Global X Research Team

Global X Research TeamAs we cross the halfway mark for 2016, many investors are taking stock of their portfolios’ performance and looking to identify opportunities to add to or scale back allocations to various investments.

In 6 months, the markets have experienced two bouts of extreme volatility, with the first occurring in January and February relating to the spillover effects of sub-$30 oil prices, and the second occurring in June as the markets reacted to the surprise Brexit vote. Read Global X’s Take on the Brexit

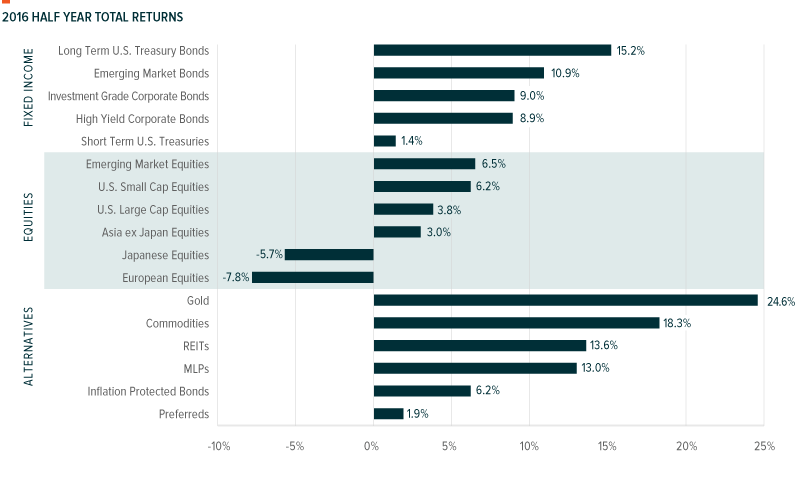

Despite these destabilizing events, most asset classes are up this year, with all but two of our identified asset classes delivering positive returns. Around the world, investments have generally benefited from dovish central bank policies as well as a strong rebound in commodity prices.

Within equities, emerging markets (EM) has been the best performing asset class as rising commodity prices stabilized the economies of commodity-export oriented countries. In addition, slower than expected interest rate increases have benefited emerging market companies that issue debt in USD, as it has helped weaken the dollar versus EM currencies.

Fixed Income has broadly performed well in 2016 despite fears at the end of 2015 of additional interest rate hikes in the US and high yield debt scares driven by low oil prices. Again, dovish interest rate policies and recovering commodity prices bolstered these investments as both duration and credit have delivered strong performances. In addition, the bouts of intense volatility in 2016 have driven many investors towards less risky assets, resulting in greater demand and therefore falling yields for treasuries.

Alternative investments have been among the best performing assets classes in the first half of the year as demand for store-of-value assets like gold and silver drove a recovery in precious metals. In addition, the lower for longer interest rate policies around the world helped bolster income producing alternatives like REITs and MLPs.

Below is a breakdown of the year to date total returns for a variety of benchmark indexes spanning multiple asset classes.

Source: Bloomberg. 12/31/2015 to 6/30/2016.

Source: Bloomberg. 12/31/2015 to 6/30/2016.

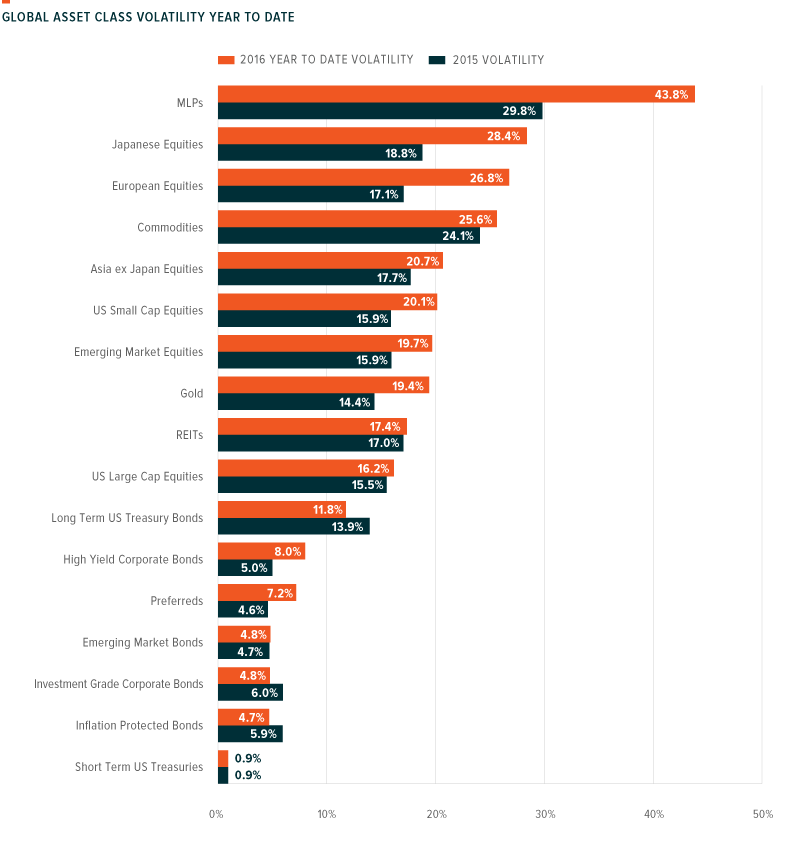

As mentioned, one of the key themes this year was the rise in global market volatility. Below is a comparison of the volatility in 2015 compared to the 2016 year to date annualized volatility. 13 of the 17 major asset classes have experienced higher volatility compared to 2015, despite mostly positive market performance.

Source: Bloomberg. 12/31/2015 to 6/30/2016.

Source: Bloomberg. 12/31/2015 to 6/30/2016.

Looking forward, we believe increased volatility will remain the norm as markets react to central bank policies, Brexit negotiations, and political elections. In addition, growth will remain elusive as the global economy struggles with challenging demographics like slowing population growth and an aging population, as well as fully priced equity markets with many mature and highly competitive industries.

Given these broad themes, we believe investors would be well suited to allocate to:

- Multi-factor smart beta ETFs, which can harvest returns from factors which have historically outperformed the broad market, while diversifying the risks associated with each individual factor

- Emerging and Frontier market ETFs, which access countries that are exhibiting higher economic growth and have less mature industries than developed markets

- High dividend ETFs which can generate returns even in a sideways market

- Thematic ETFs which seek to benefit from long term structural changes like changing demographics, consumer habits, demand for natural resources, and emerging technologies.

- Commodity miner ETFs which can provide leveraged exposure to underlying commodities like gold, silver, and lithium, while delivering more tax-efficient returns than commodity futures.