Rohan Reddy

Rohan Reddy2018 has not stopped the wild ride for MLP investors that began in 2014. The initial euphoria of tax reform earlier in the year abated as the broad equity markets became more volatile. In mid-March as the Federal Energy Regulatory Commission (FERC) ruling disallowing a previously accepted MLP income tax allowance saw fatigued investors exit the MLP market. While MLPs have recovered by more than 14% since the nadir in late-March,1 a new elephant has entered the room: uncertainty around the future of the MLP structure. Will MLPs simplify their organizations and convert to the more traditional C-Corporation (C-Corp) structure? In this quarter’s MLP Insights, we seek to tackle this question by discussing:

- The History of MLP Roll-Ups

- Recent C-Corp Conversions & the Reasoning Behind them

- Energy Infrastructure: The New Energy Infrastructure Landscape

The History of MLP Roll-Ups

Kinder Morgan (KMI) pioneered the MLP roll-up in August 2014. Just before oil prices collapsed, the company announced they would roll up their entire family structure, which consisted of three separate publicly traded MLPs. At the time, MLP performance had been quite strong, and it was a tough pill to swallow for some unitholders as MLP unitholders were forced to swap their units for cash and lower yielding KMI stock. KMI cited lower cost of capital, a simplified family structure, and future dividend growth among their primary reasons for the roll-up, but the overarching driver in our opinion was flexibility. By becoming one large corporation, Kinder had much more flexibility over their distribution policy so they could reduce their debt over time and organically fund growth opportunities, without needing to depend as much on the capital markets.

Little did we know at the time, but this was the beginning of a series of significant organizational changes in the MLP world, as many MLPs have since opted to cut distributions, remove Incentive Distribution Right (IDR) payments to their general partners, or undergo c-corp rollups in an effort to self-fund growth.

As oil prices began falling precipitously towards the end of 2014 and finally bottoming out in early 2016, many MLPs were forced into difficult positions. While cash flows generally remained much stronger than the Exploration & Production (E&P) space, contagion spread to midstream infrastructure as worries over lower oil prices affected volume expectations for MLPs. As a capital intensive business that doesn’t retain much cash flow, MLPs relied heavily on access to the capital markets to fund their growth. Yet, as oil prices fell and remained low, credit access tightened up as ratings agencies warned MLPs that they were over-levered, and unit prices fell to such low valuations that additional offerings often weren’t conceivable.

Over the next few years, many MLPs had to address this issue in what became known as moving to a self-funding model. The more conservative MLPs were able to simply slow down the growth of their distributions, whereas others needed to make painful cuts to their distributions or reconsider their corporate structure.

Below is a list of midstream MLPs that have undergone distribution cuts and/or corporate actions in the form of IDR restructurings or C-Corp/partnership consolidations during the MLP downturn.

Recent C-Corp Conversions & the Reasoning

To clarify, the decision to undergo a c-corp roll up is not necessarily a sign of weakness for an MLP. Each situation is unique, but management will simply try to determine if the c-corp structure makes the most sense for their assets, which can be influenced by a host of factors including investor base, taxation, valuations, complexity of corporate structure, and underlying assets, just to name a few.

Yet in the current market, there have been three dominant factors that have changed today’s environment for MLPs, making it more different to be an MLP than it was just five years ago.

First, the state of the MLP capital markets have remained weak. Despite IDR restructurings, equity capital remains very expensive as the MLP market has failed to experience much of a rebound, keeping equity costs elevated. While the debt funding environment has somewhat improved, the market remains weary of MLPs increasing their leverage levels, making management teams hesitant to rely on the debt markets. This has perpetuated the need for MLPs to self-fund their growth and as a consequence become more conservative with their distribution policies.

Second, the Tax Cuts and Jobs Act (TCJA) reduced the effective tax differential for the MLP structure compared to C-Corps from 8.4% to 7.2%. While MLPs retained most of their tax benefits relative to the C-Corp structure, tax reform made it less punitive to be a traditional c-corp, particularly when considering other factors like the ability of certain c-corps to now more aggressively depreciate capital expenditure (CapEx) spending.

Third, the unexpected FERC ruling in March disallowing the recovery of an income tax allowance (ITA) for MLPs on regulated cost-of-service pipelines meant that all else equal, a FERC regulated cost-of-service pipeline could collect higher tariffs under the C-Corp structure than it could as an MLP.

Ultimately, we believe these three factors have led to structural uncertainty surrounding MLPs, which has contributed to MLP units remaining at depressed levels despite surging energy production, a sustained period of higher oil prices, and a more stable business model.

To this end, there have been a number of MLPs that have sought to eliminate the uncertainty and undergo c-corp conversions. Prior to the FERC ruling, in 2018, one midstream MLP rolled-up into its C-Corp parent, ArchRock Partners (APLP). Since the FERC ruling, Tallgrass (TEP), Williams (WPZ), Spectra (SEP), & Enbridge (EEP) have announced they will fold into their C-Corp structured parent. Numerous other MLPs have stated that they are actively evaluating their structure, which is industry code for: waiting to see what happens to the valuations of MLPs that already announced conversions. We believe the market ultimately could reward these conversions due to reduced uncertainty surrounding corporate structure, greater flexibility, improved governance, and easier access for institutions. As such, we expect this conversion trend will accelerate in the near-to- medium-term as management teams monitor market reception to the roll-ups and attempt to structure any potential C-Corp conversions in a way that minimizes the taxable impact to unitholders.

Energy Infrastructure: The New Energy Infrastructure Landscape

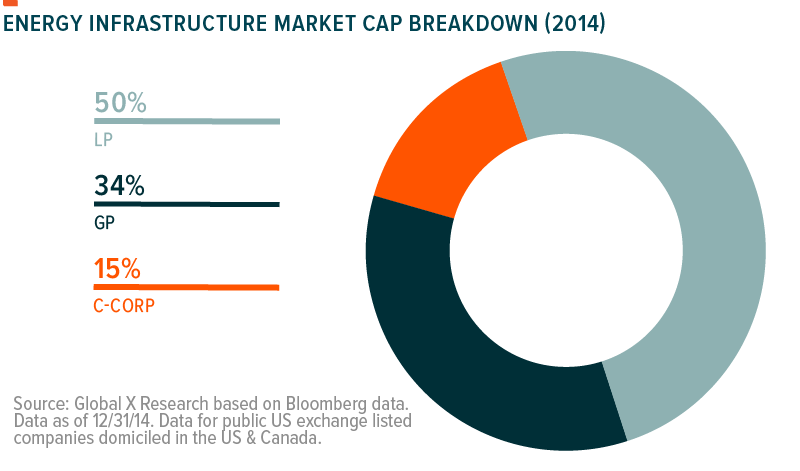

The MLP acronym was used synonymously to describe midstream energy infrastructure in the earlier part of the decade as virtually all US energy companies looked to capitalize on the MLP boom by dropping their midstream assets inside the MLP structure. Often, there would be an accompanying publicly traded General Partner (GP) that had IDRs allowing investors to play either the MLP structure in an effort to maximize yield potential, or the GP that was expected to have greater total return potential due to the IDRs. For reference, the chart below shows what the infrastructure landscape looked like in terms of market cap breakdown at the end of 2014. The space was heavily dominated by the General Partner/Limited Partner structure, with the lone pure US midstream C-Corp company being Kinder Morgan.

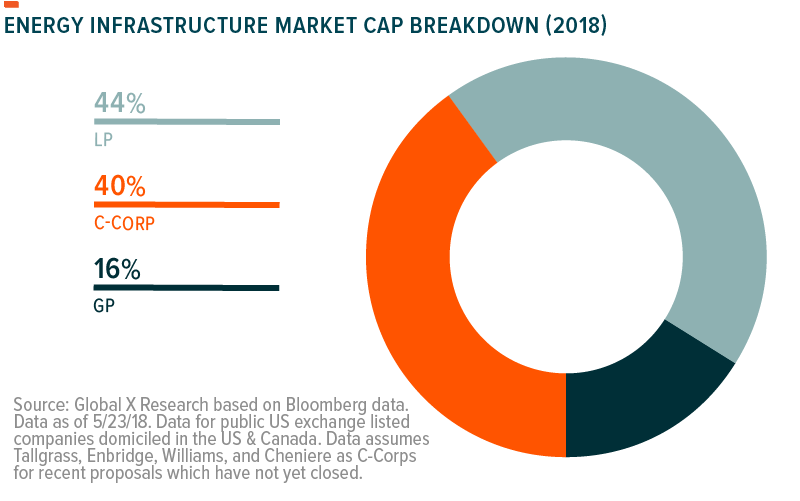

Today, that LP/GP story is beginning to fade away as midstream companies begin to embrace the more simplified C-Corp structure. Assuming all the prior transactions discussed above close, nearly 40% of the US listed energy infrastructure market cap will comprise of C-Corps, a steep jump from just 15% at the end of 2014.

We believe that this trend towards the C-Corp structure is unlikely to end here. Over the coming months, many MLPs will be watching to see what the market reception is for these conversions. This certainly won’t mean all MLPs will cease to exist, but the MLP industry is going to change. With some MLPs forming committees to evaluate their structure (Antero Midstream), others stating they’re looking to simplify their corporate structure (Energy Transfer), and some outright stating the MLP vehicle is no longer an effective financing vehicle for them (TC Pipelines), we believe MLP indexes are likely to become more concentrated than they were before as MLPs either abandon the structure or roll into their parent in an effort to improve their balance sheet while maintaining their partnership tax status (NuStar).

All these changes beg the question, how does one invest in energy infrastructure going forward? We believe it depends on what type of an investor you are. If you’re an income-oriented investor, the MLP structure may still be the preferred solution as MLPs have historically displayed higher yields with potential tax benefits that the C-Corp structure does not offer. But if you’re looking to invest in the energy infrastructure theme and capture a more complete exposure set of the industry, you may want to begin exploring solutions on how to capture exposure to that C-Corp segment as well, which pure MLP indexes will miss. We believe energy infrastructure is in a transition phase, with the C-Corp structure becoming an increasingly important part of the industry and asset class.

Related ETFs

MLPA: The Global X MLP ETF invests in some of the largest, most liquid midstream Master Limited Partnerships (MLPs).

MLPX: The Global X MLP & Energy Infrastructure ETF is a tax-efficient vehicle for gaining access to MLPs and similar entities, such as the General Partners of MLPs and energy infrastructure corporations.

Please click the fund names above for current fund holdings. Holdings are subject to change.