Global X Research Team

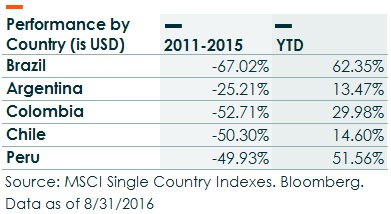

Global X Research TeamFrom 2011 to 2015, the commodity ‘super cycle’ cooled down and reversed, punishing economies that had become too dependent on exporting raw materials. South America’s largest economies — Brazil, Argentina, and the Andean nations of Colombia, Chile, and Peru — were particularly affected, with declining export values causing GDP growth to fall, currencies to weaken, and stock markets to sell off. Yet in 2016, these five countries have been among the best-performing emerging markets.

How did 2016 unexpectedly become the year of South America’s resurgence? In this piece, we discuss how the strong performance of equities in South America’s five largest economies have largely been driven by:

- A reversion to the mean in valuations of South American equities

- The rebound in key commodity exports, like oil, gold, iron, and soybeans

- Positive political developments in Brazil, Argentina, and Colombia

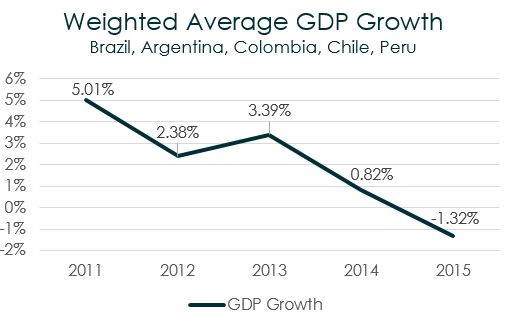

An important driver for this year’s returns in South America is a reversion to the mean, as abnormally low valuations for South American equities have begun to normalize. Economic growth among these regional powerhouses had deteriorated since 2011, with high-flying GDP growth falling from over 5% per year to a recession in 2015 with growth below -1%.

Source: Focus Economics, 2015.

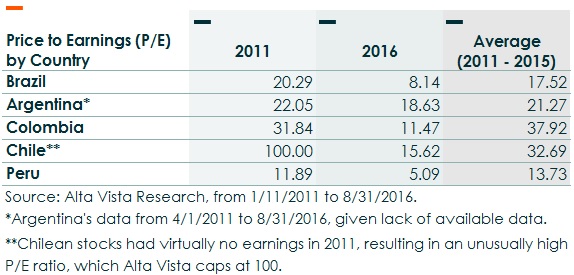

Going from such lofty GDP growth and expectations in 2011 to a recession in 2015 meant that some of the most desirable high growth securities in the world were being dumped in droves. This selloff pushed valuations from highs in 2011 to outright bargain levels by the beginning of 2016, as many of these countries were trading at less than half of their average price to earnings (P/E) from 2011 to 2015. Therefore, one explanation for the 34% average returns across these countries so far in 2016 could simply be a normalization of valuations back towards longer term averages.

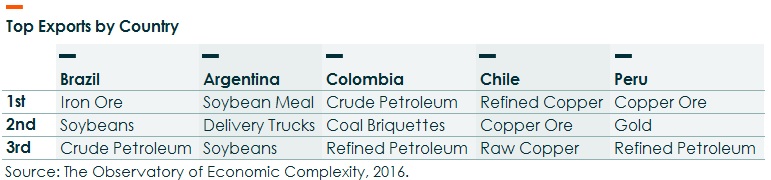

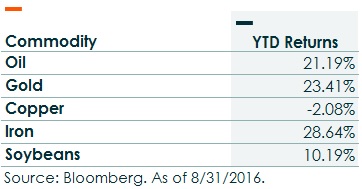

A second important contributor to the turnaround in these countries has been this year’s rebound in commodity prices. The end of the commodities ‘super cycle’ was the leading cause of the initial selloff, and therefore the rebound in key commodities exported by each of these countries has undoubtedly helped their economies, currencies, and markets regain strength.

In 2016, oil, gold, soybeans and iron have all rallied significantly. Copper, the lone top export commodity that is down this year, is a major export from Chile, which has not enjoyed such a sizeable turnaround as the oil exporting countries: Brazil, Colombia, and Peru.

Another factor contributing to the positive returns has been an improving political landscape. Brazil, Argentina, and Colombia have each benefitted from new leadership and/or policy reforms that markets have responded to favorably.

Brazil

Dilma Rousseff, from the Left-wing Workers’ Party, was impeached and replaced by new President Michel Temer, a right-leaning politician from the PMDB party. Many market participants view Temer as a more business-friendly leader than Rousseff, as he has pledged to reduce the government’s deficit, privatize state-run companies, and deregulate various industries.

Argentina

Argentina’s political resurgence began in late 2015 as the country elected Mauricio Macri, ending 12 years of rule under the leftist Peronist government. Since taking office, Macri has made rapid and meaningful changes including removing tariffs and trade restrictions, lifting capital restrictions and floating Argentina’s peso, and settling unpaid debts with creditors, allowing Argentina to return to international capital markets.

These changes have led to additional positive developments, including MSCI’s decision to review the country for a potential upgrade to Emerging Market status, and Argentina’s relative strength versus other international equities.

Colombia

In August, the Colombian government reached a peace deal with the FARC rebel group after 52 years of war that claimed over 220,000 lives and forced over 5 million people to relocate. Pending a national referendum in October, a peace deal is not only expected to boost national safety and morale, but also help to attract more foreign capital as international investors’ perception of Colombia improves with the deal.

Conclusion

The combination of normalizing valuations, a rebound in key commodity prices, and an improving political landscape, have all contributed to the phenomenal returns among South American equities in 2016. Despite high returns this year, extremely depressed valuations in South American equities and commodity prices could continue to revert higher towards long term averages over the coming years, providing additional tailwinds to these stocks. In addition, further progress in the political arena with quality leadership that promotes free trade, reduces government deficits, and tackles corruption, could also continue to propel the resurgence of South American stocks.

Global X offers five ETFs that target South American equities.

- The Global X MSCI Colombia ETF (GXG) invests in among the largest Colombian stocks.

- The Global X MSCI Argentina ETF (ARGT) invests in among the largest stocks of Argentine companies and companies with high economic exposure to Argentina.

- The Global X Brazil Consumer ETF (BRAQ) and Global X Brazil Mid Cap ETF (BRAZ) provide targeted exposure to domestic-oriented segments of the Brazilian stock market.

- The Global X FTSE Andean 40 ETF (AND) provides investors with broad exposure to the Andean region, comprised of Colombia, Peru, and Chile.