Rohan Reddy

Rohan ReddyThe December MLP Monthly Report can be found here offering insights on MLP industry news, the asset class’s performance, yields, valuations, and fundamental drivers.

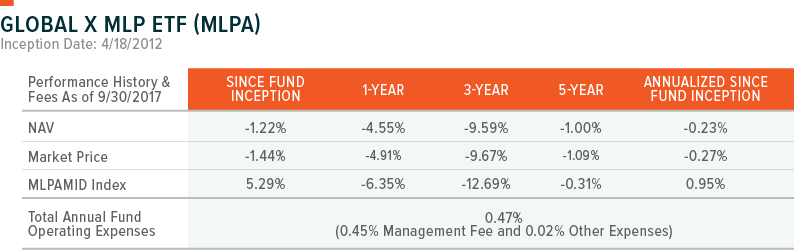

Summary

News:

1) Brent crude exceeded $64/barrel for the first time in two years, as the market tightened further due to strong demand and the continued impact of the output cuts from OPEC, Russia, and other oil exporters. OPEC raised its demand forecast for 2018 by 360k bpd to 33.42m bpd. OPEC and other oil exporters reached an agreement between on November 30th to extend oil output curbs until the end of 2018.

2) On November 13th, MPLX LP (MPLX) announced an $8.1 billion dropdown transaction from parent, Marathon Petroleum (MPC). The transaction will be funded by $4.1 billion in cash from MPLX and $4 billion in new common equity issuance to Marathon Petroleum. In addition, Marathon offered to buy out the Incentive Distribution Rights (IDRs) from MPLX. These transactions, if approved, would take effect in February 2018.

3) The U.S. House of Representatives passed a tax plan that would reduce the income tax rate from pass-through entities (including MLPs) to 25%. This measure was included to ensure that pass-throughs maintain a tax-advantaged status versus corporations, which would also enjoy a tax cut. The Senate introduced a separate tax plan for publicly traded partnerships (including MLPs) that would allow for a 23% deduction on income received from these entities.

Sources: Reuters, MPLX.

Performance: Midstream MLPs, as measured by the Solactive MLP Infrastructure Index, fell -1.86% last month as year-end MLP selling pressure continued. The index has fallen -10.83% over the last one-year period. (Source: Bloomberg)

Yield: The current yield on MLPs stands at 8.28%. MLP yields remained higher than the broad market benchmarks for High Yield Bonds (5.68%), Emerging Market Bonds (5.38%), Fixed Rate Preferreds (5.33%), and REITs (3.91%).1 MLP yield spreads versus 10-year Treasuries currently stand at 5.86%, higher than the long-term average of 3.81%. (Sources: Bloomberg, AltaVista Research, and Fed Reserve)

Valuations: The Enterprise Value to EBITDA ratio (EV-to-EBITDA), which seeks to provide more color on the valuations of MLPs, held flat last month. Since November 2016, the EV-to-EBITDA ratio has increased by approximately 17%. (Source: Bloomberg).

Crude Production: The Baker Hughes Rig Count increased last month to 923 rigs, rising by 14 rigs compared to last month’s count of 909 rigs. The rig count has more than doubled since its recent low point in May 2016 of 404 rigs. US production of crude oil rose marginally to 9.682 mb/d in the last week of November compared to 9.553 mb/d at the end of October. (Source: Baker Hughes & EIA)

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance data current to the most recent month- and quarter-end, please click here