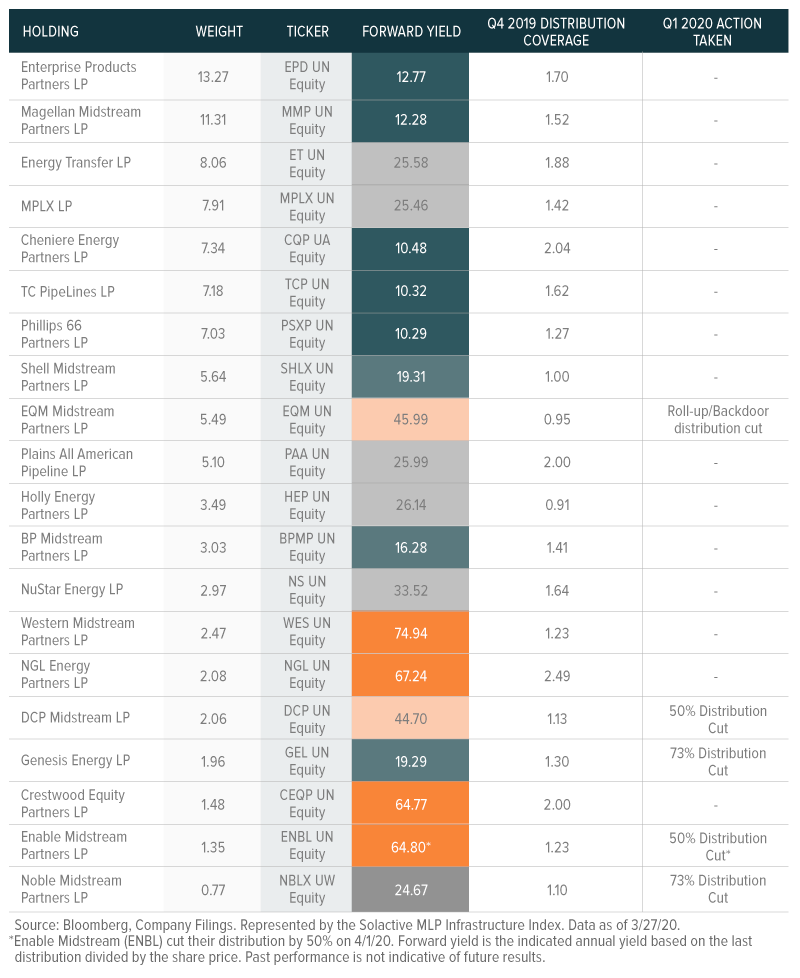

Distribution Cuts Could Continue, But Not All Are Signs of Weakness

If oil remains below $30 for an extended period, it’s possible MLPs could experience declines in revenues and volumes from their upstream E&P counterparties. Such a decline could impact the MLP’s ability to cover their distribution and potentially result in cuts. It’s important to note, however, that in recent years many MLPs increased their distribution coverage ratios and therefore may have a greater buffer against cutting their distributions than they did in 2016.

MLPs that may be on stable footing could also cut their distributions if they think the market is not rewarding their high yield. Many MLPs are now yielding in excess of 20%, which is unlikely to be maintained by their management teams. While such distribution cuts could be painful for investors expecting that income, they could benefit investors from a total return perspective over the long term. It is likely that an MLP would put that saved cash to work by either reducing debt to improve the quality of their balance sheet, or buying or developing new assets to improve growth prospects.

So far, 4 midstream MLPs (DCP, NBLX, GEL, & ENBL) and 2 midstream C-Corp taxed entities (TRGP, ENLC) cut their distributions.

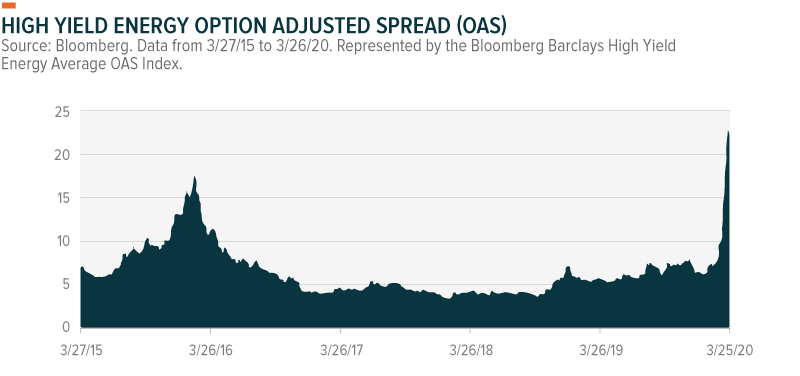

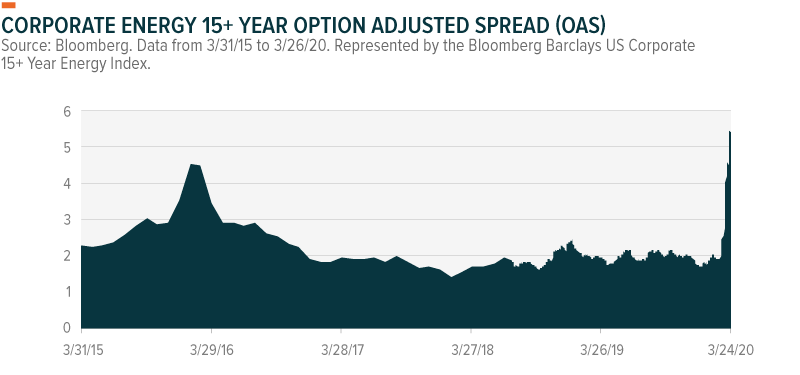

E&P Credit Risk is Worth Watching

Midstream MLPs and corporates depend on the going concern of their E&P customers as bankruptcies can take volume offline or nullify contracts. This is especially true for MLPs with a narrow customer base, such as smaller MLPs and dropdown MLPs. Default risk among E&Ps is priced higher now than in 2015 and early 2016 when oil prices were at similarly low levels. E&Ps may ask for relief from midstream service providers in the form of transportation rate reductions. While this could lead to lower revenues for the midstream space, it may prevent broader bankruptcies within the Energy complex. The option adjusted spread (OAS) below is a type of yield spread that takes into account options features on bonds.

Exploration & Production (E&P) Credit Default Swap (CDS) Spreads

Below is a table of E&P CDS spreads right now and compared to historical levels. CDS spreads can be thought of as the cost of insuring a company’s debt. The cost rises when companies are considered more credit risky.

Conclusion

The world is flooded with oil during a period of an extraordinary shutdown of the global economy. This confluence of events has quickly sprung enormous pressure on oil prices, threatening many energy companies around the world. While midstream MLPs and energy infrastructure companies should typically be more insulated from day-to-day price movements in oil, the current environment threatens oil production volumes, and therefore impacts MLP revenue expectations. At the same time, the rapid selloff in virtually all Energy-related assets places valuations of even the highest quality MLPs in uncharted territory.

While the backdrop may look bleak, there is little doubt that the market has priced in its worst fears for the Energy sector. A positive catalyst such as a sooner-than-expected resumption in economic activity, support from government stimulus packages, resilient US producer volumes, or an OPEC+ production quota agreement, could therefore spur a significant recovery in valuations. In this environment, we believe it is wise to maintain exposure to the larger, more integrated MLPs and energy infrastructure companies as they tend to have more client and geographic diversification, as well as higher quality balance sheets.

Related ETFs

MLPA: The Global X MLP ETF invests in some of the largest, most liquid midstream Master Limited Partnerships (MLPs).

MLPX: The Global X MLP & Energy Infrastructure ETF is a tax-efficient vehicle for gaining access to MLPs and similar entities, such as the General Partners of MLPs and energy infrastructure corporations.

Please click the fund names above for current fund holdings and important performance information. Holdings are subject to change.