Morgane Delledonne

Morgane DelledonneFollowing a year where inflation consistently shaped markets and central bank monetary policy, 2023 appears unlikely to create rate shocks, even as inflation remains top of mind. We expect more gradual interest rate hikes around the world than last year amid slower economic activity. In this environment, investor focus is likely to shift to opportunities stemming from China’s reopening and defensive strategies in developed markets.

Investment strategies highlighted this month:

- Chinese Equities and Copper Find Tailwinds – The reopening of the Chinese economy and the government’s rescue of the country’s property market are key structural tailwinds for copper. Copper miners offer a leveraged play.

- E-Commerce an Ally to Consumer Purchase Power – With high inflation in the West, the consumer’s hunt for discounts and flexible payment options is positive for e-commerce sales. China’s recovery could also boost the sector.

- Food Inflation Could Accelerate AgTech Adoption – Global warming, the war in Ukraine, and higher production and transportation costs are likely to keep food inflation elevated. We believe higher food prices could trigger a quicker shift towards AgTech, a shift that may offer investors a defensive positioning.

Copper and Copper Miners: An Indirect Way to Capture China Reopening

Three factors triggered the marked rebound in Chinese equities since the beginning of the year: reduced geopolitical risk between China and the U.S. following the G20 meeting last November, the government’s property market rescue, and the end of COVID-19 restrictions. The MSCI China Index has climbed almost 14% year-to-date.1 Themes that have outperformed the benchmark index’s fast start to the year include the Solactive China Cloud Computing v2 index returning over 21%.2

Despite the current COVID-19 wave ahead of the Chinese New Year, we believe China’s economic recovery creates opportunities in Chinese equities and copper. The current market rebound is likely to accelerate once COVID cases peak, probably in Q1.3 Chinese inflation remaining low will likely allow the People’s Bank of China (PBOC) to maintain its accommodative stance.

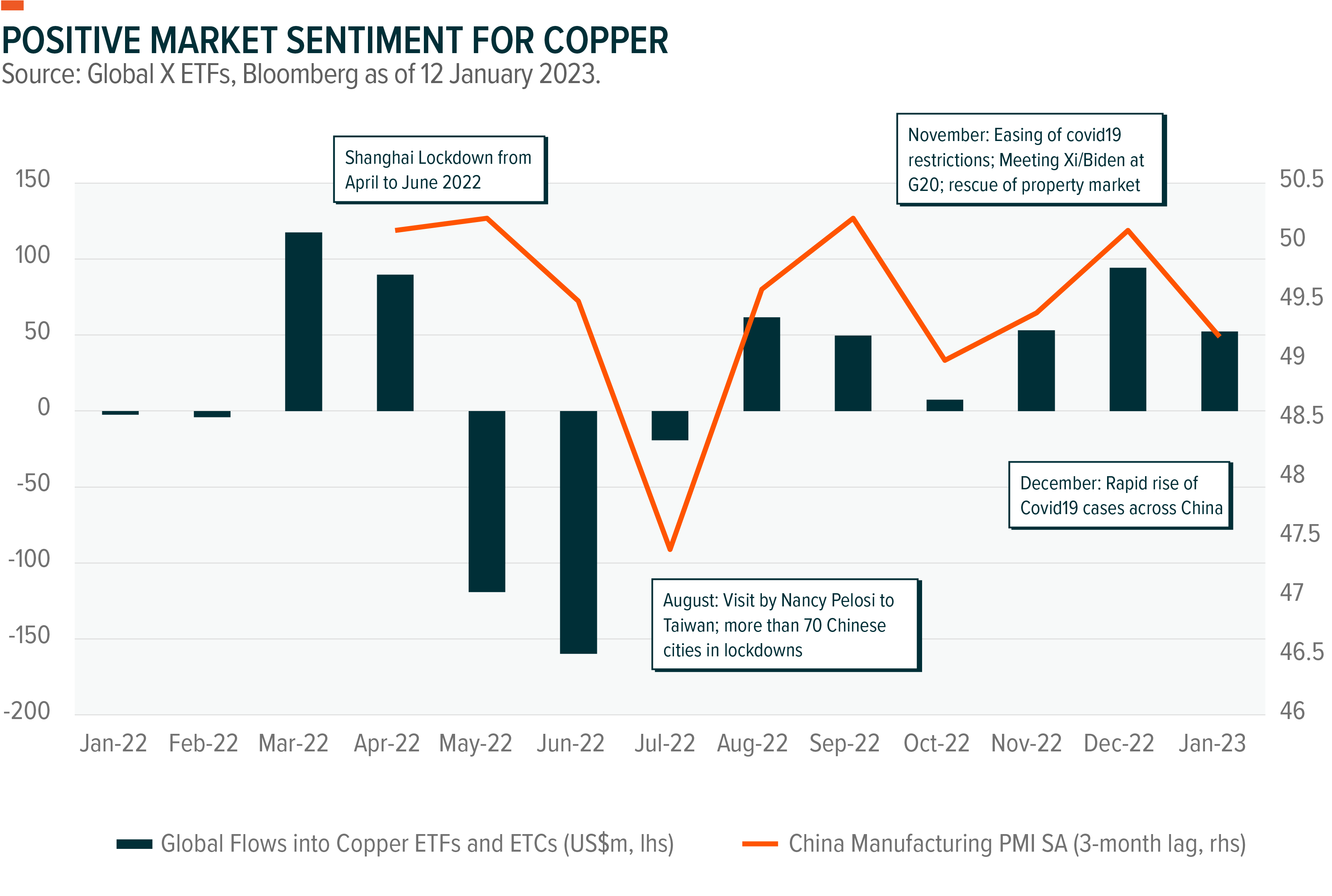

Market sentiment for Chinese assets, copper included, is more positive overall despite investors remaining polarised. Flows into copper-related ETFs and ETCs are quite sensitive to investor sentiment towards China, which as the world’s largest consumer of copper accounts for more than half of total demand. China’s economic development and infrastructure projects and construction have tripled the nation’s copper demand in recent decades. The graph below shows the positive correlation between global flows into copper trackers and the 3-month lag China Manufacturing PMI. The significant rebound in net inflows since mid-November last year followed a series of positive news that fueled optimism about a quick Chinese recovery.

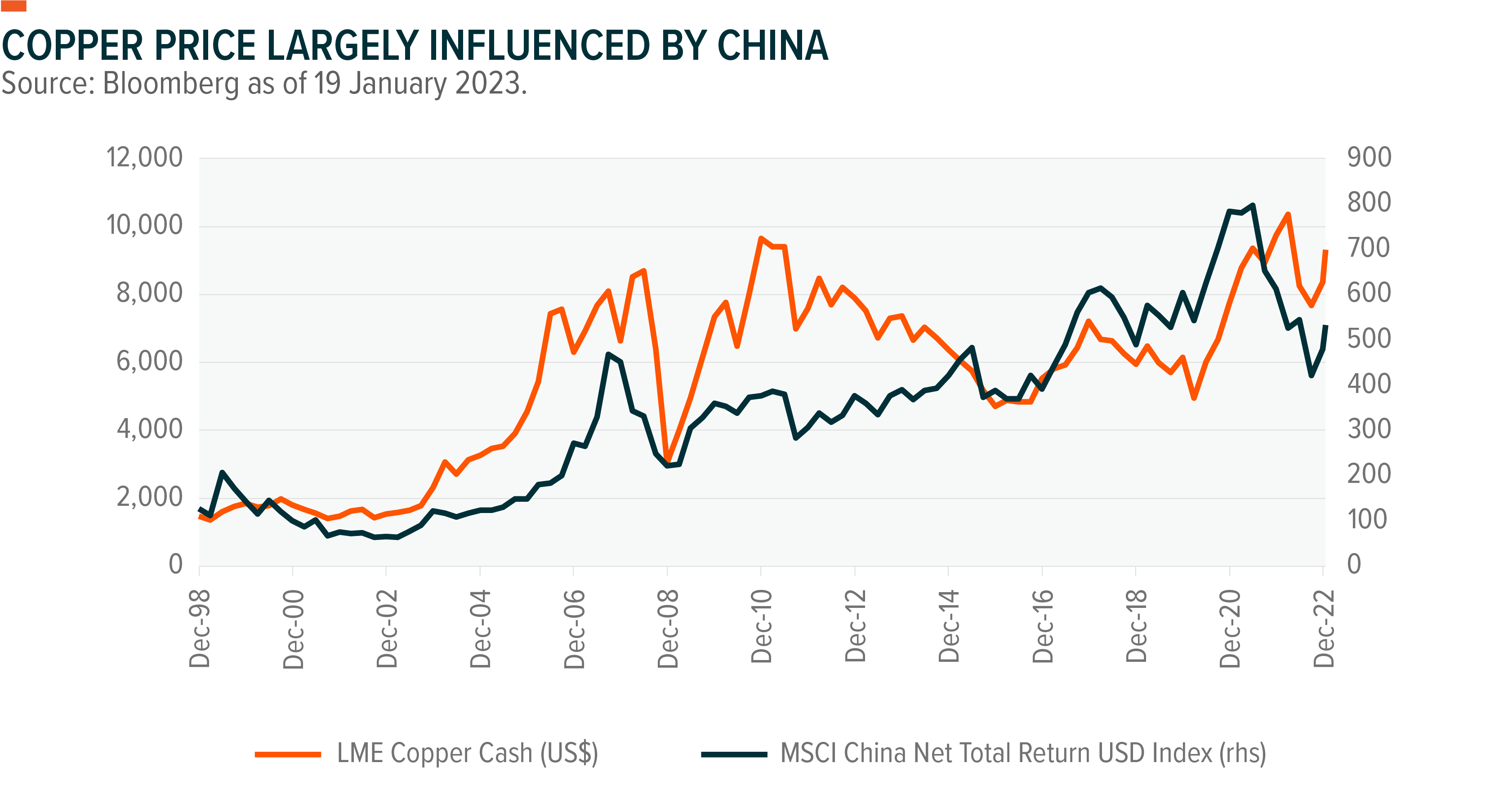

Copper and its leveraged strategy through copper miners is expected to benefit from improving economic data in China while also being supported by structural demand as a core component for clean energy technologies and electrification. Copper prices exhibit a positive correlation to economic indicators and with Chinese equities (0.44). Copper prices have increased by more than 11% since the beginning of the year, and copper miners’ equities have increased by about 16%.4

E-Commerce: An Increasing Solution to Purchase Power Crisis

Despite slowing economic activity, labor markets in developed markets remain tight and will likely continue to support retail sales. In the United States, the unemployment rate is at 3.5%, its lowest level in five decades, and only cooling very slowly in certain sectors, such as Tech.5 In Europe, UK and euro area unemployment rates are also at their lowest points in decades at 3.5% and 6.6%, respectively.6 Demographics and workers not returning to work after the pandemic are playing a role in the tightness of the job markets. For example, the U.S. labor force participation rate is at 62.3%, below its pre-pandemic level.7

Higher mortgage rates and negative real wage growth will likely continue to weigh on U.S. and European consumers. In December, U.S. retail sales dropped 1.1% for the second consecutive month.8 However, we expect the online retail market to be more resilient than the broader sector in developed countries where inflation remains elevated. The flexibility in payment options that e-commerce offers, such as buy now, pay later (BNPL) and the online retailers’ capacity to offer large discounts, could lead digital sales to outperform traditional sales in 2023.

While U.S. consumer credit increased at an annualized rate of 7.1% in November and personal savings neared a new historical low, online consumption has increased.9 U.S. consumers spent a record US$9.12 billion on Black Friday, up 2.3% compared with 2021.10 Similarly, Cyber Monday online sales rose 5.8% to US$11.3 billion.11 In addition, e-commerce accounts for nearly 20% of retail sales worldwide, leaving the sector with a high growth tilt.12

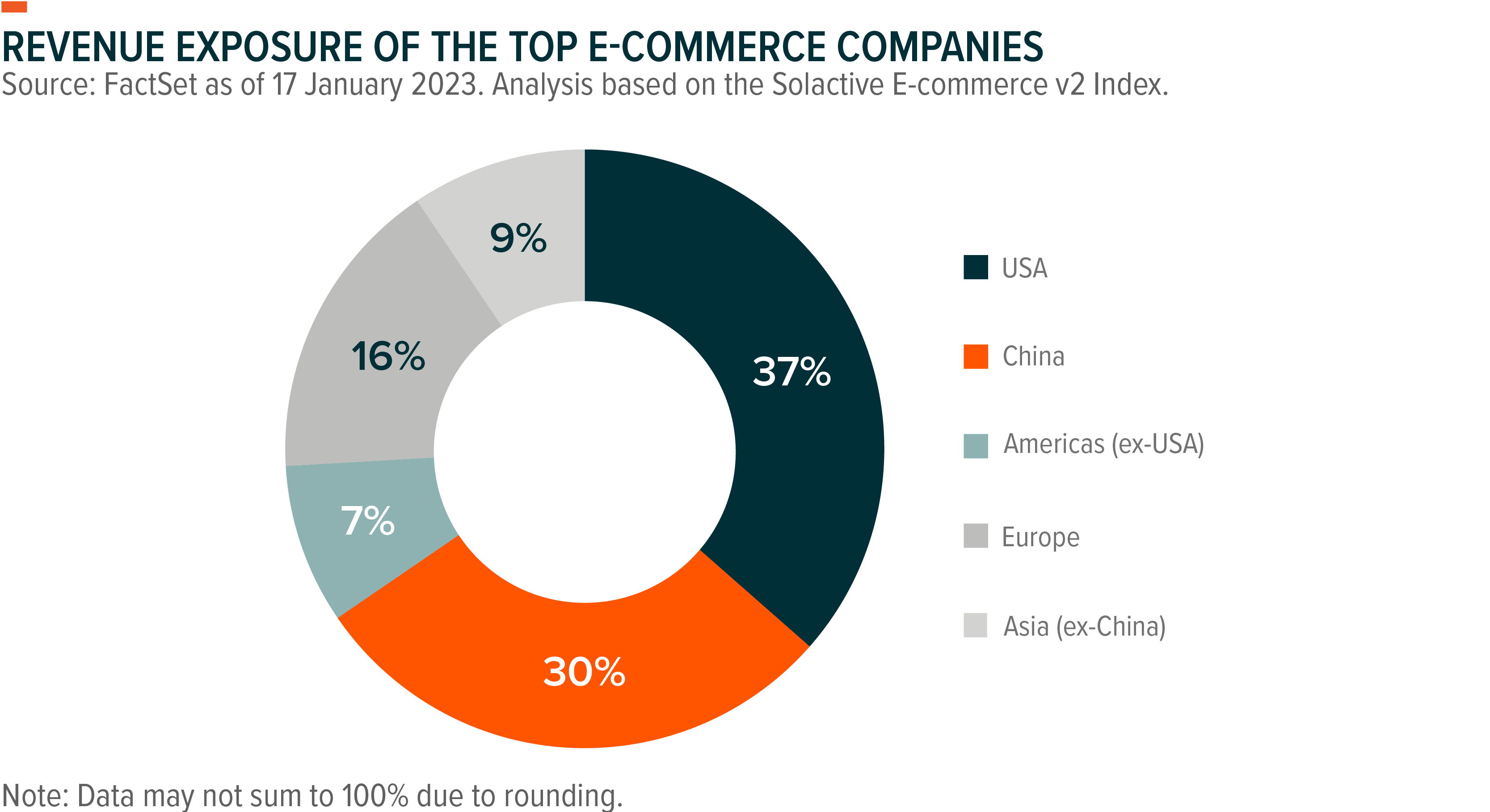

In China, growth supportive measures coupled with the end of COVID-19 restrictions could boost Chinese consumers’ spending this year, which would directly benefit e-commerce companies. China accounts for about a third of the world’s top e-commerce retail sales.13

Also, E-commerce sector valuations are attractive. The basket of e-commerce companies in the Solactive E-commerce v2 Index indicates average 12-month forward sales growth of 13% and price to sales growth of 0.08x, well below those of the NASDAQ 100 Index (0.29x) and the MSCI ACWI Index (0.42x).14

AgTech & Food Innovation: Food Inflation Could Help Digitize Agriculture

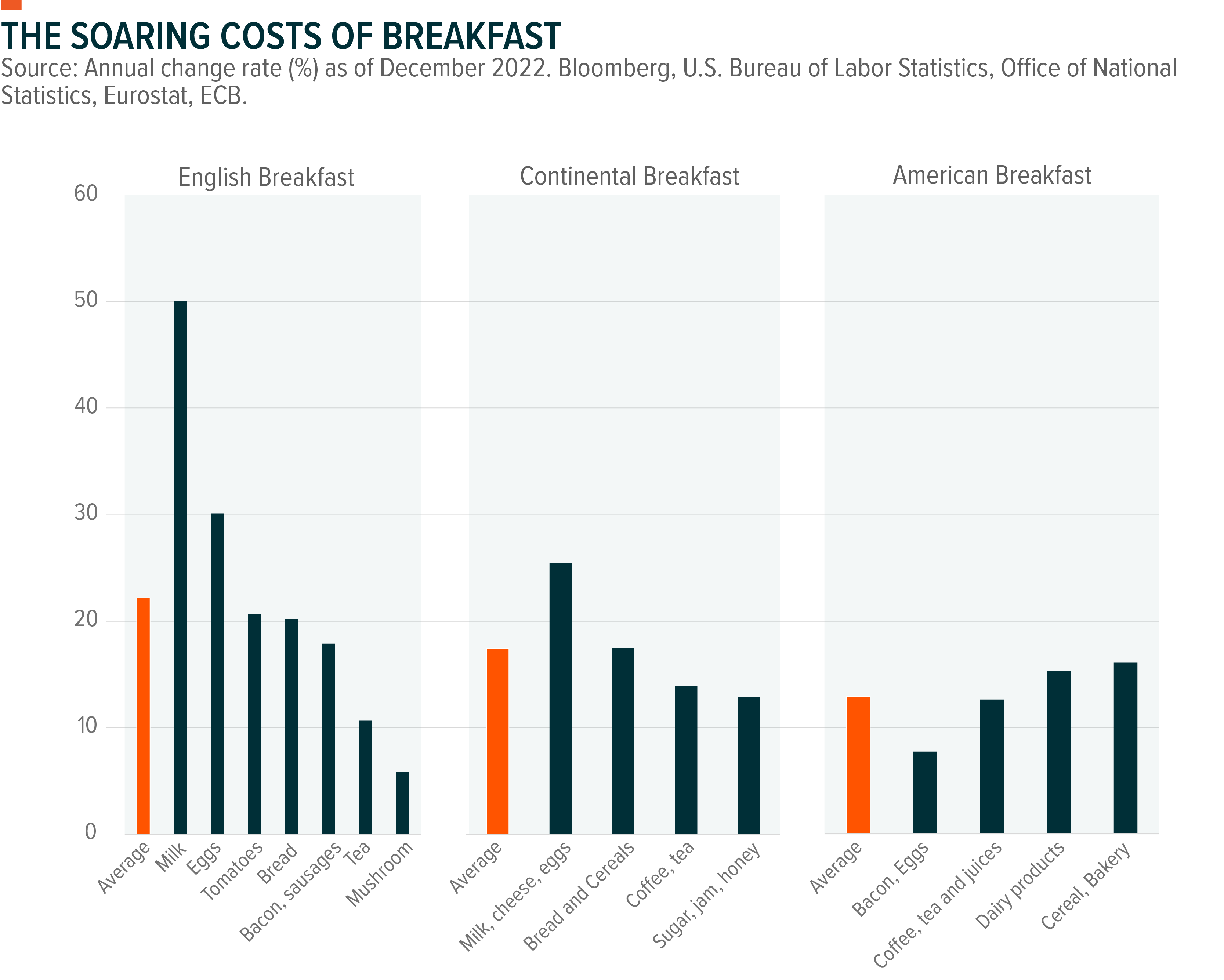

The war in Ukraine created major challenges for global agriculture, as local supply disruptions in Russia and Ukraine removed a significant share of the world’s grain supply and led to soaring nitrogen fertilizer costs, which tripled last spring. Headline inflation in the U.S. and Europe is cooling amid lower energy prices, but food inflation continues to increase in both regions.

The FAO Food Price Index, a measure of the monthly change in international prices of a basket of food commodities, reached an all-time high at 160 points in spring 2022. The index was 17% lower at the end of 2022, but it remains over 40% higher than in 2020, prior to the energy crisis in 2021.15 High agricultural production and transportation costs combined with lower harvests due to severe droughts last summer are now becoming embedded in food costs globally. These dynamics are likely to result in significant shortfalls in food production this year, and possibly beyond.

We believe that stubbornly high food inflation is likely to accelerate the shift towards sustainable and digital farming. It makes agriculture technology, and precision agriculture technologies in particular, more appealing as a way to mitigate costs for farmers and ultimately reduce the volatility in food prices. These technologies can increase crop yields efficiently while using fewer traditional inputs, such as land, water, energy, pesticides, and fertilizer.

The AgTech & Food Innovation theme offers defensive characteristics given its high exposure to consumer staples companies that can pass on those food costs to consumers. The Solactive Agtech and Innovation Index has increased over 11% since the beginning of the year, led by the Consumer Staples sector, which represents over half of the index.16