Arelis Agosto

Arelis AgostoThe healthcare diagnostics market is undergoing a transformative shift. Driven by advancements in genomics and a growing arsenal of non-invasive testing methods, diagnostics are playing an increasingly critical role in detecting early signs of illnesses and improving patient care.

Genomic sequencing technology has revolutionized the healthcare industry, fundamentally transforming our understanding of biology and human health. More accessible price points for genomic profiling and ever-improving technologies have accelerated adoption of such technology and enabled a comprehensive study of the human genome.

This piece is part of a series that dives deeper into this year’s iteration of our flagship research piece, Charting Disruption.

Key Takeaways

- Aided by a growing toolkit of genomic technologies that are non-invasive and at increasingly accessible price points, the market opportunity for diagnostic tests to improve patient care appears vast.

- The healthcare industry has largely focused its efforts on developing improved diagnostic tests for cancer, but neurological disorders could present another large opportunity for companies in the space.

- As companion diagnostic tests play an increasingly important role in the success of investigational treatments and the widespread adoption of approved therapies, pharmaceutical and biotechnology firms continue to prioritize partnerships and acquisitions to strengthen diagnostic capabilities.

Oncology Sector Has Validated Diagnostic Promise

Aided by a growing toolkit of genomic technologies, the role of diagnostic tests has increased in importance and can improve patient care across their diagnostic and treatment journeys.

Using current standard of care, only about 25% of cancers are detected via screening.1 The remaining 75% are detected when the patient is symptomatic, and most likely in a later stage of cancer.2 Largely as a result, cancer accounts for 609,000 deaths a year in the United States, making it the second leading cause of death.3

New diagnostic tests, namely liquid biopsies, offer fast and accurate detection of cancer via non-invasive blood tests. These tests look for biomarkers in the patient’s blood – biological molecules that serve as medical signs for specific illnesses. Key applications include:

- Health Check: Routine test for presence of disease-specific biomarkers in asymptomatic individuals.

- Diagnostic Aid: Informs diagnosis in suspected cases, such as patients with underlying symptoms.

- Therapy Guidance: Helps identify if a patient has a specific biomarker that is targeted by a commercially available drug. It also helps predict response, and thus determines if the patient should receive the treatment. These tests are referred to as companion diagnostics (CDx).

- Intervention Outcome: Measures presence of the illness during treatments and helps determine patient response to treatment.

- Recurrence Monitoring: Measures presence of illness during remission to monitor any potential recurrence of the disease.

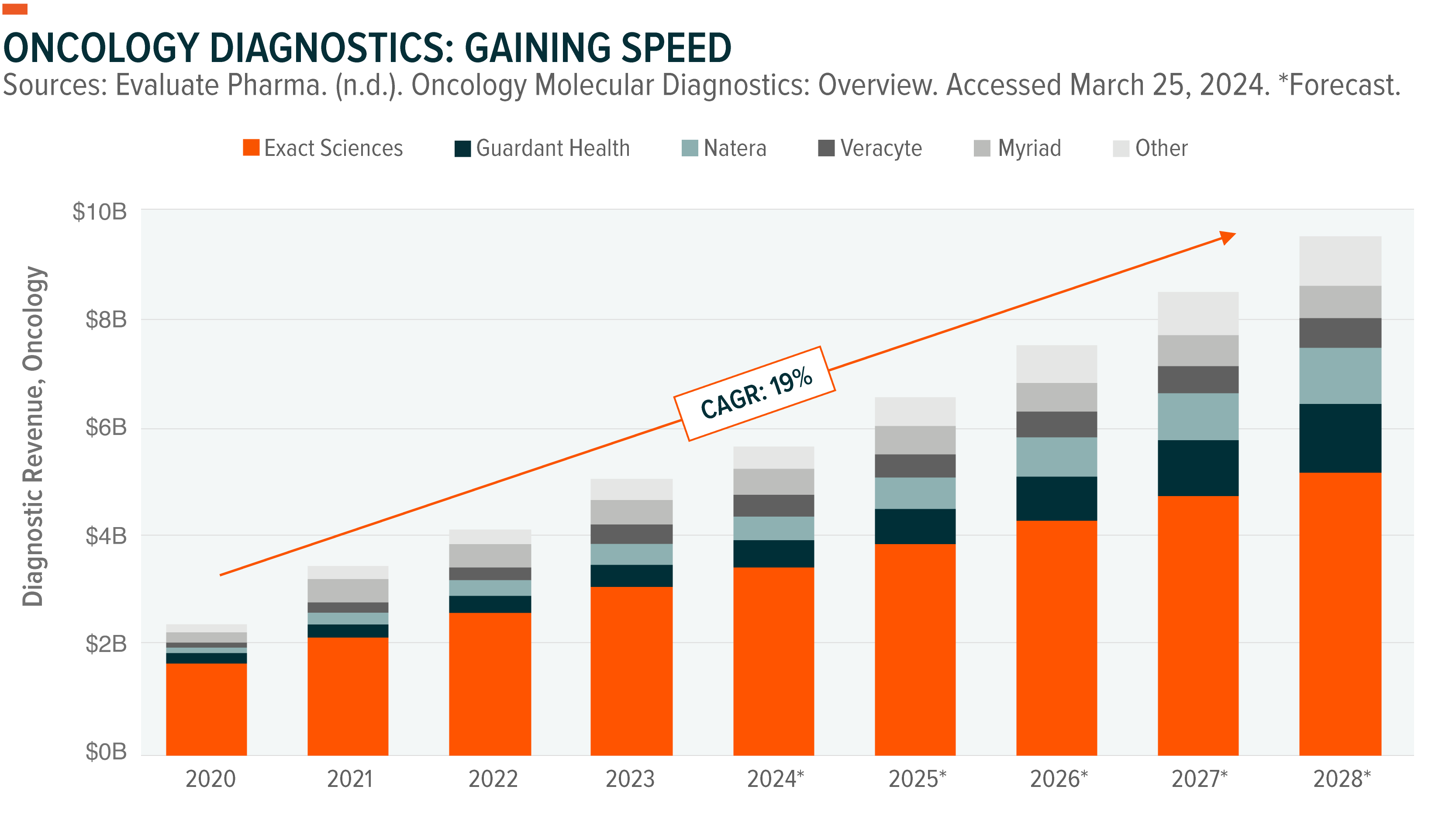

Understandably, the healthcare industry has largely focused its efforts on developing improved diagnostic tests for cancer. The oncology diagnostics industry achieved over $5 billion in revenue in 2023, though it represents a total $78 billion market opportunity.4,5 Through 2028, the industry is expected to grow at a 19% compound annual growth rate (CAGR).6

Neurological Disorders Present Highest Unmet Need

As the industry seeks to expand the repertoire of non-invasive tests, neurological disorders are a growing area of interest. Neurological illnesses are notoriously difficult to diagnose, though new tests offer a more accurate and cost-effective alternative to traditional methods.

Diagnosing Alzheimer’s traditionally relies on expensive PET scans or measuring biomarkers in spinal fluid, collected via a lumbar puncture. These methods are expensive, around $5,000 and $1,000, respectively.7 Capacity issues are also notable, with only about 2,000 PET centers in the United States.8 With current diagnostic standards, patients are diagnosed, on average, 2.8 years after symptom onset, and 75% of people living with the symptoms of Alzheimer’s are undiagnosed.9

New blood-based and plasma-based alternatives offer a more scalable, less invasive option with the goal of identifying Alzheimer’s presence even before a patient is symptomatic. These tests are also more cost effective, estimated to cost $400 per test, propelling an estimated Alzheimer’s diagnostics market of $8 billion.10,11

These efforts are expected to also play a pivotal role in the treatment of Alzheimer’s patients. The recent success in slowing cognitive and functional decline of Alzheimer’s has been largely concentrated in early-stage cases, as shown by the recent approval of Eisai’s Leqembi and the expected approval of Eli Lilly’s Donanemab in 2024.12 The Alzheimer’s treatment category is expected to grow to $11.5 billion by 2028 from $703 million in 2023.13

Accelerating Pharmaceutical and Diagnostic Conversion

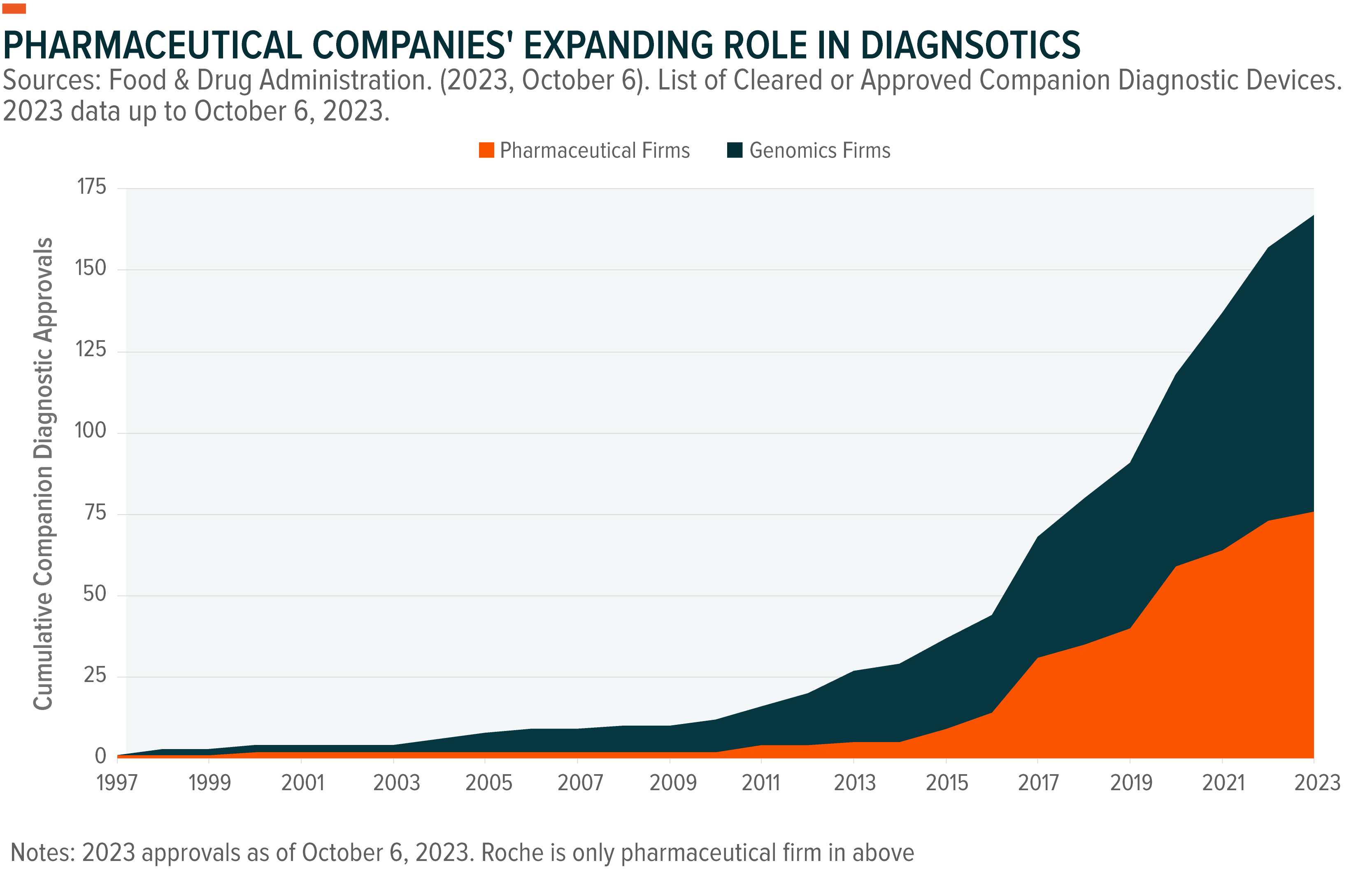

The relationship between therapeutic and diagnostic capabilities is becoming more important over time, as new, more complex treatments come to market. As with Alzheimer’s treatments, diagnostic capabilities can propel or hinder the adoption of life-changing treatments. Growing efforts from pharmaceutical firms to partner with or acquire diagnostics firms are expected to further refine diagnostic capabilities across nearly all disease categories.

A key area of increasing partnerships is diagnostic tests specifically made to help match patients to a specific therapy or drug. These are known as companion diagnostics (CDx), and they look for possible gene changes or biomarkers in the patient’s sample that commercially available drugs target. The tests can also shed light on potential side effects and measure how well the treatment works after administration.

CDx tests play an increasingly important role in the success of investigational treatments and the widespread adoption of approved therapies. As a result, pharmaceutical and biotechnology firms continue to prioritize partnerships and acquisitions to strengthen diagnostic capabilities. An estimated 46% of total CDx tests approved by the FDA are offered by pharmaceutical firms.14

Conclusion

Many patients suffer because early detection tests either don’t exist, are too expensive, or are too invasive. Advancements in genomics, however, are opening the door to a much broader array of tests that are accurate, inexpensive, and simple to implement. Such diagnostics could lead to earlier intervention and, hopefully, improved patient outcomes. The oncology market alone is massive given the prevalence of cancer in the broad population, and expansion into other areas such as neurology could present an even greater market opportunity for companies in the genomics and pharmaceutical industries.