Colombia, priced for pessimism but positioned for recovery, offers an attractive asymmetric opportunity. Trading below 9 times earnings with a ~7% dividend yield, the market’s depressed valuation reflects policy uncertainty and macro headwinds under soon-to-be former President Petro. Upcoming elections could catalyze a shift back toward center-right leadership, potentially driving a re-rating similar to Argentina’s recent experience. Beyond valuations and politics, a medium-term recovery in Venezuela could represent additional upside, as renewed trade and supply chain integration could add meaningfully to Colombia’s GDP growth.

Key Takeaways

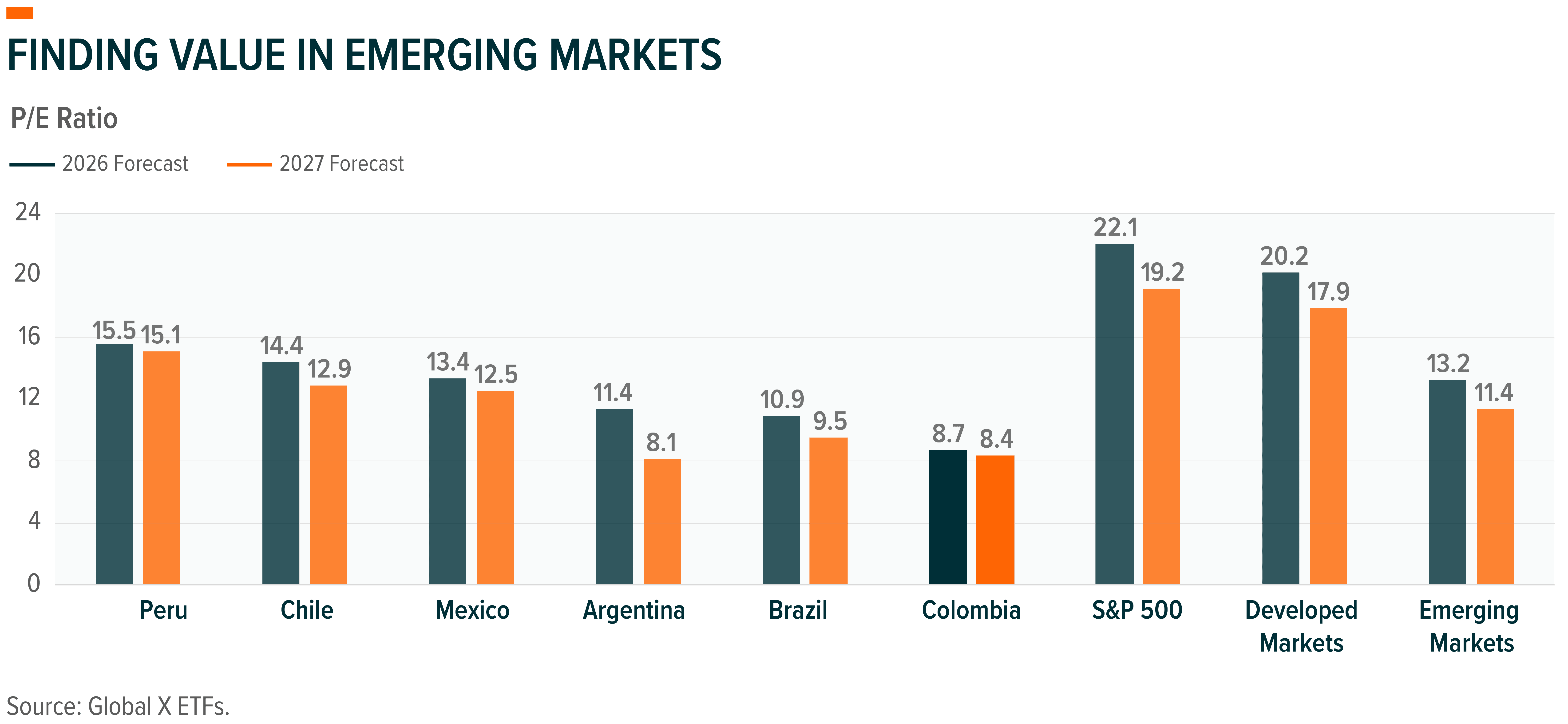

- Value: Despite recent strong momentum, Colombia is one of the cheapest emerging market countries and trades below 9x P/E with a strong ~7% dividend yield.

- Argentina 2.0?: Upcoming presidential elections in May present an opportunity for the country to return towards center-right leadership after four years of far-left control under the Petro administration. This could drive a market re-rating similar to the recent politically-driven rally in Argentina.

- A Venezuela Proxy: Although not a short-term driver, a recovery in Venezuela could present a tremendous opportunity for Colombia, given historic trade and economic ties.

Colombian equities offer a bargain value compared to other Latin American, broad Emerging, and Developed Markets. Even after a dizzying almost 200% rally over the past two years, Colombian equities still carry the lowest P/E multiple in the group at below 9x compared to 11.8x for MSCI Latin America, 13.2x for MSCI EM, and over 22x for the S&P 500 Index1. The depressed valuation reflected significant policy uncertainty and discontent that has plagued the market under President Petro since 2022. Macro imbalances and rising inflation following a larger-than-expected 23% minimum wage-hike represent short-term headwinds. However, the market’s ~7% dividend yield and deep valuation cushion help assuage our concerns2.

Understanding Colombian Politics and the Potential for Change

The important dates and catalysts for Colombian equities to follow are the March 8 Congressional elections and presidential consultas (consultas presidenciales), as well as the presidential election slated for May 31 (with a potential runoff on June 21). 100% of both chambers of the bicameral Congress, made up of a Senate and a Chamber of Representatives, will be up for election. The results will help determine the amount of support the future president will have from congress to implement policies. Importantly, the consultas are binding internal primaries that will select the main candidate from each party for the May presidential election. This will help consolidate the vote from the current wide range of candidates and should provide more color on the voting intentions from the current large proportion of undecided voters, which is still around 60%3.

On the left, we see support for Ivan Cepeda as part of the Pacto Amplio (left-wing coalition).Cepeda is running on a platform representing a continuation of President Petro’s current market unfriendly policies. Recent polling puts his support between 20-30%4. Although he was recently barred from participating in the consulta on March 8, we expect the left to eventually rally around him or Roy Barreras (politician and former ambassador to the UK) should Barreras significantly outperform current expectations at the upcoming consulta.

On the right is Abelardo de la Espriella, a right-wing independent candidate that is also polling slightly above Cepeda. His rise as an outsider with a strong presence on social media mirrors that of Milei in Argentina and Bolsonaro in Brazil. He will run outside the consulta system as an independent, which risks splitting the center-right coalition, the “Gran Consulta”. Despite close numbers in the polls, betting markets have Espriella roughly ten percentage points ahead of his next competitor5.

Amongst the center-right there are many candidates running, but Sergio Fajardo and Paloma Valencia are two of the leading candidates that we expect to perform well. Importantly, the consulta will help narrow the field and is a key milestone ahead of the Presidential election. There are 15 candidates running on center-to-right leaning pillars and only one promising continuation of market unfriendly Petro policies. This leaves us optimistic about a consolidated center-right vote in the second round.

Why Does This Election Matter?

After four years of leftist rule under President Petro, Colombia may be approaching a familiar inflection point we’ve seen recently across Latin America. In recent years, the political pendulum has begun to swing back toward economic orthodoxy under center-right leadership, as seen in Argentina and Chile.

Under President Petro, many Colombian corporates saw limited growth prospects and focused their capital allocation on opportunities outside of the country. Based on recent discussions with several corporates, we see this trend starting to reverse. As such, the presidential election could mark a turning point in the domestic growth story as the country restores fiscal discipline and unlocks investment.

Colombia: The Best Way to Play a Venezuelan Recovery

Under Maduro’s leadership, Venezuela faced increasing economic hardship, with the International Monetary Fund (IMF) estimating that nearly a quarter of the population (over 7 million people) have left the country since 2015. Nearly 3 million of those migrants fled to neighboring Colombia6,7. Should the situation in Venezuela stabilize, we see significant opportunities for Colombia. In addition to migration back to Venezuela, which could improve Colombia’s pressured fiscal accounts over the medium term, infrastructure rebuilding and supply chain reintegration would benefit Colombia, given their geographic and historical trade ties. Recent research reports estimate that a return of bilateral trade flows to pre-2010 levels could add ~1% to Colombia’s GDP over 3-5 years mainly through manufacturing and exports8. Before virtually closing its border to Colombian products in 2010, Venezuela was Colombia’s second largest export market, peaking at 17.4% of exports in 2007 versus less than 2% in 20249. The Venezuelan government stopped nearly all investment more than a decade ago and entire supply chains will need to be revamped before goods can easily flow into the country, which should create a relative advantage for Colombia given its shared border. Due to sanctions and shallow public equity markets, investments in Colombia likely provide the best proxy exposure to potential recovery in Venezuela.

Conclusion

Colombia represents a rare combination of deep value, identifiable political catalysts, and underappreciated regional optionality. With valuations pricing in persistent pessimism, a potential shift toward more market-friendly leadership and longer-term upside from Venezuelan normalization create a compelling asymmetric opportunity.