Rohan Reddy

Rohan ReddyEditor’s Note: RATE traded under the ticker IRHG from inception until November 14, 2022.

On July 6, 2022, we listed the Global X Interest Rate Hedge ETF (RATE) and the Global X Interest Rate Volatility & Inflation Hedge ETF (IRVH) on the New York Stock Exchange (NYSE). The Global X Interest Rate Hedge ETF (RATE) seeks to tactically hedge against sharply rising long-term U.S. interest rates while also benefitting during market stress when interest rate volatility rises. The Global X Interest Rate Volatility & Inflation Hedge ETF (IRVH), seeks to hedge relative interest rate movements arising from a steepening of the U.S. interest rate curve, and to benefit from periods of market stress when interest rate volatility increases, while also providing inflation-protected income. IRVH and RATE now bring Global X’s Options based ETF suite to 14 funds totaling over $9.6 billion in assets under management.1

Key Takeaways:

- In an effort to control inflationary pressures, central banks globally are resorting to hawkish monetary policies. The subsequent rise in interest rates is raising costs for companies globally and putting pressure on the broader markets.

- When developed central banks increase policy rates due to inflationary pressures, equity and debt markets historically underperform. Interest rate option strategies can be appealing in volatile market environments, as inflationary pressures permeate across the economy.

- RATE is designed to functionally act as if an investor owns a position in long-dated put options on long-term treasury bonds by utilizing payer swaptions. IRVH combines over-the-counter options on the interest rate markets with U.S. Inflation-Protected Treasuries Securities (TIPS) in an effort to hedge inflation and interest rate risk.

- RATE and IRVH can act as portfolio hedges in a low-cost manner: for discerning investors looking to diversify or hedge their portfolios against interest rate risk, RATE seeks to do so by actively managing interest rate risk in an exchange traded fund (ETF) vehicle. RATE is expected to benefit when long-term interest rates rise or when interest rate volatility is elevated and causes rates to spike. IRVH is designed to help investors benefit from an increase in inflation, as well as interest rate volatility, which may materialize through a steepening yield curve.

Investing in a Changing Rate Landscape

Rising interest rates are a key concern for many investors today, as central banks are reacting to persistently high inflation. In response to multi-decade high inflation prints, central banks are aggressively raising rates and rolling back bond buying programs from previous years. The Federal Reserve (Fed), for example, intends to raise rates through 2022 and 2023 through a combination of 25, 50 and recently 75 basis point (bps) hikes for the first time since 1994, and the futures curve is pricing in over 8 hikes of 25 bps by year end.2 This would put the implied Fed Funds policy rate at approximately 3.54% at the end of the year.3

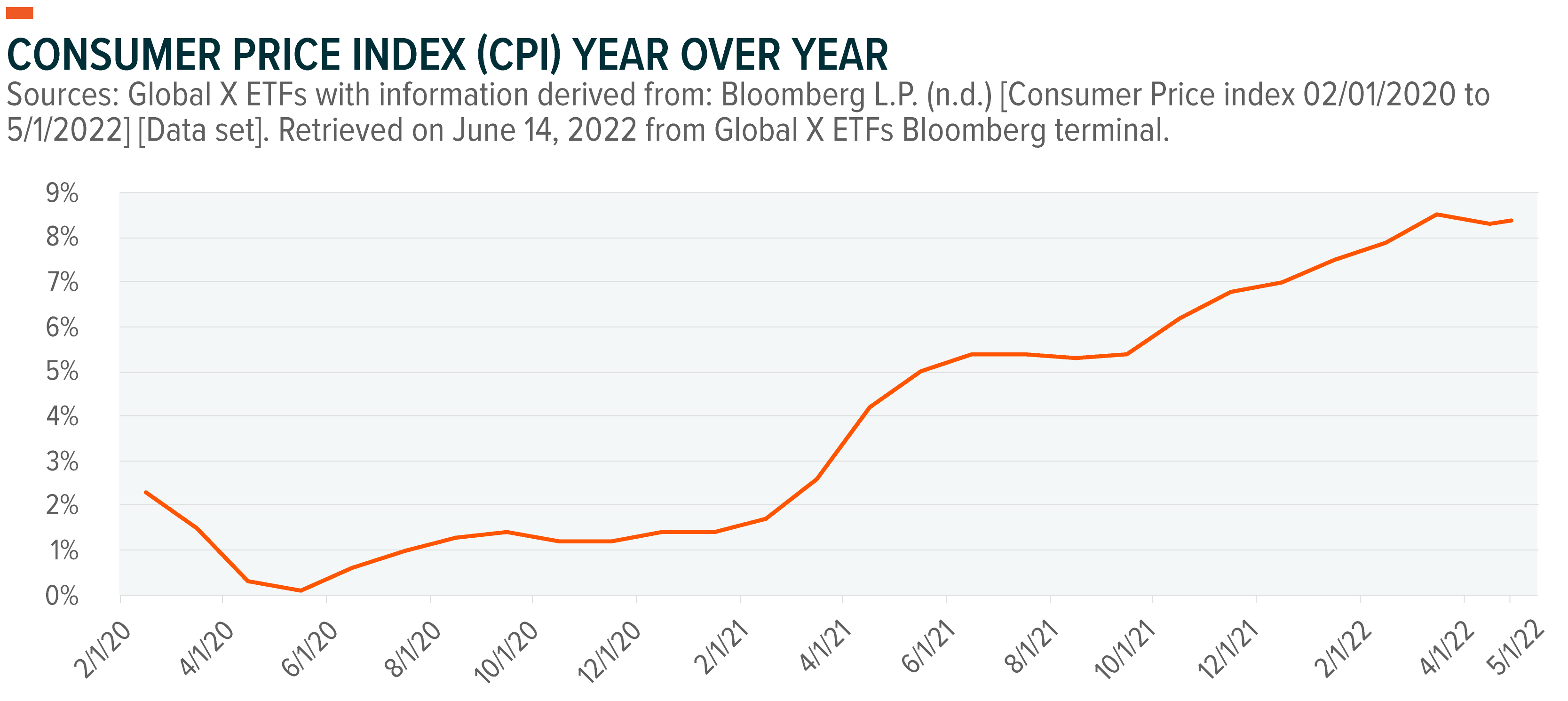

The Fed’s aggressive policy response is due to inflationary pressures spreading across the entire economy. The latest inflation print in May came in at 8.6% year-over-year (YoY), significantly higher than levels even just 12-18 months ago, as we can see in the graph below. These levels of elevated inflation are unlikely to dissipate due to multiple factors indicating late cycle activity, including a tight labor market, high energy prices, supply chain issues, and consumer strength.

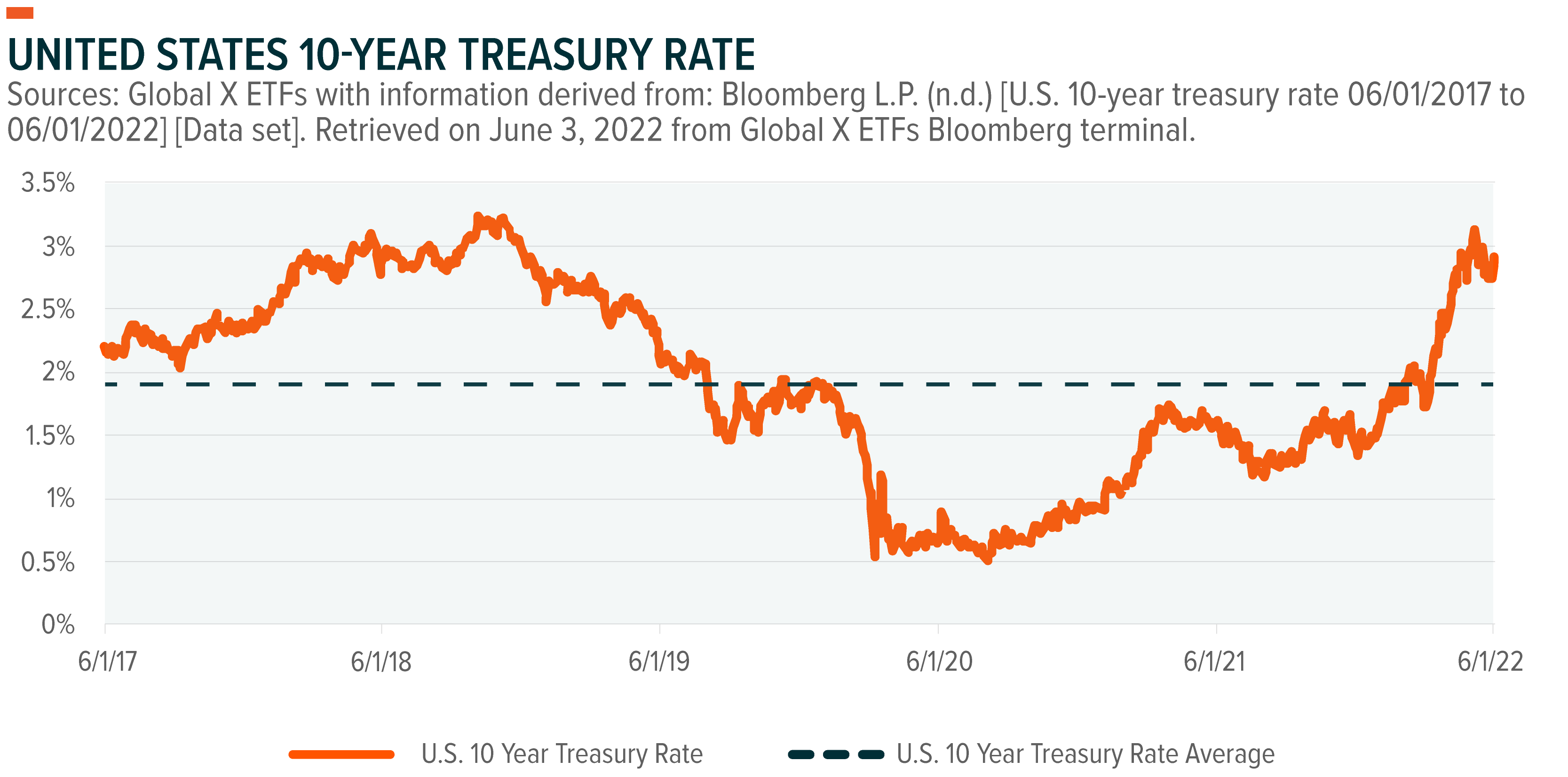

The Fed’s hawkish policy stance and sticky inflation is causing the bond market to react. Yields have been spiking up in this time frame, and the 10-year treasury rate has been hovering around 3% recently, a level not seen since 2018.

Equity Market Performance in a Rising Rate Environment

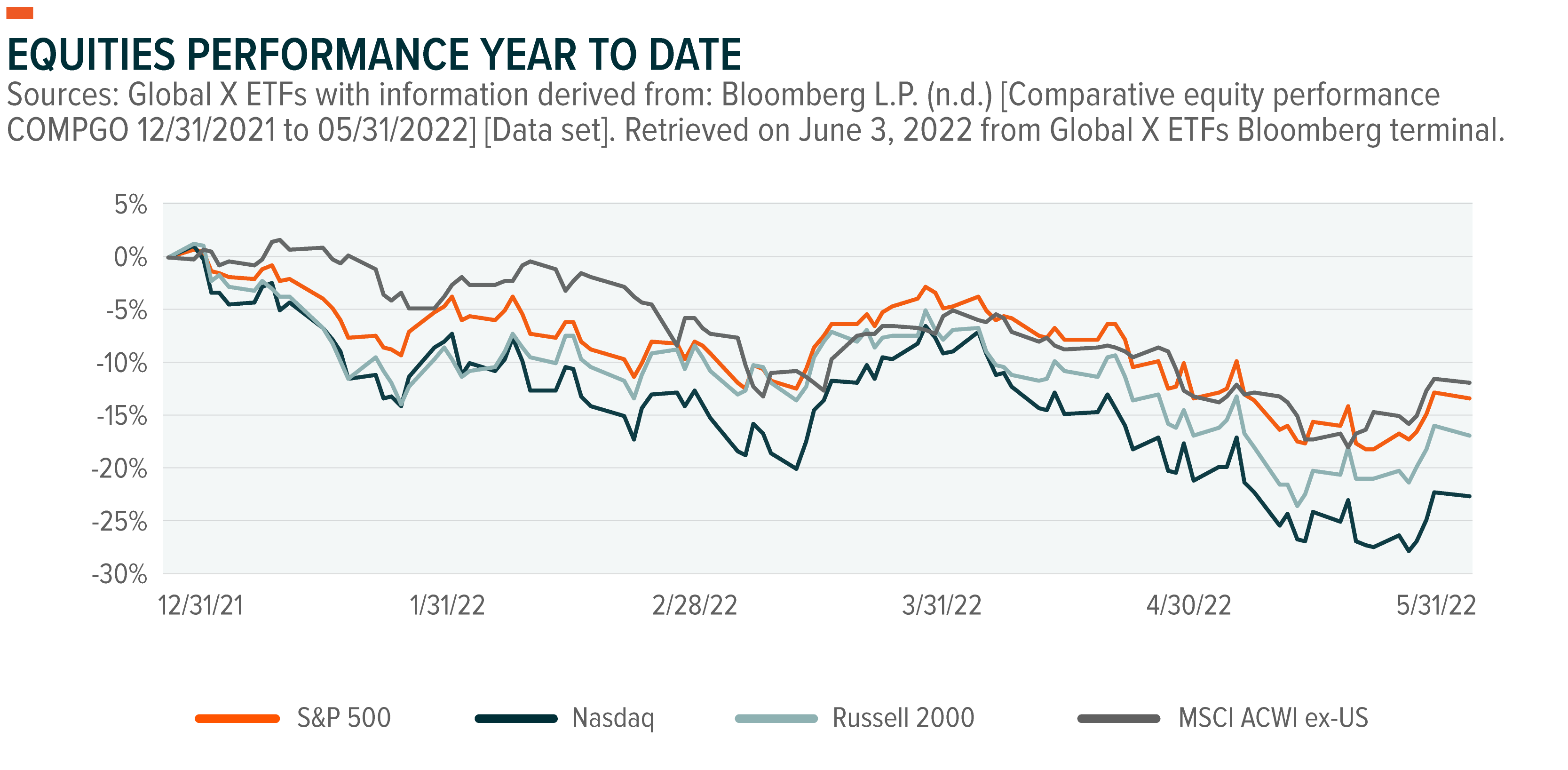

After a decade-plus of ultra-low interest rates, it was only natural that equity markets would perform well on the back of low financing costs. The latest bout of rate hikes is pressuring equities this year though. Most of the market decline is coming from lower price to earnings ratios though, known as multiple contraction, rather than because of deteriorating fundamentals through a decline in earnings, for example. In fact, S&P 500 earnings growth was up 9.2% for Q1.4 But the forward price-to-earnings (P/E) ratio dropped from 22.7x to 18.3x.5 Consequently, growth-oriented sectors like Technology have lagged the most, and indexes with heavy tech exposure like the Nasdaq 100 have underperformed.

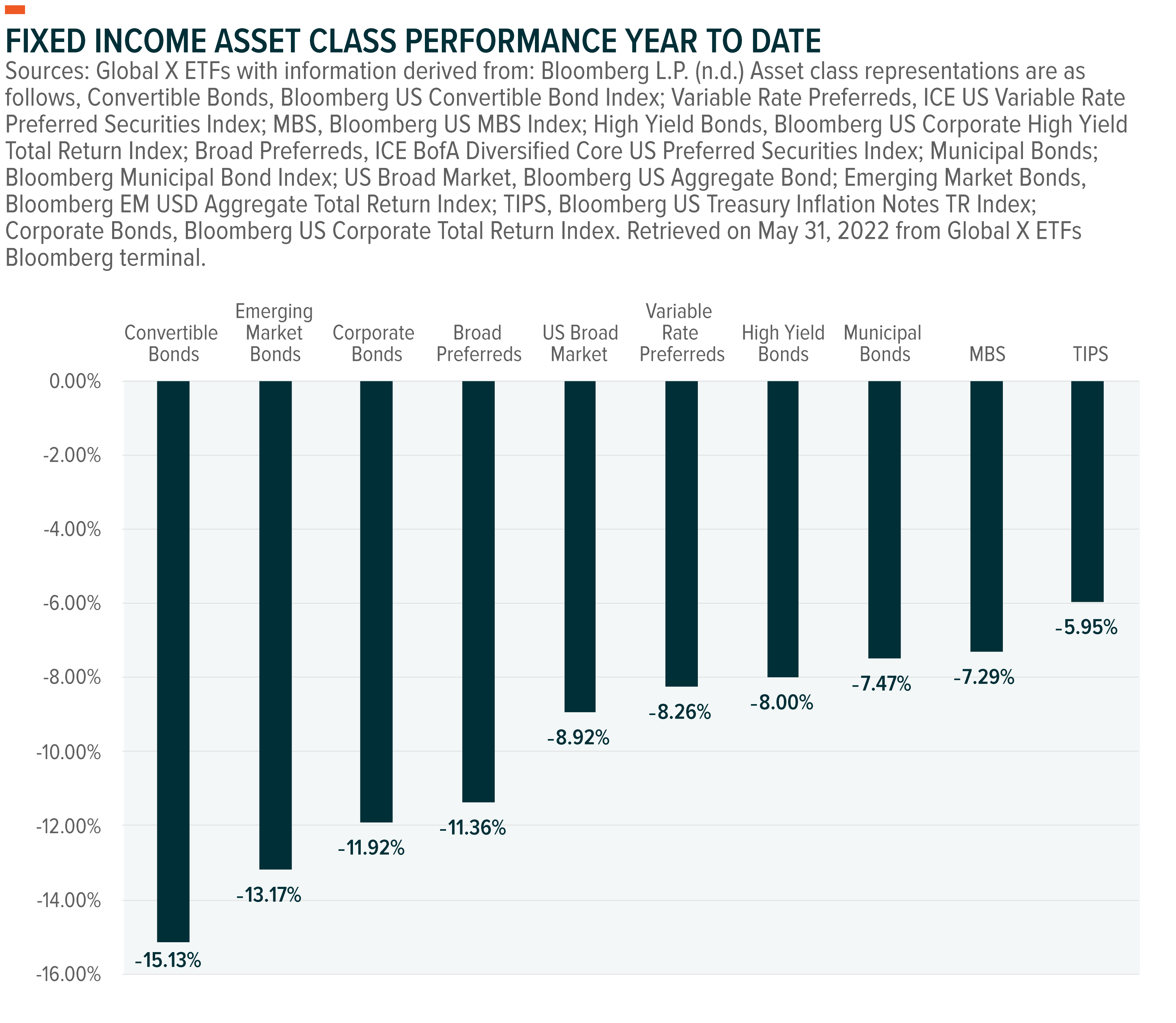

Fixed Income Performance

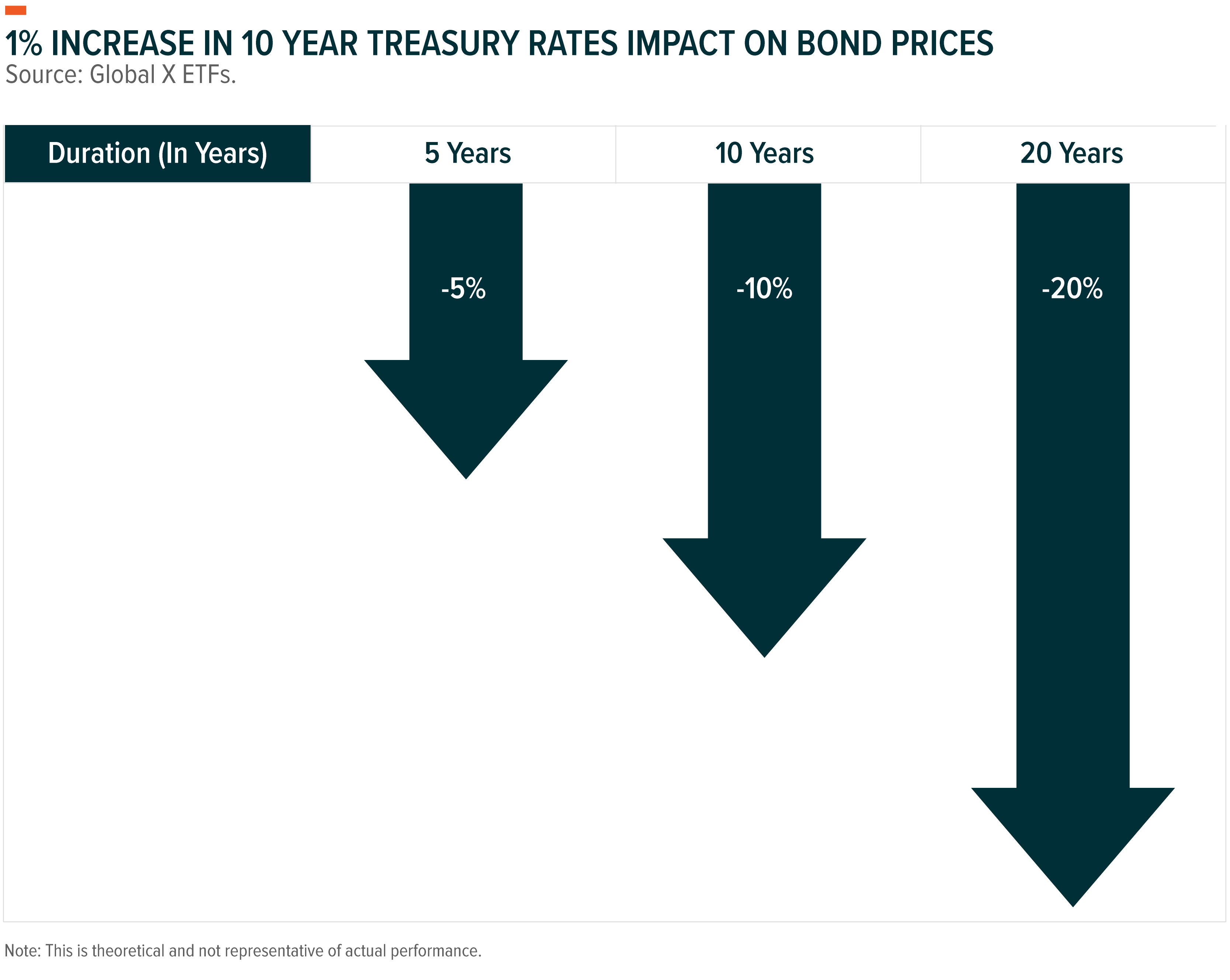

Ultra-low interest rates were not a boon to just equities, but also contributed to strong fixed income performance. Duration sensitive assets performed well as interest rates have remained low since the financial crisis, particularly with tight credit spreads. However, the rise in rates this year means investors need to be cognizant about how much interest rate risk is present in their portfolios. For many income investors or conservative investors, this duration risk may range from moderate to substantial. The inflationary environment and lack of real (inflation-adjusted) yield is likely to compound this problem further.

This duration risk amid today’s rising rate environment is flowing through fixed income’s performance this year. The broad bond market is down -9.3% this year through May 31, a staggering drawdown for the bond market.6

RATE, Explained

Strategies that specifically target interest rate risk are one potential solution for investors to consider in a rising rate environment. They can help mitigate both duration risk inherent in most fixed income instruments, and equity market multiple contraction in response to rising rates.

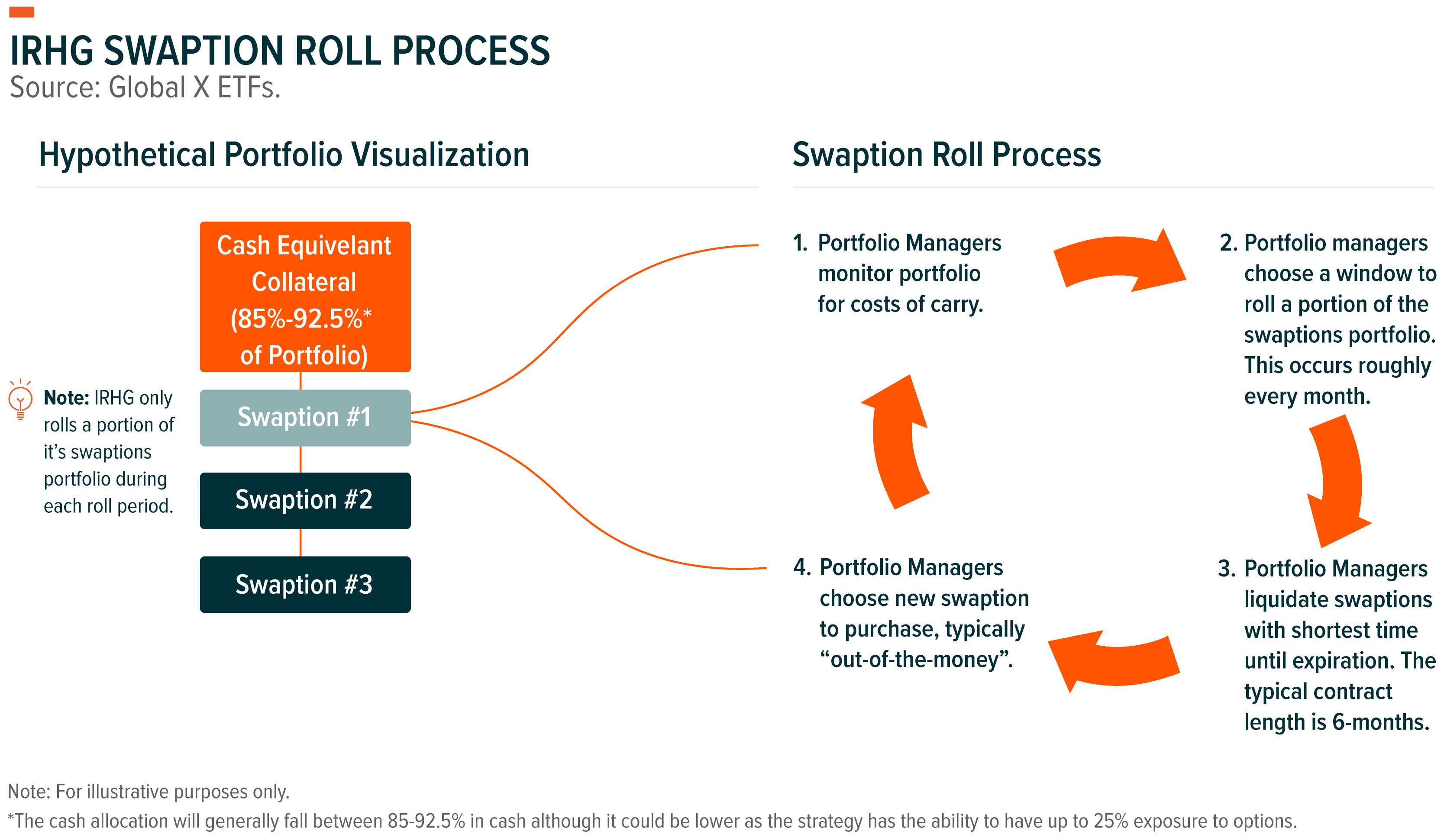

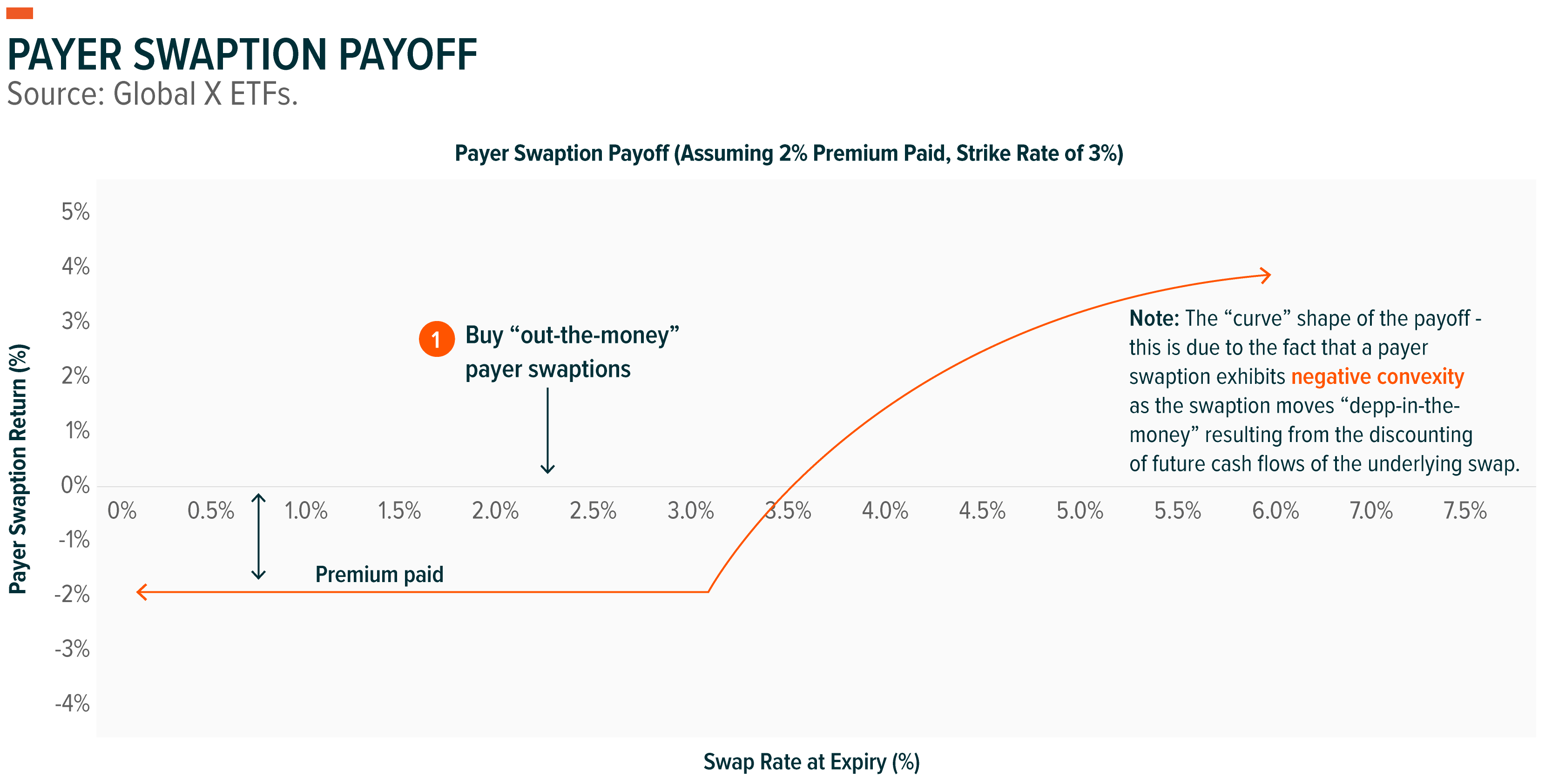

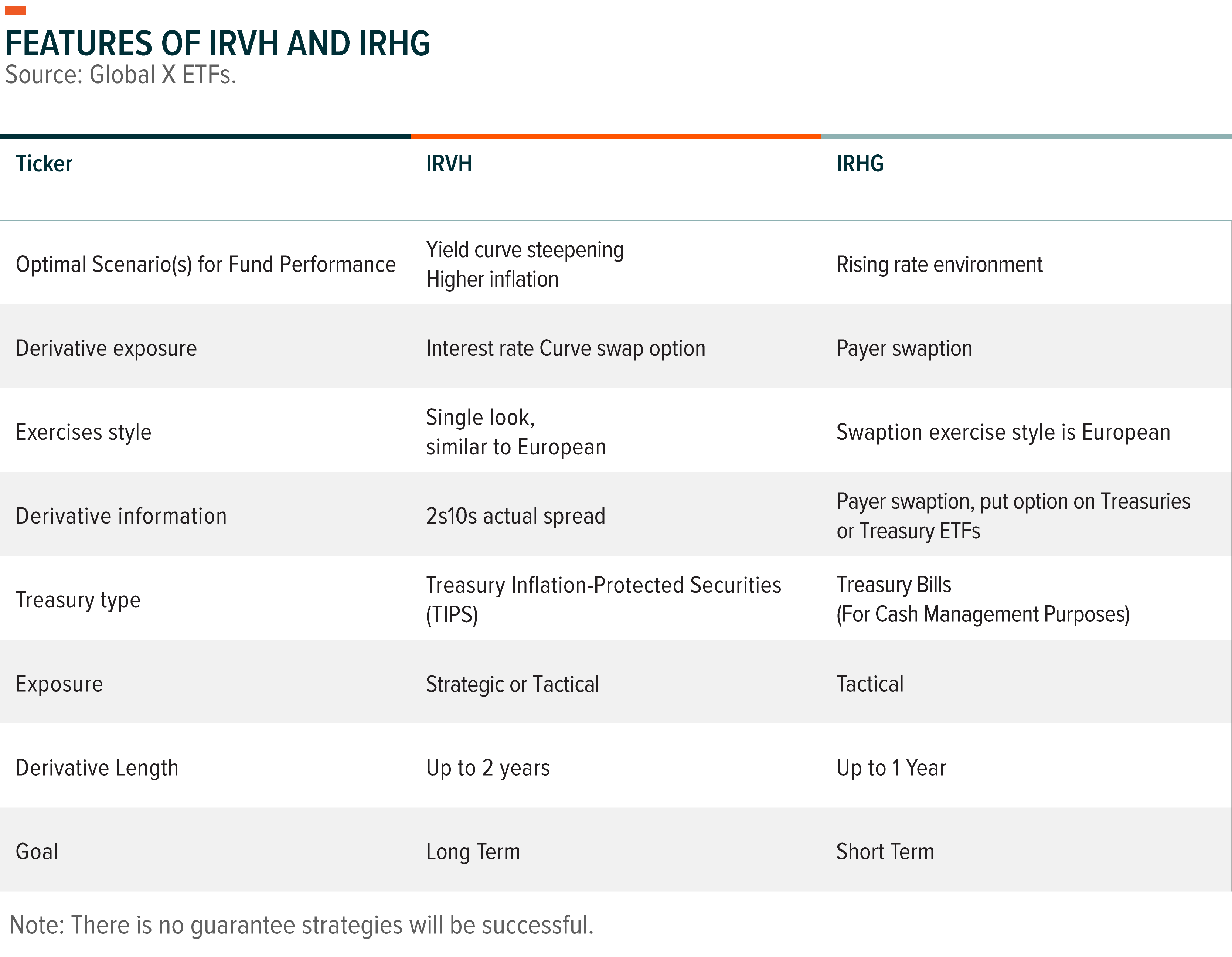

The Global X Interest Rate Hedge ETF (RATE) uses interest rate swaptions and may give investors the ability to hedge interest rate risk either in their fixed income portfolio or more broadly across their entire portfolio. The strategy aims to produce a short-term inverse correlation to long-term treasury bonds and a high correlation to longer-dated interest rate movements. While the fund has the ability to invest in put options on ETFs that primarily invest in U.S. Treasuries and/or put options on U.S. Treasury futures, the fund will primarily invest in payer swaptions, as well as the cash collateral associated with maintaining the positions.

In the interest rate payer swaptions, the Fund has the right (but not the obligation) to enter into a new swap agreement where the Fund pays a fixed interest rate and receives a floating interest rate. Since options have expiration dates, the Fund must periodically migrate out of options nearing expiration and into options with later expiration dates— a process referred to as “rolling.” Global X actively manages this roll process.

RATE’s Strategy in Detail

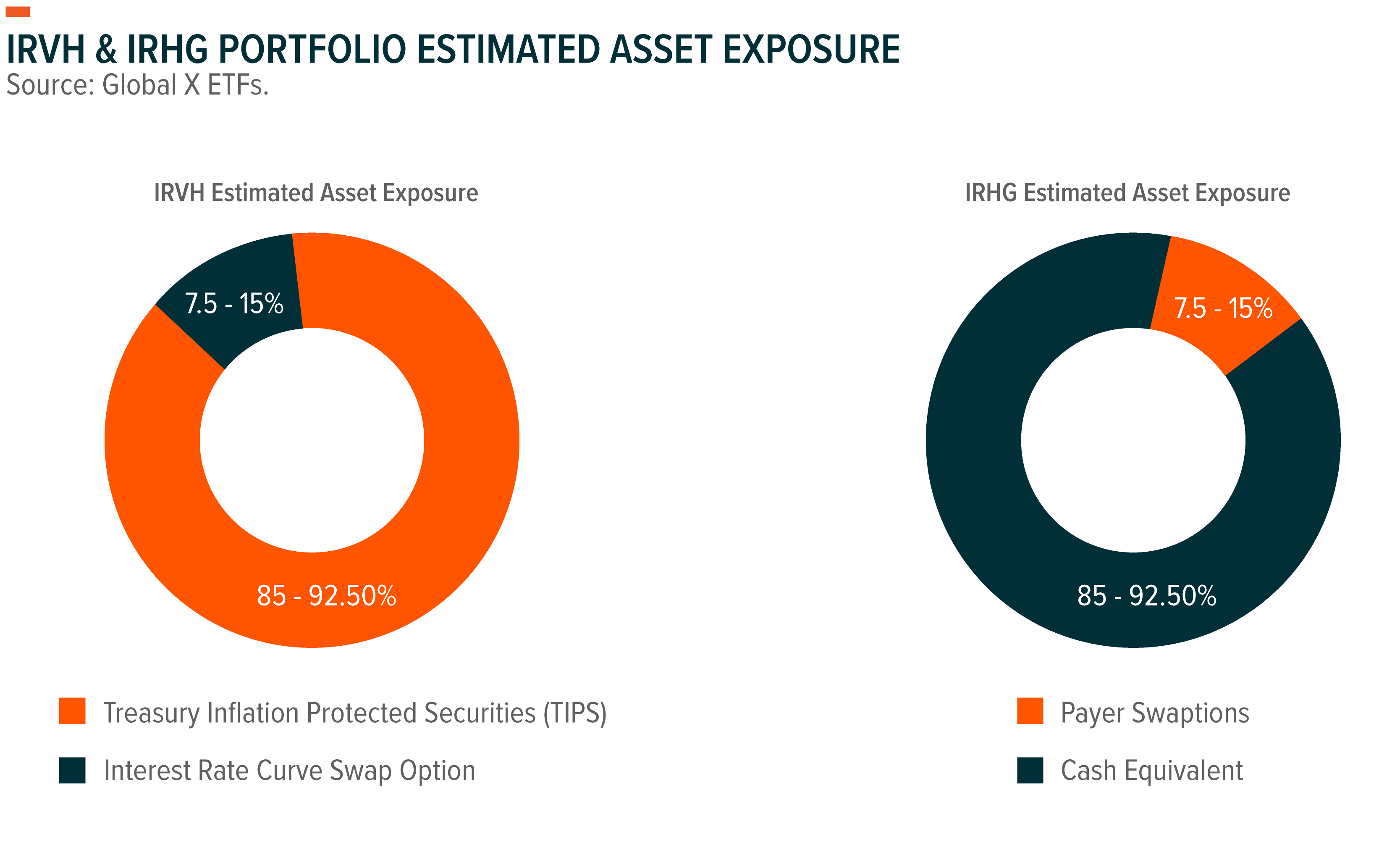

RATE will buy payer swaptions that will generally fall in the range of 7.5-15% of the fund’s assets, although the prospectus allows for an allocation upwards to 25% under normal circumstances. The fund will aim to have its swaptions be purchased at slightly out of the money in order for the fund to have exposure to interest rates.

The strategy utilizes swaption contracts less than 1-year to expiration on the 10 year rate swap. The swap rate is benchmarked to the 10 Year Secured Overnight Financing Rate (SOFR). SOFR is used, as since the financial crisis there is little unsecured bank to bank lending. SOFR is reported in terms of large volumes of transactions and is secured with collateral. All else equal, the strategy would be expected to benefit when long-term interest rates increase and decrease when long-term interest rates decrease.

Portfolio or Investor Goals

RATE provides investors with a tactical tool for higher rates. The fund utilizes slightly shorter options contracts and therefore also have greater cost to maintain the position. The options have more time decay due to shorter expirations. This means the value of the options decline at a greater rate due to a passage of time. This is hard to sustain for a long stretch of time – thus, this strategy is better suited as a tactical allocation. RATE is more of a pure play on a long option strategy while IRVH is more of an option overlay on bonds.

IRVH is more of an option overlay strategy compared to RATE. The TIPS are designed to protect investors against inflation, and the options used in IRVH are longer dated, compared to RATE. TIPS are a Treasury bond that is indexed to an inflationary gauge to protect investors from the decline in the purchasing power of their money. TIPS allow the end investor to benefit from inflation that is higher than expected.

IRVH is expected to pay a positive distribution; the curve steepening and flattening is typically a multi-year cycle that reflects the Fed’s easing and tightening cycles, respectively. The positive carry along with the option being hopefully an improvement to risk-adjusted returns make this strategy more attractive as a longer term holding in lieu of an allocation to Treasuries or TIPS. The carry is referring to the positive yield that comes from the TIPS, as a portion of the positive yield is used to pay for the cost of the curve option.

Portfolios managers of RATE may choose to allocate to swaptions over put options on long term treasury bonds because exchange-traded puts only go out a few months, which is shorter than desired. By using swaptions, the fund is able to have flexibility on strike and tenor. 10yr swap rates can be thought of as a proxy for 10yr Treasury yields.

Depending on duration risk in a fixed income portfolio allocation, investors may consider allocating a greater portion of their fixed income assets to RATE.

IRVH, Explained

The Global X Interest Rate Volatility and Inflation Hedge ETF (IRVH) is a potential solution for investors that targets both inflation and the effects of interest rate volatility. IRVH provides exposure to numerous omnipresent factors for investors – inflation, rates, curve steepness, and interest rate volatility, and may be a substitute for traditional fixed income allocations like treasuries in a volatile interest rate environment.

IRVH is actively managed and provides diversification and an efficient hedge for a hypothetical traditional 60/40 equity and fixed income portfolio. Active management allows the fund to seek to capitalize on opportunities on the operational side in changing market trends and efficient options execution. The ETF structure allows for greater liquidity which investors can benefit from as both as a tactical vehicle or a long-term vehicle.

The weighting between the two legs (TIPS & interest rate curve spread options) is designed to help balance the risk between rising inflation and interest rate risk. The fund’s primary objective is to hedge relative interest rate movements arising from a steepening of the US interest rate curve and to benefit from periods of market stress when interest rate volatility increases, while also providing inflation protected income. This combination offers the potential to provide low correlation to bonds and equities, the common allocations in a 60/40 portfolio. IRVH loosely tracks the Solactive TIPS Index for its TIPS exposure and purchase interest rate curve spread options generally at-the-money (ATM) on the difference (spread) between the 2-year and the 10-year (2s10s) swap rates. These options should benefit if the spread widens, i.e. the 2s10s curve steepens.

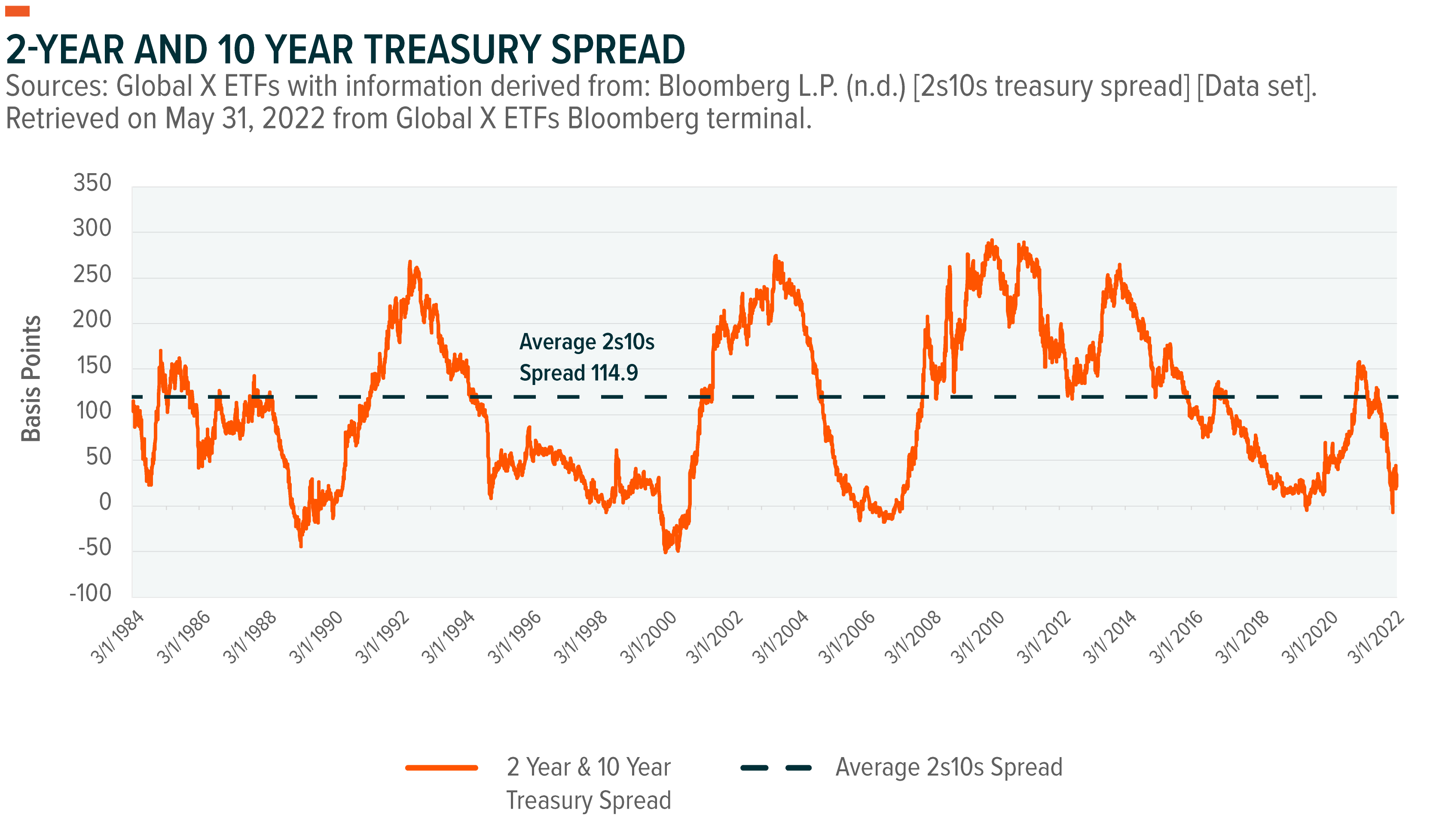

The 2s10s Treasury yield spread is the difference between the 2-year treasury yield and the 10-year treasury yield. A negative 2s10s yield spread has historically been viewed as a recessionary indicator or precursor to market weakness. The Fed signaled that it will further tighten credit and reduce its balance sheets, which is likely to affect the steepness of the yield curve. The Fed’s balance sheet ballooned to $9tn after years of quantitative easing and pandemic support.7 An unwinding of these measures, including quantitative tightening at beginning of June 2022, may start to flow through into movements on the yield curve.

The graph below highlights that the average 2s10s spread going back 30 years is 114.9bps. Currently, the spread sits at 19bps leaving ample room for widening spreads.

As we have seen historically, the curve steepness is highly correlated to Fed cycles. It rarely sits at its average that we have seen near 115 bps. Instead, it tends to trend in one direction for years as the Fed tightens and vice versa when it switches to easing. For values that are close to 0, the curve is signaling that we are near max hawkishness – as the market consensus would then feel that recession is likely and the Fed would need to turn to be more accommodative.

IRVH’s Strategy in Detail

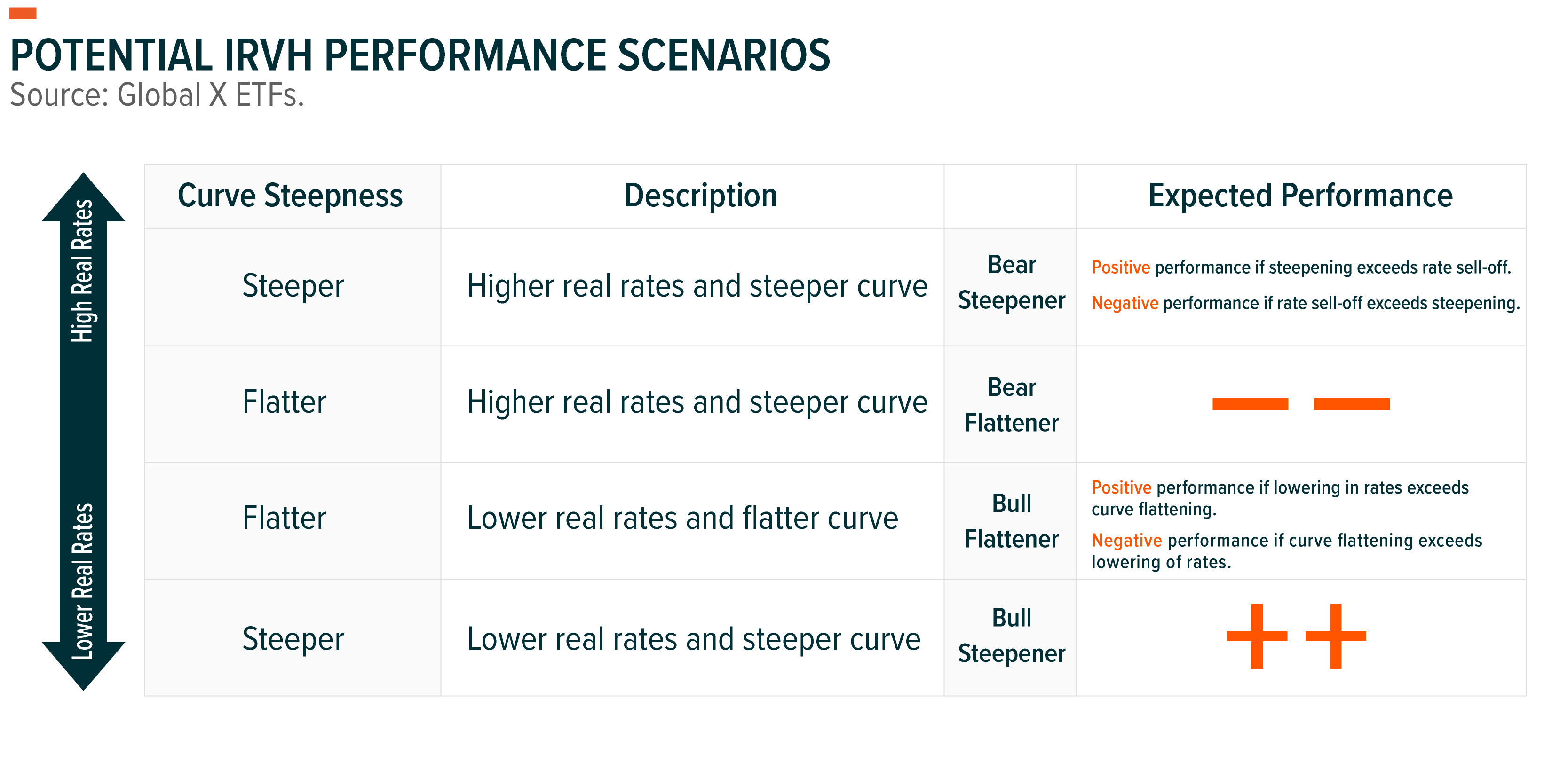

IRVH can be implemented as part of a fixed income, equity, or alternatives sleeve. IRVH should benefit most from a bull steepening in rates and if inflation expectations and rate volatility rise. A bull steepener occurs when the yield curve steepens due to a sharper drop in short-term rates relative to long-term rates. Steepening yield curve would benefit the yield spread curve options and accordingly lower rates would benefit the TIPS portfolio. IRVH may also perform well during periods of uncertainty because it can potentially benefit from both fewer rate hike expectations and increasing inflationary pressures. The payer curve options IRVH implements are on the 2s10s curve and benefit when the forward 2s10s spread widens.

IRVH seeks to strategically protect purchasing power, mitigate inflation risk, capitalize from interest rate volatility along with a steepening US interest rate yield curve. The strategy can navigate these complex market environments by holding uniquely positioned over-the-counter curve options and TIPS.

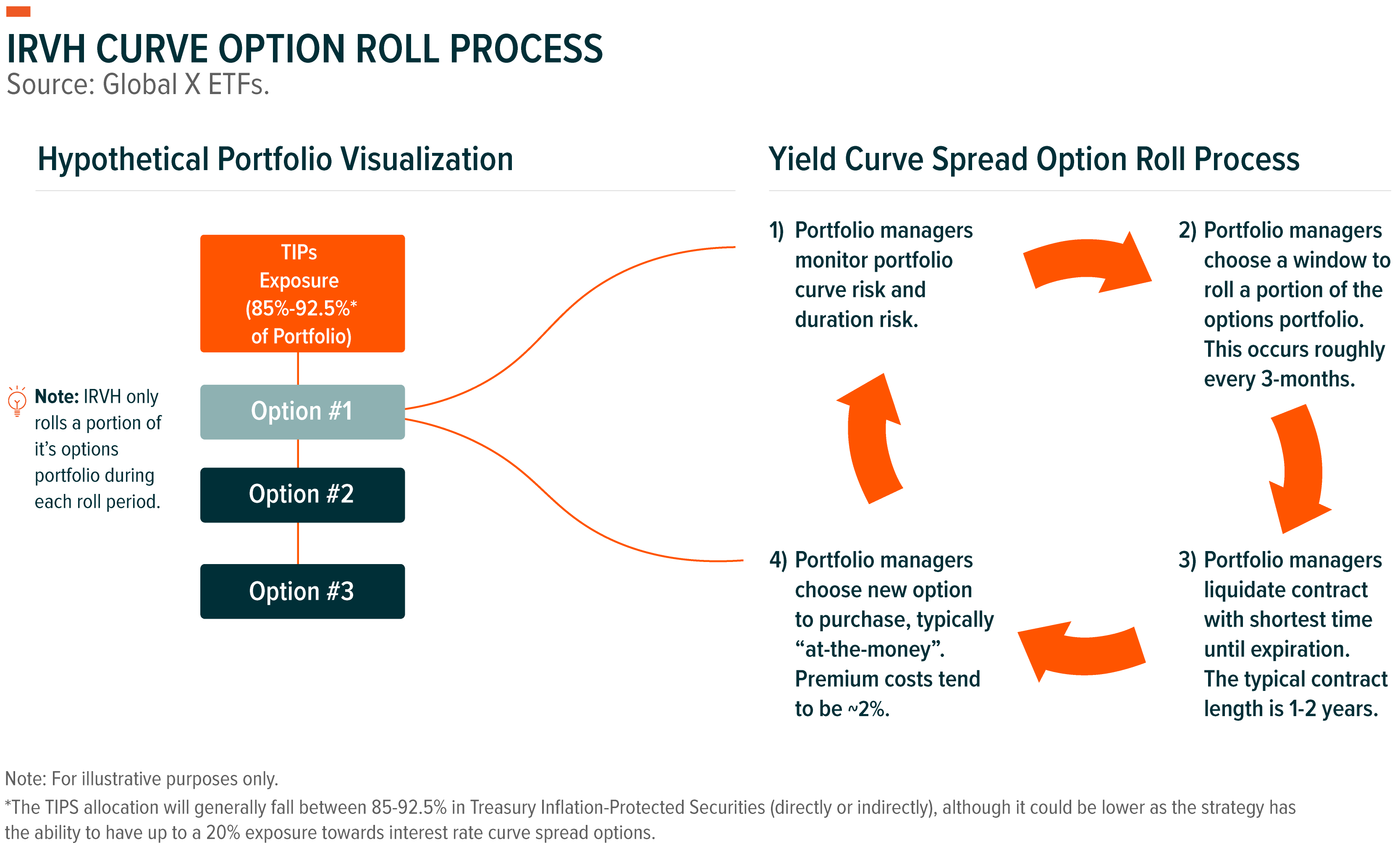

The TIPS allocation loosely follows the Solactive TIPS Index as guidance for performance and duration. The fund will loosely follow the full index because the fund has limited amount of capital and is only allocating approximately 85-92.5% of the fund into TIPS (directly or indirectly). The investable pool of Treasury Inflation-Protected Securities will range from 1-30 year maturities, investing across the maturity curve. The Solactive index represents 40-50 plus securities, while IRVH will hold significantly fewer securities based on liquidity. The Fund can also use other ETFs to gain exposure to TIPS.

By equally managing the variables, this should help mitigate adverse shifts in treasury rates and a flattening yield curve. The goal of the fund is to have 1 standard deviation selloff in rates equal 1 standard deviation steepening of the yield curve; as the fund needs to adjust for volatility and the actual positioning would be risk adjusted. The TIPS allocation will generally fall between 85-92.5% in Treasury Inflation-Protected Securities (directly or indirectly), although it could be lower as the strategy has the ability to have up to a 20% exposure towards interest rate curve spread options.

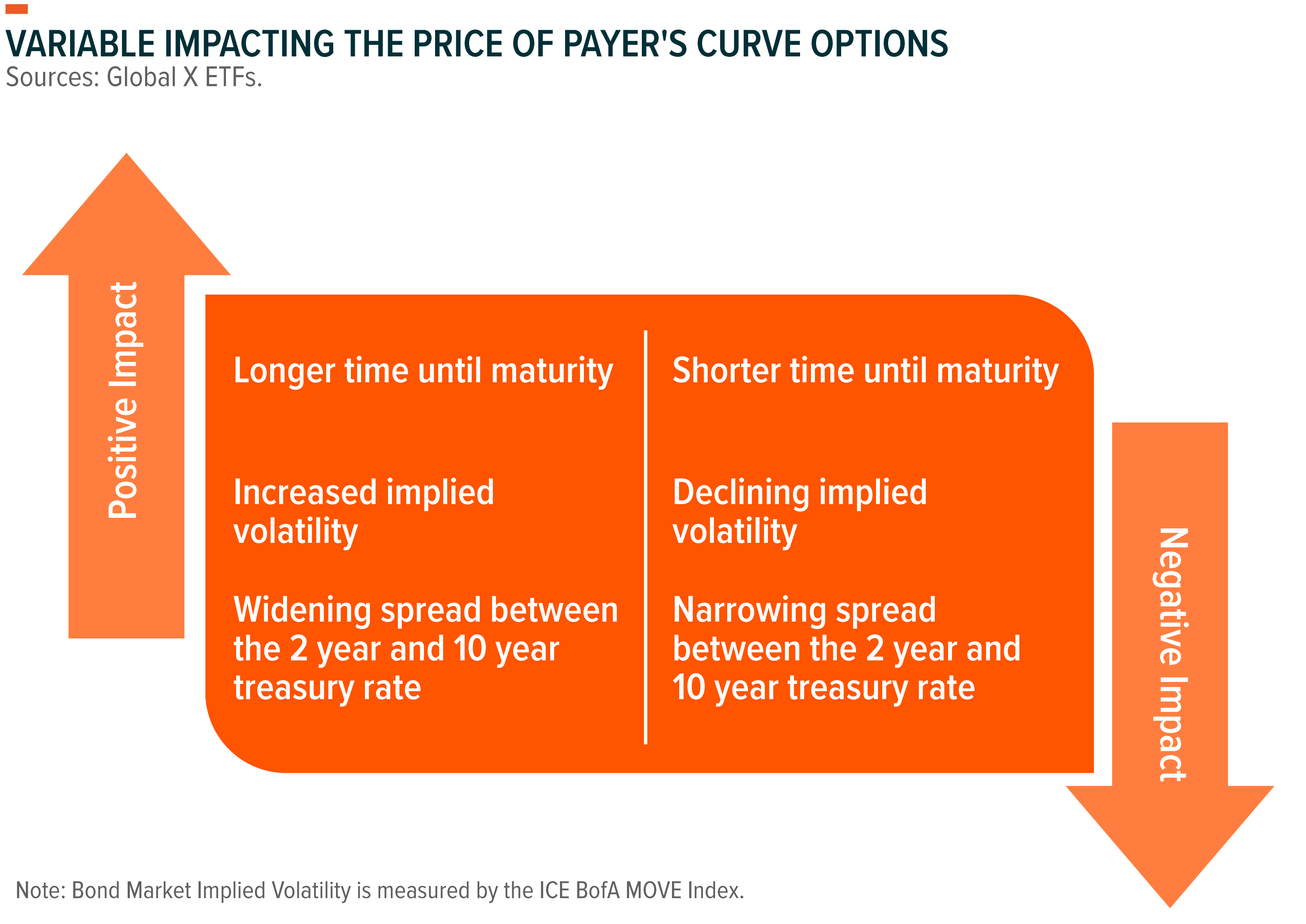

An interest rate curve spread option is where the buyer pays a fixed price for the right (but not the obligation) to receive the difference between the spread of a long-term interest rate and a short-term interest rate and the option’s strike price. The options in IRVH are weighted in an effort to balance the real rates and yield curve components in the strategy. The options are expected to be rolled quarterly, and initially the options will be purchased at-the-money (ATM). We also anticipate the options to be sold prior to expiration.

IRVH may also offer income potential from its interest payments from the TIPS that are held in the fund. As the fund is actively managed, the portfolio managers are able to be more flexible operationally on the trading of the options contracts to distribute yield and roll the fund’s curve options.

IRVH’s TIPS & Interest Rate Curve Spread Options Relationship

IRVH offers investors the potential to hedge against both inflation and the shape of the yield curve by pairing a TIPS portfolio with Over-the-Counter (OTC) interest rate curve spread options.

IRVH invests in interest rate curve spread options positioned so the fund benefits when the 2s10s spread widens, also known as the yield curve steepening. The yield curve can steepen from either rising long-term interest rates or falling short term interest rates, which are historically associated with large equity market declines.

An interest rate curve spread option is an option tied to the spread between two constant maturity swap rates with different terms. The payoff is determined by the difference between the option strike and the swap rate spread at the curve option’s expiration. IRVH will generally purchase options referencing the 2-year and 10-year treasury swap rate spread, which is the difference between the 10-year treasury rate and the 2-year treasury rate. If interest rate volatility increases in that investors expect larger fluctuations in interest rates, then the value of the options held by IRVH should increase.

IRVH is composed of approximately 85-92.5% in Treasury Inflation-Protected Securities (directly or indirectly) and 7.5-15% in a ladder of interest rate curve spread options. The options utilized are single look options that can only be exercised at expiration. These interest rate curve spread options are used to take a view on future relative changes in different parts of the yield curve as the floating leg of a yield curve spread option that benefit from a widening of the 2s10s interest rate swap curve. This can occur in two ways: (1) short term rates lowering (2) long term rates rising, widening the 2s10s spread.

The underlying swap rate for the contracts is the spread between the 10-Year Treasury yield and 2-Year Treasury yield. This is what gives investors exposure to the shape of the yield curve. Utilizing OTC options gives IRVH the ability to customize its contracts with counterparties. With expiration dates of 1-Year to 2-Years, the underlying options do not have to be rolled as frequently, reducing transaction costs.

IRVH may perform well during periods of uncertainty because it can potentially benefit from both fewer rate hike expectations and increasing inflationary pressures. As such, IRVH can benefit from lower front-dated yield expectations, typically occurring in a more risk-off environment when equities and bonds are selling off or in a higher inflation expectation environment.

Comparing IRVH and RATE

While IRVH and RATE use exotic option strategies, they are designed to benefit from a changing interest rate landscape. Both funds are designed to have strong performance in different interest rate environments. Below summarizes a few of the key variables associated with each fund.

The optimal scenario for fund outperformance should be market factors that lead to yield curve steepening and higher inflation for IRVH and a rising rate environment for RATE.

A steepening yield curve shows the difference between short- and long-term yields widening. A steeper curve suggest that investors expect better market conditions to prevail in the long term. This can occur as a bear steepener or a bull steepener. A bear steepener occurs when the yield curve steepens due to a sharper rise in long-term rates relative to short term rates. A bull steepener occurs when the yield curve steepens due to a sharper drop in short-term rates relative to long-term rates.

There are two types of option exercises – American and European style options. American style options can be exercised at any time prior to expiration. European options are referred to as single look as they can only be exercised at the one time of expiration. IRVH uses a single look yield curve spread option that is similar to European style options. RATE uses a payer swaption that has a European exercise style.

Interest Rate Curve Swap Option: ~20x notional

Payer Swaption: ~10x notional

Options exposures may be greater than the estimates shown. Please see the funds’ prospectuses for more information.

IRVH can be implemented as part of a fixed income, equity, and alternatives sleeve. All else equal, if the 2s10s spread increases, IRVH’s options are expected to contribute to performance. If 2s10s spread decreases, IRVH’s options are expected to detract from performance. Positive values of this spread may indicate future economic growth while negative numbers may indicate an economic downturn. IRVH’s options portfolio may benefit during periods of both fewer rate hike expectations and increasing inflation expectations. Generally, IRVH would be expected to benefit when the yield curve steepens and underperform when the yield curve flattens or inverts.

For illustrative purposes only.

For illustrative purposes only.

Essentially providing inverse exposure to treasury bonds, RATE can be used to reduce duration risk in a fixed income portfolio, or as a tactical hedge depending on an investor’s views on rates. RATE offers investors the ability to be nimble during periods of rising interest rates, but also long-term as a way to mitigate the impacts of duration. RATE may work well in a portfolio as a tactical hedge as it provides potential for better risk-reward potential as interest rates rise to hedge a bond portfolio. All else equal, as interest rates increase, RATE’s swaptions are expected to contribute to performance. The contrary is also true, which is as interest rates decrease, RATE’s swaptions are expected to detract from performance. Moreover, all else equal, as rate volatility increases, RATE’s swaptions are expected to contribute.

Using RATE in a portfolio allows investors to hedge the duration risk imbedded within the investors’ fixed income sleeve. For investors with elevated duration risk, IRVH may help alleviate the downside of a portfolio during rising rate environments. During falling rate environments, IRVH should mitigate the full capture of the upside, compared to a pure portfolio of long-duration fixed income securities. Thus, RATE may be best implemented in a portfolio when there is belief that interest rates will rise or continue rising.

Why Investors Should Consider Interest Rate Curve Swap Option Strategies

In today’s rising rate environment, using options-based ETFs targeting interest rate moves and volatility can be an attractive strategy for investors who are seeking an efficient or tactical hedge and diversification within their portfolios.

The Federal Reserve has been very hawkish and has signaled accelerated tapering through this year and next year. For the long end of the curve, there is significant equity risk in a rising rate environment. We believe that one way that investors can help protect their portfolios is to allocate a portion of their portfolio into funds that are designed to have strong performance in a different interest rate environment.

Option strategies can provide investors with potential downside mitigation without selling or choosing cash allocations. For investors looking to diversify their exposure in fixed income, such as only an allocation to US treasuries, interest rate curve swap options strategies could provide exposure to a more strategic diversified set of factors. For investors looking to tactically hedge their interest rate exposure, interest rate curve swap options strategies offered at a low price could provide significant protection without needing to manage the hedge themselves.

Related ETFs

RATE: The Global X Interest Rate Hedge ETF is an actively-managed ETF designed to benefit when long-term interest rates increase. RATE seeks to achieve its investment objective primarily by investing in long interest rate swap options (“swaptions”) and long positions in short term U.S. Treasury securities. The latter is mainly utilized for cash management purposes. RATE may invest in U.S. Treasury bills directly or through other ETFs.

IRVH: The Global X Interest Rate Volatility & Inflation Hedge ETF is an actively-managed ETF designed to offer investors inflation-protected income potential while also potentially benefiting from a steepening of the yield curve and an increase in interest rate volatility. IRVH seeks to achieves its investment objective by primarily investing in, directly or indirectly, a mix of TIPS and interest rate options on the shape of the yield curve.

The value of TIPS increases with inflation, a feature that is intended to protect investors from inflation risk. However, TIPS are also highly sensitive to interest rates. By purchasing yield curve spread options, IRVH seeks to partially mitigate some of the interest rate sensitivity of TIPS, as the options are expected to benefit from a steepening of the yield curve and an increase in interest rate volatility.