Rohan Reddy

Rohan ReddyIn recent years, Q4 has not been kind to midstream energy, and 2019, so far, has not been an exception. Yet despite shorter term headwinds, like tax loss selling pressure, we remain optimistic for the asset class over a longer time frame as fundamentals and valuations continue to contradict recent price trends. In this piece, we discuss a variety of relevant near- and medium-term topics affecting the midstream energy space, including:

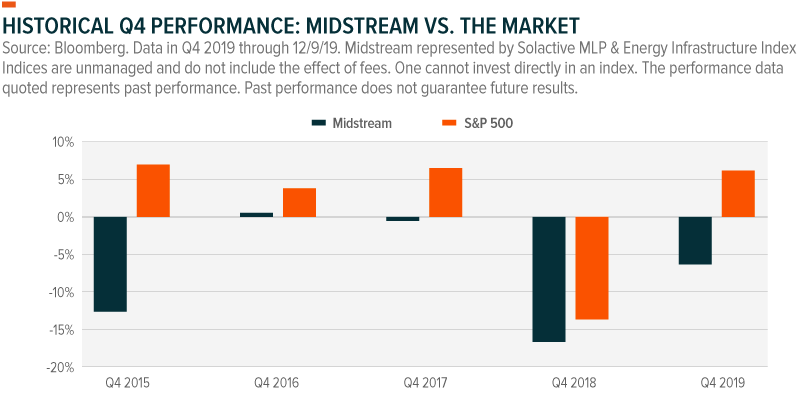

- Seasonal Q4 selling pressure affecting near term returns: the energy sector’s underperformance made it a prime target for tax loss harvesting, leading to near term headwinds

- Fundamentals show strong corporate performance that defies price movements: industry fundamentals like revenues, coverage ratios, & earnings remain on solid footing, but certain basins and upstream counterparties could introduce challenges

- Outlook for 2020 remains optimistic: A variety of improving macro factors, receding technical pressures, and solid operating results leads us to a positive 2020 outlook

Seasonal Q4 selling pressure affecting near term returns

The decade-long bull market left few sectors behind, but Energy was the outlier, with the sector underperforming the S&P 500 by over 82% the last five years.i Strong performance across broad equity indexes and fixed income left little opportunity to tax loss harvest, or sell investments at a loss to offset realized gains in other areas of one’s portfolio. With Energy underperforming, however, much tax loss harvesting was concentrated on the sector and its sub-industries like midstream oil & gas, amounting to substantial selling pressure on the sector around year end.

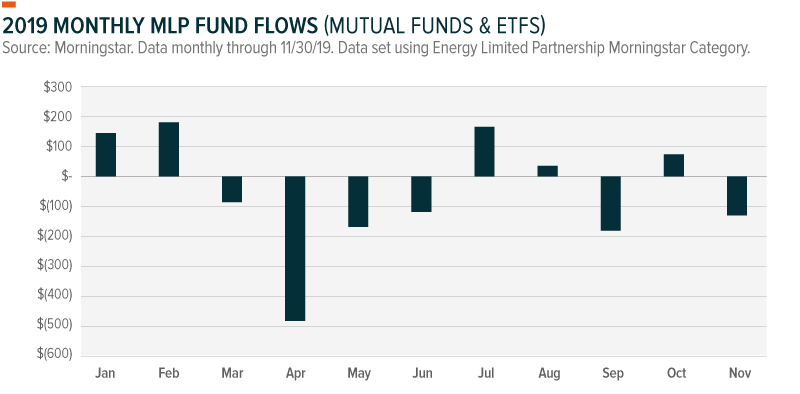

Related to tax loss harvesting, negative fund flows in the MLP space also applied selling pressure to the space. Over $3 billion left MLP funds in the trailing 12-month period, including more than $1 billion in outflows over the past 3 months.ii Considering MLP funds manage $45 billion in assets for an asset class with ~$450 billion in free float market cap, fund flows can impact share prices in the near term.iii Flows are not being felt equally across the industry, though. At Global X, our two MLP ETFs saw a combined $114 million in net inflows during this timeframe.iv Investors may be growing increasingly wary of underperformance from active managers, high fees, or exposure drift.

Fundamentals show strong corporate performance that defies price movements

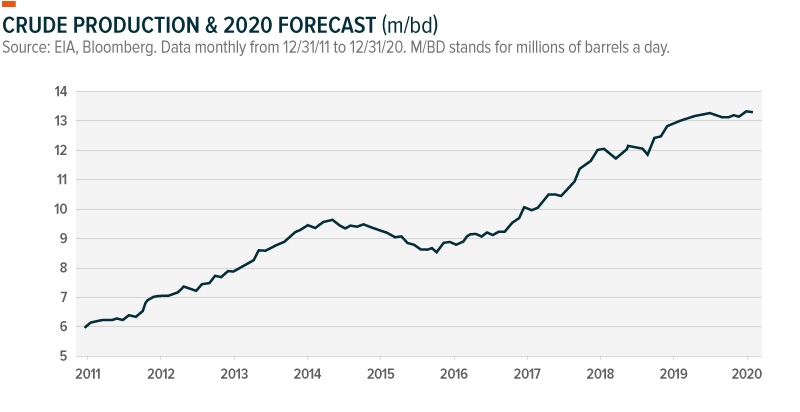

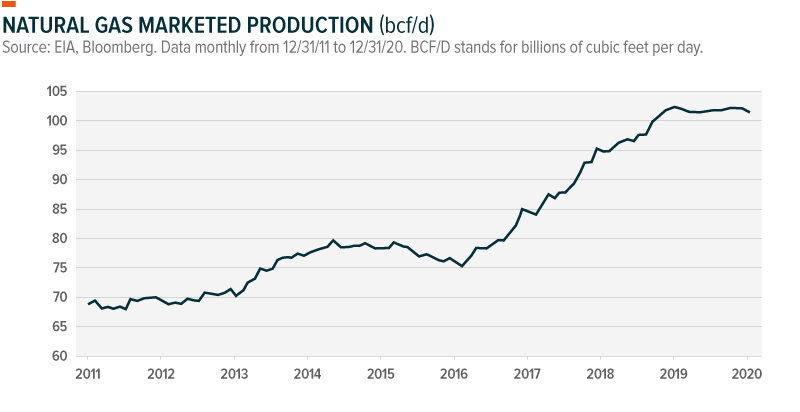

Despite near term selling pressures, the midstream energy complex’s fundamentals have routinely defied price movements. US oil production grew by 10%, crude exports grew by 6%, and liquified natural gas exports nearly doubled, utilizing nearly all pipeline capacity to transport oil and gas around the country.v Dividend coverage ratios for the asset class are cushioned by 30% on average and price-to-cash flow valuations are trading at early-2016 levels of 5x when oil prices were hitting rock bottom.vi This leaves room for potential multiple expansion, but sentiment is detracting from the operating results.

With strong cash flows and low valuations, private equity firms are circling the space for buyout opportunities. But these seemingly positive catalysts have not resulted in a sustained rally.

Midstream fundamentals enjoyed a sustained boost from increasing US energy production, but there’s evidence the hypergrowth period of production may be subsiding. Shale production experienced outsized technological gains in this period that enabled oil & gas to be drilled more economically. As with any maturing industry, however, growth was bound to level off at some point, and we believe this is contributing to some of the share price declines in midstream.

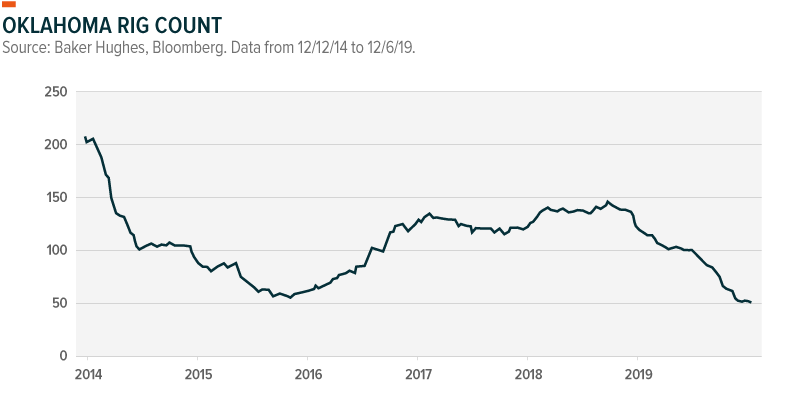

Certain basins were challenged too, with rig counts falling more drastically in those regions. The Oklahoma plays were hit by reduced capital spending and a rig drop off exceeding many of the other basins. Oklahoma midstream companies were hit harder than their peers in the index. Devon Energy (DVN) is no longer running any rigs in the STACK play in Oklahoma, crippling midstream entity, EnLink Midstream (ENLC), in the process. Enable Midstream (ENBL), another Oklahoma focused midstream company, took the brunt of this reduced Oklahoma activity too, and is underperforming its peers. These challenges seemingly overshadowed positive basin stories like the Permian, where nearly 4.7 million barrels were produced in November versus just 4 million the same time last year. Marcellus shale gas production grew 5% from last November.vii This illustrates the importance of diversifying midstream exposure across firms and basins.

Outlook for 2020 remains optimistic

In light of the fourth quarter jitters, and a rocky year overall, it’s easy for investors to become disenchanted with midstream. But the valuations and fundamentals continue to paint a compelling picture. Midstream is one of the most undervalued asset classes across the equity universe. And the strength of the cash flows and dividend coverage makes for a more positive asset class outlook in 2020.

Upstream counterparty risk & commodity prices remain our top concerns, but we’re optimistic for multiple reasons. A drilling slowdown appear already priced in and financiers are limiting capital issuance to upstream producers in search of free cash flow and returning capital to shareholders. Drillers will be forced to live within their means and take more prudent economic steps. Breakeven drilling levels keep falling, which helps support higher production. Most new wells can run profitability with oil trading between the high $40’s and low $50’s, and existing wells can cover operating expenses at $27-$37 a barrel across basins.viii The Saudi Aramco IPO also supports higher oil prices, as evidenced by the additional 500,000 barrel cut by OPEC+. Between a stabling global economy, a weakening dollar, a bottoming interest rate cycle, and limits on output, there are many reasons to believe the commodity markets will support stable oil prices, potentially providing the much needed confidence to revalue the MLP and midstream space higher.

Related ETFs

MLPA: The Global X MLP ETF invests in some of the largest, most liquid midstream Master Limited Partnerships (MLPs).

MLPX: The Global X MLP & Energy Infrastructure ETF is a tax-efficient vehicle for gaining access to MLPs and similar entities, such as the General Partners of MLPs and energy infrastructure corporations.

Please click the fund names above for current fund holdings. Holdings are subject to change.