On December 10, 2025, we listed the Global X Gold Miners ETF (AUAU) on the New York Stock Exchange ARCA. AUAU delivers exposure to companies primarily involved in the gold mining industry. The fund seeks to track, before fees and expenses, the NYSE Arca Gold Miners Index, a rules-based index that follows the performance of global publicly traded gold mining equities, weighted by market capitalization.1

Gold miners have historically leveraged gold’s price performance, dedicating cash flows toward increasing operational efficiencies, and sometimes returning value to shareholders via dividends and share buybacks.2 We believe AUAU’s holdings of gold mining stocks could introduce potential cash flows via its exposure to gold mining equities, where gold itself has traditionally been a non-cash flow producing asset.

Gold’s reputation as a potential safe-haven asset, which is derived from its scarcity and historic value retention properties, has led it to be adopted in the reserves of central banks and in investment portfolios worldwide.3 The investment ecosystem that surrounds gold, however, has a variety of inlets, and gold miners are participants that can offer return potential tied to gold’s value, as well some of the more conventional shareholder opportunities that are brought about through equity investing. Gold miners tap into the performance of the precious metal by realizing revenues from production volumes at prevailing prices. They are also able to utilize the cash flows that they generate from mining gold to reinvest and increase operational efficiencies and potentially remit dividends and repurchase stock. We believe the influence that these cash flows might have represents a material differentiator from physical gold and gold ETFs.

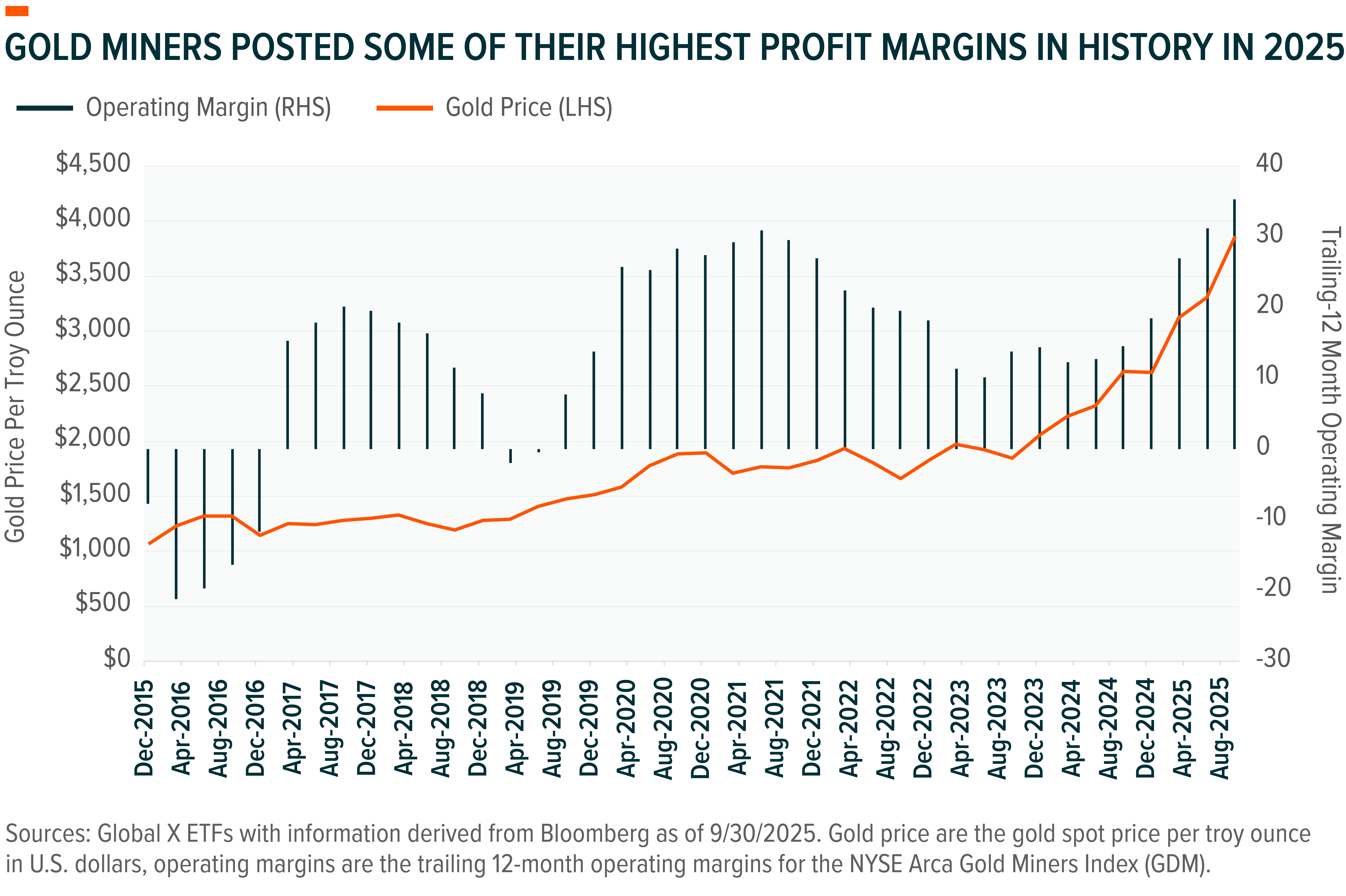

Gold’s qualities have taken on new meaning in recent years. Structural buying by global central banks, perceived currency risks, and the proliferation of global and macroeconomic risk factors all led gold to breach all-time highs in 2025.4 Amidst the historic rally, gold miners witnessed rapidly increasing profit margins that were pivotal to the triple-digit returns seen in the year-to-date performance of the NYSE Arca Gold Miners Index.5 While past performance is not a guarantee of future results, gold trades in the vicinity of its all-time high as of the end of November 2025, but we believe its rally may still have room to run given the structural tailwinds that have underpinned its advance. Further, we think gold mining equities stand out as an underappreciated and potentially underinvested segment in this space.

Key Takeaways

- Structural buying trends associated with central banks and fundamental shifts in the global macroeconomic environment have fueled gold’s record rally in 2025. We believe such factors are likely to remain intact going into 2026 and beyond.

- Historically elevated profit margins point to gold miners being undervalued and under owned as the trade into physical gold trusts becomes increasingly crowded.

- AUAU provides broad exposure to gold mining equities that may be able to leverage operational efficiencies and raise distributions during favorable markets, potentially generating cash flows compared to the traditionally non-cash flow producing asset, and potentially outperforming the underlying commodity.

A Historical Store of Value: Gold’s Record of Value Retention

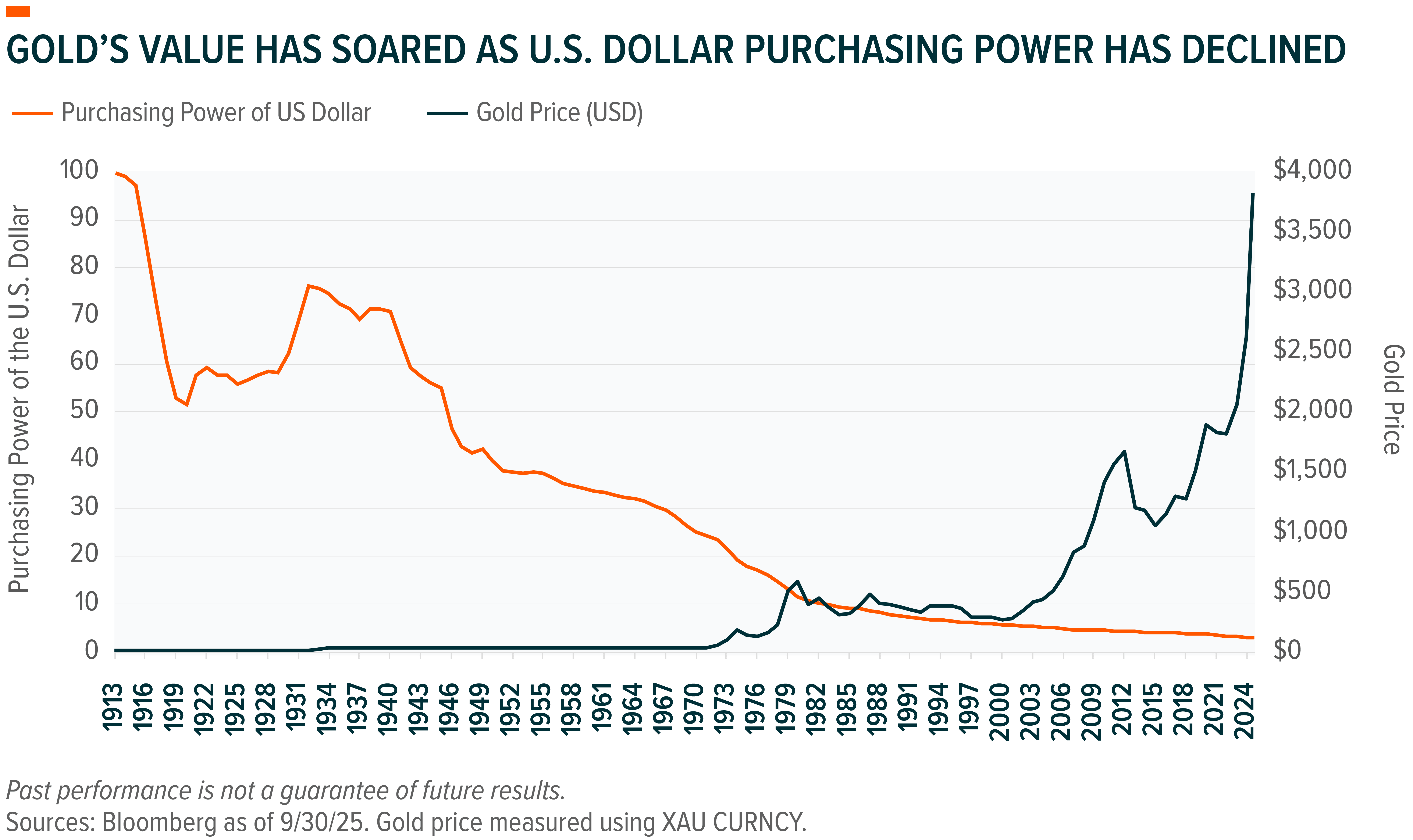

Gold’s track record has stood the test of time. It has maintained its purchasing power for thousands of years, with military salaries in 2023 still roughly on par with what Rome paid its legions millennia ago.6 It has even outperformed global equities and most major commodities as a medium of exchange since the unraveling of the U.S. gold standard in 1971 and the collapse of the Bretton Woods system thereafter.7 This is a status that deviates sharply with fiat currencies, which are not backed by gold, and have seen their purchasing power broadly eroded over the past 25-years.8 By contrast, the price of gold has risen by 9.1% on an annualized basis (from December 31, 1970 to the end of November 2025), a trend that runs counter to that of the U.S. dollar and many other major currencies that saw their purchasing power erode, which we believe demonstrates gold’s value retention qualities.9

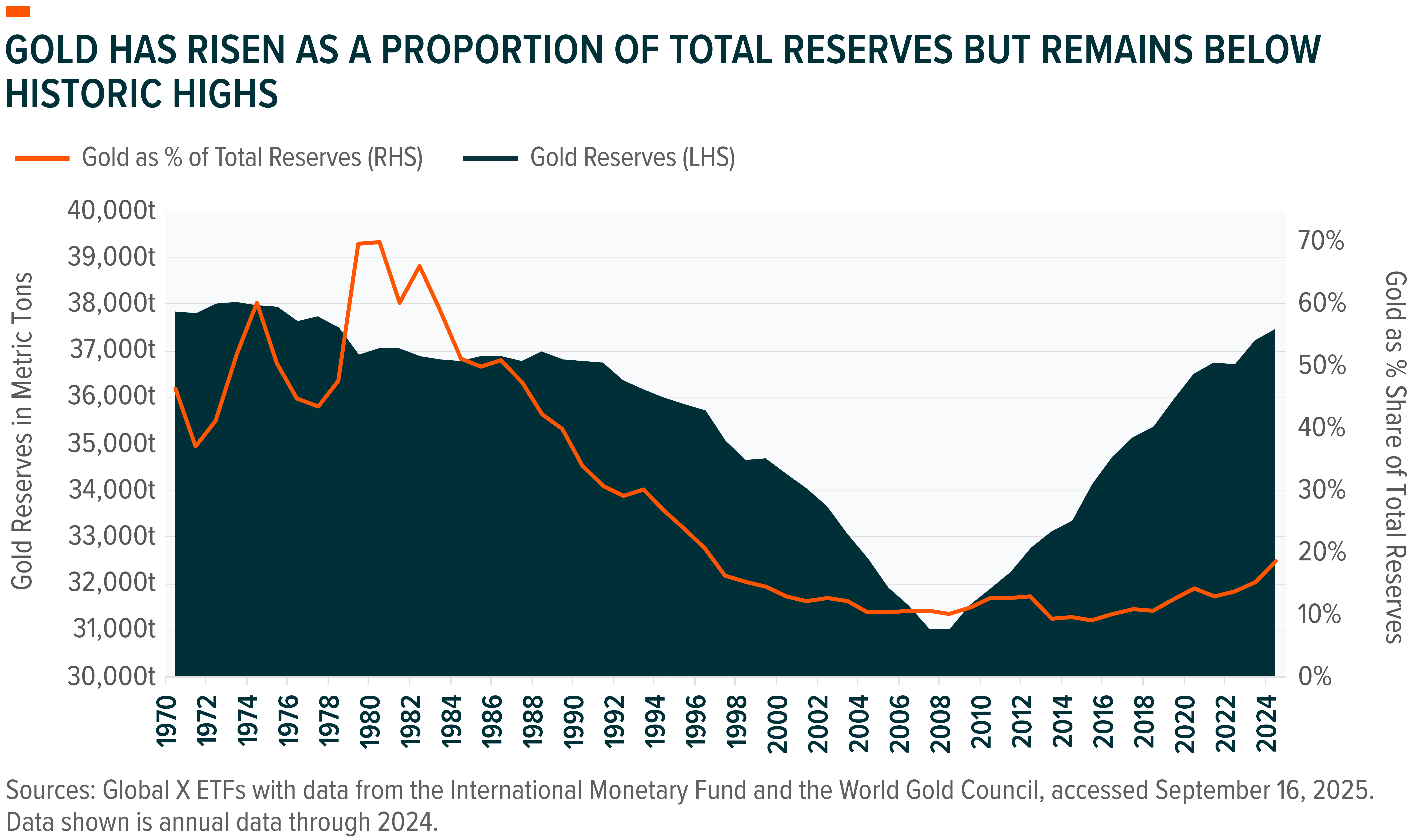

These features centered around value retention have supported investors’ willingness to adopt gold exposure over the years. Today, those traditional drivers are being amplified by a shifting macroeconomic landscape and geopolitical climate, shaped in part by the weaponization of dollar assets against Russia in 2022. Together these factors set the stage for the latest wave of global central bank gold buying. Since 2022, dollar debasement has led global central banks to acquire over 1,000 tonnes of gold per year, a pace roughly double the average annual rate of net central bank gold purchases from the decade prior. In fact, gold holdings as a proportion of global reserves now outweigh U.S. Treasury bonds for the first-time since the mid-1990’s.10

We view these trends to be structural in nature, given their geopolitical motivation. It’s important to note, however, that these recent shifts only represent an acceleration of the central bank purchases that markets had been witnessing dating back to 2010.11 At that time, investors were already rationalizing the value proposition that could be offered by gold. In the post-COVID era, however, heightened inflation and a diminished political appetite to curtail deficit spending is likely to have further stoked interest in precious metals. With gold’s performance during times of crisis, its inflation hedging qualities, and its role as a portfolio diversifier being cited as the three most relevant motivators for buying gold amongst emerging market central banks, these market forces may have logically driven monetary authorities to increasingly favor gold.12

While the pace of bank purchases has accelerated, we believe there remain a variety of other forces at play that may keep bank purchases of gold on the front burner. In fact, central banks have increasingly reported that gold’s proportion of total global reserves is likely to increase, with nearly 95% of survey respondents expecting global gold reserves to rise over the next 12-months, based on survey results from the end of June, 2025.13 Relative to the post-Bretton Woods high of ~70%, gold holdings as a proportion of total global reserves currently at roughly 19% at the end of 2024. While another post-Bretton Woods high remains unlikely in our near-term forecast, it does help depict the vast runway for continued bank buying that is possible, as monetary authorities worldwide signal little impetus to halt their gold purchases.

Gold Miners: A Different Way to Play the Gold Trade

Before gold reaches its end buyer, it must be prospected and extracted from the ground by gold miners. Gold mining stocks can entail a variety of participants that can include large gold producers that own multiple mines and operate across diverse jurisdictions; mid-tier producers that operate one or two mines; or mixed miners that produce a variety of metals. Regardless of size, one thing gold miners have in common is their ability to maintain a level of operational leverage to gold prices, as the relatively fixed nature of their cost structure can lead margins to widen, particularly if gold price advances outpace operating costs.14 Gold miner equity valuations can also hinge on operating efficiencies, balance sheets, and project investment opportunities, in addition to their ability to adequately manage their operations. During strong advances in gold prices, gold miners may generate excess cash flows which can be purposed toward improving balance sheets and/or enhancing shareholder distributions.15

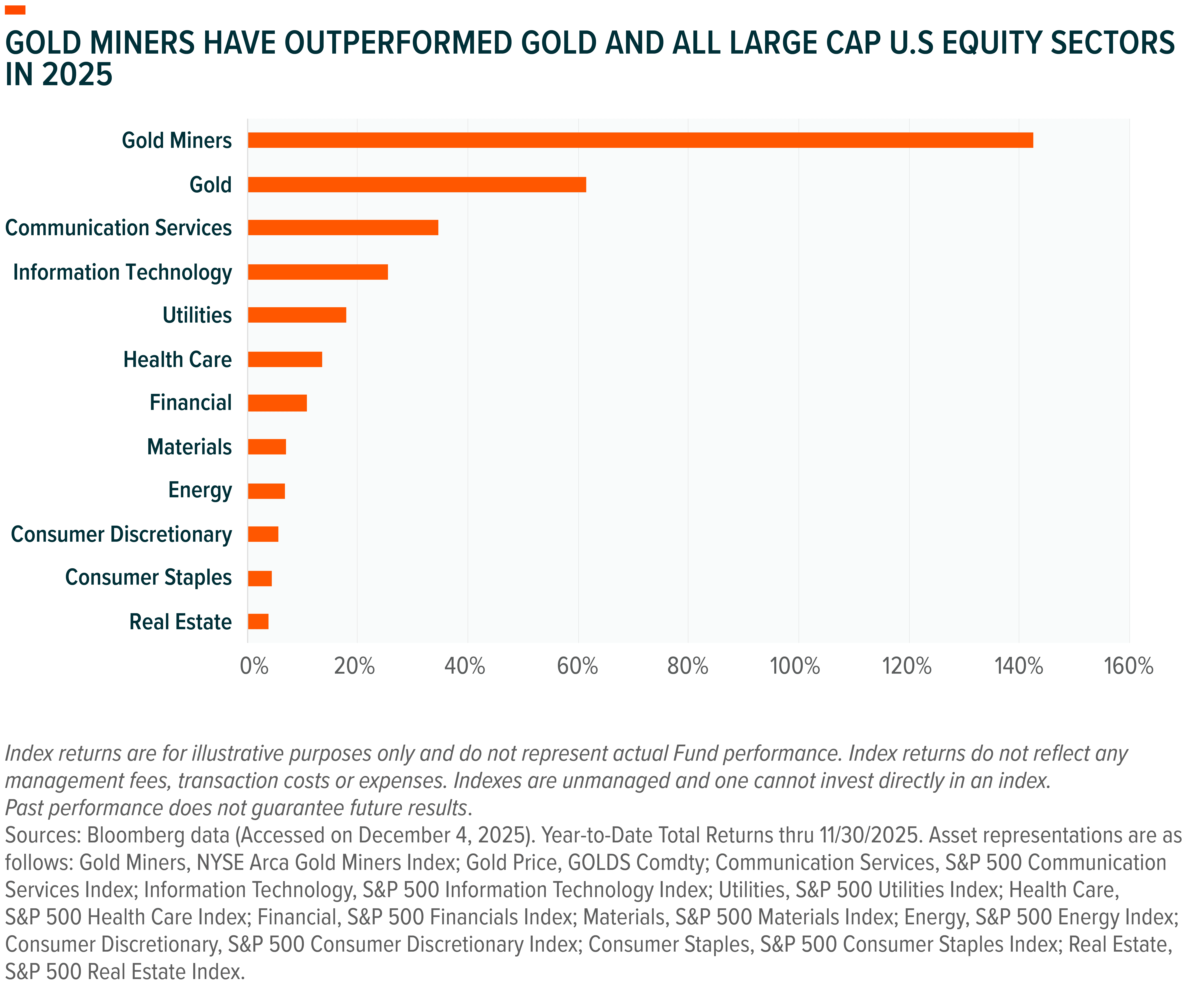

This relative value proposition has been evident in recent years, as the historic advance in gold prices has led gold mining margins to expand to historic levels. This broadening profitability has led gold miners to significantly outpace gold’s price performance in 2025, with gold miners returning ~143% year-to-date through the end of November versus gold’s price performance of ~62%.16 Despite the strong advance, gold miners remain relatively under owned relative to gold ETFs, with mining equities representing the smallest share of global stocks since 1900.17 At the same time, flows to gold trust ETFs, which represent interests in physical gold assets, grew for five consecutive months in 2025, putting on display investor interest in gold that culminated in nearly $503 billion in net assets.18

Historic improvements in profitability further underscore the health of the gold mining landscape. While gold breached its all-time high price at least 50 times in 2025,19 operating margins on constituents of the NYSE Arca Gold Miners Index (GDM) have more than tripled from 10.19% in Q2 2023 to 35.33% at the end of Q3 2025. Should gold prices remain structurally elevated, these margins could sharply boost company cash returns, shifting balance sheets into net cash positions and setting miners up to potentially boost share buybacks and shareholder distributions in 2026.20 We believe these fundamental factors further substantiate the value proposition of gold miners, with capital expenditure opportunities and mergers and acquisitions representing other potential catalysts for share price appreciation.

AUAU: The Case for Gold Miners

The Global X Gold Miners ETF (AUAU) is a passive index-based ETF that invests in a broad range of gold mining companies. This includes common stocks, preferred securities with equity-like characteristics such as those of common stocks, American Depositary Receipts (ADRs), and Global Depositary Receipts (GDRs) of companies listed on select global exchanges that are involved in the gold or silver mining industry. Such constituents are then weighted according to their float-adjusted market capitalization, subject to caps based on their categorization as large or small constituents.

In addition to the aforementioned factors, we believe gold miners remain distinct from physical gold trusts due to the following characteristics:

- Price Leverage: Rising gold profits can boost profits and cash flows for gold miners, offering leveraged exposure to the underlying commodity.21

- Operating Efficiency: Gold miners can realize wider margins on higher gold prices as operating costs remain steady, allowing them to achieve operational efficiencies, potentially boosting growth and equity valuations.

- Potential Distributions: Growing cash flows may raise cash dividends and share repurchases, thereby benefiting shareholders.

While performance can vary, we believe the evidence shows that gold mining equities has the potential to outperform gold prices over strong bull cycles, as revenue growth may significantly outpace production costs. Such results are evidenced by performance year-to-date in 2025, as well as historical periods such as January 2000 through 2008 and again from 2008 through 2012, although we note periods of drawdowns can also lead gold miner equities to underperform gold.22 Gold miners have also outperformed every major sector in the S&P 500 in 2025, as mining fundamentals continued to leverage elevated gold prices.

Conclusion: Cyclical Tailwinds May Fuel the Next Phase of Growth for Gold Miners

Gold’s meteoric price advance over the last couple years has been largely symptomatic of positive currency trends and persistent macroeconomic uncertainty. However, with a variety of trade and geopolitical risks still unresolved heading into 2026 a continued advance in gold prices remains a distinct possibility. Gold prices have continued to advance despite the current period of economic expansion, suggesting that gold’s price advance remain primarily driven by factors outside of market risk hedging. Should inflation accelerate, or a downturn in the current economic cycle take place, gold could very well move higher. Given the panoply of structural and cyclical factors at play, we think the trajectory for gold prices remains upward, barring a major shift to the fundamental narrative, providing a constructive environment for the mining equities in the Global X Gold Miners ETF (AUAU).

Related ETFs

AUAU – Global X Gold Miners ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.