Global X Research Team

Global X Research TeamThe Global X research team updated the Scientific Beta Factor Report for Q2 2018, analyzing the performance and characteristics of factors in the US and international markets. The full Q2 Factor Report can be read here.

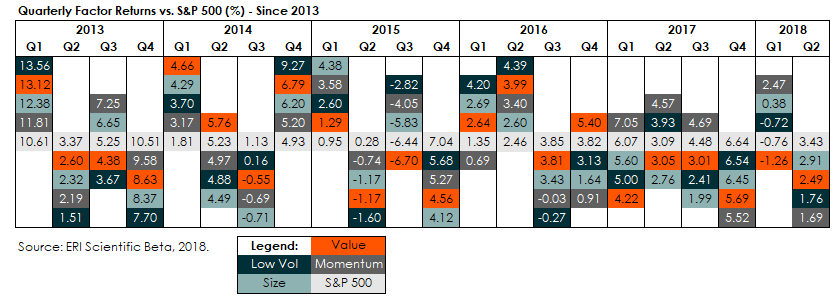

United States: Factors Fall Flat in Q2

Despite strong performance in Q1, factor exposures failed to outperform the S&P 500 in Q2 2018. All four factors (Value, Size, Momentum, and Low Volatility) delivered positive performance for the quarter, yet they each underperformed the S&P 500 by average of 122 basis points (bps). Over the past one-year period, Momentum has been the only factor to outperform the S&P 500, doing so by 75 bps.

One of the key drivers for factor underperformance in Q2 was a collective underweight to the Information Technology (Tech) sector, which dominates the S&P 500. The Global X Scientific Beta US ETF (SCIU) is 11% underweight to the Tech sector relative to the S&P 500 because factors like Value and Size tend to have less exposure to this sector. In addition, the fund’s weighting scheme is designed to be more diversified than top-heavy market cap weighted indexes. A few very large companies in the Tech sector, however, have been the major drivers of returns for the S&P 500 this year.

Value index represented by the Scientific Beta United States Value Diversified Multi-Strategy Index. Momentum represented by the Scientific Beta United States High-Momentum Diversified Multi-Strategy Index. Size Index represented by the Scientific Beta United States Mid-Cap Diversified Multi-Strategy Index. Low Volatility represented by the Scientific Beta United States Low-Volatility Diversified Multi-Strategy Index.

International: Factors Worked in Europe

In the international markets, factor performance was more mixed this quarter. Europe continued to enjoy success, with three of the four factors outperforming their broad market benchmark, the STOXX Europe 600 Index. In the Asia ex-Japan and Japan regions, factor performance was more challenged, with all factors in Asia ex-Japan underperforming and in Japan three of the four factors underperformed their relevant broad market benchmarks.

In Europe, all four factors except Value outperformed the STOXX Europe 600 Index. Low Volatility outperformed by 156 bps, Momentum outperformed by 92 bps, Size outperformed by 82 bps, while Value was the lone underperformer by 234 bps.

In Asia ex-Japan, all four factors underperformed the benchmark MSCI Pacific ex-Japan Index. Size had the largest underperformance at 481 bps, Value underperformed by 376 bps, Low Volatility underperformed by 331 bps, and Momentum underperformed by 238 bps.

In Japan, all factors except Low Volatility underperformed the MSCI Japan Index. Low Volatility outperformed by 139 bps, while Momentum underperformed by 195 bps, Value underperformed by 69 bps, and Size underperformed by 27 bps.

For Fund performance, please click on the fund ticker: SCIU, SCID, SCIX, SCIJ