Global X Research Team

Global X Research TeamOn February 26th, the Global X Guru™ Index ETF (GURU) underwent its quarterly rebalance. Explore the February 2016 Guru Report here.

- Between the most recent quarterly rebalances (November 25th to February 25th), Guru is down -12.95%, while the S&P 5001 is down -6.02%.

- Much of the underperformance is attributable to the continued struggles of major equity hedge funds, which are down almost -7% this year

- Guru’s February rebalance saw above-average turnover with 16 stocks leaving the fund and 21 new additions. The majority of companies leaving are shorter-term holdings that had generated negative returns.

- The select list of hedge funds from which Guru sources its high conviction ideas was updated, resulting in 28 new hedge funds being added to the list and 21 being removed.

- We believe the higher overall turnover in this rebalance is a positive for Guru as equity hedge funds look to find new ideas that will reverse their recent fortunes. In addition, Guru’s more aggressive tilt towards cyclical and sensitive sectors may set up the fund for stronger returns if the market returns to a more bullish environment.

Performance

In the Guru: 2015 Year in Review blog post, we discussed how Guru’s performance is often a magnification of the returns experienced by equity hedge funds because Guru is a long-only fund, while equity hedge funds can have short positions and therefore less market exposure. Unfortunately, the trend of poor returns from equity hedge funds in 2015 has largely continued as the HFRX Equity Hedge Index2 returned -6.93% from the November 2015 to February 2016 rebalances. Over the same period Guru was down -12.95% and the S&P 500 was down -6.02%3.

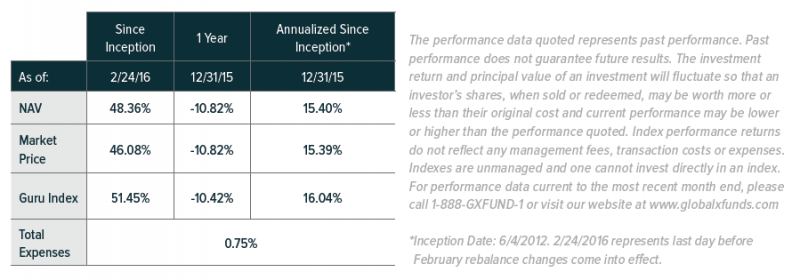

For GURU performance data current to the most recent month- and quarter-end, please click here.

An attribution analysis of Guru’s performance over this time demonstrates that 70% of the fund’s underperformance came from the selection effect, or the sector-agnostic returns from concentrated stock picks by major hedge funds. The high selection effect demonstrates that many hedge funds have been unsuccessful with their individual stock picking regardless of the sector. The allocation effect, or the fund’s over or underweight to different sectors, contributed to 30% of its underperformance. Most of the allocation effect is attributable to the more aggressive collective positioning of high conviction hedge fund picks, which has led to Guru underweighting sectors that tend to do better in selloffs, such as utilities, telecoms, and consumer staples.

Rebalance

Guru’s latest rebalance saw the removal of 16 of the fund’s 42 components and the addition of 21 new holdings. Guru tracks concentrated positions reported in 13f filings from a select list of hedge funds for which the 13f valuation is most valuable. The February rebalance typically exhibits higher than average turnover because not only are new 13fs released in February, but the select list of hedge funds tracked by Guru is also refreshed to ensure only large, low turnover hedge funds with concentrated positions are included in the select list. 28 hedge funds were added to the select list and 21 were removed, bringing the total number of hedge funds followed by Guru to 60.

The majority of the stocks leaving Guru during this rebalance have been shorter-term losers, as hedge funds cut their losses on companies that had not performed. The winners that were removed tended to be longer-term high-returners, as hedge funds took their gains in these positions.

| Number of Holdings Removed from Guru | Avg Return while in Guru | Avg Time in Guru | |

| Winners | 5 | 62.6% | 2.7 Years |

| Losers | 11 | -19.2% | 1.5 Years |

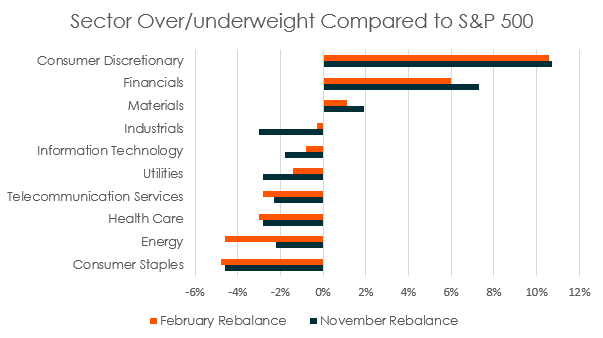

Despite the significant turnover in individual holdings, Guru’s sector over/under weights compared to the S&P 500 remained largely in-line with the previous rebalance. The fund continues to be heavily overweight towards consumer discretionary stocks and financials, while maintaining an underweight to consumer staples and health care. Guru increased the magnitude of its underweighting to energy stocks while becoming virtually neutral-weight on industrials.

Looking forward, we believe the selling of short term losers and higher overall turnover during this rebalance is a positive ‘spring cleaning’ for Guru, as equity hedge funds look to find new ideas that will reverse their recent fortunes. In addition, Guru’s more aggressive tilt towards cyclical and sensitive sectors may set up the fund for stronger returns if the market returns to a more bullish environment.