Global X Research Team

Global X Research TeamThe Global X China Innovation ETF posted a return of 8.61% in Q4 2022. By comparison, the MSCI All China Index, which serves as the benchmark for KEJI returned 9.11% over the same period. In this piece, KEJI’s portfolio managers discuss how China’s changing market conditions affected the fund and our strategy going forward.

The performance data quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. Returns shown for periods one year and greater are annualized. For performance data current to the most recent quarter or month end, please click here. Total expense ratio: 0.75%. Inception date: 2/22/21.

China’s Zero-COVID Policy Came to a Close

In December, China took the fast track towards exiting the zero-COVID policy and normalizing its economy. We expect China’s market to have a much better outlook in 2023 considering low inflationary pressure, the government’s strong support for the economy, and an extremely low base from 2022.

The emphasis is on the word “normalize.” The last two years were very unusual from an economic policy perspective. We should not make the mistake of viewing the status quo of the last two years as the new norm.

China suddenly withdrew its zero-COVID policy in mid-December for several reasons. First, the transmission of the current Omicron BA.4/5 variant was so rapid that it became almost impossible to track and quarantine. Second, in the second half of 2022 the case fatality rate fell to the same level as the seasonal flu. Third, President Xi had a strong incentive to boost the economy after the 20th Party Congress, where he secured his third term and appointed his allies to the top positions. Aside from the policy changes around Covid, since December, the Chinese government also rolled out many market-supportive policies, including to the property market.

The portfolio managers believe the normalization of China’s economy will positively impact not only Chinese consumers but also many industries in East Asian economies like Taiwan, Vietnam, and Korea, with a particularly strong impact on the hardware and semiconductor sectors.

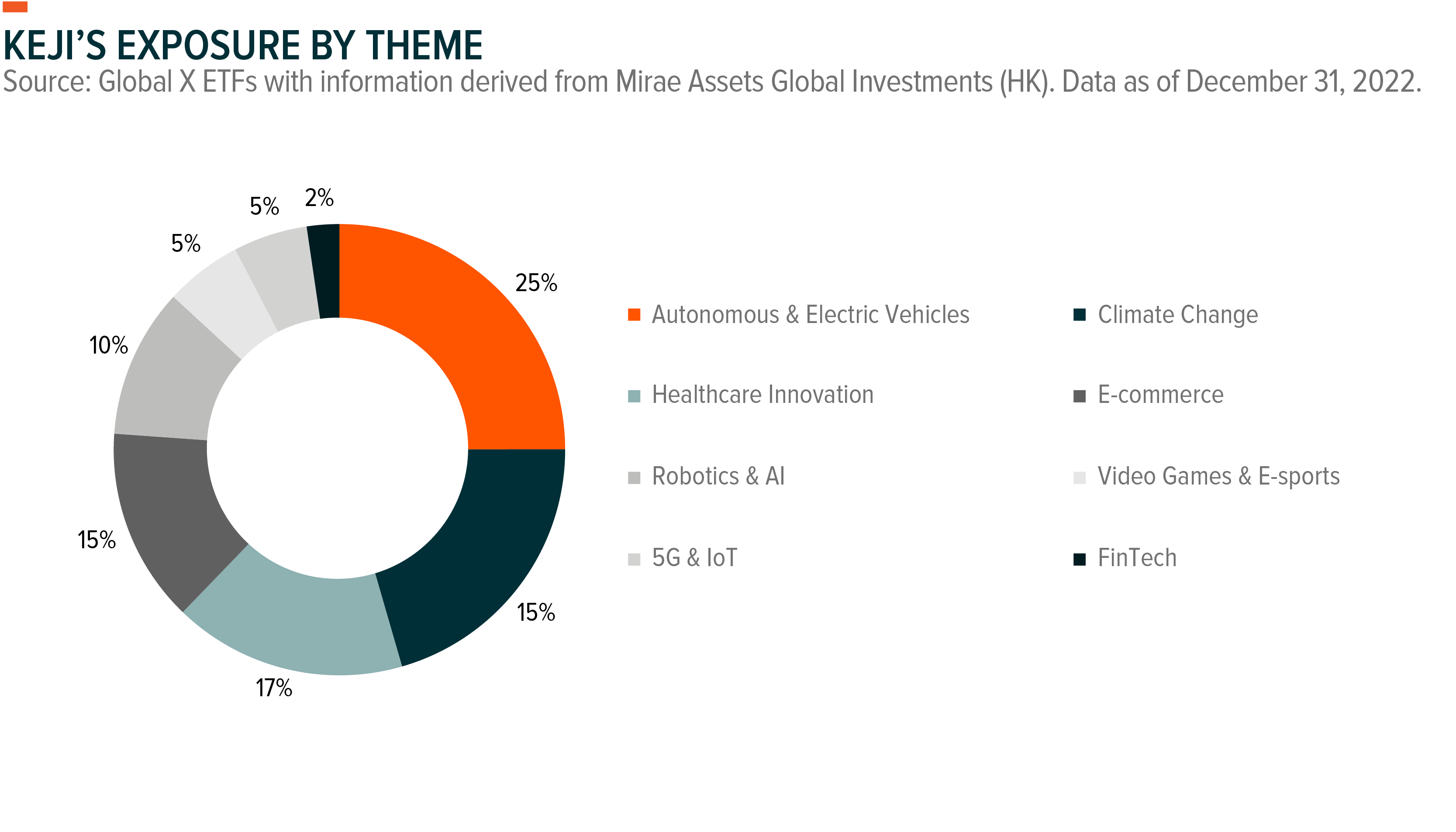

Even as these tailwinds blow, although the fund invests exclusively in Mainland China and Hong Kong equities, it underperformed the benchmark over the last two months as its exposure was more positioned on long-term growth stocks like EV batteries, automation, and clean energy. The current China rally was driven by deep value stocks like internet stocks and Hong Kong-listed stocks, as foreign money suddenly flowed in. In contrast, the mainland bourse, which has many genuine growth stocks, saw muted performance, partly because mainland investors were still overwhelmed with the surge of COVID cases and its direct impact on the economy in the near term.

The sentiment from mainland investors is understandable, but despite short-term challenges, it seems very likely that the economy will rebound strongly starting in February and March. We have seen in other countries that the recovery tends to be strong after the peak infection rate is passed, similar to what happened with India’s economy in 2022 after it suffered from an outbreak in Q2 2021.

Outlook and Strategy: The Future of Chinese EVs in the Post-Subsidy Era

Many investors may be wondering why Chinese EV stocks underperformed. First, China’s EV purchase subsidies were discontinued in January 2023, so the managers expect a meaningful sales decline in January and February which may have an adverse impact on related stocks. Second, plunges in Tesla’s share price created the potentially misleading perception that the adoption of EVs will slow down. Third, the sector was a relative outperformer over the last three years, while internet stocks and other cyclical sectors were severe underperformers. Fourth, and we believe most importantly, investors might be concerned about China’s EV battery companies’ limitations for global expansion. Whereas investors see Korean companies as potential beneficiaries of the US Inflation Reduction Act, they likely see the Act as having negative implications for Chinese companies.

Among these points, the fourth is arguably the most important, but each will be addressed below.

It has been known for a while that Chinese subsidies for EVs would be phased out by 2023. Discussion on the “post-subsidy era” abounded in Chinese financial media, so it was by no means a surprise. A positive consequence is that subsidy issues should no longer affect auto demand in the future. Another implication is that China is the only country to abolish the subsidy, which is a testament to how cost competitive Chinese EV’s have become. In fact, the managers expect strong EV exports from China to the world going forward.

Second, Tesla’s price cut in China was largely caused by idiosyncratic problems rather than broader problems with the EV market. The core issue is that Tesla failed to launch new models in China and did not comprehensively update the Model 3, which was released seven years ago. In China, where there are lots of outstanding EV models and consumers have a strong preference for new designs, relying too heavily on older models is a misstep.

Third, even though EV stocks outperformed the market in the last three years, they heavily underperformed their earnings trend. The average forward price-to-earnings ratio (PER) of the Solactive China Electric Vehicle & Battery index fell to 15x forward earnings by the end of December.1 In the manager’s opinion, this valuation is abnormal given the sector’s great growth potential. The world’s EV penetration rate was only 8% in 2022, and they expect it will reach 60% in a decade. Few business models will show this kind of huge growth potential, yet the forward PER is sitting at 15x. In their view the fundamentals are pointing towards a higher valuation in the future.

On the fourth point regarding barriers that may restrict Chinese EV-related companies from entering the US market, the managers do not believe this should be a significant cause of concern. In their view, the US will eventually accept Chinese-made or Chinese-related batteries. One of the US’s main goals in enacting the Inflation Reduction Act is building out its domestic EV battery supply chain. That does not necessarily mean that the US intends to entirely exclude Chinese battery makers. Recently, Ford and CATL are discussing building a CATL-operated battery factory in the US, but Ford will have 100% ownership. In exchange, CATL will operate the factory and receive an outsourcing service fee.2

Eventually, EVs will become just one of many manufactured goods, and the key question is who will have a better cost structure and engineering pool to make attractive and competitive goods. The managers believe China’s supply chain is well-positioned to meet those criteria.

Related ETFs

KEJI – Global X China Innovation ETF

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.