Rohan Reddy

Rohan ReddyThe November MLP Monthly Report can be found here offering insights on MLP industry news, the asset class’s performance, yields, valuations, and fundamental drivers.

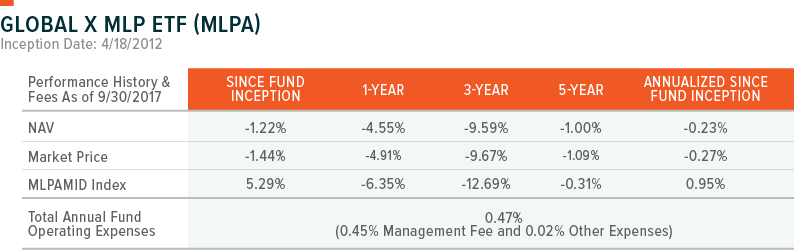

Summary

News:

1) Enterprise Products Partners L.P. (EPD) announced they would be cutting their distribution growth guidance in half, raising distributions by $0.0025 a quarter instead of $0.005. This policy will be effective through 2018. Management stated their reasoning as, “You’ve not see the market rewarding the distribution growth that we have been paying out.”

2) Genesis Energy, L.P. (GEL), cut their distribution by 31%, resetting the distribution to $0.50/quarter after previously raising their distribution for 48 straight quarters. Going forward, GEL will increase its quarterly distribution by at least $0.01 per common unit.

3) Holly Energy (HEP) announced they reached an Incentive Distribution Right (IDR) buyout agreement with their General Partner, HollyFrontier (HFC), in exchange for $1.25 billion in equity common units. In addition, HollyFrontier will waive $2.5 million of limited partner (LP) cash distributions per quarter for twelve quarters, representing a total savings to HEP of $30 million.

Sources: Bloomberg, Enterprise Product Partners L.P., Genesis Energy, L.P., Businesswire, HollyFrontier Corp.

Performance: Midstream MLPs, as measured by the Solactive MLP Infrastructure Index, fell -5.38% last month as the market took a negative outlook regarding the recent changes in certain MLP distribution policies. The index has fallen -7.11% over the last one-year period. (Source: Bloomberg)

Yield: The current yield on MLPs stands at 8.08%. MLP yields remained higher than the broad market benchmarks for High Yield Bonds (5.43%), Fixed Rate Preferreds (5.32%), Emerging Market Bonds (5.30%), and REITs (3.97%).1 MLP yield spreads versus 10-year Treasuries currently stand at 5.70%, higher than the long-term average of 3.78%. (Sources: Bloomberg, AltaVista Research, and Fed Reserve)

Valuations: The Enterprise Value to EBITDA ratio (EV-to-EBITDA), which seeks to provide more color on the valuations of MLPs, fell by -1.45% in October compared to September as MLP equity prices dropped due to tapered expectations of distribution growth. Since October 2016, the EV-to-EBITDA ratio has increased by approximately 17%. (Source: Bloomberg).

Crude Production: The Baker Hughes Rig Count fell last month to 909 rigs, dropping by 31 rigs compared to last month’s count of 940 rigs. The rig count has more than doubled since its recent low point in May 2016 of 404 rigs. Rig counts may be leveling off as well economics improve and near-term upstream Capital Expenditure (CapEx) spending scales back. US production of crude oil fell marginally to 9.553 mb/d in the last week of October compared to 9.561 mb/d at the end of September, as the effects of Hurricane Nate weighed on production in the Gulf of Mexico region. (Source: Baker Hughes & EIA)

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. For performance data current to the most recent month- and quarter-end, please click here