Rohan Reddy

Rohan ReddyThe August MLP Monthly Report can be found here offering insights on MLP industry news, the asset class’s performance, yields, valuations, and fundamental drivers.

Summary

News:

1) In its final ruling on July 18, 2018, the Federal Energy Regulatory Commission (FERC) eased its initial ruling from March, which had disallowed the recovery of an income tax allowance (ITA) in cost of service contracts for MLPs. The final ruling allows for a recovery of an ITA for MLPs with a C-Corp parent, assuming the financials of the MLP are fully consolidated with the C-Corp parent. The ruling also eliminates refunding of the accumulated deferred income tax (ADIT) for pipelines with cost of service contracts owned by MLPs.

2) Energy Transfer Equity, L.P. (ETE) announced a roll up of Energy Transfer Partners, L.P. (ETP). ETP will merge with ETE. ETE will maintain its partnership tax status. In addition to the 11% premium buyout of ETP, the simplification eliminates ETP’s incentive distribution rights (IDRs). The transaction implies a 31% stealth distribution cut to ETP unitholders. The transaction is expected to close by Q4 2018. Energy Transfer has said they are open to a future C-Corp conversion.

3) Williams (WMB) and private equity firm, KKR & Co (KKR), announced a joint venture (JV) to acquire Discovery’s midstream business from TPG, another private equity firm, for $1.2 billion. Discovery is privately held. Under the terms of the JV, WMB and KKR will have 40% and 60% ownership rights, respectively, and Discovery will be operated by WMB.

Sources: S&P Global, FERC, Natural Gas Intelligence (NGI), Energy Transfer Equity, L.P. and Williams.

Performance: Midstream MLPs, as measured by the Solactive MLP Infrastructure Index, jumped by 6.2% as clarity by FERC on their March ruling was less inhibitive to MLPs than previously anticipated. The index has fallen -5.8% since last July. (Source: Bloomberg)

Yield: The current yield on MLPs stands at 7.67%. MLP yields remained higher than the broad market benchmarks for Emerging Market Bonds (6.33%), High Yield Bonds (6.31%), Fixed Rate Preferreds (5.59%), and Investment Grade Bonds (4.20%).1 MLP yield spreads versus 10-year Treasuries currently stand at 4.71%, higher than the long-term average of 4.36%.2 (Sources: Bloomberg, AltaVista Research, and Fed Reserve)

Valuations: The Enterprise Value to EBITDA ratio (EV-to-EBITDA), which seeks to provide more color on the valuations of MLPs, rose 4.33% last month. Since July 2017, the EV-to-EBITDA ratio has risen by approximately 7.68%. (Source: Bloomberg).

Crude Production: The Baker Hughes Rig Count went up last month to 1048 rigs, rising by 1 rig compared to last month’s count of 1047 rigs. The rig count has more than doubled since its recent low point in May 2016 of 404 rigs. US production of crude oil held flat at 10.900 mb/d in the last week of July compared to 10.900 mb/d at the end of June. (Source: Baker Hughes & EIA)

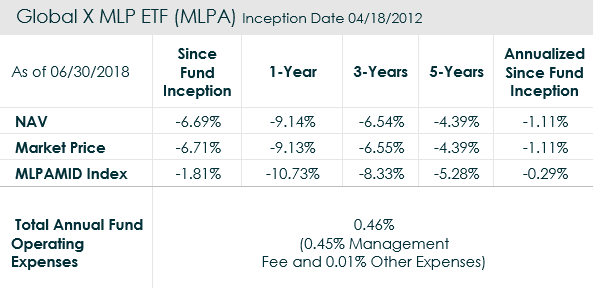

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance data current to the most recent month- and quarter-end, please click here

As of 07/31/2018, Energy Transfer Partners, L.P. (ETP) was a holding in the Global X MLP and Energy Infrastructure ETF (MLPX), with a 3.74% weighting and the Global X MLP ETF (MLPA) with a 9.80% weighting. Williams (WMB) was a holding in the MLPX ETF, with a 7.26% weighting.

MLPA ETF and MLPX ETF do not have any holding in Energy Transfer Equity, L.P. (ETE), Discovery, KKR & Co (KKR) and TPG Capital L.P. (TPG).