Global X Research Team

Global X Research TeamIn this post, we interviewed Vince Esposito, Managing Partner at Sungarden Investment Research, about organizing dividend paying stocks into tiers for their hedged dividend strategy.

Sungarden is an investment research firm that manages over $180 Million in client assets through separately-managed accounts. Sungarden prioritizes dividend income and avoiding “big” losses through a long-short approach. Sungarden’s flagship strategy is called Hedged Dividend and it is designed to help respond to the increasing portfolio cash flow needs of investors, while attempting to protect against turmoil in the stock market.

In a recent whitepaper, Sungarden® introduced the idea of ‘dividend tiers.’ Can you explain this approach and how it’s different from more traditional approaches to dividend investing?

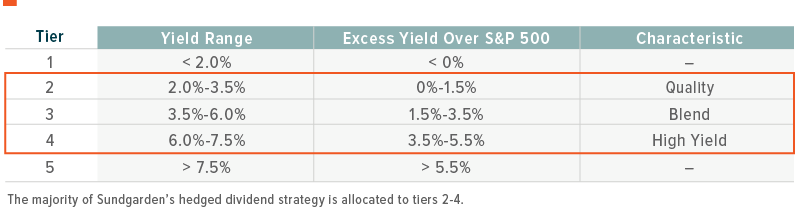

Many approaches to dividend investing focus merely on whether or not a stock pays a dividend. We think investors are not solely after dividend-paying stocks, however, but rather a well thought out portfolio of stocks that has the potential to produce a suitable amount of income to support their retirement. To address this, we created a portfolio strategy that allocates across five dividend “tiers,” which groups stocks according to their 12-month dividend yield relative to the yield of the S&P 500 Index. The decisions of how to allocate across these tiers are based on our analysis of their potential yield, risks, and total return, in order to help investors achieve their retirement goals.

Tier 1 consists of stocks with yields below the S&P 500’s yield, which recently stood at around 2.0%. These stocks are not considered for the portfolio given their low yields. Tier 2 includes those which yield up to 1.5% more than S&P 500, so up to about 3.5% today. These stocks are considered for inclusion, but occupy a very small portion of the portfolio. They are typically Blue Chip companies whose combination of yield and quality can act as an anchor for the portfolio. Tier 3 consists of companies whose yields are between 1.5% and 3.5% over the S&P yield (or 3.5%-5.5% today). These stocks represent an attractive blend of quality, yield, and value. Tier 4 is an important category for boosting the yield of the overall portfolio as it consists of high yield stocks generating income in a range of 3.5%-5.5% above the S&P 500’s yield (5.5%-7.5% today). These stocks can help increase the portfolio’s overall income and tend to exhibit strong value characteristics. The last category, Tier 5, consists of stocks which we consider to have extremely high yields, generating 5.5% over the S&P 500 (over 7.5% today). These stocks are considered, but do not occupy a large portion of our portfolio, as we are mindful of not over-reaching for yield.

Are there similarities between building an equity portfolio based on dividend tiers and how a portfolio manager approaches building a bond portfolio?

Absolutely. Our system of dividend tiers is akin to a multi-strategy or flexible bond portfolio in that we are allocating across different perceived levels of risk. We invest according to where we believe the tradeoff between the yield and total return is in our favor. A bond manager does this by sizing up things like credit quality and duration. We look at credit quality, but also factor in other fundamental and quantitative analyses. Bond managers have benefitted from generally falling or stable interest rates for more than three decades. Importantly, we think this tailwind will soon turn into a massive headwind for bond managers, since their main source of principal appreciation (falling rates) is likely gone and the income currently being generated by bonds is historically low in many sectors. By contrast, we believe that investing for dividend income, applying a tiered dividend system to help control yield and reduce risks, and supplementing that with a hedging mechanism, is a powerful combination at this stage of the stock and bond bull markets.

Does a rising rate environment change your approach to dividend tiers, or your income approach more broadly?

It does, but we view this in a positive light because it highlights the flexibility we have in constructing hedged dividend portfolios. There are few reasons why: 1) Traditional income-paying stocks like REITs, Utilities, Telecoms, Energy, and Financials don’t always move in sync with each other or with interest rates; 2) Our approach devotes a significant amount of our attention to researching “non-traditional” dividend payers. Many of the stocks that meet our criteria for investment come from industries not typically known for delivering high dividend yields like Retail, Pharmaceuticals, Gaming and Industrials; and 3) We seek to profit directly from rising rates by owning inverse ETFs and/or options that provide short exposure to segments of the bond market.

How do you view income-oriented alternatives like MLPs and REITs, compared to common stocks that pay dividends?

We typically have exposure to MLPs, though we like to own them through ETFs and not individual positions, as the latter will trigger K-1 tax reporting. Within the REIT sector, each REIT can have very different exposures and business models. For that reason, REITs are often a core part of our portfolio, and we tend to diversify across a variety of types of REITs. We are particularly attracted to those whose fortunes are closely tied to particular economic sectors we favor, such as mobile phone towers, technology data centers, entertainment and senior care facilities. We prefer these to the traditional shopping center and office REIT sub-sectors.

Sungarden takes a long-short approach to an income investing. What are the potential advantages of this approach versus a long-only income portfolio?

We have been alternative investment managers for nearly two decades because we believe that moderate-risk investors are better off with a long-short approach than a stock-bond approach to achieve their investment objectives. That is why we complement our equity selection and dividend tiering systems with a dedicated short position, or “hedge” on the equity portfolio to potentially limit the impact of major declines in the broad equity market. As markets become more complex, the availability of investment information becomes more immediate and ubiquitous, and market participants create more sophisticated trading mechanisms, we believe that active managers like ourselves must make risk-management a full-time job. We believe this makes a long-short approach an essential core portfolio strategy for all but the most aggressive investors. When the next market disruption comes along, long-only positions and passive asset allocation decisions could potentially give back years of hard-earned returns. We aim to sidestep those types of outcomes, and believe that our core long-short, tier-driven, income and total return approach can do that better over time than its long-only and passive peers.