Pedro Palandrani

Pedro PalandraniWith last recession ending over 10 years ago, investors are becoming more concerned for the inevitable ‘next one.’ While attempting to accurately time a recession can be a futile exercise, adequate preparation – through gaining knowledge of defensive or countercyclical investments and thoughtful portfolio construction – can help investors weather the eventual storm.

One misconception some investors hold is that high growth, disruptive themes are cyclical in nature and therefore at above-average risk should the economy falter. In this piece, we identify long term themes that we believe could prove resilient during an economic downturn. But first, a history lesson.

Economic Downturns can be Opportunities for Certain Themes

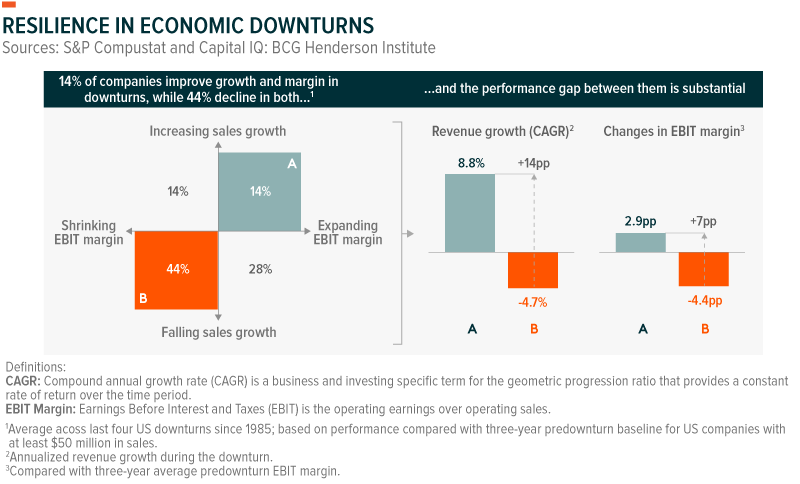

History shows that certain companies can benefit when economic conditions weaken. In the last four downturns, 72% of companies experienced declining revenue, but 14% sustained revenue and margin growth despite the challenging economic circumstances.1 Which types of companies gain during a contraction? The first camp includes firms that benefit from specific policies. Governments attempt to step in and support the economy during downturns, and therefore can drive growth in certain industries. The second camp includes more traditional ‘defensive’ stocks, or those with inherently inelastic demand. The most attractive firms may be those that stand at the intersection of both factors.

The alcohol industry during the Great Depression offers a useful example. In 1933, with a crumbling economic backdrop, the US government repealed the prohibition of alcohol with the 21st Amendment in an effort to boost economic activity and tax revenues. With ever-present demand, alcohol sales took off, spurring job creation and consumption. The repeal generated $1.35 billion in alcohol-related taxes for the federal government, amounting to half of its total revenue in 1934.2 The move also resulted in annual net social benefits of $3.5 billion in today’s prices, or one-third of 1% of GDP from 1934–37, according to estimates.3

Cannabis: Parallels with the Repeal of Alcohol Prohibition

The so-called recession-proof alcohol and tobacco industries are relevant comps for the nascent cannabis industry. Alcohol and tobacco tend to experience steady demand regardless of the business cycle. Yet, inelastic demand is only one factor when evaluating cannabis’ potential. The other is the increased potential for cannabis legalization in a downturn, given its growing track record of generating economic growth and tax revenues. Like the repeal of alcohol prohibition during the great depression, we believe cannabis legalization is more likely to occur during a downturn as governments become more motivated to spur the economy and access new sources of tax revenue.

A Kansas City Fed study on the economic impact of cannabis legalization found that Colorado created roughly 18,000 direct jobs and indirectly boosted employment in areas like construction, security, and legal services by as much as 23%.4 Taxes on cannabis sales, which include a 15% excise tax, a 15% special sales tax, and a 2.9% state sales tax, have raised more than $1 billion for the state since legalization. The money provided funding for school construction, local governments and cannabis research.5

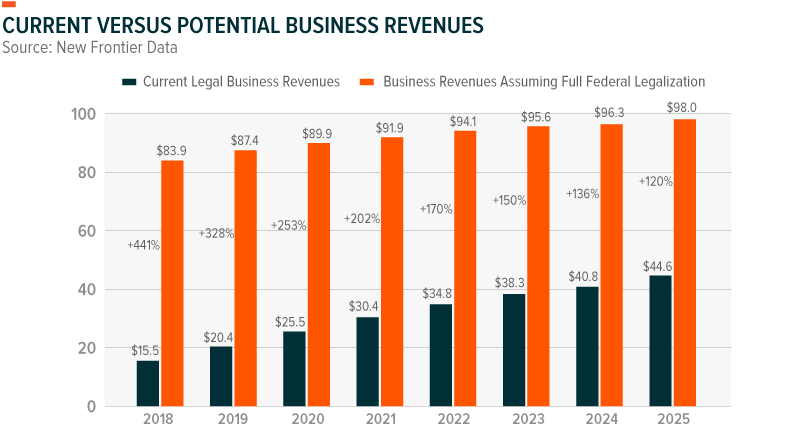

Cannabis legalization at the federal level could generate $132 billion in aggregate tax revenue and more than a million new jobs across the country by 2025.6 Currently, there are approximately 340,000 jobs (direct and indirect) tied to the cannabis market. Extrapolated, that would mean 1.46 million jobs under a fully legalized system.7

Interests rates remain historically low and appear set to stay low for some time. Meanwhile, government debt relative to GDP is at a 70-year high. Monetarists who favor monetary policy to promote growth and Keynesian economists who advocate for greater government spending may have no other option than to suggest new tax revenue opportunities, particularly if the economy enters zero or negative growth territory. Cannabis legalization could create one such growth opportunity.

Infrastructure: A Worthy Destination for Government Stimulus During Recessions

A country’s infrastructure underpins its economic activity. It enables businesses and individuals to operate in a more efficient manner while directly impacting employment and economic output. Beyond providing the essential foundation for economic activity, new infrastructure is vital for enabling technological developments like autonomous vehicles and 5G networks and can be a medium to address climate risk and public health challenges. However, total public construction spending as a percent of US GDP declined from 2.1% in Q4 2009 to 1.5% in Q3 2019.8 In other words, infrastructure spending shrunk on a relative basis during the longest, and potentially the largest, expansionary cycle in history.

According to research from S&P, a 1% increase in US infrastructure spending as a percentage of GDP translates to a 1.7% increase in GDP over the next three years, or a 70% return on investment.9 This is backed by the effect of the short-term fiscal multiplier, which, similar to other government spending, boosts aggregate demand in the economy.

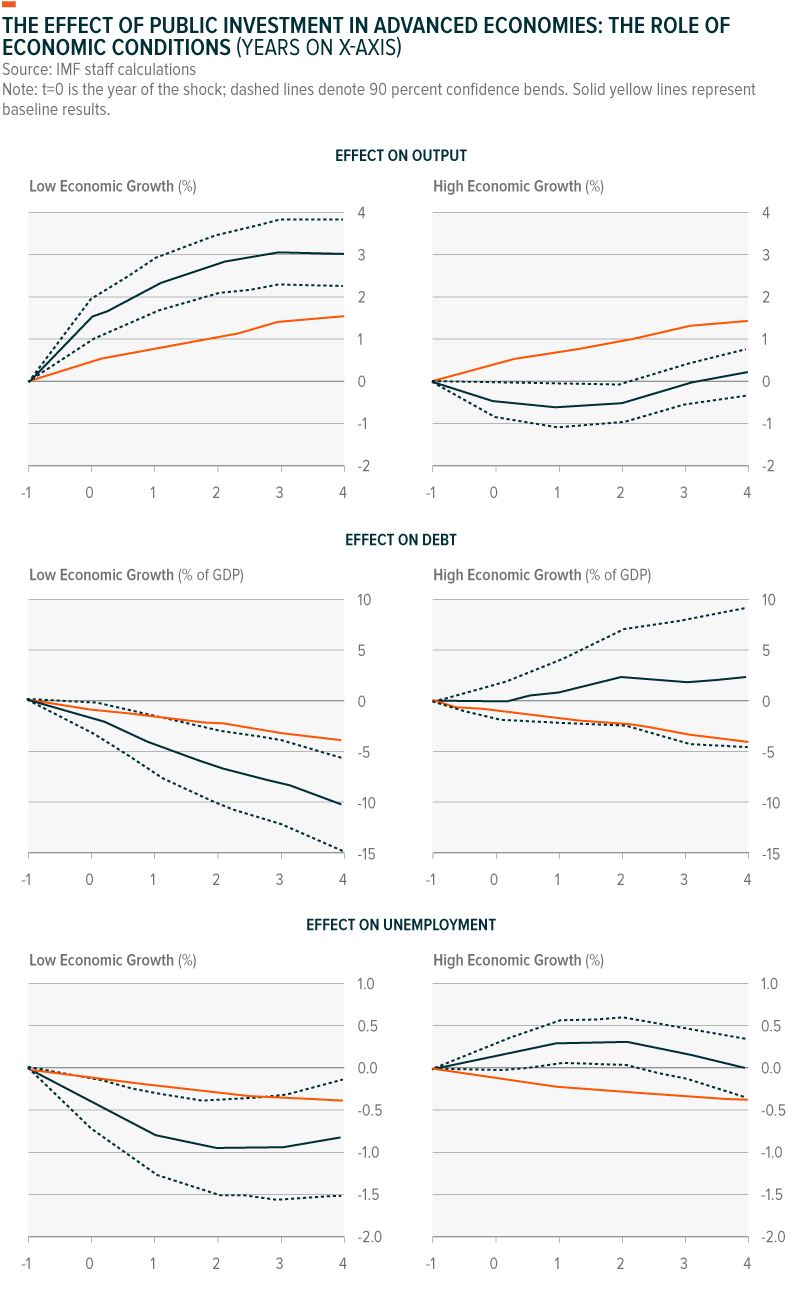

Research based on current economic theory suggests that the timing of infrastructure spending matters. When the economy is in recession, additional public infrastructure spending provides a greater short term boost to economic activity than it does during an expansion.10 The rationale holds that during recessions economic inputs such labor, production capacity, and raw materials, among others, remain idle. The ability to quickly access these inputs helps to stimulate economic activity. During an expansion, however, low unemployment rates, high capacity utilization rates, and limited excesses across economic inputs, means additional infrastructure spending may simply create a backlog. Additionally, higher public spending in an expansion could nudge inflation to higher levels, adding pressure to the Fed to set more restrictive monetary policy, which could offset any fiscal stimulus.

Similarly, an IMF study found that additional public infrastructure spending during an expansion does not significantly impact employment.11 While an increase in public spending of 1% of GDP could decrease the unemployment rate by 0.5% in the first year and 0.75% in the medium-term under certain conditions, this impact is not seen during high growth periods.12

Infrastructure spending also has a long-term impact on the economy as productivity is expected to increase given the ties of infrastructure with economic efficiency. The relationship between infrastructure and productivity can be analyzed from supply side economics. For example, improved transportation alternatives such as new highways and new transportations systems could facilitate the access and distribution of products to companies. In the same vein, companies could gain access to more skilled labor and vice versa, promoting higher labor productivity.

There is mounting evidence that supports the relationship between infrastructure spending and economic growth, especially during recessionary periods. We believe these studies increase the likelihood of a major federal infrastructure package during adverse economic circumstances, supporting the revenues of infrastructure development companies in a counter-cyclical manner.

Health Care Demand Doesn’t Slow for Recessions

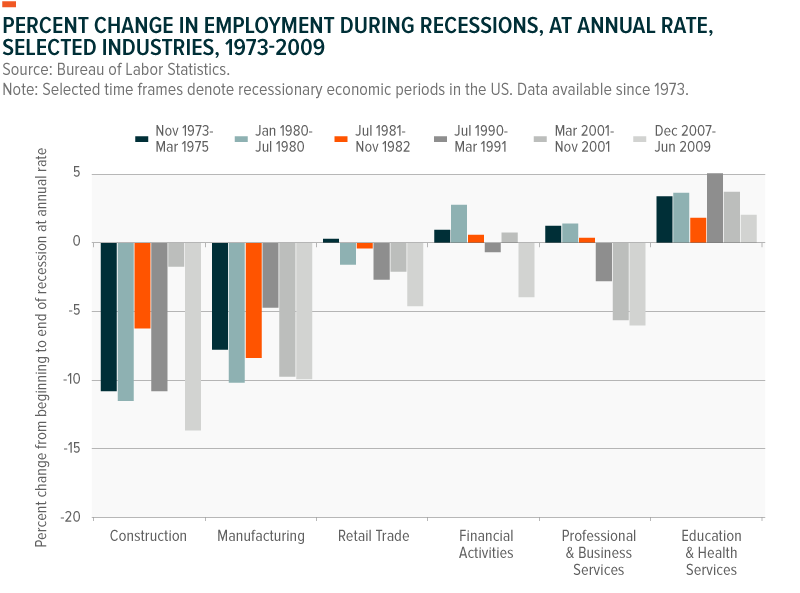

In 2019, the number of seniors 65 and older surpassed the number of children five and younger, representing a significant change in global demographics.13 As the population ages, it puts an increasing strain on the health care system in areas like health care products and services, medical devices, senior homes, as well as biotechnology and pharmaceuticals. And even if the economy slows, these health-related industries could remain insulated as insurers and governments shoulder most of the associated costs. For perspective, employment in the health care sector has increased for more than 40 years regardless of the business cycle.14 The Bureau of Labor Statistics (BLS) believes the health care sector will likely to continue to grow employment until at least 2026, mainly because of the aging of US population.15

For out of pocket expenses, the health care sector may be insulated as well. While people prioritize expenditures during a recession, health care expenses are often at the top of the list. Evidence suggests that disposable income declined between 2000 and 2010, a period with two economic recessions, but spending on health care steadily increased.16

Expansion of health insurance coverage may also stabilize the space. Changes in employment-based insurance coverage do correlate with economic activity, but since the last recession 34 states expanded Medicaid coverage to ~13 million adults as of 2018.17 The percentage of people without coverage fell from over 14% in 2008 to slightly below 9% in 2018.18 This fundamental change could help diversify payers and sustain the level of health-related spending, even during a downturn.

Biotech and pharmaceutical firms may also be immune to the impact of downturns given the nondiscretionary characteristics of their products. Valuations of these firms depend primarily on the success of a drug or device, and its addressable market, rather than cyclical factors. Because of recent breakthroughs in the space, many sub-themes, like gene editing, are transforming human health and health care services. For example, CRISPR is a gene editing treatment that just recently began human trials. Two patients received CRISPR treatments, one with transfusion-dependent beta thalassemia and one with sickle cell disease. Prior to treatment, the beta thalassemia patient needed an average of 16.5 blood transfusions per year. Nine months after receiving treatment, the patient no longer needed transfusions and tested for near-normal hemoglobin levels. The sickle cell disease patient also showed positive results after the treatment.

While we are still at the very early stages of adoption of these medical breakthroughs, the payments by insurers, governments, and inelastic consumers should help support these high growth potential areas regardless of the economic cycle.

Conclusion

Thematic investing prioritizes identifying long term structural themes, but investors may still want to be aware of the cyclical factors that can impact these themes in the short term. With slowing economic growth around the world and at least moderate risk of a recession in the next few years, investors are increasingly considering how to position their portfolios more defensively. While it is our preference for thematic investments to occupy long term strategic allocations within a portfolio, considering allocations to defensive or counter-cyclical themes could help smooth shorter term returns. We believe cannabis, infrastructure, genomics and longevity, are a few themes that could not only withstand a potential recession, but perhaps thrive.

Related ETFs

POTX: The Global X Cannabis ETF (POTX) seeks to invest in companies across the cannabis industry. This includes companies involved in the legal production, growth and distribution of cannabis and industrial hemp, as well as those involved in providing financial services to the cannabis industry, pharmaceutical applications of cannabis, cannabidiol (i.e., CBD), or other related uses including but not limited to extracts, derivatives or synthetic versions.

PAVE: The Global X U.S. Infrastructure Development ETF (PAVE) seeks to invest in companies that stand to benefit from a potential increase in infrastructure activity in the United States, including those involved in the production of raw materials, heavy equipment, engineering, and construction.

GNOM: The Global X Genomics & Biotechnology ETF (GNOM) seeks to invest in companies that potentially stand to benefit from further advances in the field of genomic science, such as companies involved in gene editing, genomic sequencing, genetic medicine/therapy, computational genomics, and biotechnology.

LNGR: The Global X Longevity Thematic ETF (LNGR) seeks to invest in companies positioned to serve the world’s growing senior population through exposure to health care, pharmaceuticals, senior living facilities and other sectors that contribute to increasing lifespans and extending quality of life in advanced age.