Global X Investment Strategy Team

Global X Investment Strategy TeamAfter 11 hikes since March 17, 2022, the Federal Reserve (Fed) paused its quantitative tightening and at its December meeting, plotted a series of rate cuts in 2024. These developments create a much different outlook for fixed income markets as they introduce the possibility of a steeper yield curve. The difference between 10-year U.S. Treasury yields and 2-year U.S. Treasury yields (2s10s) was still negative as of 2023 year-end, but inflation metrics appear promising and on a downward trend. In our view, a systematic, options overlay on a fixed income portfolio using interest rate options may provide some defense as the yield curve potentially steepens.

In this scenario, the Global X Interest Rate Volatility & Inflation Hedge ETF (IRVH) may be a worthy consideration for investors looking to enhance a fixed income portfolio’s risk management capabilities.

Key Takeaways

- History tells us that the yield curve eventually “un-inverts,” and with inflation receding and interest rate cuts now part of the Fed’s dialogue for 2024, the seeds are in place for it to steepen. But timing this move is difficult, potentially leaving income investors flat-footed.

- The interest rate options market is where institutional investors often go to add a level of risk management to fixed income portfolios. IRVH offers retail investors access to this market.

- Traditional fixed income index tracking strategies are popular among income investors looking to gain core fixed income exposures. IRVH may be a suitable complement to achieve prudent fixed income portfolio diversification.

Yield Curve History Doesn’t Repeat, It Rhymes

The short end of the yield curve tends to reflect central bank monetary policy. However, long-end, nominal yields typically exhibit a term premium due to the uncertain path of inflation over the duration of a bond’s life.1 As central banks enact monetary tightening (or easing) measures to combat elevated inflation, shorter-term tenors tend to reflect higher (lower) rates quickly. All else equal, this catalyst typically lowers (increases) inflation expectations and interest rates for the longer end of the yield curve, resulting in a negative slope (positive slope) of the yield curve. The federal funds rate has historical demonstrated a -0.64 correlation with the 2s10s yield curve spread since June 1976.2

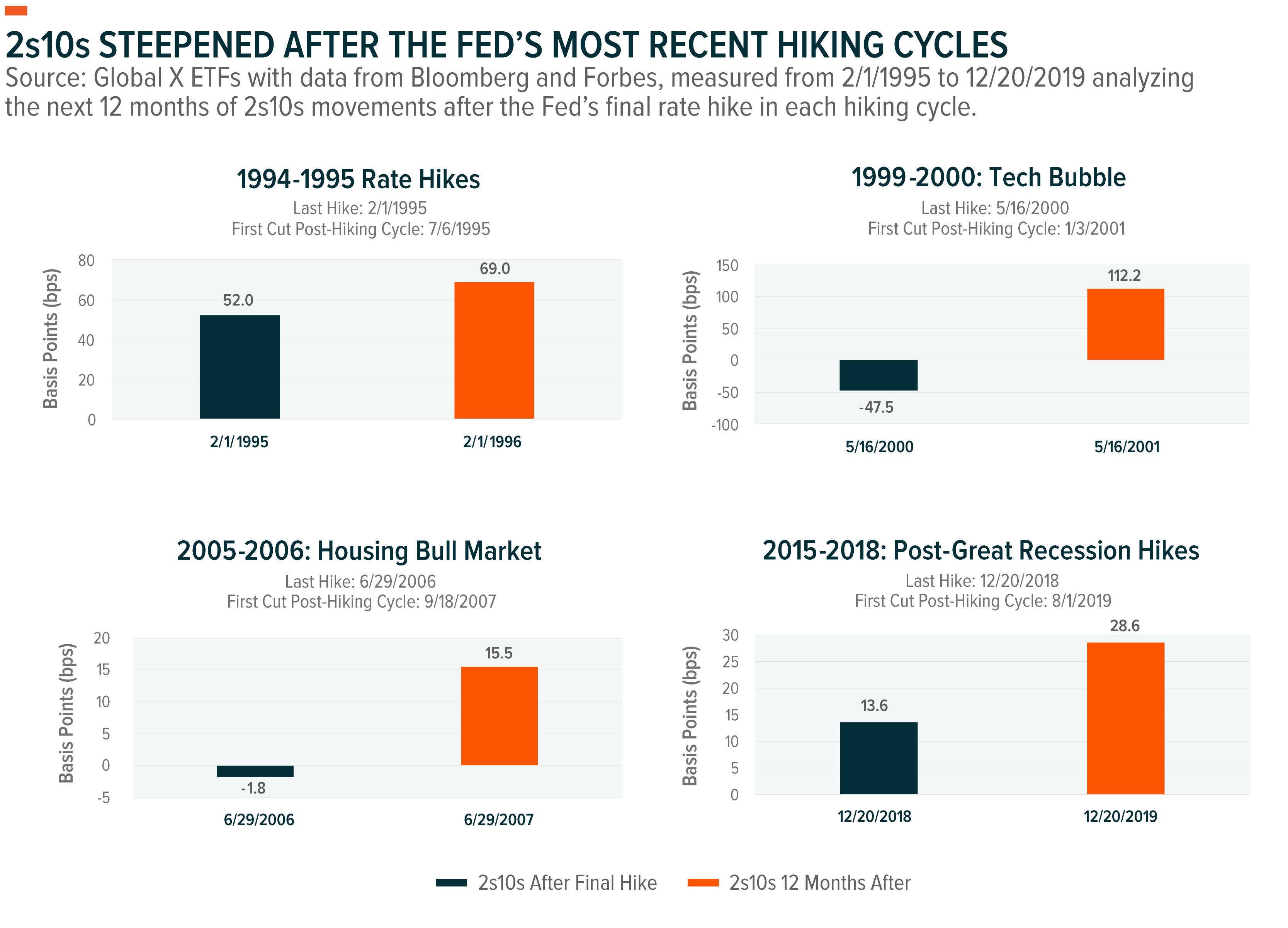

Recent Fed hiking cycles depict this dichotomy. In the 12 months following the final hike of each analyzed cycle below, three out of the four periods saw at least one rate cut and the 2s10s steepened by a median of 17 basis points.

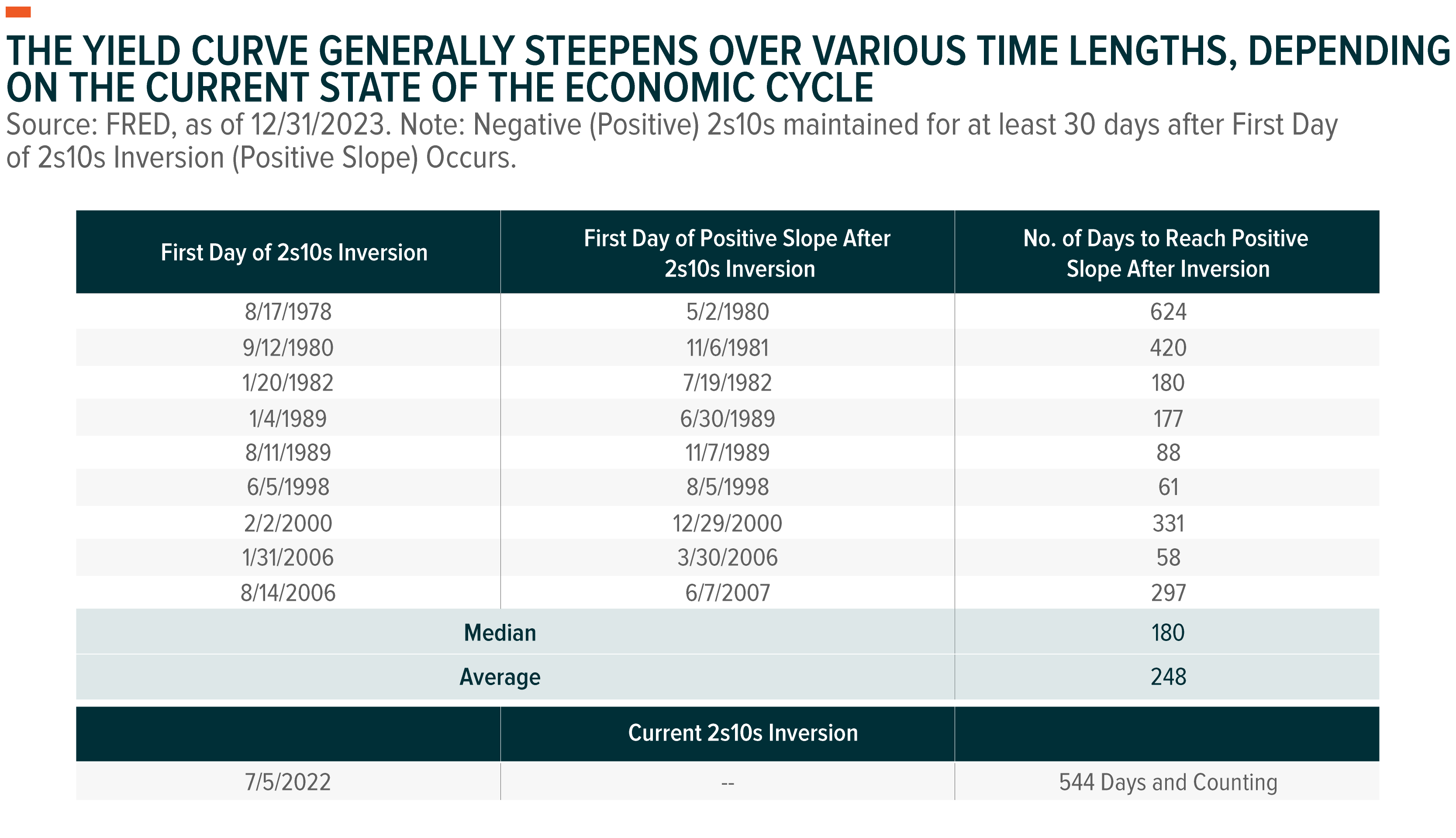

However, not all final rate hikes in the above timeframes occurred at a time when the 2s10s was inverted. The mean-reverting forces from a negatively sloped 2s10s to a positive 2s10s are difficult to pinpoint in the short term. Historically, it has taken anywhere from 58 to 624 calendar days for the 2s10s to resume a consistent, positive slope after the first day of consistent inversion. The current inversion cycle is on the higher end of the historical range. Thus, a strategic allocation to yield curve spread options may be prudent in the current environment.

IRVH May Be a Solution for a Steeper Yield Curve

The deep, U.S. dollar denominated, over-the-counter interest rate options market currently has $23 trillion in notional amount outstanding.3 Traditionally, access to this robust market was difficult for retail investors to obtain because it required a direct counterparty, such as a large bank. The Global X Interest Rate Volatility & Inflation Hedge ETF (IRVH) provides access in the form of yield curve spread option exposure.

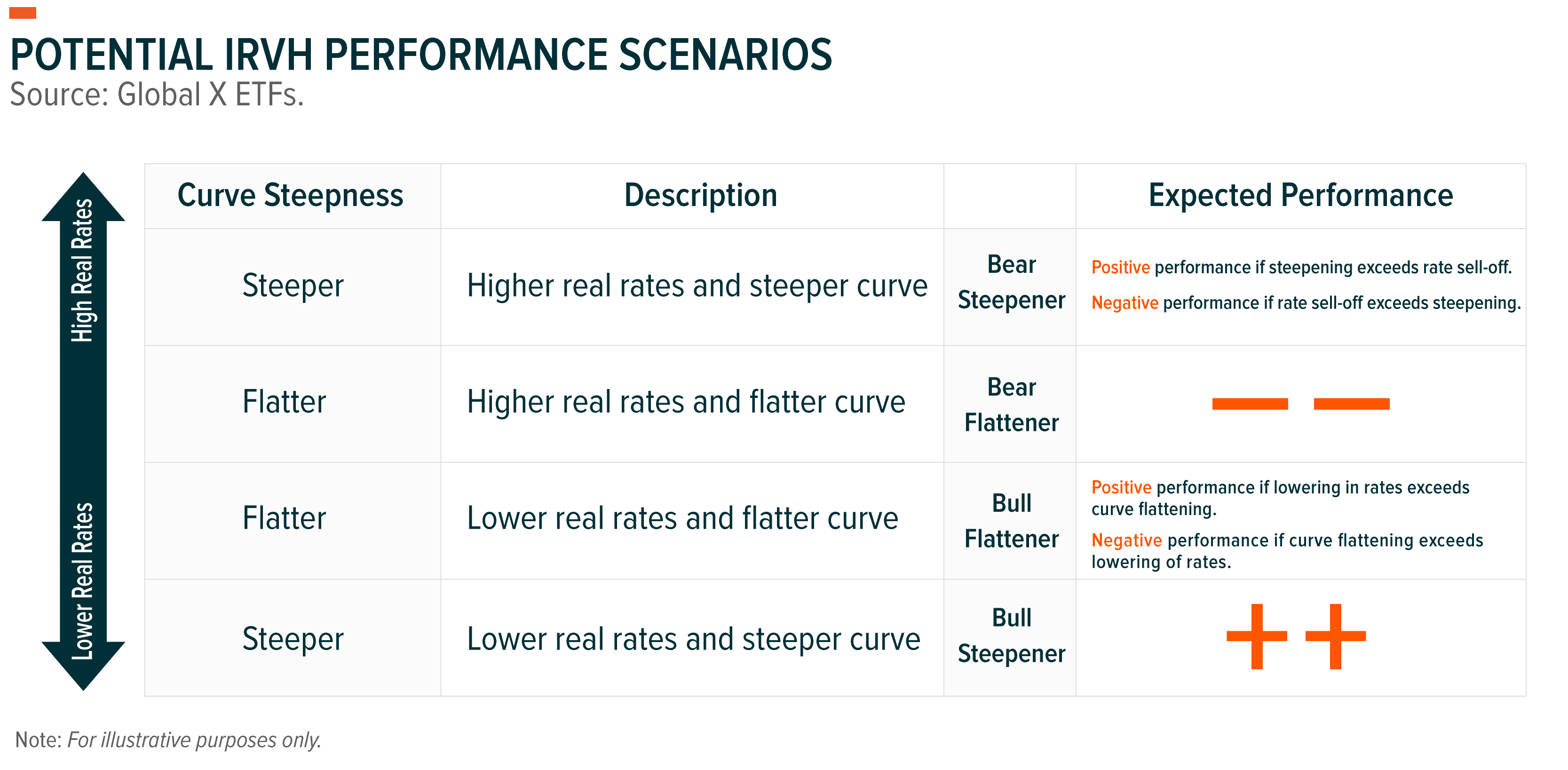

IRVH owns a portfolio of TIPS designed to provide inflation-protected income, paired with an overlay of yield curve spread options. These options are designed to benefit when the spread between 10-year and 2-year interest rates increase and are designed to benefit when short-term interest rates fall or long-term interest rates rise, all else equal. They may provide a hedge against an increase in inflation expectations, potentially giving investors the opportunity to speculate or hedge against potential movement in the yield curve.

IRVH Can Bring More Diversification to a Fixed Income Portfolio

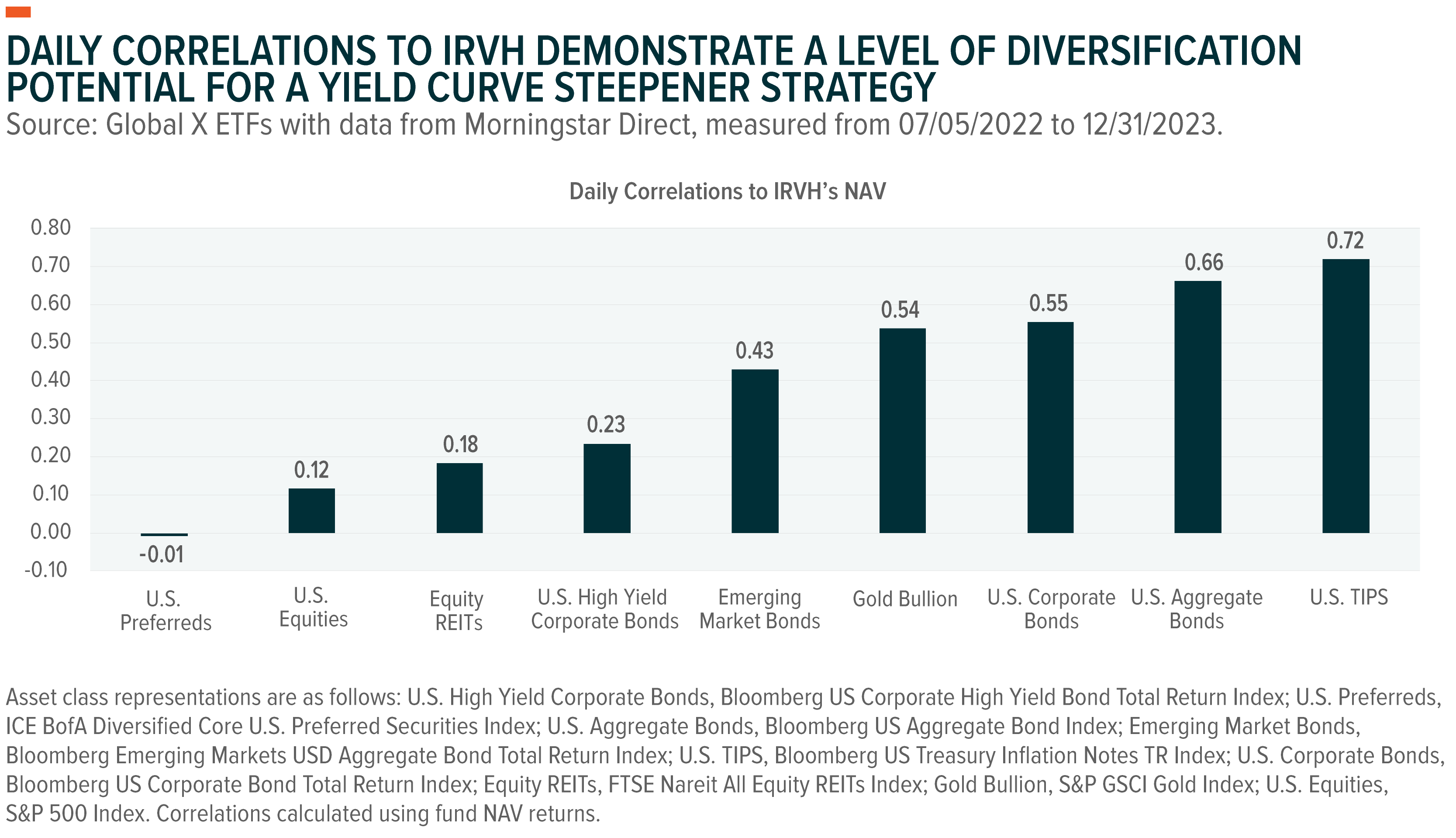

With $300 billion in assets under management (AUM) currently tracking it, the Bloomberg US Aggregate Bond Index (Agg) is a popular way to implement core fixed income exposure in a portfolio.4 However, U.S. Treasury bonds and mortgage-backed securities comprise 67% of the Agg’s total allocation.5 For investors looking for additional diversification, they may find IRVH a capable strategy given its exposure to TIPS and yield curve spread options, which is exposure that the Agg does not currently maintain. This has translated to lower correlations between IRVH and other sub-asset classes across equities and fixed income.

Past performance is not a guarantee of future results.

Conclusion: Investors May Want to Brace Their Fixed Income Portfolios

The fixed income market appears to be at a turning point with the Fed signaling that its hiking cycle is over with inflation on a clear downward trajectory. The most recent reading of the Personal Consumption Expenditures (PCE) Price Index (Core PCE, ex food and energy) at 3.2%, its lowest since April 2021.6 As the yield curve shifts through this process, we believe that IRVH can offer investors a defensive posture through its systematic strategy of a core TIPS portfolio paired with yield curve spread options.

Related ETFs

IRVH – Global X Interest Rate Volatility & Inflation Hedge ETF

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.