Global X Research Team

Global X Research TeamFor the period September 30, 2022 to December 31, 2022 (the “Period”), the Global X Emerging Markets Bond ETF (the “Fund”), sub-advised by Mirae Asset Global Investments (USA) LLC, posted a return of 8.23% (including distributions paid to unitholders). The JP Morgan EMBI Global Core Index (the “Index” or “Benchmark”), in comparison, returned 8.40% during the same period.

The performance data quoted represents past performance and does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance quoted. For performance data current to the most recent month or quarter-end, please click here. Total expense ratio: 0.39%.

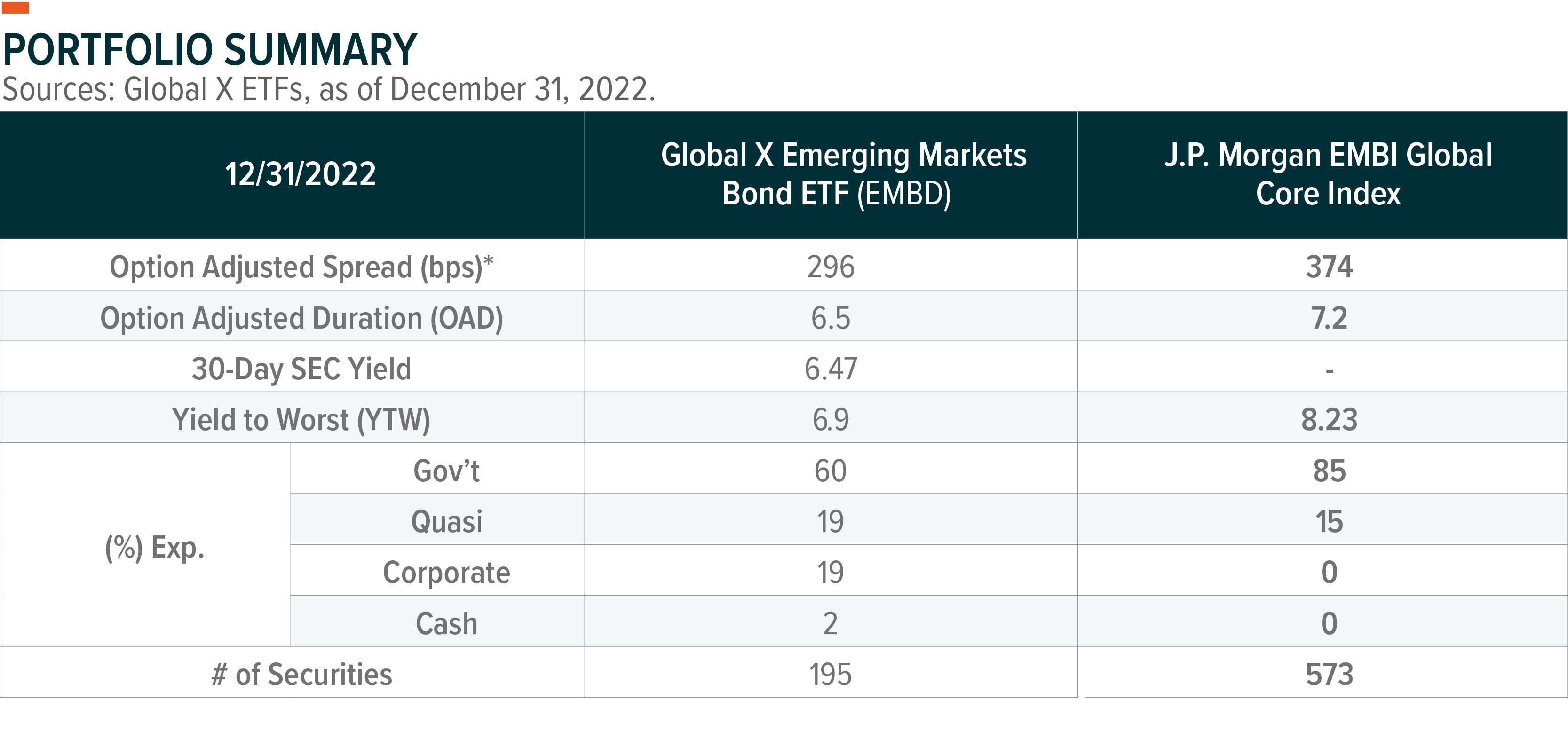

The Index tracks liquid, US dollar emerging market (EM) fixed- and floating-rate debt instruments issued by sovereign and quasi-sovereign entities.

General Market Review

In its last scheduled meeting of the year, the US Federal Reserve (Fed) raised the federal funds rate target range by 50 basis points (bps) to 4.25-4.50% and maintained its hawkish policy stance as Federal Open Market Committee (FOMC) members projected the policy rate to continue to climb in 2023 and remain at higher levels for longer. But that did not reverse the improving sentiment towards risk-assets, which started in early Q4 2022. Rather than relying on the Fed’s hawkish guidance, investors found comfort in softer-than-expected US consumer price index (CPI) data and indications that the pace of policy tightening may slow and that inflation had peaked, creating a market narrative of “peaked central bank hawkishness.” Consequently, easing financial conditions, supported by a declining US dollar, boosted risk-asset sentiment even as other macro uncertainties continued to linger.

Emerging market assets benefited from the turnaround in risk-asset sentiment as concerns over a recession in major economies and risks of continued monetary tightening abated. However, the major catalyst for boosting emerging market asset sentiment came from the Chinese government’s easing of the zero-COVID policy. The Chinese government dismantled COVID-related restrictions much quicker than expected and eased its policy stance on the property market to support a pro-growth agenda for 2023. Consequently, industrial metal prices rallied during the Period as investors upgraded China’s growth outlook for 2023. Improving growth outlooks for China and emerging markets, amid slowing growth in developed markets on the back of lagged effects of policy hikes, created bullish market conditions for EM assets, which was reinforced by a decline in the US dollar during the Period.

Based on the JPM EMBI Global Diversified Index, Argentina (37.62%), Kenya (21.29%), Egypt (19.88%), Nigeria (17.21%) and South Africa (9.43%) outperformed the broader EM sovereign market. Egypt received final approval from the International Monetary Fund (IMF) Executive Board for a 46-month, $3 billion Extended Fund Facility (EFF) package after the Central Bank of Egypt agreed to a key bailout condition of moving to a “durably flexible exchange rate regime” and subsequently devalued the currency in late-October.1 Effectively, Egypt was given immediate access to about $347 million to help support the nation’s balance of payments and its general budget. In South Africa, political risks subsided from President Cyril Ramaphosa’s “farmgate” corruption scandal after Ramaphosa consolidated support from allies by winning re-election as the leader of the ruling African National Congress (ANC) party.

On the contrary, Zambia (-6.75%), Ghana (-5.83%) and Brazil (3.61%) were notable laggards during the Period. In Ghana, the government announced a voluntary domestic debt-exchange program for its local bonds, asking holders to take losses to interest but with no haircut to the principal value. While debt restructuring parameters were pending an agreement with domestic creditors, Ghana suspended interest payments on US$13 billion of Eurobonds, as well as commercial loans and most bilateral obligations, taking bondholders by surprise as participants were expecting the government to request a debt-service suspension through a consent solicitation rather than a unilateral default.2 Meanwhile, Brazil underperformed as policy uncertainty clouded the outlook after Luiz Inacio Lula da Silva won the presidential elections, promising to abolish a constitutional spending cap to allow the government to spend more on social projects and infrastructure. Separately, major oil exporters such as Saudi Arabia (3.37%) and Qatar (4.02%) underperformed as the Middle East region was impacted by weaker energy prices.

Portfolio Review

During the Period, the Fund underperformed the Index by 17 bps. The Fund’s lower duration relative to the Index and security selections positively contributed to performance, adding 26 bps and 20 bps, respectively. However, the Fund’s country selections detracted 63 bps from performance.

The Fund’s performance was mainly contributed to by its exposure to China (34 bps), Morocco (22 bps), and Colombia (13 bps). China’s shift towards accommodative economic policies, including some measures aimed at easing pressure on the real estate sector, and subsequent optimism regarding the economy’s re-opening positively contributed to the Fund’s country and security selections. The Fund’s overweight exposure to Colombia became beneficial as budget estimates were undershot. In a statement, Finance Minister Jose Antonio Ocampo reiterated the government’s commitment to prudent macro policy, which included continuing to meet the fiscal rule, eschewing capital controls, moving towards export diversification, continued review of new oil exploration contracts and other actions to ensure the improvement of external balances. Meanwhile, Peru (-16 bps), Kazakhstan (-11 bps) and Nigeria (-8 bps) were major detractors during the Period. Political turmoil increased in Peru as Congress expedited and passed Pedro Castillo’s impeachment vote on the grounds of “permanent moral incapacity” after Castillo attempted to dissolve Congress. While then-Vice President Dina Boluarte was sworn in to the executive title, fatal protests continued in response to the impeachment. Effectively, Boluarte proposed a constitutional reform to expedite the general elections from 2026 to 2024 in an attempt to cater to growing pressures from the population and allow time for political reforms that could limit the stalemate between Congress and the executive branch. Exposure to Nigeria further weighed on performance as the Fund held an underweight position amid a rally on an announcement that the government plans to extend the tenors of its outstanding debts and explore other appropriate debt liability management options, such as bond buybacks and bond exchanges, in an attempt to save money on debt servicing costs.

Outlook and Strategy

As we head into Q1 2023, we are cautiously optimistic about the outlook for the EM credit market over the near-term, despite overhanging macroeconomic uncertainties. We believe that much of the interest rate hikes behind us and that the continued moderation of inflation dynamics supports the case for further adjustments to the Fed’s tightening policy as growth momentum continues to slow. Until growth risk becomes the dominant investment theme in market outlooks, we expect investors to find credit assets, including emerging market credits, as an attractive investment option to pursue income.

Secondly, a welcomed turnaround in major policy direction by the Chinese government not only alleviated global growth concerns, but also boosted the case for cyclical assets, such as emerging markets, in the near-term. Whereas regulatory reform and strict enforcement of the zero-COVID policy were the main goals of the Chinese government for much of 2022, in 2023 we are seeing the focus shift back towards economic growth, which includes a certain degree of easing on the property and tech sectors. As growth momentum recovers in China and emerging markets, the growth slowdown in western economies on the back of lagged impacts of higher interest rates could further support the case for emerging market assets even as overall growth momentum continues to trend lower in 2023.

With lower immediate global growth concerns on the back of China’s pro-growth policy agenda and resilient growth momentum in developed markets, we are much more likely to see a “higher for longer” interest rate in the US. For 2023, we expect central banks to keep interest rates at restrictive levels for longer, which makes central bank overtightening a major investment risk in the latter half of the year as growth momentum slows.

Emerging sovereign markets have experienced a notable upswing since October 2022, largely attributed to the narrative surrounding these markets reaching the apex of inflation in Q4 of 2022, enabling central banks to implement less stringent policies going forward. Inflation rates within emerging markets have since moderated, falling from the multi-decade high of 6.71% as of the end of September 2022 to a more subdued 4.76% as of the end of December 2022.3 The resilience and the lack of contagion risk, during the selloff in 2022 amid the most aggressive tightening cycle by the Fed since 1970s, revealed how mature the asset class has evolved and illustrated how EM economies have built stronger external buffers to safeguard against capital outflows. With the exception of several vulnerable EM sovereign issuers that lacked the ability to absorb external shocks, most EM economies weathered the interest rate shock and stronger US dollar pressure much better than most had expected. As inflation and monetary policy risks ease, we expect investors to find EM credits to be another source of higher income potential until growth risks and central bank overtightening risks materialize.

From a credit risk perspective, we prefer to maintain a portfolio tilt toward higher quality issuers over idiosyncratic and/or higher-beta exposures even though some distressed EM issuers have already priced in restructuring risks to a greater degree. With most of the interest rate hiking cycle behind us, we plan on using rate volatility to reduce the portfolio’s underweight duration exposure by taking profits on our floating-rate bonds and building positions on BBB issuers with solid external balance sheets. With China’s sooner-than-expected reopening and its new pro-growth agenda, commodity producing corporate issuers from the Latin American region appear to be attractive from a risk-reward perspective. So, we plan to add those exposures based on a bottom-up analysis. Though near-term positive momentum supports the case for investors to take on greater risks for high-yielding assets, we caution against taking unnecessary risks on fundamentally vulnerable EM issuers because the Fed appears to be quickly moving towards quantitative tightening as it attempts to withdraw liquidity from the system.

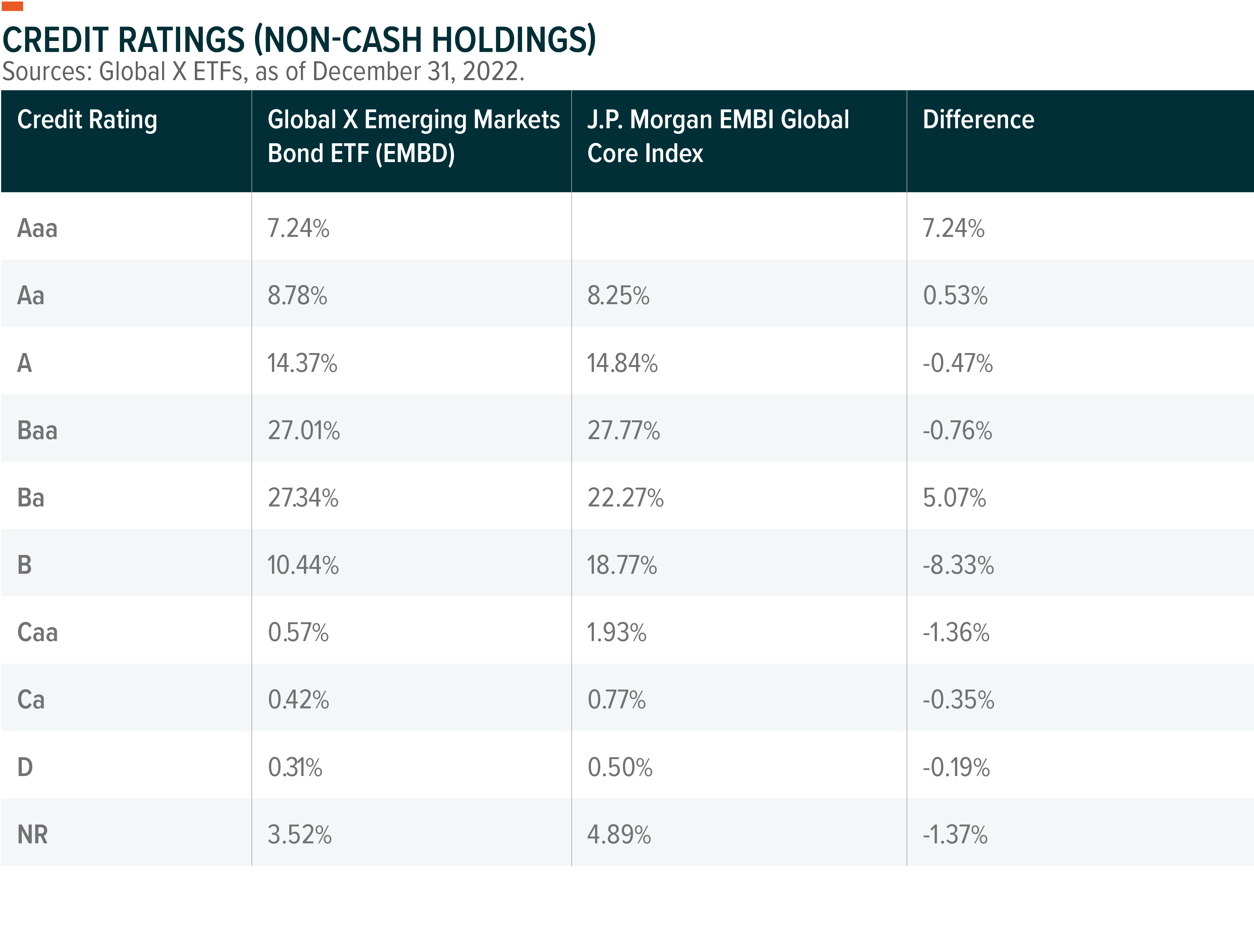

Credit Ratings noted are by Fitch, Moody’s, and Standard & Poor’s. Ratings are measured on a scale that generally ranges from Aaa (highest) to D (lowest). If more than one of these rating agencies rated the security, then an average of the ratings was taken to decide to security’s rating.

Related ETFs

EMBD – Global X Emerging Markets Bond ETF

Please click the fund name above for current fund holdings and important performance information. Holdings are subject to change.