Global X Research Team

Global X Research TeamThe Global X research team updated the Scientific Beta Factor Report for Q3 2017, analyzing the performance and characteristics of factors in the US and international markets. The full Q3 Factor Report can be read here.

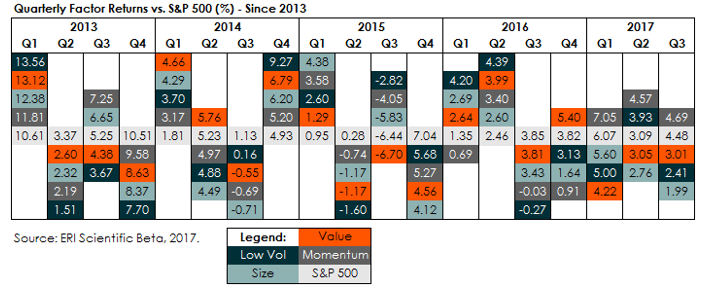

United States: Momentum Continues its Dominance… Again

Momentum has now led the four factors below and outperformed the S&P 500 in each of the first three quarters of 2017. In Q3, it was the only factor to outperform the S&P 500, rising 4.69% vs. 4.48% for the benchmark. Value, Low Volatility and Size underperformed by 147, 207, and 249 basis points (bps), respectively, weighing on the returns of multi-factor strategies that target these factors.

Value index represented by the Scientific Beta United States Value Diversified Multi-Strategy Index. Momentum represented by the Scientific Beta United States High-Momentum Diversified Multi-Strategy Index. Size Index represented by the Scientific Beta United States Mid-Cap Diversified Multi-Strategy Index. Low Volatility represented by the Scientific Beta United States Low-Volatility Diversified Multi-Strategy Index.

International: Momentum and Value Lead the Way

Momentum’s outperformance carried over to the international arena, beating the regional benchmark in Europe, Japan, and Asia ex-Japan. In addition to Momentum, Value also outperformed in each region. Low Volatility was the factor laggard, falling behind each of the regional benchmarks this quarter.

In Europe, three factors outperformed the Stoxx Europe 600 index, including Momentum, Value and Size. Momentum outperformed by 218 bps, followed by Value at 129 bps, and Size with 58 bps outperformance. Low Volatility underperformed the benchmark by 102 bps.

In Japan, Momentum and Value outperformed the benchmark MSCI Japan Index, while Low Volatility and Size lagged behind. The best performing factor was Momentum, delivering 130 bps of outperformance versus the benchmark, followed by Value with 15 bps outperformance. Low Volatility underperformed by 149 bps and underperformed by 192 bps.

In the Asia ex-Japan region, three of the four factors outperformed the benchmark MSCI Pacific ex-Japan Index. The best performer was Value, delivering 198 bps of outperformance, followed by Momentum with 133 bps outperformance and Size with 37 bps. Low Volatility underperformed by 72 bps.

For Fund performance, please click on the fund ticker: SCIU, SCID, SCIX, SCIJ