Rohan Reddy

Rohan ReddyThe November MLP Monthly Report can be found here offering insights on MLP industry news, the asset class’s performance, yields, valuations, and fundamental drivers.

The latest quarterly MLP Insights piece providing analysis into the midstream space can be found here as well.

Summary

News:

- Enbridge and Plains acquired WES’s 15% interest in Cactus II Pipeline, LLC for an aggregate amount of $265 million. Plains and Enbridge are now the sole owners of Cactus II, with 70% and 30% ownership interests, respectively. Plains will remain the operator. Cactus II, in partnership with Enbridge’s Ingleside Energy Center, offers a premier and industry-leading solution for delivering abundant, responsibly produced North American energy supplies to the US Gulf Coast and global markets. The acquisition announced is a major development in the US Gulf Coast’s plan to streamline the flow of oil from the expanding Permian Basin to international markets.

- The G7 nations are finalizing plans to impose a cap on Russian oil prices rather than a discount to a benchmark; this will be effective from December 5. This is despite a warning from the World Bank that any plan would require the active participation of emerging-market economies, particularly China and India, the largest buyers of Russian crude. The decision is intended to ensure that sanctions imposed by the EU and the US to limit Moscow’s ability to fund its invasion of Ukraine do not choke the global oil market. This would also increase market stability and simplify compliance, reducing the burden on market participants.

- US diesel and heating oil inventories are at historic lows, forcing up costs for fuels vital to industry, freight, farming, and many families. Fuel inventories haven’t been this low since 1951. Diesel stocks are shrinking amid constant demand and increased exports to Europe to offset Russian supplies. European restrictions on seaborne Russian crude oil are set to tighten in December and be extended to refined goods in February, worsening pressure on US inventories. These changes threaten US-European bidding wars for supplies. Diesel is vital to US industry, construction, and transportation. Recent refinery closures have reduced domestic supplies. Strong product demand, low inventories, and US energy cost advantages continue to underpin refining profit margins.

Sources: Western Midstream Partners, LP. (2022, November 2). Western midstream partners, Enbridge and Plains announce Cactus ii pipeline transaction.; Slav, I. (2022, November 4). The G7 will set a fixed price on Russian oil. Oilprice.; Chu, A. (2022, November 17). US diesel and heating oil stocks scrape lows before winter. Financial Times.

Performance: Midstream MLPs, as measured by the Solactive MLP Infrastructure Index, increased by 13% last month. The index increased by 30.68% since last October. (Source: Bloomberg)

Yield: The current yield on MLPs stands at 7.22%. MLP yields remained higher than the broad market benchmarks for Investment Grade Bonds (5.93%) and lower than the Fixed Rate Preferreds (7.38%), Emerging Market Bonds (8.50%) and High Yield Bonds (9.14%).1 MLP yield spreads versus 10-year Treasuries currently stand at 2.77%, lower than the long-term average of 5.66%.2 (Sources: Bloomberg; Board of Governors of the Federal Reserve System. (2022, October 31). Preformatted package: Treasury constant maturities [Data set]. Data Download Program.)

Valuations: The Enterprise Value to EBITDA ratio (EV-to-EBITDA), which seeks to provide more color on the valuations of MLPs, increased by 7.14% last month. Since October 2021, the EV-to-EBITDA ratio is up by approximately 0.46%. (Source: Bloomberg)

Crude Production: The Baker Hughes Rig Count increased to 768 rigs, increasing by 3 rigs from last month’s count of 765 rigs. US production of crude oil decreased to 11.900 mb/d in the last week of October compared to September levels of 12.000 mb/d. (Sources: Baker Hughes. (2022, November 11). North America rig count.; U.S. Energy Information Administration. (2022, November 11). Petroleum and other liquids.)

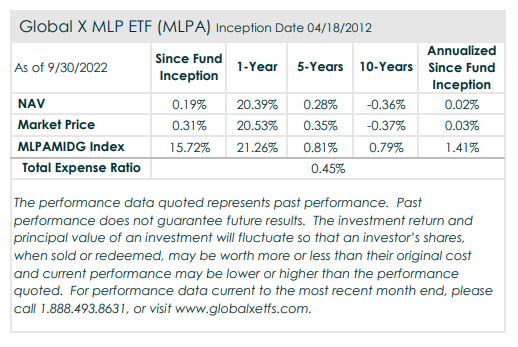

For performance data current to the most recent month- and quarter-end, please click here.

As of 10/31/2022, Western Midstream, LP (WES) was a holding in the Global X MLPA ETF (MLPA) with a 7.51% weighting. Plains All American Pipeline, LP (PAA) was a holding in Global X MLPA ETF (MLPA) with a 6.39% weighting.

MLPA does not have any holding in Enbridge, Inc (ENB), Plains GP Holdings, LP (PAGP), Cactus II Pipeline, LLC.

DEFINITIONS

Solactive MLP Infrastructure Index: The Solactive MLP Infrastructure Index is intended to give investors a means of tracking the performance of the energy infrastructure MLP asset class in the United States. The index is composed of Midstream MLPs engaged in the transportation, storage, and processing of natural resources.

S&P MLP Index: S&P MLP Index provides investors with exposure to the leading partnerships that trade on the NYSE and NASDAQ. The index includes both master limited partnerships (MLPs) and publicly traded limited liability companies (LLCs), which have a similar legal structure to MLPs and share the same tax benefits

Bloomberg US Corporate High Yield Total Return Index: The Bloomberg US Corporate High Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on Bloomberg EM country definition, are excluded.

ICE BofA Fixed Rate Preferred Securities Index: The ICE BofA Fixed Rate Preferred Securities Index tracks the performance of fixed rate US dollar denominated preferred securities issued in the US domestic market.

Bloomberg EM USD Aggregate Total Return Index: The Bloomberg Emerging Markets Hard Currency Aggregate Index is a flagship hard currency Emerging Markets debt benchmark that includes USD-denominated debt from sovereign, quasi-sovereign, and corporate EM issuers.

Bloomberg US Corporate Total Return Index: The Bloomberg US Corporate Total Return Value Unhedged Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD denominated securities publicly issued by US and non-US industrial, utility and financial issuers.

Crude Oil: Measured based on the Generic 1st ‘CL’ Future, which is the nearest crude oil future to expiration.

EBITDA: Earnings before interest, tax, depreciation and amortization (EBITDA) is a measure of a company’s operating performance. Essentially, it’s a way to evaluate a company’s performance without having to factor in financing decisions, accounting decisions or tax environments.

Average Spread: Average spread is the average of the excess of the MLPs yield over the 10 year treasuries yield.

Enterprise Value (EV): EV is a measure of a company’s total value, often used as a more comprehensive alternative to equity market capitalization.