Paul Dmitriev

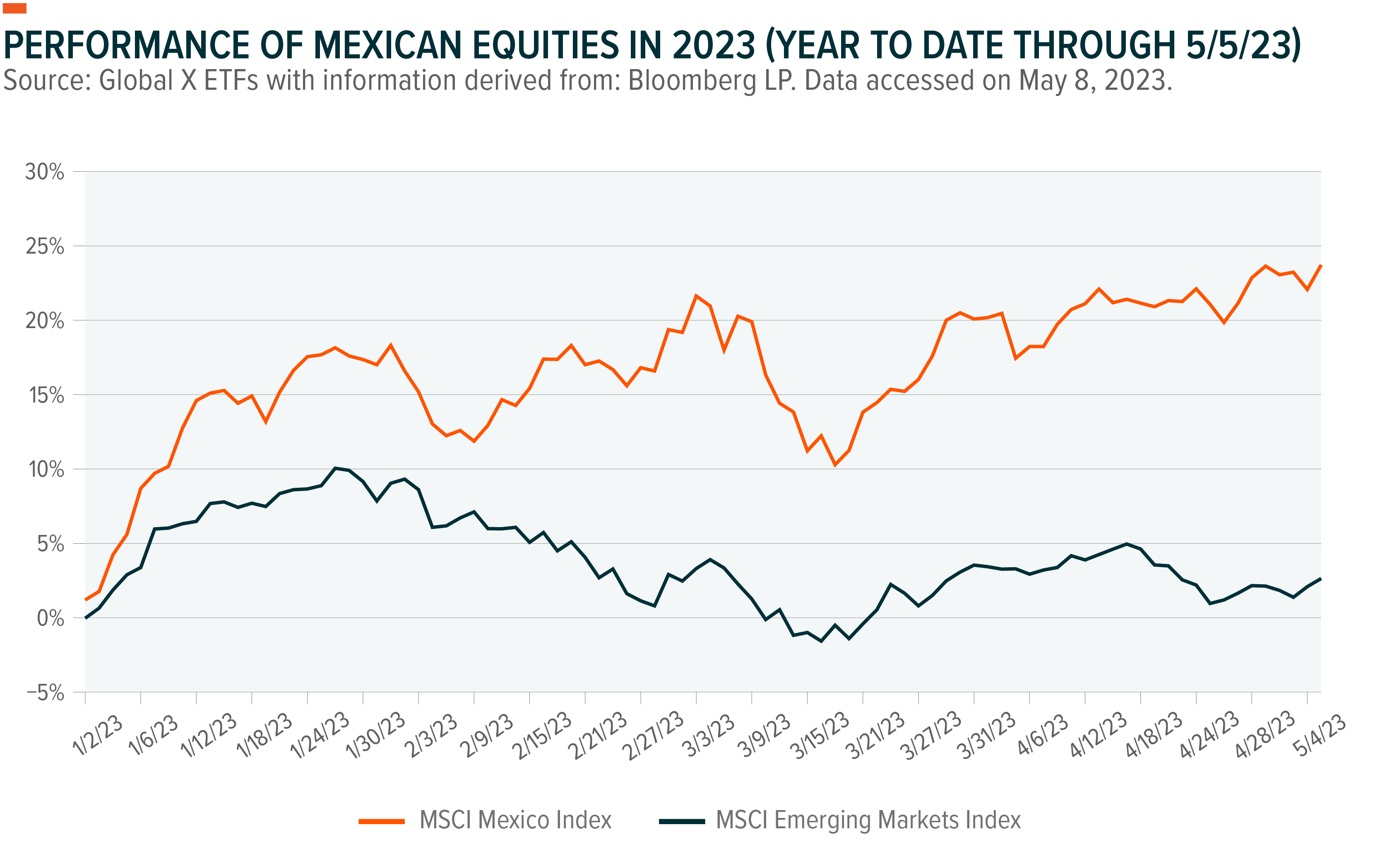

Paul DmitrievWe recently traveled to Mexico and met with political consultants, nearshoring and security experts, central bank members, ratings agencies, local pension fund managers, and corporations. We also completed site visits in northern Mexico, where nearshoring is front and center. Mexico has been one of the best performing markets in 2023, with the MSCI Mexico Index up 23.7% year to date through May 5th (24.6% including dividends).1 Although the country faces exogenous risks from a potential slowdown in the US, uncertain elections in 2024, and security risks, Mexico is differentiating itself from its Latin American peers and appears to have finally found a structural growth story with the emergence of nearshoring. In addition, Mexico has benefited from a strengthening peso, a prudent and independent central bank that has decoupled from the US Federal Reserve, positive pension reforms, and an opportunity for normalization in politics. We are optimistic for the country’s potential as it looks to take advantage of its new “Mexico Moment.”

Past performance does not guarantee future results. One cannot invest directly in an index.

Key Takeaways

- Mexican equities have notched impressive gains in the first four months of 2023, likely aided by a resilient peso, pension reforms, and a prudent and independent central bank.

- As the US seeks to decouple from China, Mexico is poised to be a potential winner from nearshoring, as American corporations look to diversify supply chains, reduce transportation expenses, and take advantage of Mexico’s low-cost labor pool

- We think recent changes to the government’s pension system could provide a tailwind for Mexican equities, though political and security concerns remain.

A Potentially Transformative Growth Engine in Nearshoring

Nearshoring appears to be gaining speed and relevance as “de-globalization” continues to take place. As competition and distrust between the US and China increased, companies began looking at not just cost savings and differences in labor, but also supply-chain security as a way to potentially mitigate geopolitical uncertainty. Strict and abrupt COVID-19 shutdowns in China, along with growing manufacturing and transportation costs, have also played a role in corporate decision making. For example, manufacturing labor costs grew 12.5% in China year over year (YoY) in 2020, to US$6.50/hour, compared to only 3.4% in Mexico, to US$4.82/hour, increasing the hourly wage difference between the two countries from 19% to 26% per hour.2 For the next 20 years or so, we think nearshoring has the potential to give Mexico a structural growth pillar that could support several sectors in phases, likely starting with areas such as manufacturing, transportation, and logistics before gradually supporting consumption, tourism, and other domestic industries. In our meeting with ASUR (Cancun airport operator), management was optimistic that demand for domestic vacations would increase and that ASUR could benefit over time.

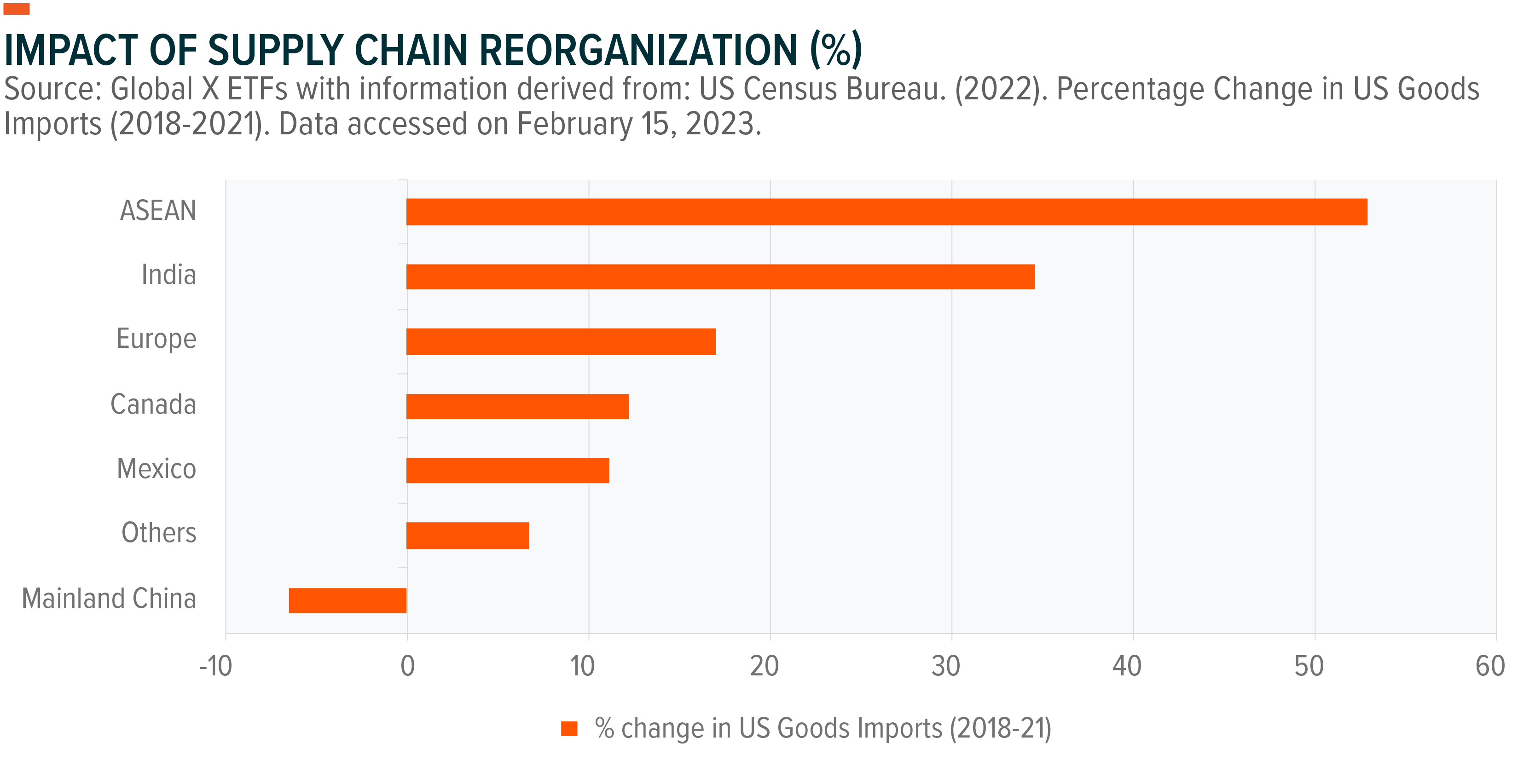

Mexico is no longer asking to join the table, instead it is the US and Canada that are asking for Mexico’s help as they seek to diversify their supply chains away from China. Consequently, we believe nearshoring could be a bigger opportunity for the country than joining the North American Free Trade Agreement in 1994. Current manufacturing exports from Mexico represented 35-40% of the nation’s GDP in 2022 and should continue to grow as existing manufacturing clusters, and emerging clusters, will likely continue to take manufacturing market share from Asian economies.3,4 In turn, we expect nearshoring to come in waves, as each technological cluster takes time to build, from the initial investment decision, to construction, to eventual manufacturing. The first wave continues to be driven by the automotive sector, as evidenced by Tesla’s recent decision to invest US$5bn in a new manufacturing plant outside Monterrey, but we believe that others, such as medical devices and semiconductors, could eventually follow.5 Importantly, Mexico continues to move up the supply chain into higher value-added products. Our visit to Monterrey, a key nearshoring beneficiary, surprised us with the amount of expensive cars, full restaurants, and construction on new warehousing capacity compared to Mexico City. We met with managers at Banregio, a Monterrey-based bank, who mentioned that consumers are experiencing increasing disposable income, already supporting what we saw on the ground. We met with a management team at Fibra Uno, a Mexico-based real estate investment trust, that pointed out high rental prices, labor shortages (not just in northern Mexico near the US border), brisk growth in Monterrey, a surge in industrial park capacity, and growing imports of capital goods, all of which suggest that nearshoring is happening, and probably even accelerating. The team at Fibra Uno also shared their estimation that every square meter of manufacturing capacity needs roughly two square meters of logistics capacity, which would further highlight the knock-on effects from nearshoring.

What’s Driving the Peso?

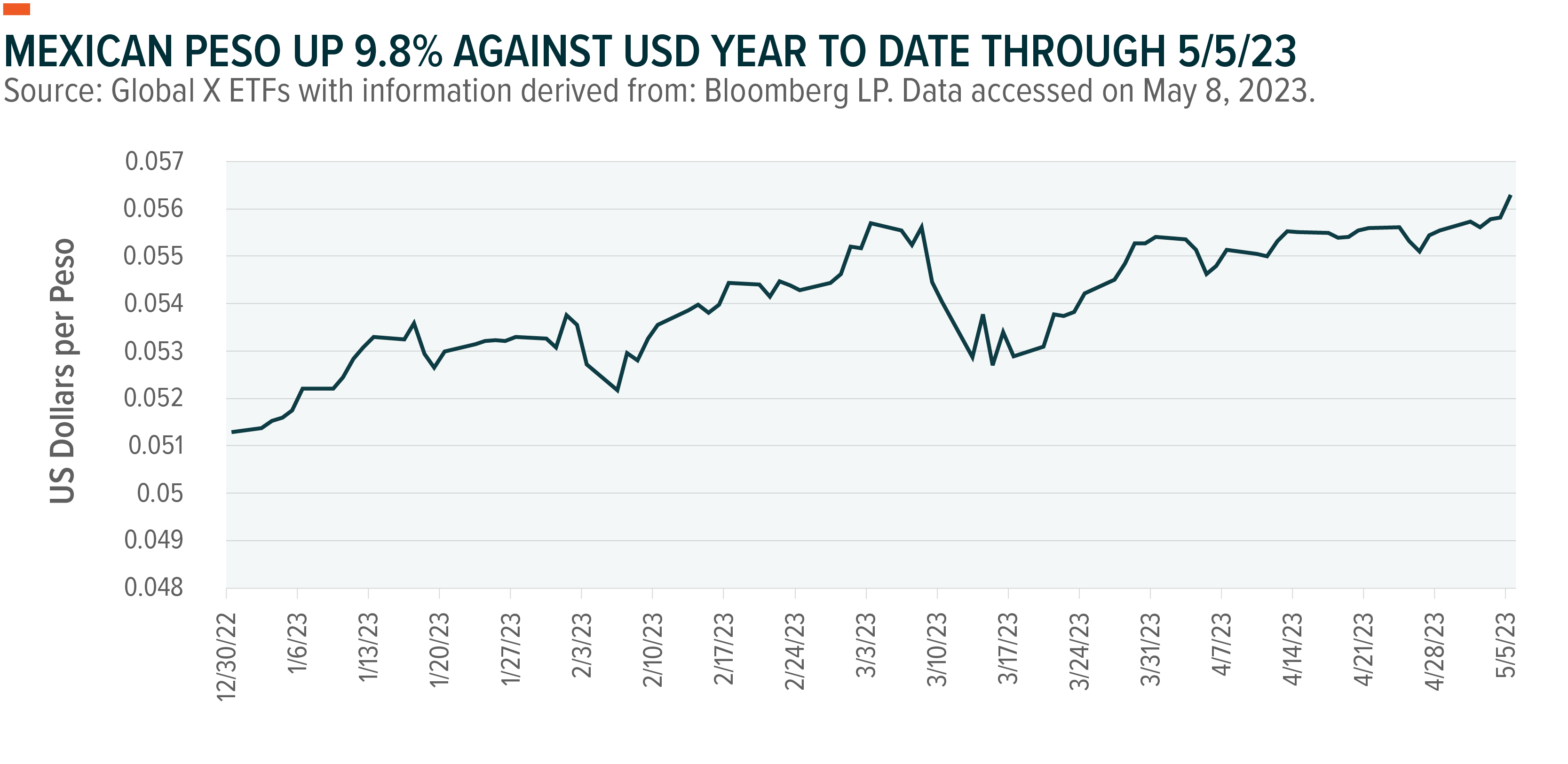

Recently, Mexico’s peso has been more resilient against the US dollar, and other emerging market (EM) currencies, than expected, appreciating 5.2% in 2022 and another 9.8% year to date through May 5th.6 We see this as having been driven by (1) moderation in monetary tightening in advanced economies, (2) positive market perception of domestic policies, and (3) a deep and highly liquid foreign exchange market, which helps mitigate some foreign inflationary pressures, rather than the usual assumption of remittances and nearshoring. Lower outflows from Mexico’s government bond market, as well as reduced US Treasury purchases by Mexicans, also appeared to help support the peso. Looking ahead, we think the valuation of the peso appears fair, given light positioning, strong carry, lower geopolitical risks relative to other EM countries like China, a hawkish-for-longer Bank of Mexico (Banxico), expectations for policy continuity, strong fiscal accounts, and a likely recovery in tourism.

Historically, Mexico has been perceived as a high beta, or more volatile, play on the US economy, meaning that it is viewed as moving with greater momentum, either up or down, relative to the US. This is largely due to increasing interlinkages between the two economies, along with increasing remittances, which have surged in recent years and can top US$5bn a month.7 However, according to one senior Banxico economist we spoke with, Mexico typically has weaker monetary policy transmission through the economy of an estimated four-six quarters relative to more-developed economies, due to lower financial penetration and a large informal market. In addition, Mexican inflation has been more persistent and run hotter than in the US. Importantly, Banxico has maintained orthodoxy and adherence towards its single mandate of 3% inflation, and it has responded rapidly, hiking rates by 725 basis points (bps) over the course of 15 consecutive meetings starting in June 2021 in an attempt to achieve convergence to its target.8 Our meetings with Banxico also suggested that, despite changes at the Central Bank Board, less experienced members have leaned on existing staff, appear willing to stay in restrictive territory for longer, and do not feel the need to follow the US Federal Reserve in lockstep – i.e. they have been able to “decouple.” Banxico starting its rate hiking cycle ahead of the US is further evidence of decoupling. Mexico has seen other prudent reforms, including pension reforms that took place in 2021 and were not highly covered by the press. Going forward, we expect Mexico’s good performance to continue, at least in a relative value setting versus LatAm peers, which will likely trade with political headlines and commodity cycles. On the other hand, we think Mexican valuations are more likely to remain attractive, as positioning remains light and we are starting to see two structural stories play out (i.e., pension reform and nearshoring).

Pension Reform

Although it has largely gone under the radar, recent pension reforms will likely have a drastic impact on flows, valuation, and overall investment in Mexico through 2030. The changes were effective as of January 1, 2021, but most will be gradually phased in. Highlights include (1) an increase in total contributions from 6.5% to 15% of salary over eight years, with employer contributions climbing from 5.15% to 13.87%, (2) the average worker is anticipated to see his/her retirement benefits increase approximately 40%, (3) a reduction to the required number of contribution weeks to be eligible to retire and receive the minimum guaranteed pension and, (4) a decrease in commissions charged by AFORES (pension funds).9,10 The roughly 100bps-per-year increase in total contributions from 6.5% in 2022 to 15% in 2030 could approximately double AFORES’ assets under management (AUM) to more than 10tn Mexican pesos (MXN), which could represent some 39% of Mexico’s GDP.11 Assuming no change in investment allocation, 51% would be invested in government debt, 15% in domestic corporate debt, 12% in foreign equities, 8% in structured investments and 7% in domestic equities.12 Assuming this increase in AUM, investments into Mexican equities could add MXN350bn (7% of MXN5tn), or approximately 4.9% of the Mexican Stock Exchange’s (MexBol) recent market cap.13 Just as importantly, the reform is expected to benefit 14mn employees and increase the number of eligible workers for retirement by 50%.14

Security

Mexican security issues have recently been in headlines and could pose a risk to nearshoring, something we were reminded of during our visit, as stoplights turn into de-facto yield signs to help reduce the risk of hold-ups at red lights at night. Generally speaking, the fight against organized crime only began in earnest in 2006 under the Calderon Administration. Due to the late start, Mexico has historically suffered from weak institutions (police, attorneys, jails, etc.), and Calderon’s successor, Enrique Peña Nieto, did not increase budgets to fight crime. The current Administration of President Andrés Manuel López Obrador (AMLO) has generally focused more on social programs and reducing poverty over reforming the judicial system or investing in local police forces.15 This appears to be one factor that has allowed criminal organizations to expand their activities, the worst being attempts to control and influence local governments and political institutions. Not only is this bad for business, but also for social life. In turn, it also forces companies to spend more on security. We met with Guillermo Valdes, Mexico Former Director, Center of Investigation & National Security, who told us that crime has gone from roughly 80% drug trafficking to less than 50% drug trafficking over the past 20 years, as gangs have diversified into activities such as theft from oil pipelines, trafficking people to the US, and robberies on roads/railways (the most common impact on corporations). Valdes also noted that although US-Mexico cooperation helped take down the violent Zeta gang, recent moves by US hardliners to label gangs as terrorist organizations risks backfiring, as it can create a stronger rejection of US presence and cooperation. Given the anticipated scale of potential opportunity ahead for Mexican firms on the back of nearshoring, the next administration will likely have to find a way to work in tandem with the US to improve security to not threaten future foreign direct investment (FDI) decisions.

Is Gridlock Good for Growth?

With elections around the corner in 2024, it is looking increasingly likely that either Claudia Sheinbaum or Marcelo Ebrard will run as AMLO’s successor under the Morena flag (presidents in Mexico are limited to a single six-year term). However, unlike AMLO, neither candidate has the same “cult of personality” that has helped him maintain an approval rating north of 60%, despite questionable performances on the economy and security.16 While Sheinbaum or Ebrard may win, the Morena party appears increasingly likely to face further losses within Congress, which could create even more gridlock. In turn, this could force Morena leadership to move to the center and bargain in order to get much done. Furthermore, as Morena was created by AMLO, for AMLO, we are starting to see divergent factions emerge amongst the party, which could weaken its base against opposition parties with strong regional footholds. As nearshoring continues to grow in importance for Mexico and states start to see tangible benefits, being an obstacle to this growth would likely turn any leader that acts in opposition into a lame-duck and risk long-term damage to his/her political party. In our view, it is becoming clear the country needs reforms that target energy, infrastructure, and institutional strength to maintain a GDP growth rate of 1-2% per year.

Conclusion: Numerous Structural Tailwinds Could Support Growth

In our opinion, Mexico appears to have a tremendous opportunity ahead to potentially benefit from many years of growth, driven by structural tailwinds including (1) nearshoring, (2) pension reform, (3) improving international relations and, (4) political stability. In emerging markets, which are rife with unexpected change, investors generally seek out and, in many cases, even pay a premium for stability. Mexican equities, as measured by the MSCI Mexico Index, were recently trading at a 11.8x price to earnings (PE) ratio (based off estimated 2024 earnings), which is below their historic multiple of roughly 13x.17 By investing in energy, infrastructure, and people, we believe the country could benefit from waves of growth that could dissipate through all sectors of the economy. Active managers have opportunities to take advantage of these trends as they permeate through the economy. Every meeting during our trip was positive on the potential Mexico has with nearshoring trends, but coupled with the aforementioned tailwinds, we believe the country could surprise on the upside.

Related ETFs

EMM – Global X Emerging Markets ex-China ETF

EMC – Global X Emerging Markets Great Consumer ETF

Click the fund name above to view current holdings. Holdings are subject to change. Current and future holdings are subject to risk.