Global X ETF Model Portfolio Team

Global X ETF Model Portfolio TeamStability Over Volatility

Investors should plan for a likely U.S. recession later this year. Historically, recessionary pressures weigh on earnings growth, with investors focusing on yield for a good portion of their total return. In 2022, higher-yielding areas of the market outperformed the S&P 500 as the Federal Reserve (Fed) aggressively raised interest rates, shifting investors’ focus from future growth potential to current income.

Currently, markets expect the Fed’s benchmark rate to peak around 5%, which may slow economic growth and ideally reduce inflation.1 Still, rates could stay higher for longer, given the tight labor market, resilient consumer, and elevated inflation, which could create a favorable environment for income investors. This whitepaper outlines yield-focused solutions, especially applicable during times of economic uncertainty.

Key Takeaways

- Focus on quality dividends that can withstand economic shocks.

- Defensive sectors with high payout ratios typically outperform during late-cycle and recessionary environments.

- Equity income portfolios must be flexible enough to balance yield and total return throughout business cycles.

Viable Dividends During Market Downturns

Dividend income can provide a margin of safety during times of market stress. But not all dividends are created equal. As the old saying goes, “cash is king,” and some companies may cut payouts to retain cash through economic downturns. However, quality firms with strong balance sheets and free cash flow typically have more resilient payouts. The financial discipline of quality firms can enable reasonable payouts to shareholders while retaining enough earnings to fund growth.

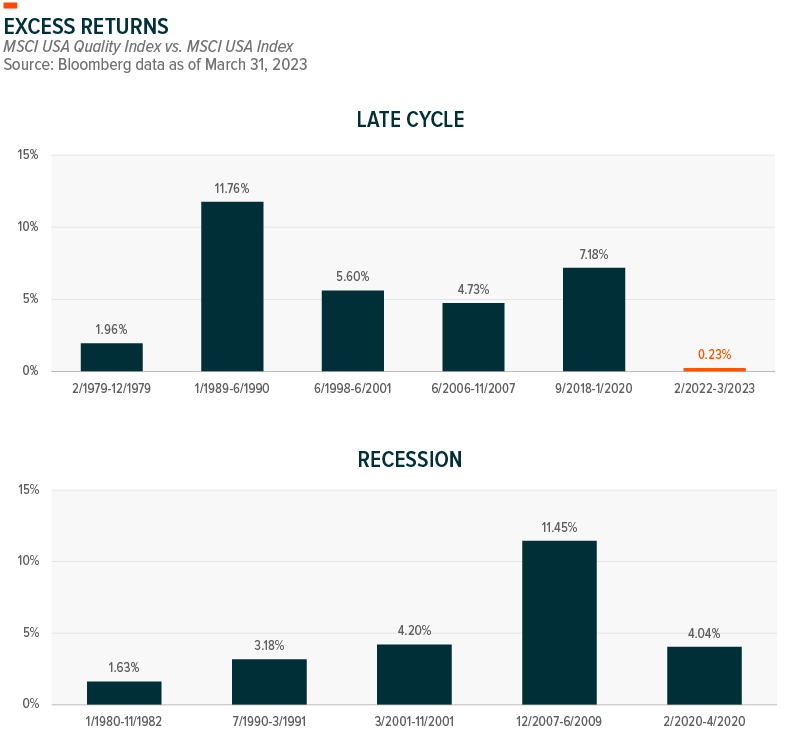

We prefer yield stability, especially during recessionary environments. Quality stocks often have stable payout ratios and strong earnings, aiding performance versus non-dividend paying stocks during market downturns.2 Notably, quality stocks outperformed the broader market in March 2023, reversing prior months of underperformance during this late-cycle environment that began in February 2022, as seen in the chart below.3

There has been a notable delay in earnings downgrades over the past year despite weaker economic data, inflationary pressures, and a higher interest rate environment. The market sell-off in 2022 showed a wider dispersion between growth and value stock returns, and the premium attached to quality stocks, given their stronger fundamentals, possibly weighed on relative performance during the beginning of the current late-cycle stage. While substantial multiple compression makes value stocks appear attractive, varying fundamentals may create a “value trap” and could make some companies vulnerable during a recession. Therefore, the earlier mispricing of quality stocks during the challenging economic environment provided an opportunity for investors, especially those seeking stable dividend income. Quality could continue to benefit as the late-cycle stage advances.

Market downturns enhance the attractiveness of quality’s attributes, but the factor tends to underperform during early-cycle stages, highlighting the importance of understanding macroeconomic conditions.4

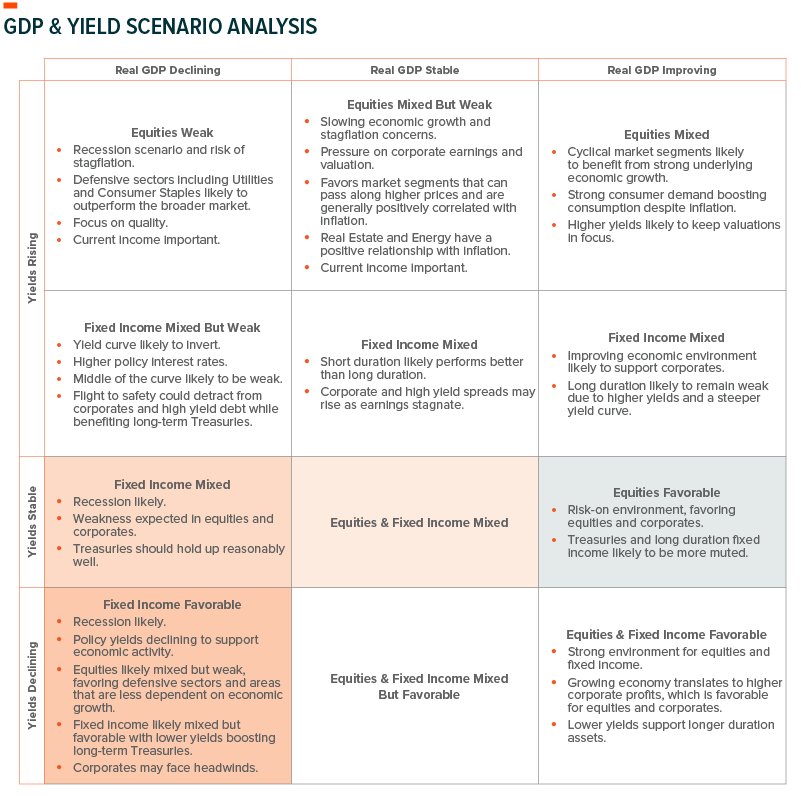

Positioning When Policy Rates Stabilize and Growth Slows

U.S. markets could contend with delayed effects from policy tightening, evidenced by the significant fall in leading economic indicators. The Conference Board’s Leading Economic Index for the U.S. is down 3.6% over the past six months through February, driven by manufacturing, credit, and consumer expectations, which more than offset strengths in labor markets and stock prices.5 Meanwhile, the Goldman Sachs Financial Conditions Index (FCI) eased, reversing a portion of its rise from 2022 lows. A one-to-three quarter lag between a peak in the FCI and the resulting drag on U.S. real GDP growth is typical.6

The scenario table on the next page outlines the typical relationship between asset classes and economic variables. Recent liquidity concerns in the banking sector could encourage a slower trajectory of rate hikes. The “Yields Stable” section of the table highlights the most likely scenario during the first half of 2023, while the “Yields Declining” section could occur as recessionary pressures accelerate between 2H 2023 and 1H 2024. Here is a summary of positioning implications based on the current economic environment.

- Weak economic growth warrants defensive exposure with a greater focus on quality. Current profitability and consistent dividend distributions to shareholders are critical.

- Longer duration assets become attractive as yields decline from peak levels.

- The potential for higher volatility could warrant exposure to covered call strategies.

International Markets Rebound, Risks Loom

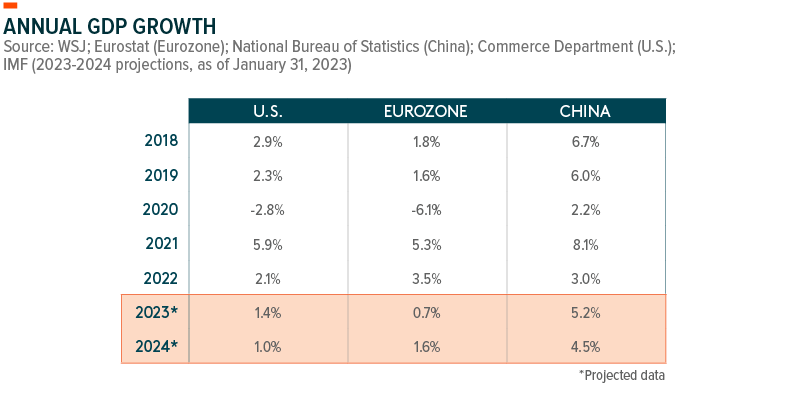

Investor sentiment is improving outside of the U.S. after nearly a decade of underperformance. During that stretch, U.S. stocks traded at a significant valuation premium relative to international developed and emerging markets compared with historic trends. In Europe, the sharp decline in energy prices and improving economic data could lead to positive earnings surprises. China’s easing COVID restrictions and policy stimulus could strengthen economic growth, supporting additional upside in emerging market (EM) equities relative to U.S. equities.

Despite potential value opportunities abroad, economic conditions remain fragile. Uncertainties surrounding the Russia/Ukraine war and China’s property market woes could prevent a meaningful economic recovery, and if these and other international headwinds materialize, investors could face an unstable dividend environment. The S&P 500’s dividend payout ratio is 36%, while the Stoxx Europe 600’s dividend payout ratio is 49%. The Dow Jones Industrial Average’s payout ratio is 53%, which is higher than the S&P 500, possibly reflecting its lower exposure to Information Technology, like Europe.7 However, while European stocks offer attractive dividend yields versus U.S. stocks, they tend to cut dividends faster during economic slowdowns.8

Equity Income Opportunities

Equity income offers many solutions that can generate yield in the current environment. Solutions include quality stocks that provide stable dividends, fit to withstand economic shocks. Investors can also consider lower beta solutions such as preferred stocks and covered call strategies that benefit from rangebound markets. Yield can also be achieved through targeted common equity exposure.

Common Equity Yield Strategies

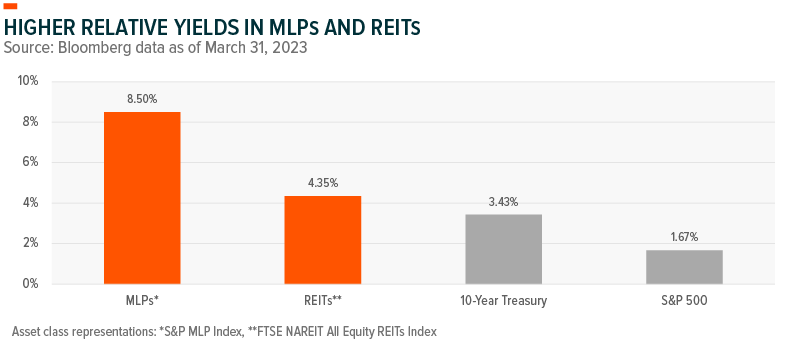

It’s important to focus on quality companies, especially during market downturns. These companies consistently grow their dividends over an extended period and are less sensitive to economic changes. Exposure to MLPs (Master Limited Partnerships) and REITs (Real Estate Investment Trusts) can also provide higher yields relative to the S&P 500 and the 10-year Treasury yield.

High Dividend Yield, MLPs and REITs

Energy stocks continued to rise in 2022. Oil prices rallied during 1H 2022, although prices retreated during the second half as recession concerns surfaced. However, energy stocks held up, diverging from the underlying WTI Crude Oil spot price. Markets rewarded energy companies because of positive earnings surprises and capital discipline. Commodities tend to weaken during recessionary phases, which could narrow the performance gap between energy stocks and oil futures. While the Russia/Ukraine war has the potential to maintain a premium on energy prices, we expect fundamental risks to cap additional upside. Conditions for MLPs and the energy sector may be difficult with less tightness in the oil market and slower U.S. drilling activity.

MLPs which cover exploration, storage, and distribution of crude oil and natural gas, are compensated on volume growth, so profits tend to rise alongside higher demand. Strong volume growth is typically associated with higher energy prices. MLPs tend to have higher yields because of their structure from a taxation perspective. MLPs must distribute 90% of their income in the form of dividends to maintain their preferred tax treatment, which includes no federal or state taxes.

REITs are companies that own or finance real estate across different property sectors. Like MLPs, REITs must distribute about 90% of their income in the form of dividends to keep their preferred tax status. Therefore, REITs tend to pay a higher-than-average yield. REITs cover a wide scope of property types, which could help investors maintain their real estate exposure through different phases of the business cycle. For example, office REITs tend to benefit when employment rises. Residential REITs benefit in areas and times of population growth and strong housing fundamentals. Healthcare REITs benefit from an aging population. Mortgage REITs hold mortgages and mortgage-backed securities (MBS) on their balance sheets, profiting from the spread between income earned and the interest paid on assets.

Generally, late-cycle dynamics such as higher interest rates can increase a REIT’s cost of debt and weigh on valuations. However, rent growth and high dividend payouts can provide a hedge against inflation. During the early cycle and expansion phase, declining interest rates and favorable growth dynamics can benefit REITs. A consideration is that recessionary conditions can negatively impact rent and property values, particularly in the office sector. The U.S. office vacancy rate has risen 3% points since 2019, burdened by layoffs and the shift to remote/hybrid work.9

Investors can also find higher-than-average dividend yield opportunities within the telecommunications industry of the Communication Services sector. Companies in this space are older, well-established, and have a history of paying above-average dividends.

The chart below shows MLP and REIT yields versus 10-year Treasury and S&P 500 yields.

Quality Dividends

We view the quality dividends segment as a core strategic holding because of its focus on profitable growth and quality value. Historically, companies with strong free cash flow and healthy balance sheets fare best among value factors during market downturns. BofA Securities research shows the risk of deep value strategies becomes increasingly pronounced during late-cycle and recession periods, while the quality factor can provide a timely hedge. Quality stocks typically provide a lower payout ratio relative to high yielding equities, but they focus on consistent dividends and dividend growth despite the economic environment. Therefore, quality stocks’ lower yield is less sensitive to economic changes.10

Sectors with Good Yields

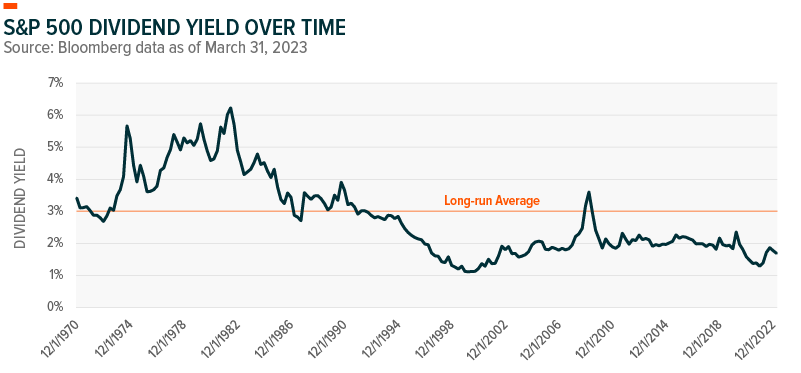

Dividend yields have remained below the long-term average of 3% for the past 30 years. The S&P 500’s dividend yield rose to 1.67% over the past year from a low of 1.20% in December 2021, though it remains below average levels, according to Bloomberg data. The index’s dividend yield rose as equity prices fell. Despite historically low dividend yields, investors can still achieve yield by positioning within sectors that have relatively high payout ratios.

When searching for equity income across sectors, we prefer established companies that generate a steady stream of cash flow. These firms can reinvest capital to cover growth while paying out a reasonable amount of earnings to shareholders.

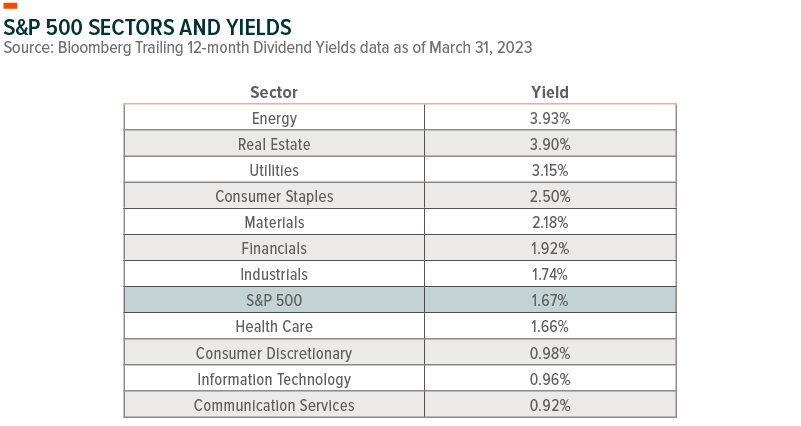

Energy offers a relatively high dividend yield of 3.93%. Despite the potential for lower oil prices during a recession, capital discipline and improved cash flows relative to previous cycles could help sustain dividends during a downturn. Utilities offer recession-proof characteristics and a 3.15% dividend yield, though, high Treasury yields can negatively impact this sector. We prefer the defensive nature of Consumer Staples, which offers a 2.50% dividend yield. The table below lists current dividend yields by S&P 500 sectors.

Preferred Equity Offers Risk Mitigation with High Yield

In the capital structure, preferred stockholders are above common stockholders and below bondholders. Preferred equity investors receive dividend income before common equity investors. Preferreds offer a fixed or variable yield, and they are usually issued by financial corporations. Yield from preferred stocks can be treated as qualified dividend income instead of ordinary income, resulting in favorable tax treatment.

We favor preferred equities due to their position in the capital structure and low beta. Their lower sensitivity to equity market price movements aids in reducing volatility relative to common equities. The dividends on variable rate preferreds float relative to a reference rate, which can be beneficial in a rising rate environment. It is important to remember that variable and fixed-rate preferreds have duration risk due to their perpetual nature.

The preferred equity market may face periods of heightened volatility during episodes of banking stress. As securities that are included in regulatory capital, banks are one of the largest issuers of preferreds. During normal market conditions, this is a boost for preferred credit quality. However, it also means that preferreds are impacted by the overall health of the financial system. The recent regional banking crisis negatively impacted preferreds, although the greater issuance by large banks since the 2008 financial crisis can offer some resilience.11

Covered Calls Offer Differentiated Yield

Covered calls perform best when markets are rangebound. The income generated from selling call options on the S&P 500, Nasdaq 100, or Russell 2000 is paid out to investors in the form of yield. Investors have full exposure to the downside, as calls expire worthless in a declining market. Exposure is capped on the upside, as the underlying security can be called away. When volatility rises, the premium received increases to compensate for market instability.

In a reasonably tight range, covered calls benefit from receiving premium income and potentially small improvements in the underlying equities while not having the underlying called. In a rising market, covered calls typically underperform the overall market because the underlying security is called away, affecting the capital gain return, not the income return. In a declining market, covered calls provide a small buffer of protection because of their premium income.

For investors seeking downside protection in a declining market, a collar strategy can be appropriate. Like a covered call strategy, calls are sold on an index such as the S&P 500 or Nasdaq 100, but with a collar, puts are also purchased on the index. The risk/reward tradeoff is a lower yield relative to the covered call on its own. The potential for higher volatility during the transition from late cycle to recession could make covered calls attractive.

Holistic Approach For Higher Yields & Total Return

Finding yield through equity income is important, but selectivity is vital given current economic uncertainties. Exposure to quality stocks can provide resilient yield. Covered calls can offer a relatively high premium during volatile and rangebound market environments. And preferred stocks can provide a reasonable income and lower beta.

Each of these areas generally focus on either yield or return potential. Combining equity income solutions can improve a portfolio’s exposure diversification while also diversifying its sources of yield. This can create a portfolio that provides a solid yield while also focusing on total returns. Although the economic outlook includes some dark clouds, opportunities can emerge during recessionary periods. Equity income portfolios must be flexible enough to capture upside while maintaining a decent yield throughout the business cycle.