Global X ETF Model Portfolio Team

Global X ETF Model Portfolio TeamGlobal confirmed COVID-19 cases are now greater than 3.3 million, Q1 GDP in the U.S. was reported to be -4.8% annualized and the U.S. unemployment number is at a shocking 30 million, but still the S&P 500 Index increased more than 30% in April.

Is this rational?

Maybe the market is looking past all of the known and expected bad news and numbers and looking towards improving virus infection trends, positive news on the treatment front, and soft openings of some U.S. States. Perhaps this is offering longer term hope bringing enthusiasm to the equity market.

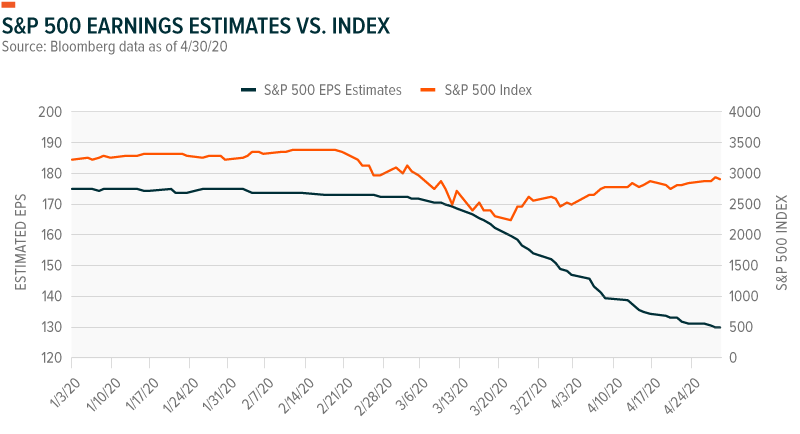

We do know that a recession began in the Q1 and that in Q2 in all likelihood we will see numbers never seen before to the tune of 30-40% decline in annualized GDP. Since a stock price is the cash flow of future earnings, if we believe the stock market is expecting a 25% decline in expected earnings per share (EPS) for the S&P 500 Index, based on the chart below, it is safe to assume that the market is looking out very far into the future. Maybe too far.

Bad news is being expressed on earnings calls and many companies have pulled guidance on both earnings and sales. Personal spending declined in Q1 and is expected to drop even more dramatically in Q2. While the Fed and Policymakers are offering support to markets where consumer demand has vanished, how long and by what degree can that support continue?