Executive orders aimed at revitalizing the U.S. nuclear energy complex kicked off a surprise rally in the nuclear sector in Q2, led by nuclear reactor manufacturers, as these actions targeted the regulatory burdens that have weighed on grid expansions for decades. We believe these policy actions could set the stage for sustained growth in the U.S. nuclear industry, potentially accelerating development in the West, which has lagged overseas rivals like Russia and China. We think the momentum is just beginning, and the recent entrance of financial backers into the sector only underscores our bullish outlook. Although we acknowledge the road ahead is winding, we believe this sector carries much potential in the decades to come.

Key Takeaways

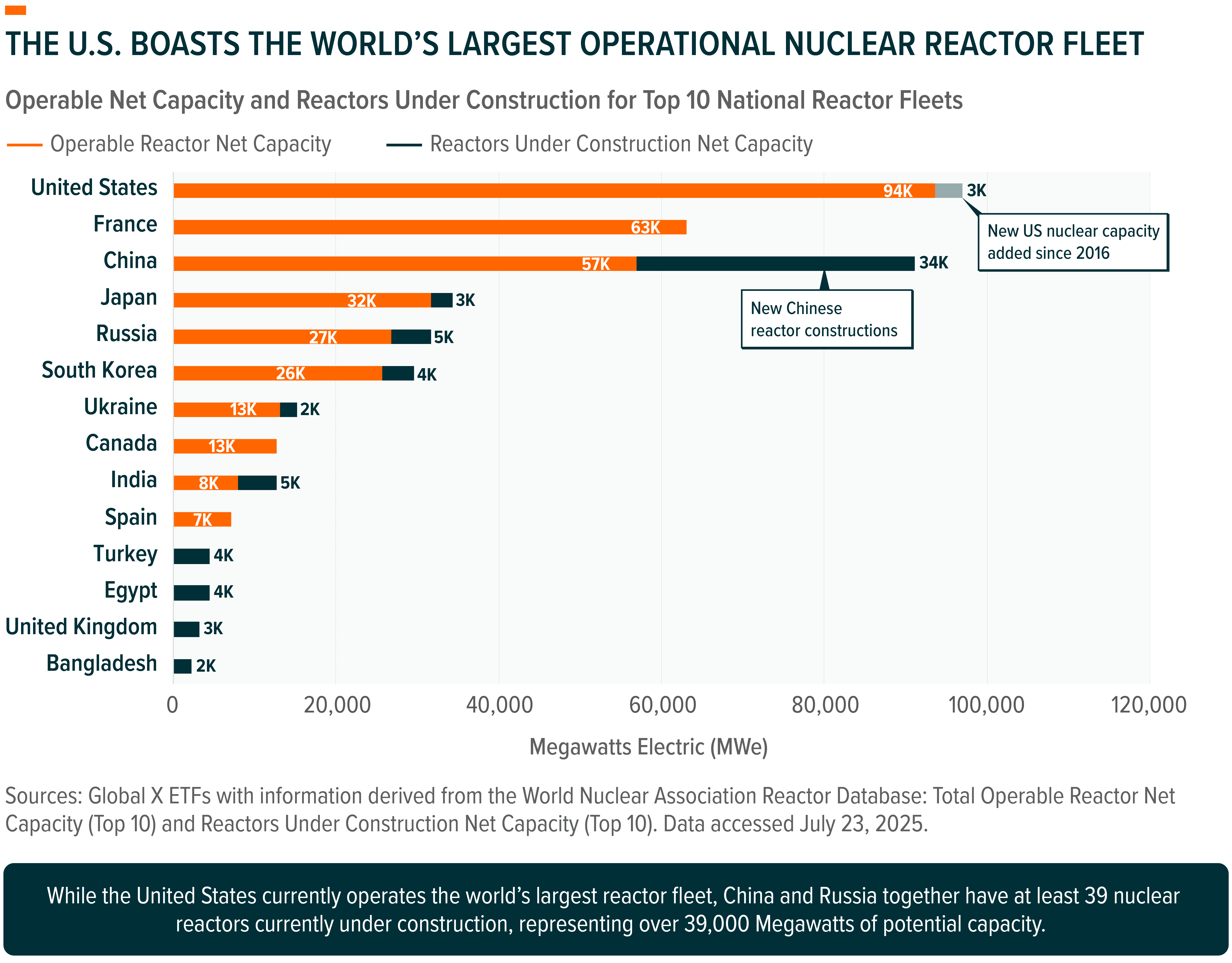

- Despite having the world’s largest fleet of operational nuclear plants, the United States has fallen woefully behind foreign rivals in reactor constructions, with China and Russia dominating construction pipelines.

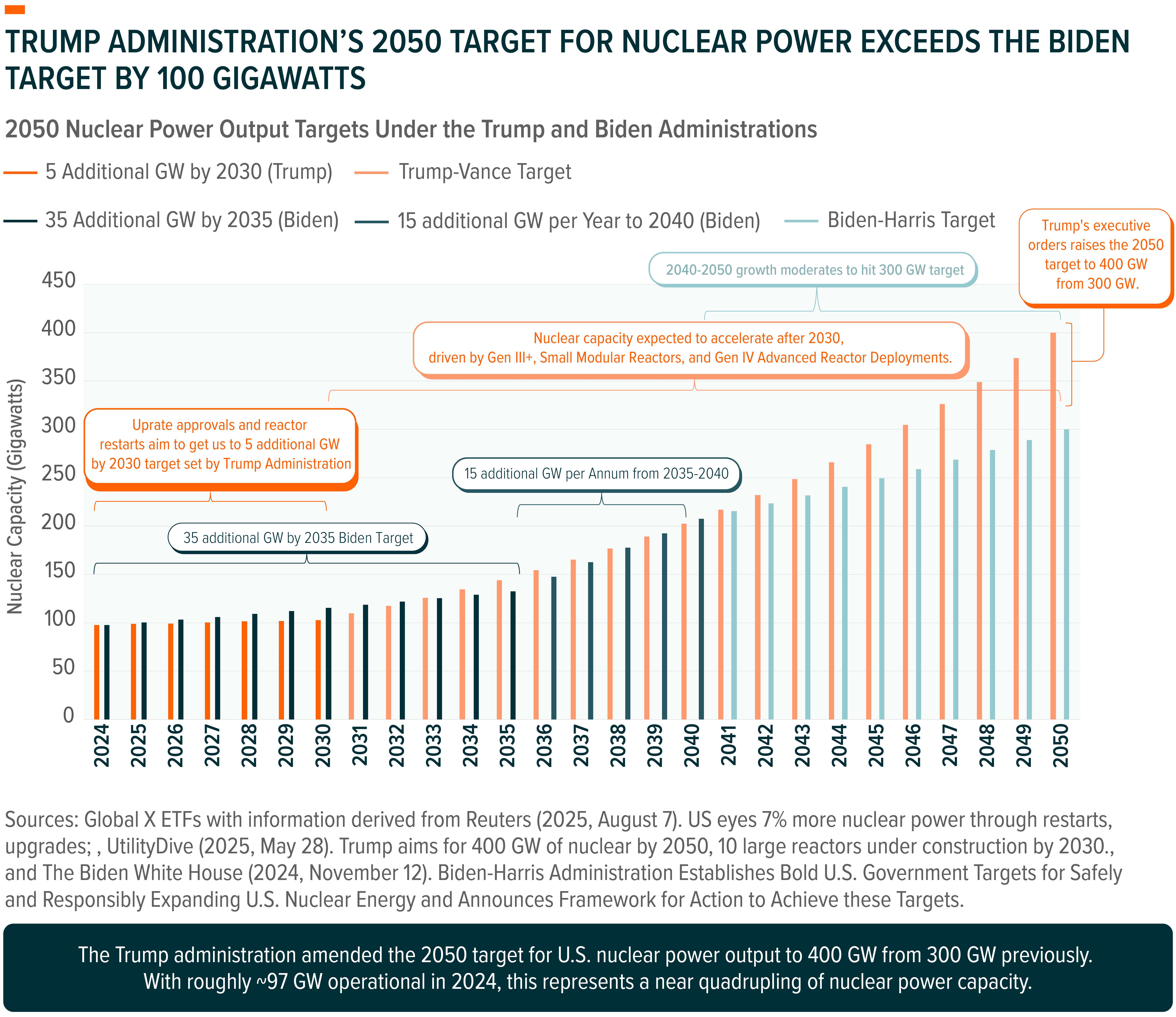

- Recent policy actions aiming to quadruple U.S. nuclear power capacity by 2050 may represent the most consequential nuclear legislation of our time, potentially leading to a sea-change for the U.S. nuclear complex1.

- We believe momentum will continue, as policy support, private sector investment, and popular opinion align in favor of nuclear power as a preferred tool for combating global energy insecurity.

A New Cold War for Power

Energy security is likely to be a vital concern for the 21st century. Global power consumption is expected to surge 4% annually through 2027, rising as much as 50%, or 13,300 TWh of electricity by 20402. Developing markets are expected to contribute the majority of that growth, as rapidly industrializing countries expand their infrastructure to meet rising consumption from an emerging middle class. At the same time, the West is not expected to stand idle, as current growth projections for electricity consumption within the United States calls for another California worth of power demand over the next three years3, contrasting starkly with the 0.1% annual growth rate we saw from 2005-20204.

We believe that this global growth will be underpinned by rapid industrialization, electrification, and the budding AI revolution, for which nuclear energy will be a fundamental necessity. 24/7 industries like hyperscale data centers require a substantial ramp-up in baseload output, given their need for continuous, uninterrupted operations; we think nuclear power may be optimally suited for this task.

Pit rising power needs against a U.S. nuclear power grid that has deployed nary two reactors over the past twenty years, and it’s easy to spot the glaring disparity between the U.S. and its overseas rivals, with China alone constructing 33 reactors over that same timeframe5. While the U.S. and Europe continue to maintain the world’s largest fleets of operational nuclear reactors, it’s clear that without substantial investment, Western nations run the risk of falling behind. Put another way, we find it difficult to envision an AI-revolution without the corresponding ramp-up in power output to support it. We think this necessitates substantial policy support.

U.S. Administration Jump Starts the Nuclear Industrial Base Via Executive Orders

On May 23rd, the U.S. Federal government announced four executive orders with the stated goals of “re-establishing the U.S. as the global leader in nuclear energy” and expanding American nuclear energy capacity to 400 Gigawatts (GW) by 2050 (from under 100 GW today). The executive orders effectively quadruple the U.S. nuclear output capacity target while addressing the regulatory burdens that have long constrained industry growth, cutting down approval procedures while codifying support for domestic nuclear supply chains and reactor deployments6.

Taken together, we believe these orders potentially amount to the most consequential policy actions enacted on behalf of the nuclear industry in the 21st century, representing a pivotal milestone for advancing U.S. nuclear policy. The orders have been dissected and broken down in the following sections.

Reforming the U.S.’s Nuclear Regulatory Commission (NRC)

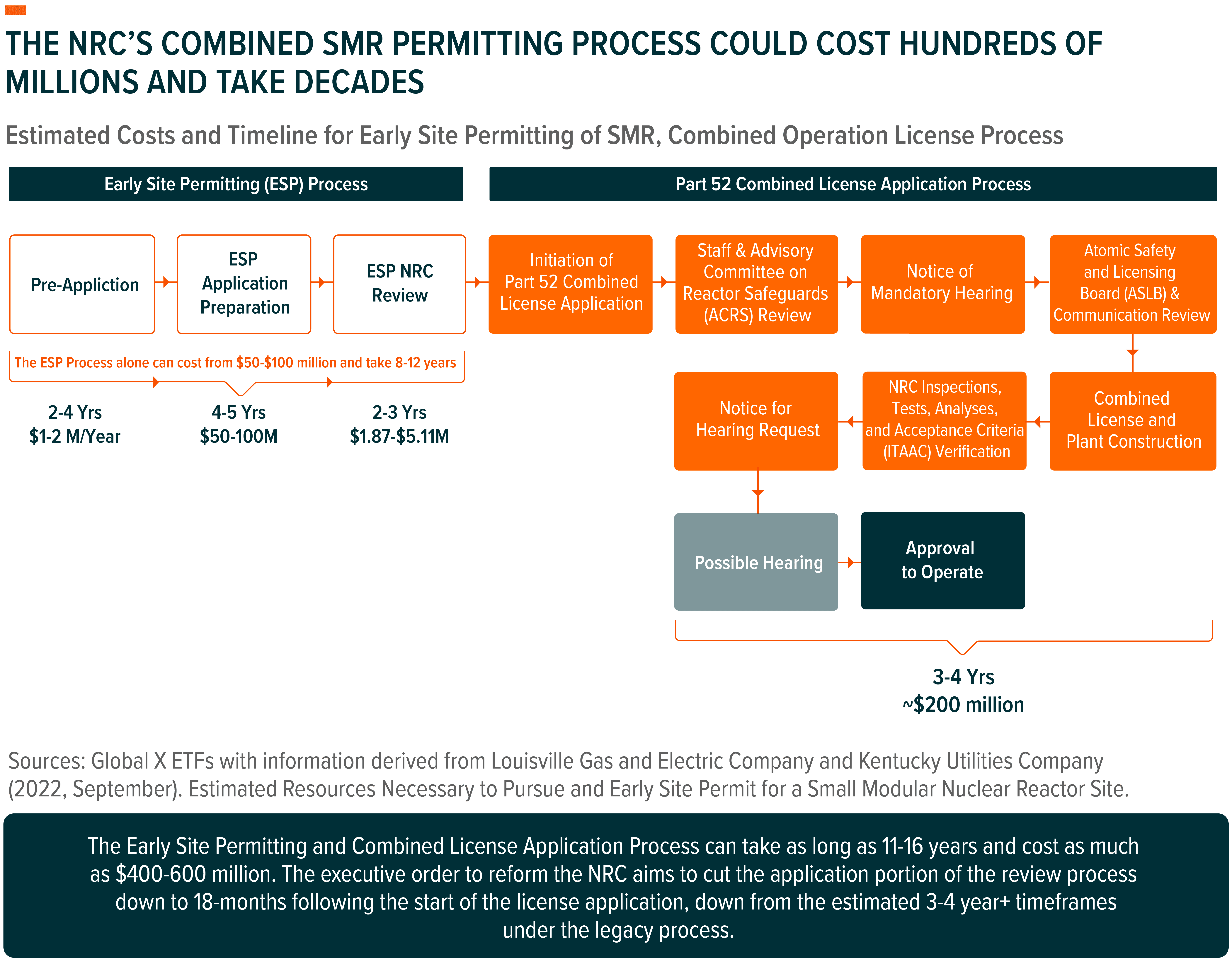

In its September 2024 presentation on reducing cost and times for licensing SMR (small modular reactor) projects, Microsoft cited that “Licensing is the single biggest bottleneck for getting new [nuclear] projects online,” noting project approval timelines that had taken decades and application costs that ranged from tens to hundreds of millions of dollars7. The 1st executive order titled “Reforming the Nuclear Regulatory Commission,” seeks to address this very concern.

Based on the legacy review process cited in a September 2022 report published by LG&E and KU, review timelines for SMRs ranged from 8-12 years from the point of pre-application to the NRC’s final approval of operating license, while total costs could range from as much as $400 million to $600 million (in the case of the Tennessee Valley Authority and Duke Energy) to pursue all required NRC licenses8.

We believe the most consequential aspects of the first order, which directs the reform of the NRC, were the explicit limitation in licensing costs and mandated reduction in approval timelines9. This includes the setting of 1) an 18-month deadline for rendering a final decision on applications to construct and operate a new reactor, 2) a 12-month deadline for rendering a final decision on applications to continue operating an existing reactor, as well as 3) fixed caps on the NRC’s recovery of hourly fees. In theory, this order could shave years off review timelines, potentially saving the nuclear industry hundreds of millions of dollars in regulatory costs and substantially shifting the economics for new nuclear builds and restarts.

Reforming Nuclear Reactor Testing at the Department of Energy (DOE)

Onerous regulations imposed by the NRC may have impeded U.S. nuclear reactor deployments for decades, resulting in the approval and construction of only three new nuclear plants over the past 25 years, and even leading a consortium of states and nuclear startups to file suit against the NRC10. Despite having the world’s largest reactor fleet, the United States has been slowly ceding nuclear leadership to overseas competitors, where the regulatory environment has been more cooperative.

The second executive order cuts at the heart of the U.S. nuclear research & development effort, aiming to reform testing requirements, and specifies several reforms, including: 1) expediting the review, approval, and deployment of qualifying advanced test reactors at DOE owned or controlled facilities within 2-years of a completed application, 2) expediting or eliminating environmental reviews and creating categorical exclusions as appropriate and relying on supplemental analyses when constructing on existing reactors sites. Collectively, these orders could cut down on the time hurdles that have delayed prototype constructions.

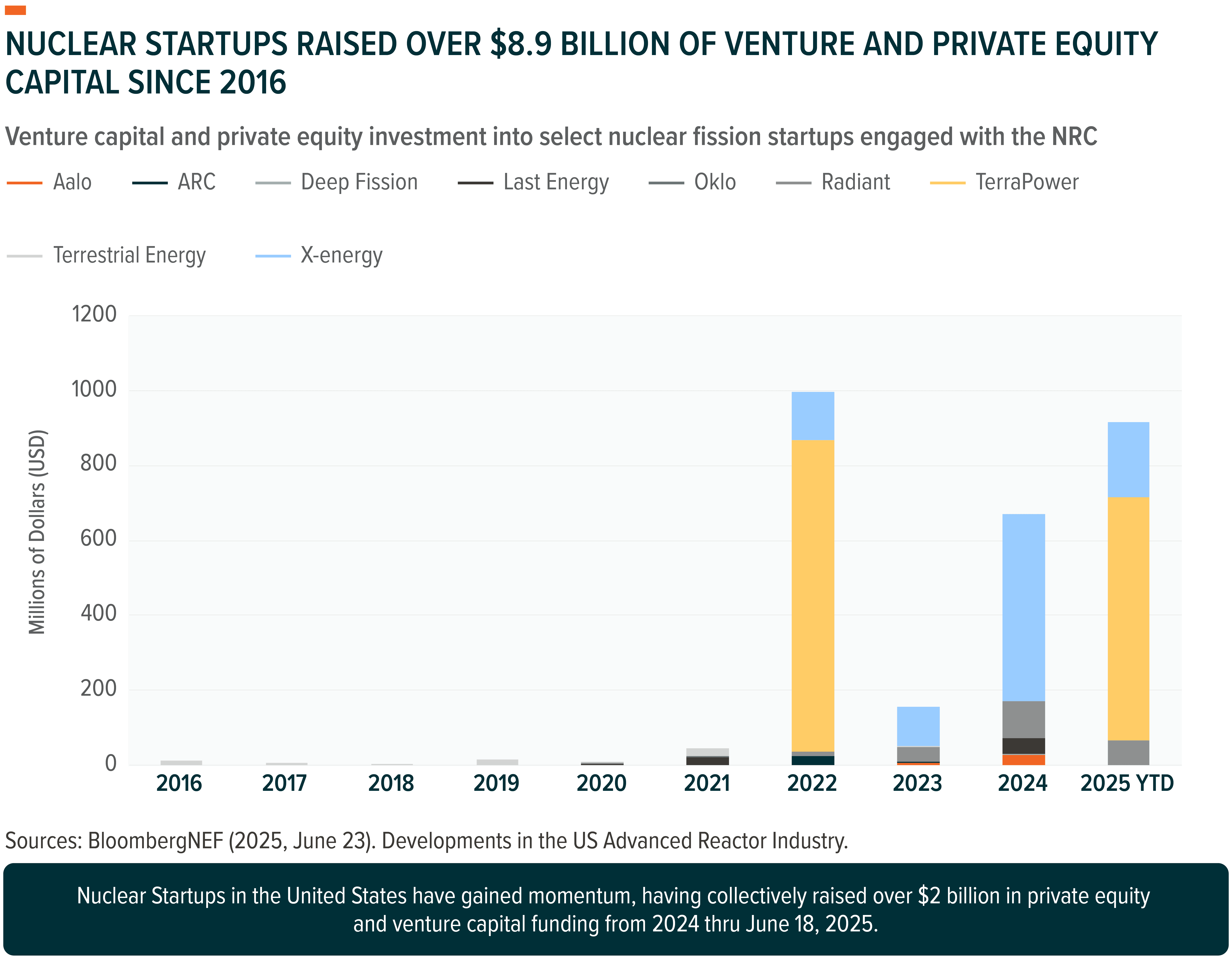

In addition to the efficiency mandates cited above, this order establishes a goal of achieving criticality (a continuous self-sustaining fissioning reaction) across three new reactor builds by Independence Day 2026. It’s already represented a potential contributor to fast-tracking R&D efforts within the United States, with the DOE announcing its selection of 11 advanced reactor projects for the Nuclear Reactor Pilot Program on August 13th. Combined with the over $8.9 billion in venture and private equity capital raised since 2016, this order potentially reflects strong momentum among advanced nuclear reactor developers within the United States11.

Reinvigorating the Nuclear Industrial Base

The third order, which seeks to reinvigorate the nuclear industrial base, targets the domestic supply chain for nuclear fuel. Among the most critical portions of this order include a directive to develop a plan for expanding domestic uranium conversion and enrichment capacity to levels sufficient to meet projected civil and defense needs for low enriched uranium (LEU), high enriched uranium (HEU), and high-assay low enriched uranium (HALEU).

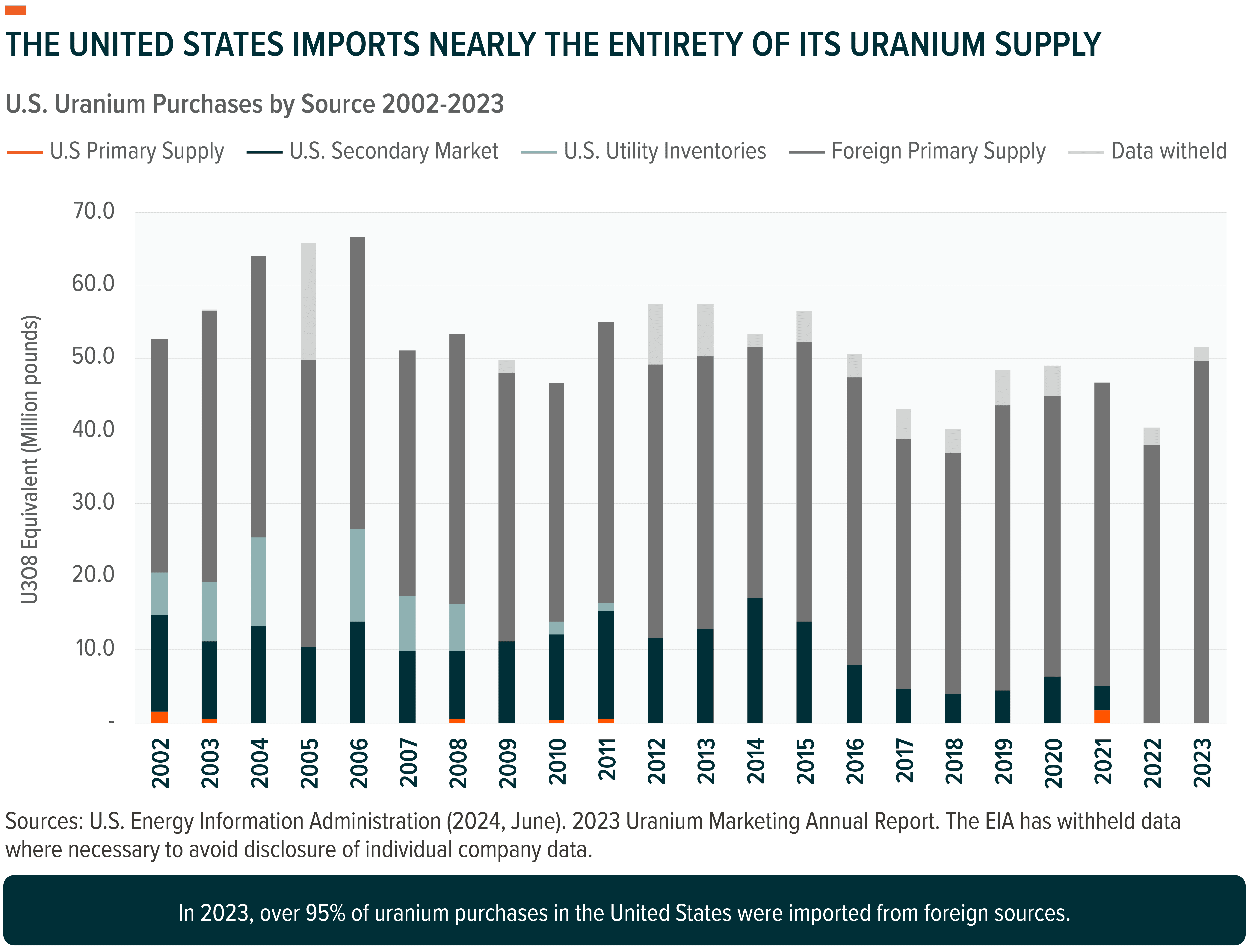

The third order opens government stocks of plutonium and excess uranium up for use by qualified pilot program reactors, alleviating near-term concerns for prototype reactor trials and supporting the administration’s order to reform nuclear reactor testing. Given the order’s emphasis on uranium supply chains, we think firms with significant exposure to the U.S. nuclear fuel cycle stand to benefit most. As of August 2025, the existing U.S. supply chain for nuclear fuel remains inadequate for meeting domestic reactor demand; while 2024 domestic uranium production rose to its highest level in 6-years of ~677 thousand pounds12, it amounted to barely 1.3% of the total 51.6 million pounds of uranium purchased by domestic utilities just one year prior13.

Further provisions in the order were made to accelerate the pace of nuclear deployments by prioritizing the work needed to facilitate 5 GW of power uprates at existing nuclear reactors. We believe this represents the first step in a process that will gradually see new reactors begin to hit the market in the 2030’s, with the long-term goal of having 10 new large reactors under construction by 2030.

Deploying Advanced Nuclear Reactor Technologies for National Security

Piggybacking off the uranium focus of the previous order, the situation is more dire for specialized enriched nuclear fuels like HALEU, which are critical to the deployment of advanced nuclear reactors, like SMRs. DOE projections call for as much as 50 metric tonnes of HALEU annually to meet nuclear demand in the 2030s14. However, U.S. private industry’s ability to meet this demand was forecast in 2023 to be just six metric tonnes per year by the late-2020s15. This issue is further compounded by foreign competition for global HALEU supplies, as overseas rivals vie to develop their own native nuclear technologies.

The fourth executive order directs the Secretary of Energy to release not less than 20 metric tons of HALEU to support any private sector project authorized to operate at DOE facilities with the aim of developing power infrastructure. The measure addresses the HALEU shortage that had been cited by reactor developers as a critical barrier to scaling SMR technology16, making government supplies available for private-sector use. It also instructs DOE to implement plans for a robust domestic supply chain to secure a reliable long-term supply of enriched uranium necessary for the sustained deployment of advanced reactors.

This order further ties the U.S. nuclear expansion to energy security and national defense, mandating the deployment of a nuclear reactor at a domestic military installation no later than September 30, 2028. It directs the Secretary of Energy to begin designating AI data centers tied to DOE facilities as critical defense assets, while classifying the electrical infrastructure supporting those data centers as “defense critical electric infrastructure.” Together, these measures underscore the national security element of this expansion17.

Conclusion: We Believe The Stars are Aligning for Nuclear Power

After decades of subdued growth, U.S. nuclear power appears to be at an inflection point, propelled by the confluence of public, private, and popular support. Public sentiment has shifted meaningfully, with a recent Gallup Poll showing 61% of Americans now support nuclear energy, a level near record highs18. At the same time, the current administration has built on the initiatives of its predecessors, doubling down its support for the industry via executive orders. With private capital flowing into the sector and the proliferation of power-hungry data centers heightening concerns over energy security, the conditions now seem aligned for a long-awaited resurgence in this once-beleaguered sector.

Related ETFs

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.