Energy shocks don’t just move prices, they reshape how countries think about supply. Severe supply disruptions act as reminders of the essential role energy plays in the world, underscoring how susceptible global economic growth is to energy prices. When risk and fear take over markets, it’s important to take a step back and look at the forest through the trees, and historically, it’s during these types of events where longer-term structural economic shifts occur.

Key Takeaways

- Energy’s critical role in enabling economic growth underscores the importance of consistent and secure supply.

- Energy shocks have the potential to cause countries to diversify their energy dependence from both a geographic and resource perspective.

- Many commodities, such as uranium and U.S. natural gas, stand out as potential long-term direct beneficiaries of this shift towards energy security.

Supply Disruptions Underscore the Fragility and Importance of Energy

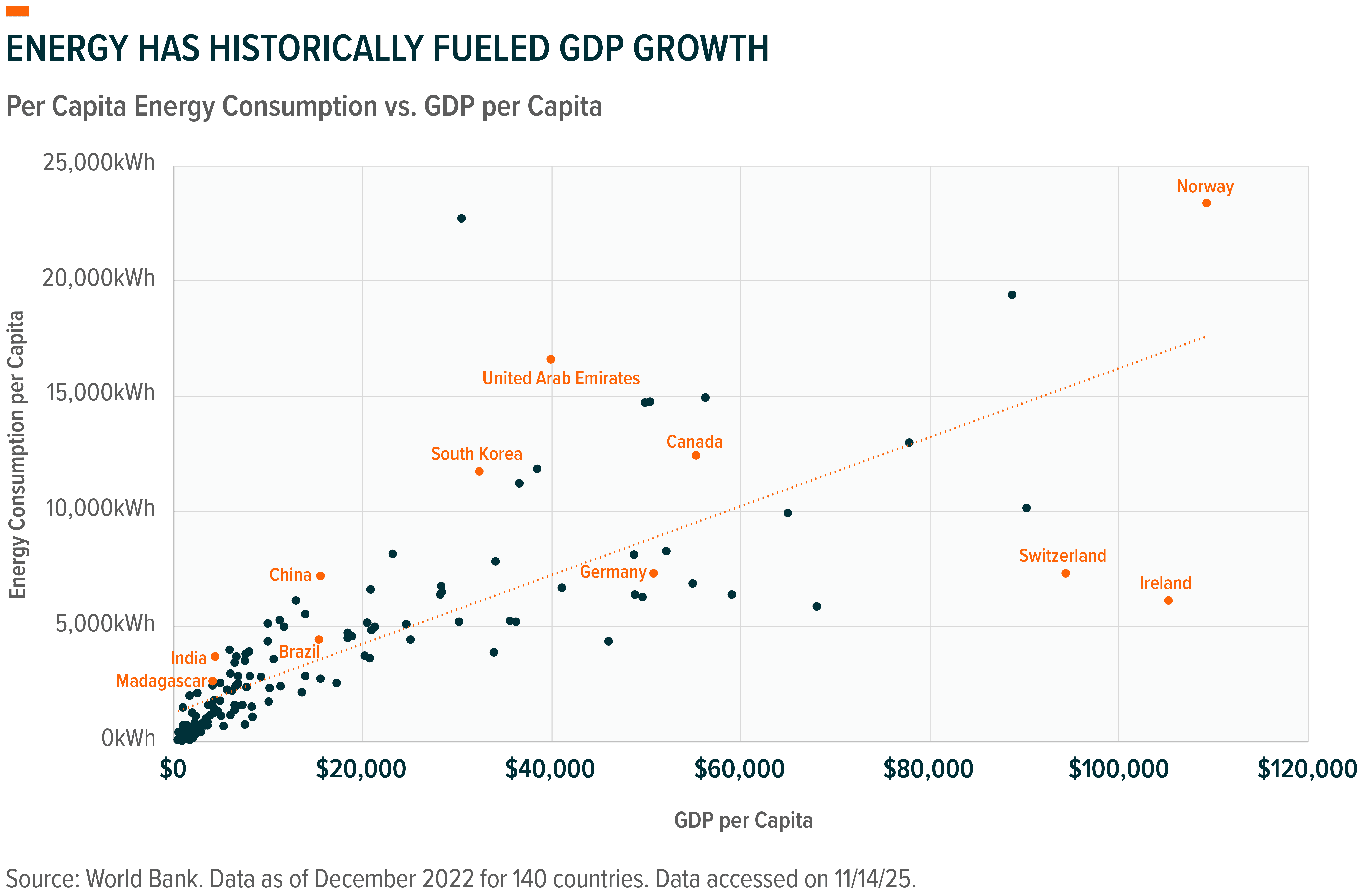

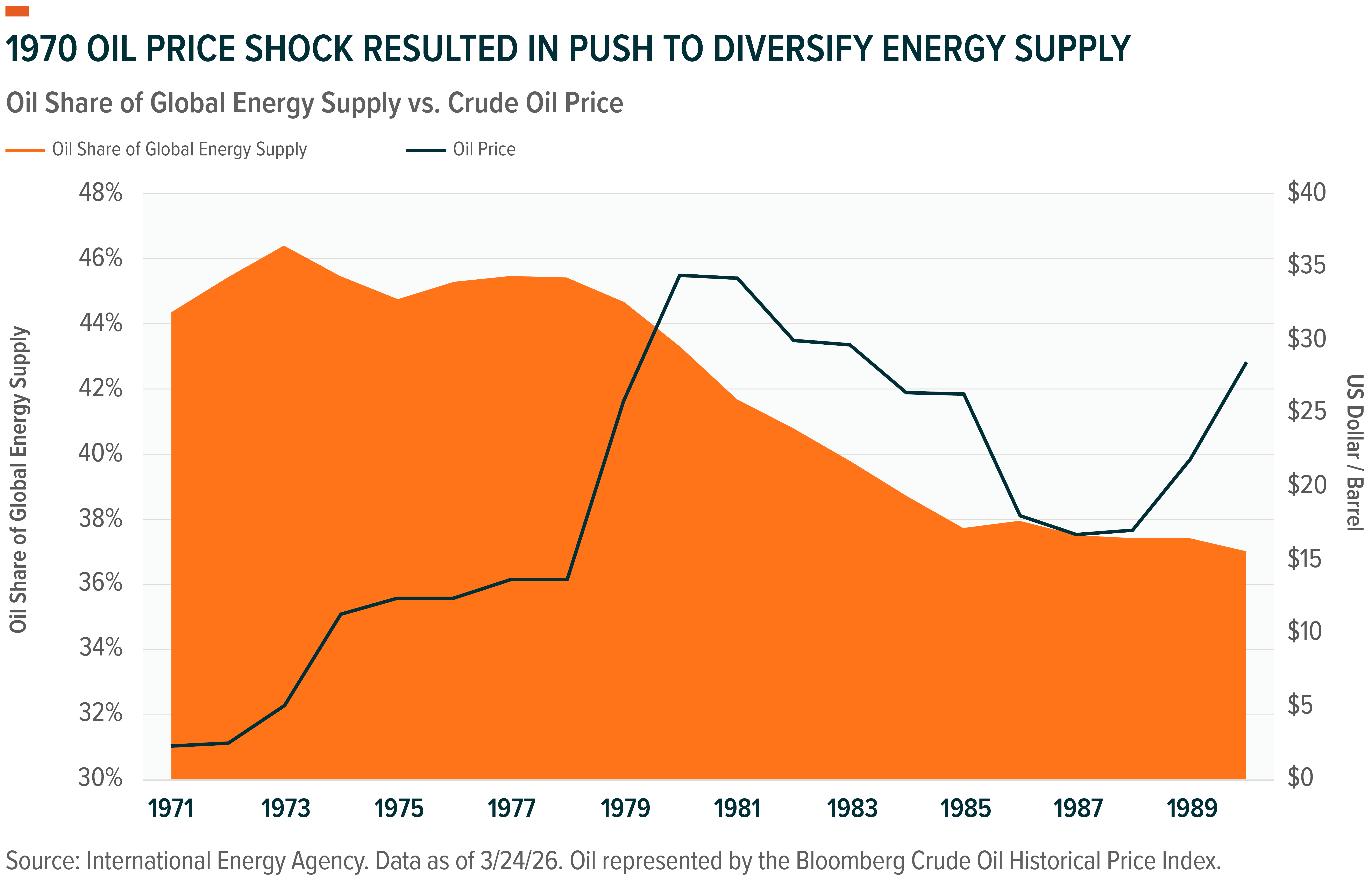

Major energy disruption events, such as Russia’s invasion of Ukraine, the 1970’s oil shock, or this year’s blocking of the Hormuz Strait, highlight not only the interconnectedness of the global energy market, but how energy truly enables global economic growth. Given energy’s essential role across many sectors of the economy, such as transportation and manufacturing, demand tends to be relatively price-inelastic in the near term. This means higher prices do little to curb consumption immediately. Instead, elevated energy costs act effectively as a tax on the global economy, squeezing consumers and increasing input costs for businesses. This added burden can weigh on industrial activity, trade, consumption, and can pressure overall growth.

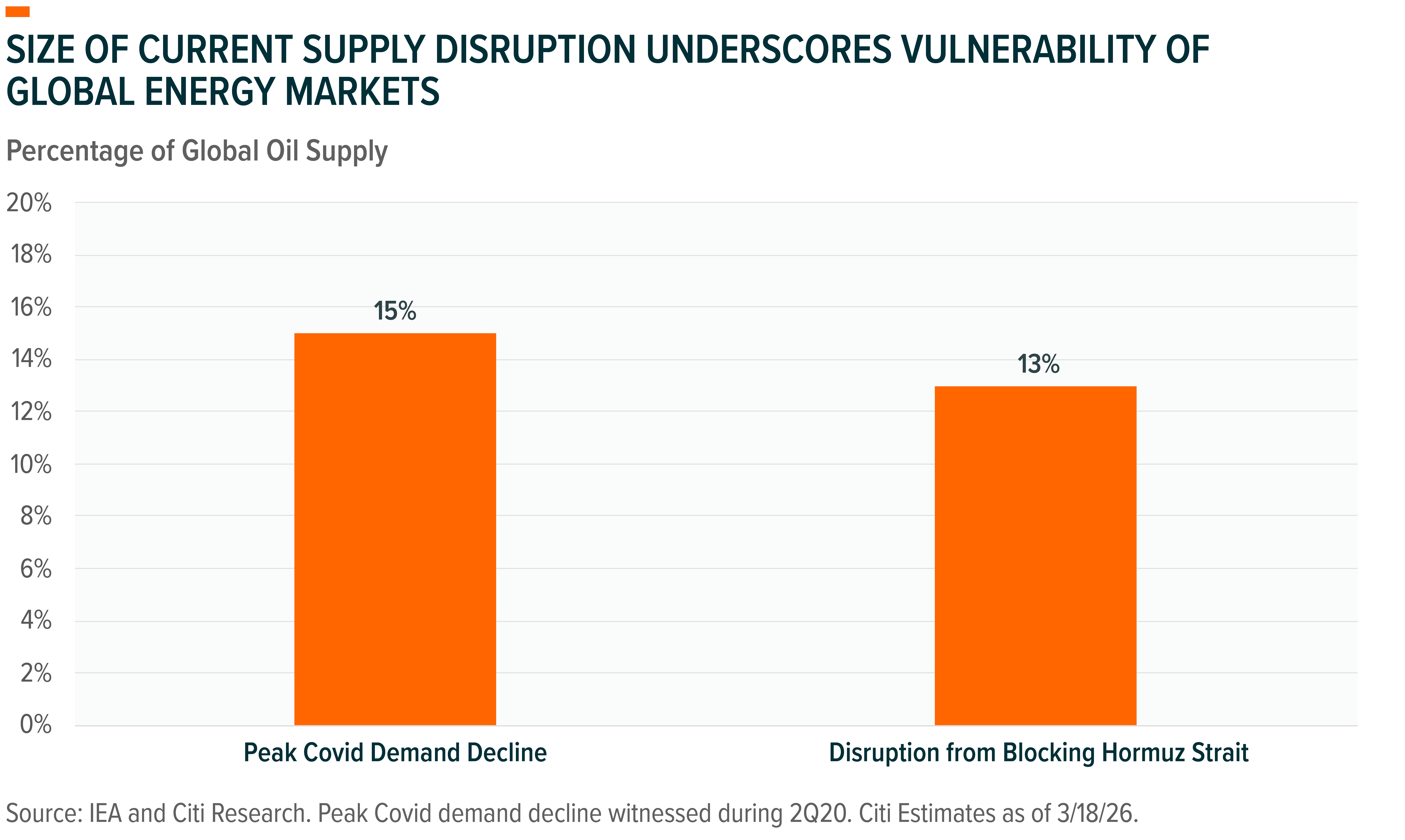

This year’s events have shown just how susceptible the global energy market is to a single geographic location. The closure of the Hormuz Strait has the potential to represent one of or the largest oil supply shocks in history, with the volume of supply temporarily taken offline comparable to the sharpest demand declines seen during the Covid-19 lockdowns.

Although the flow of energy through the Strait is expected to resume eventually, the risk of future major disruption remains. We believe a clear line has been crossed and that these types of risks, coupled with the critical role energy plays in the global economy, could change the thinking around energy supply over the medium-to long-term.

The Shift in Energy Strategy from Cost to Security

While price and return on investment have historically been the primary drivers of energy investment, supply disruptions reinforce the idea that security of supply is equally critical given energy’s central role across nearly all facets of the global economy. In our view, this supports a clear thesis: countries must diversify energy supply to enhance resilience and reduce tail risks. That diversification does not necessarily imply a move away from fossil fuels, but rather a reduction in concentration risk. This strategy involves diversification both geographically -- toward stable and trusted producers such as the U.S., Canada, and emerging suppliers like Argentina -- and across energy sources, with increased investment in nuclear and renewable energy such as solar. At the same time, the need for reliable baseload power remains essential, reinforcing that the objective is a more balanced and secure energy system rather than a wholesale shift away from existing energy sources. This renewed emphasis on security, following decades of cost optimization, could represent a structural tailwind for select industries and commodities.

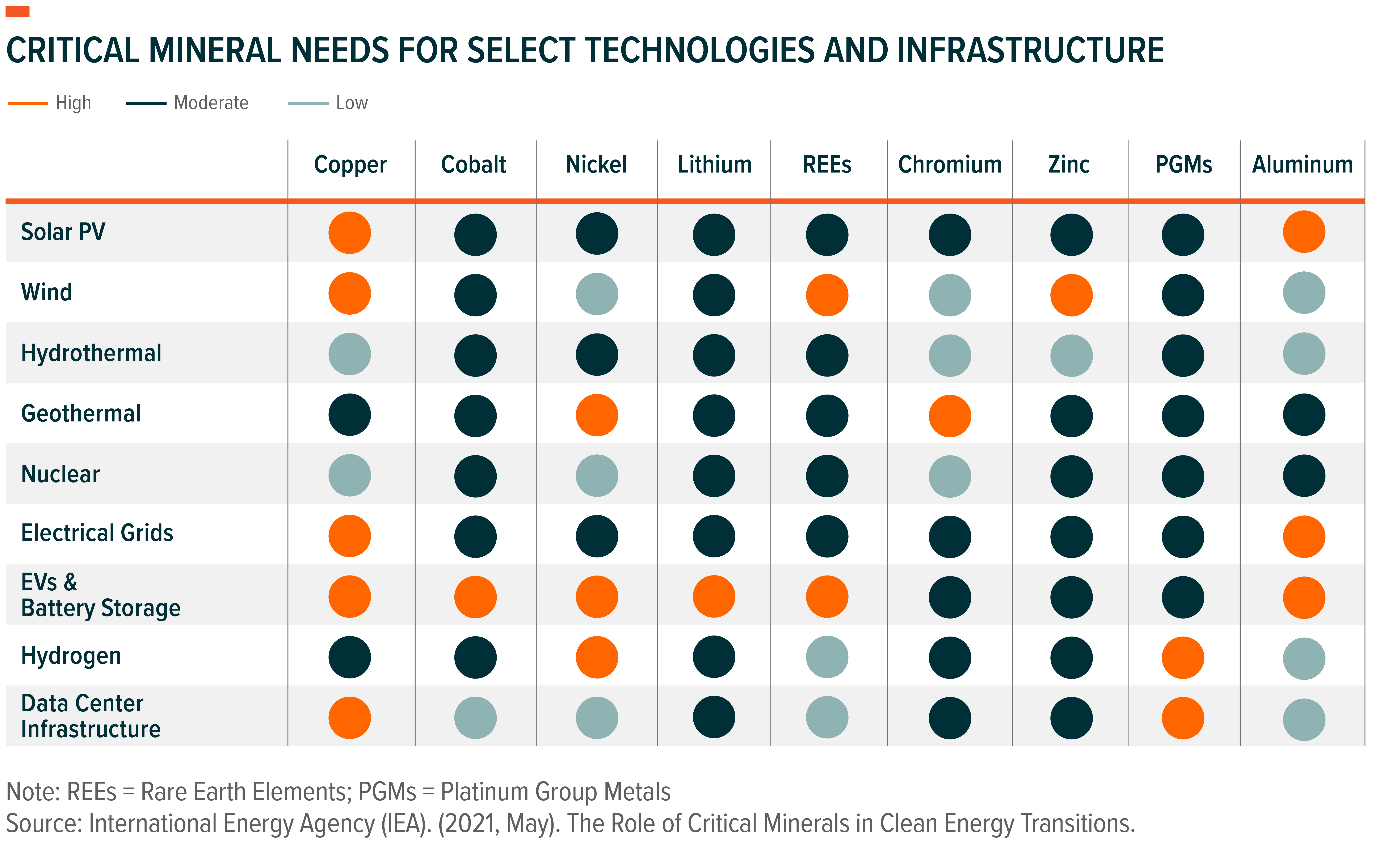

Which Commodities Could Benefit from Energy Supply Diversification?

In a world where power demand could inflect and reliable supply becomes increasingly important; we see the below commodities as potential winners:

Direct Beneficiaries:

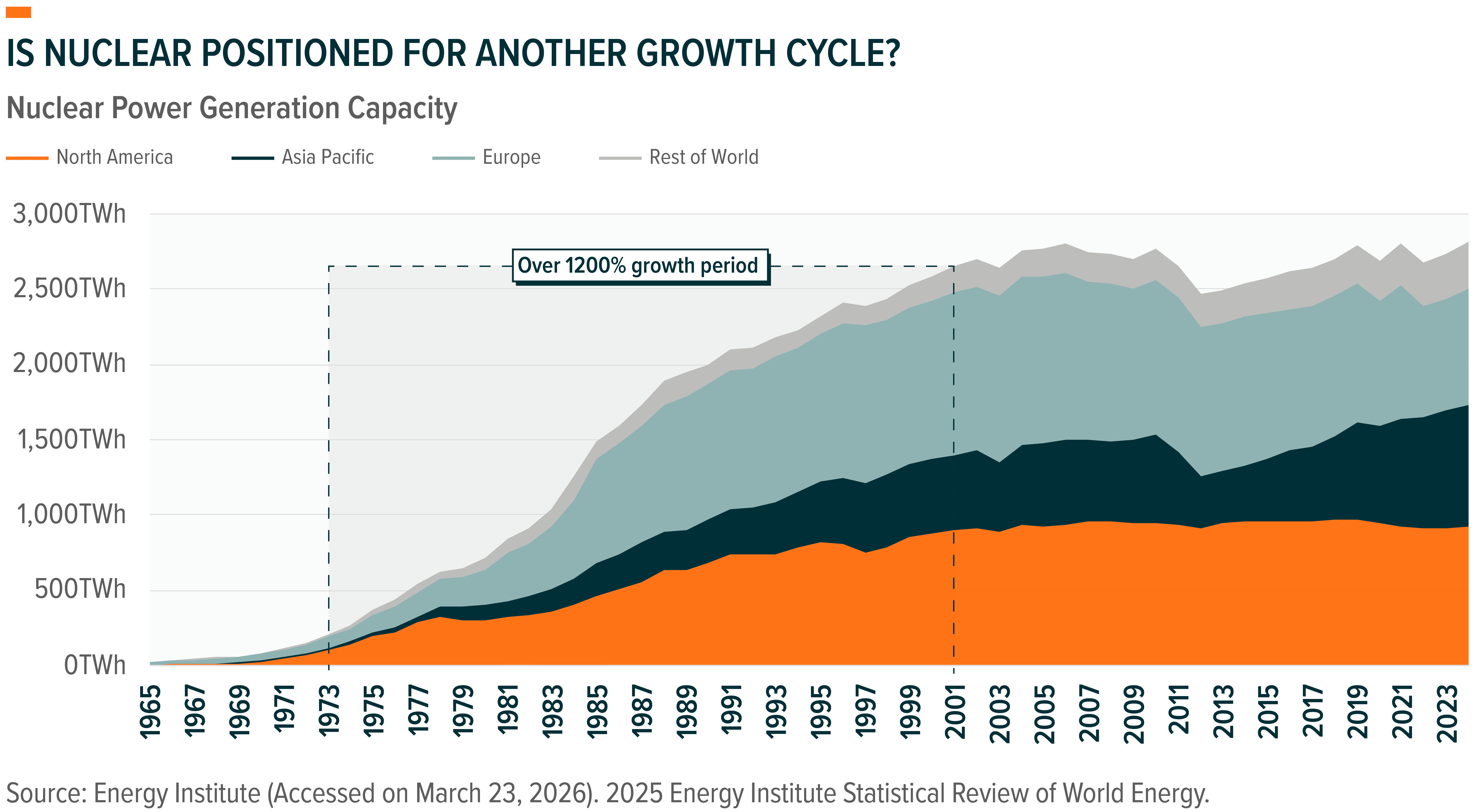

- Uranium: Nuclear energy represents a low cost, clean, and consistent source of energy, positioning uranium to be a clear beneficiary of both supply diversification and potential ongoing demand from structural trends such as electrification and AI.

- U.S. Natural Gas: U.S. liquified natural gas (LNG) players are positioned well to gain global market share given their ample supply, growing export capacity, and strategic geographical positioning. Increased demand for US LNG could also represent an opportunity for the domestic energy transmission industry.

- Silver: Solar power represents another potential alternative power generation solution, with solar becoming increasingly impactful on the overall silver market as it now represents roughly one fifth of total demand.1

Enablers:

- Copper: Diversifying energy systems to enhance security is likely to further accelerate electrification, adding to already strong demand from structural trends such as AI and grid expansion, reinforcing copper’s role as a critical enabler and further tightening an already constrained supply outlook.

Indirect Beneficiaries:

- Lithium: Diversifying energy sources to enhance security can also accelerate electric vehicle and battery storage adoption as countries look to reduce dependence on imported fossil fuels, ultimately providing additional support for long-term lithium demand especially in energy importing countries like China.

- Gold: Rebuilding energy supply chains and the strategic shift towards security over profitability should ultimately prove inflationary, benefitting stores of value such as gold.

Conclusion

We see energy supply disruptions as not just short-term price shocks but moments that could shift how countries think about energy over the long-term. The blocking of the Strait of Hormuz is just the latest example of the vulnerability of the global energy market, potentially acting as a catalyst for countries to increase investment in alternative sources of energy to ensure security of supply. We see this shift representing a structural tailwind for certain commodities involved in power generation, transmission, and storage, adding to the already robust outlook stemming from global electrification and AI trends. Overall, this energy shock once again underscores the critical role commodities play within a portfolio from a diversification perspective, while years of underinvestment and the emergence of new demand drivers positions the asset class well into the future.