Global X Research Team

Global X Research TeamAs investors keep a close eye on China’s reopening, we continue to leverage our local presence in personally monitoring consumer health, from store and travel-traffic to spending habits. We also evaluate the material impact of catalysts such as government-led stimulus measures (aimed primarily at the consumer) and other supportive policies. Searching for material evidence supporting recent confidence surveys and activity data is another important part of our process.

Key Takeaways

- Our recent trip to mainland China reinforced our view that the nation’s recovery is ongoing, albeit uneven.

- Consumer spending appeared resilient, especially when looking at demand for luxury goods.

- Domestic brands have been gaining market share from multinational rivals in recent years, a trend that we believe will continue.

Overall Consumption Remains Uneven, but We Saw Potential Pockets of Opportunity

We recently travelled to China for a week, visiting Hainan, Shanghai, Guangzhou, and Xian. Traffic in the island province of Hainan was weaker than anticipated, but September is generally a low season for tourism and there are now other options for beaches following the reopening, so we were not overly concerned. The retail company China Tourism Group Duty Free Corporation (CTGDF) has managed to get European luxury goods conglomerates LVMH and Dior to open their first stores in Hainan (both will be duty paid stores), and it seemed other mall operators such as MixC are also hoping to get LVHM into their malls. LVMH and Dior stores will be first opened in Sanya Haitang Bay mall, and CTGDF hopes to deepen this relationship with LVMH Group to open additional stores in its Haikou mall in the future. Property developer CR Land also has built nice MixC malls in both Sanya and Haikou, with high-end brands including Gucci, Prada, etc., but traffic for now seemed low. They appear to be preparing for 2025, when Hainan is set to become a duty-free province like Hong Kong, which may attract more travelers for shopping. Overall, our impression was that Hainan may take a bit more time to become a truly attractive tourist destination, and CTGDF business continues to be largely dependent on government policies (such as increased access to duty-free shopping in Shanghai and Beijing).

On the other hand, Xian was a much more vibrant city than expected, with more travelers compared to Hainan. We were impressed with Xian’s big malls and high-end brands. According to Yum China’s (YUMC) CFO, Xian used to have a population of approximately 9mn, which has increased to more than 13mn over the past several years. The city also has well-trained IT professionals, in part thanks to good universities in the city. Thus, YUMC has its digital center in Xian. We could see urbanization continuing in many cities in China like Xian, which would likely continue to support consumption growth in the country. Xian reminded us of older days of booming China. We understand Xian may be one unique city, but we doubt it’s alone given that China is such a large country.

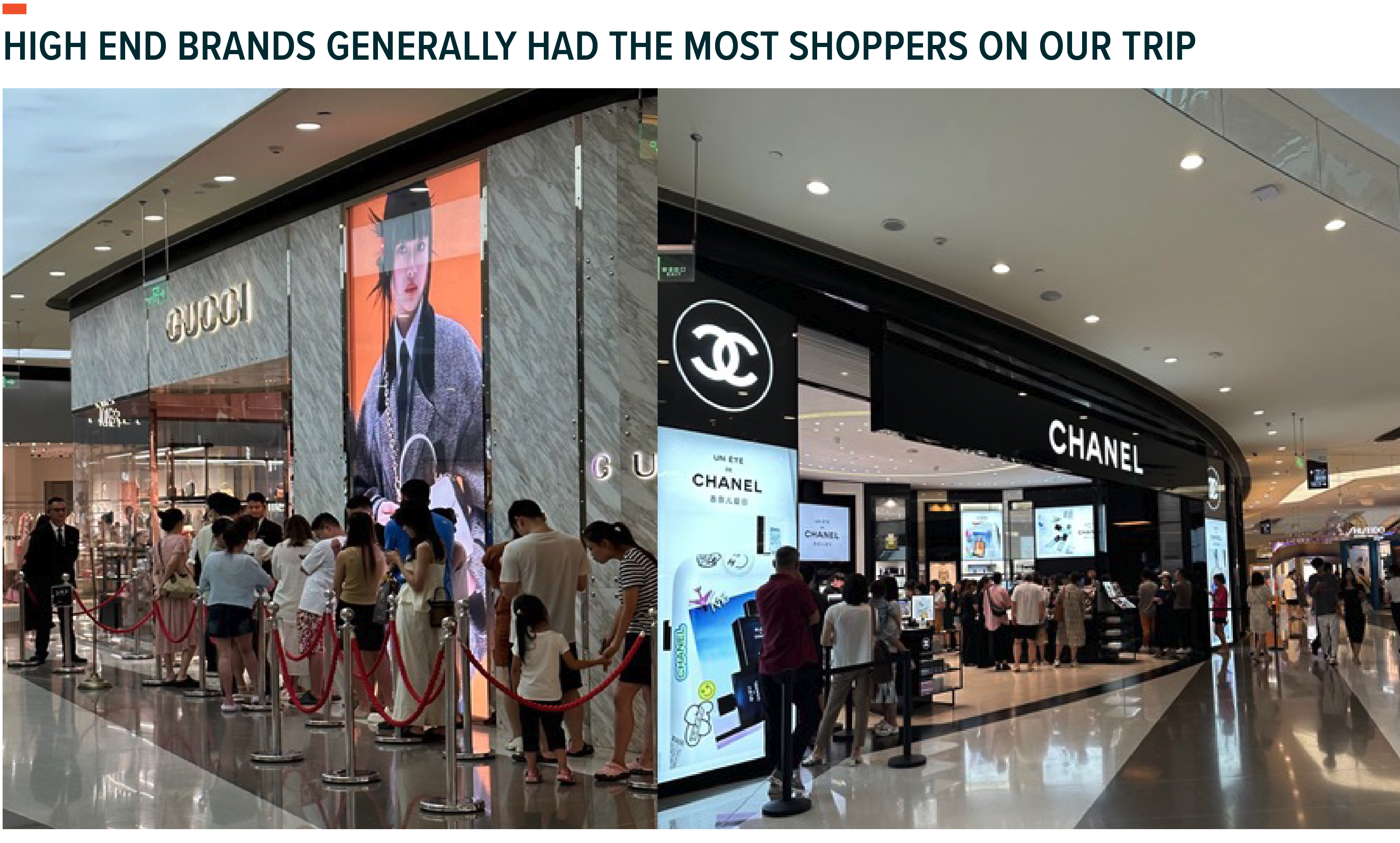

Consumption at the high end looked resilient to us. We visited Hang Lung Plaza 66 in Shanghai, which is one of the most luxurious malls in China. It seems it is not feeling any slowdown in its business, and brands continue to expand their footprints within the mall. Dior was expanding its space to 1,800sqm, using four floors in the mall. Similarly, Hermes was increasing its space to more than 1,000sqm. The mall has a five tier very important customer (VIC) program, of which Ruby requires spending an amount of Rmb 200K- Rmb 1mn and over Rmb 1mn for Sapphire. The highest tier is Emerald, which is by invitation only. Many Sapphire customers ask how much they need to spend to receive an invitation to Emerald. Watch sales can be quite volatile because volume is relatively small, but fashion and leather goods have seen steady growth with no sign of slowdown.

Local Brands Could Continue to Gain Market Share

As China’s economy grew and its middle class expanded, it wasn’t surprising to see local brands gain market share. Investments in technology, research & development, and manufacturing helped to close the innovation gap with Western competitors, while local knowledge gave Chinese companies a leg up in marketing and understanding domestic tastes. We’ve seen everything from local snack makers finding the right flavor profile to Chinese appliance manufacturers designing stove top/hood combinations that work better with woks versus American and European brands. Now, an uneven recovery following strict COVID-19 lockdowns and geopolitical tensions appear to be accelerating this trend, as China seems to be looking increasingly inward for growth.

Our sense is that while multinational brands may have an easier time raising prices near term, domestic brands could hold a long-term advantage. For example, high-end sportswear seems to be outperforming traditional brands, and popular products from Solomon, Fila, and Arcteryx appear to be selling well even with much higher price points than Nike and China-based Li Ning. As Li Ning raised prices quite aggressively in the past two-three years, we heard from distributors that there were customers complaining about Li Ning becoming too expensive. Li Ning is still cheaper than Nike, but this may be more of a brand perception issue. It takes time for consumers to accept higher pricing of Li Ning, and the company may need to launch more new products with better technology to justify higher pricing. Premiumization is often a hard job for new brands and can take time.

We think local brands can be competitive and believe many will continue to gain market share, although growth rates may slow after strong share gains by local brands like Li Ning and Anta in the past two years. One of the distributors we spoke with told us that compared to consumers born between 1980-95, those born after 1995 tend to have much stronger preference towards local brands, so time looks to be on local brands’ side, in a way.

Similar Trends Could be Emerging in the Technology Space

Given the national security concerns inherent in the tech sector, domestic firms could see support from both the top down and bottom up. In addition to the aforementioned shift toward local brands among the younger generation, geopolitical tensions and a trade war with the U.S. have the Chinese Communist Party (CCP) focused on self sufficiency and security. Historically, the CCP has shown a desire to control the economic backdrop and deliver consistent economic growth. Given its far-reaching powers, the Chinese government has multiple levers beyond traditional monetary and fiscal policies, which means the market should not underestimate the CCP and its potential impact on China’s consumption patterns.

For example, China recently instructed officials at central government agencies to halt the use of Apple’s iPhones and other foreign-branded devices for work, and such devices are no longer permitted in offices.1 The move is a blow to Apple, which is a leader in China’s high-end smartphone market, but could present an opportunity for domestic firms, such as Huawei Technologies.2 Huawei, which has struggled against U.S. sanctions on 5G technologies, recently launched an improved flagship device, which could benefit if iPhones fall out of favor.3

Conclusion

Expectations for China’s post-COVID-19 reopening did not live up to investors’ lofty expectations in the first half of 2023. However, we continue to see pockets of strength and believe that the myriad structural growth drivers we see in the country remain in place. The nation’s recovery following strict COVID-19-related lockdowns is unlikely to proceed in a linear fashion, but our time on the ground suggests that the reopening is ongoing, presenting potential opportunities for investors. We remain optimistic about the long-term attractiveness of China’s shift toward higher quality, consumption-driven growth, and believe that any signs of deeper fiscal or monetary stimulus could drive an unexpected re-rating of Chinese equities.