Rohan Reddy

Rohan ReddyQ2 began near the nadir of the global economic shutdown, as governments around the world sought to contain the rapid spread of COVID-19. Yet by the end of the quarter, some success in containing the virus allowed for certain economies to begin the re-opening process. Risk assets globally benefitted from this re-opening, along with massive monetary support from central banks, but the energy sector in particular benefitted from a path towards a more normal economy after a devastating Q1. In this quarter’s MLP Insights, we discuss the catalysts behind the recent positive move and key factors to watch going forward as the global economy begins its recovery, including:

- Energy sector’s Q2 recovery after economic data trough

- OPEC+ deal & rising demand driving a rebound in oil prices

- Declining US production from exploration & production (E&P) contributing to midstream weakness

- Rebalancing of market & attractive valuations may be an eventual catalyst

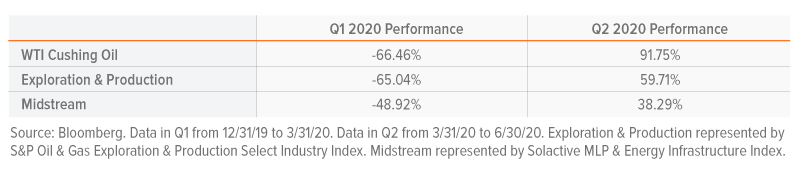

Energy Assets Began Recovery in Q2 After Painful Q1

The first half of 2020 was an unprecedented time in history. Economy-wide figures flashed the reddest of red, with U-6 unemployment jumping to 22.8% in April from 6.7% in December. Q1 GDP in the US fell by an estimated -5.0% annualized rate.1 The World Bank estimates global GDP will fall by -5.2% in 2020 from the effects of COVID-19.2 The transportation and energy segments, which are very sensitive to economic activity, had little insulation from this economic devastation. Global airline passenger revenue kilometers fell by -94% in April year-over-year, and auto sales fell by 48% from January to April of this year.3,4 Oil demand consequently fell over 20% from the end of 2019 through April this year.5

Glimmers of hope appeared by April when governments in Asia announced plans to reopen in phases, followed by similar plans in Europe and ultimately the US. By May, reports from China indicated the world’s second largest economy almost returned to pre-COVID-19 levels of oil demand. Oil prices subsequently rebounded, sparking a recovery in energy-related equities and debt. In fact, oil put up its best quarterly performance since 1990, but only after a traumatic Q1.6

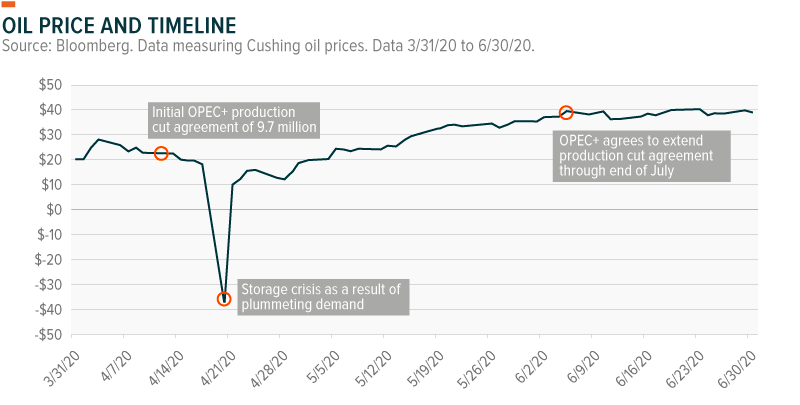

OPEC+ Production Cuts Helped Curb Oil Freefall

Despite contentious meetings to start 2020, OPEC+ came together on April 12th to implement a historic 9.7 million barrel a day (bp/d) cut.7 This was the largest oil production cut ever, eliminating about 10% of global supply. At their June meeting, OPEC+ agreed to extend their production cut agreement through the end of July.8 These cuts played a major role in reducing the global oil oversupply amid curtailed demand, allowing prices to nearly double by the end of the quarter.

Under the surface, the OPEC+ agreement remains fragile. Tensions between Saudi Arabia and Russia from earlier this year are still at risk of flaring up. In addition, smaller OPEC+ nations like Iraq, Nigeria, Angola, & Kazakhstan failed to dial back production to agreed upon levels, causing larger countries take on a greater burden of supply cuts. These smaller nations agreed to make deeper cuts in the coming months, but further compliance issues could complicate the future of these short-term production quota agreements.

US Production Comes Offline

The free fall in oil prices through April forced Exploration & Production (E&P) management teams to re-evaluate capital allocation & operational plans. With oil falling from $60 at the start of the year to under $25 by mid-March, many wells became unprofitable. Storage capacity quickly filled up as companies rushed to store production as demand collapsed. These dynamics forced E&Ps to take production offline through shutting wells.

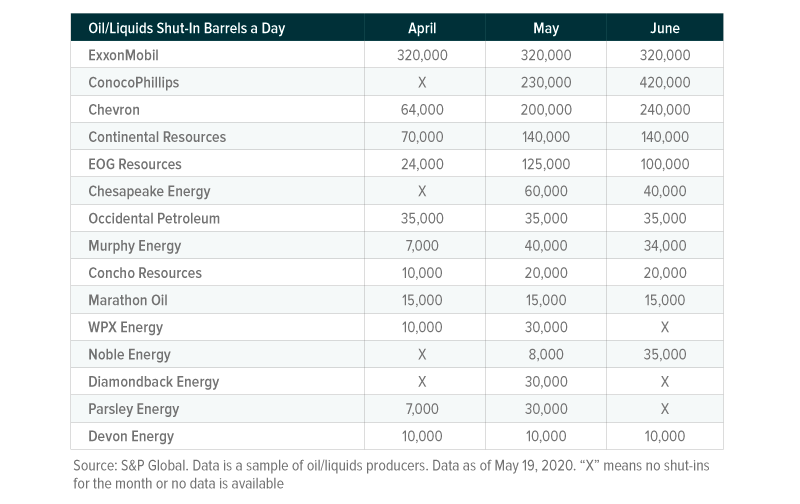

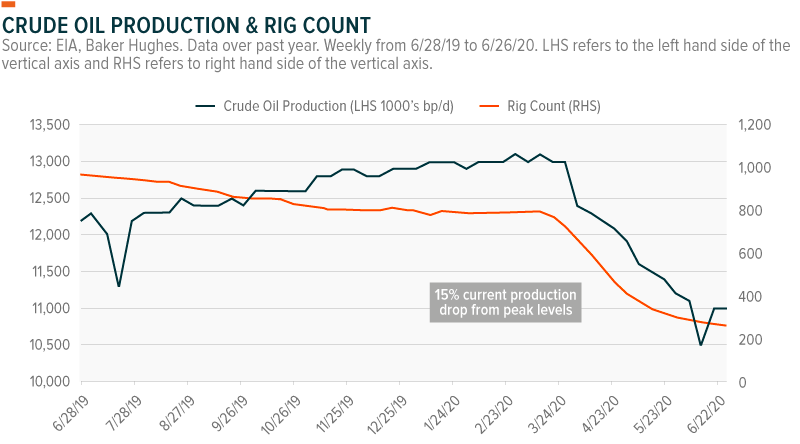

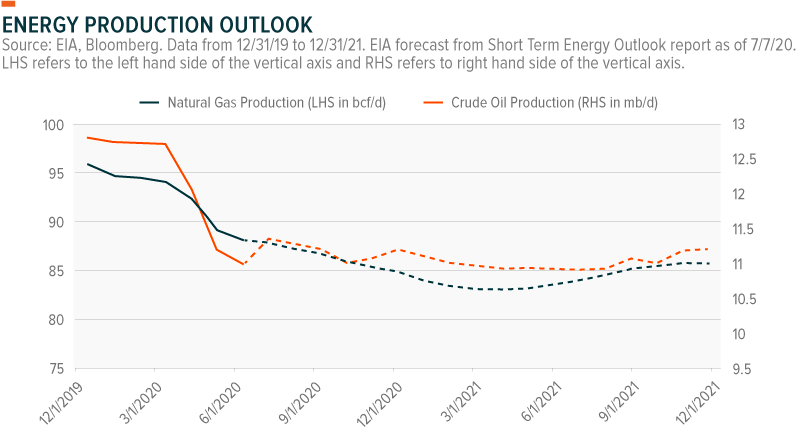

Shutting an oil well is not a decision to be taken lightly. Production teams need to manage any long-term damage to the well, and it can be costly and time consuming to ultimately restart a well’s production. E&Ps often consider this a last resort, but with oil and gas prices reaching historic lows, there was little choice. As wells shut, US crude oil production fell, dropping nearly 20% from peak to trough. Below is a sample of shut in wells by oil & liquids producers, as well as a look into how oil production and the rig count changed.

For other E&Ps, shutting and waiting wasn’t an option, with twenty three declaring bankruptcy through June.9 The most notable bankruptcy took place in late-June, with fracking pioneer, Chesapeake Energy, falling under the pressure of a $9 billion debt load. The Energy sector default rate is expected to reach 17% through the end of 2020, according to Fitch, representing roughly $33 billion in defaulted energy debt.10 This would rival only the 19.7% default rate for the sector in January 2017.11

With oil prices recovering in May and June to around $40/barrel, it’s unclear how quickly E&Ps will bring production back online. Some E&Ps may cautiously wait for sustained periods of higher oil & gas prices before re-activating wells, given the difficulty of opening and closing them. Yet at the same time, E&Ps are production-based businesses, and if prices rise to profitable levels, it may be hard for many to withhold production, particularly as they continue to service their debt.

The EIA predicts US oil production will be largely range-bound for the next eighteen months at levels 10-15% lower than December 2019. Lower production may help stabilize oil prices, but could present a headwind for midstream entities that are compensated for transported and storing commodities by volume.

Implications for Midstream

Despite the strong recovery in midstream securities during Q2, they remain in negative territory for the year. E&P bankruptcies, shut-in wells, and reduced rig activity all ultimately reduced production, hurting midstream companies that transport and store crude and natural gas.

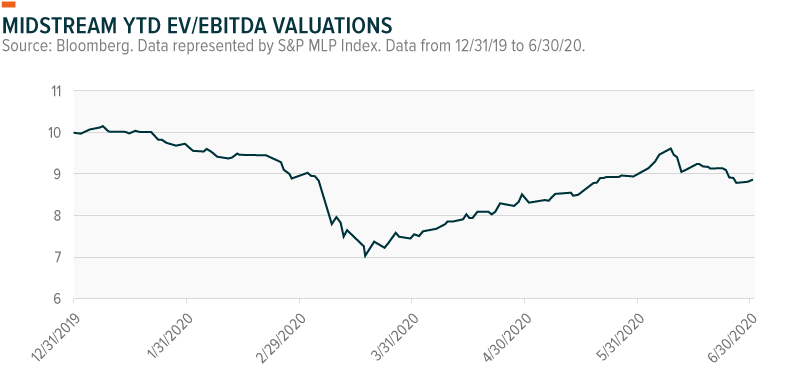

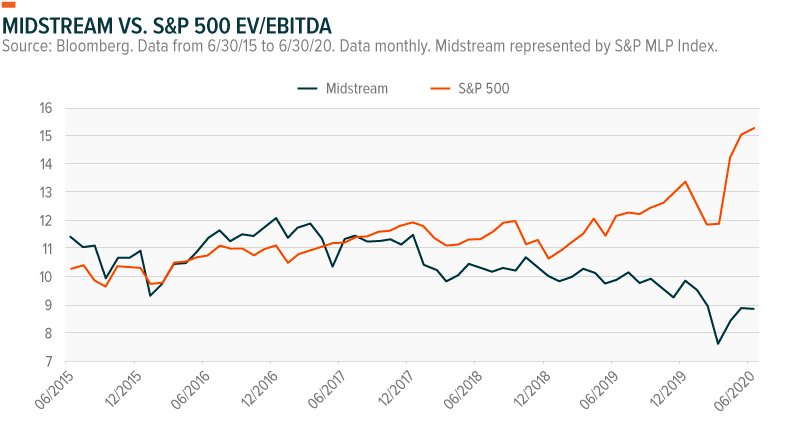

Revenues reported by midstream companies do not yet reflect this pullback. YoY sales only fell by -1% last quarter. But given lower output in recent months, future earnings releases are likely to show decreased revenues. Analysts are forecasting a QoQ decline of -12%.12 This is in-line with the macro picture and explains why many MLPs pre-emptively cut distributions in Q1. Below is a valuations picture of the asset class’s EV to EBITDA (Enterprise Value to Earnings before Interest, Taxes, Depreciation, & Amortization).

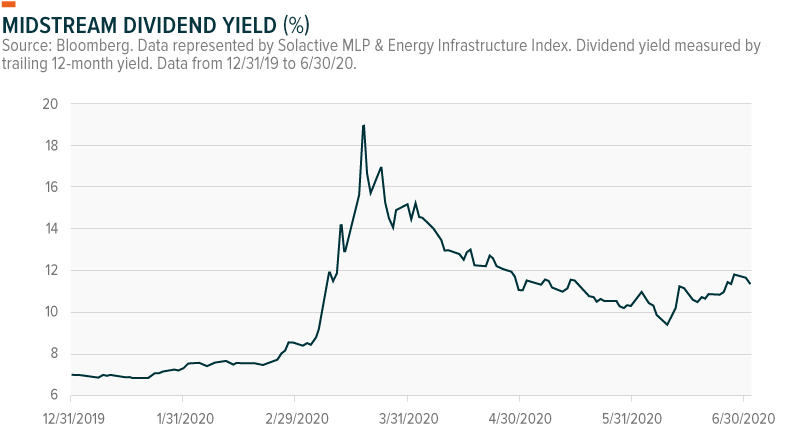

The Q1 distribution cuts, combined with Q2 price recovery, caused dividend yields to retreat from their extreme levels, but remain well-above their starting point for the year.

Outlook For Midstream

The three factors most important to MLP and midstream energy prices are COVID-19’s impact on oil demand, OPEC+ supply agreements, and the resilience of MLP customers – E&P companies.

Covid-19’s impact on demand: reopening economies around the world will slowly revive oil demand. Gasoline usage would rise as commuters return to work and commercial demand for crude would pick up as factories return to full capacity. A smooth reopening process may result in a quick V-shaped recovery in energy demand, providing a catalyst to propel midstream further. But major setbacks in the reopening process, due to more outbreaks, would continue to suppress crude usage. In such a scenario, E&P’s may face further challenges, resulting in greater production cuts or bankruptcies, keeping pressure on the midstream space.

OPEC+ supply agreements: The OPEC+ production cut agreement runs through the end of July. By late summer, we envision OPEC+ beginning to taper their production cuts to meet rising demand and stabilized oil prices. Many OPEC+ countries rely on full oil production to balance their budgets, and will grow impatient. However, downside risk remains if OPEC+ heavyweights, Saudi Arabia and Russia, resume their aggressive tactics to compete for market share and keep a lid on oil prices.

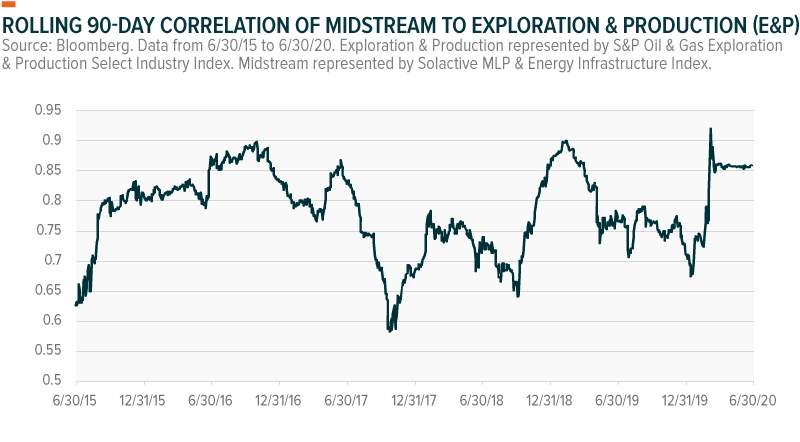

E&P strength: E&Ps are an important customer for midstream, so this period of turmoil led to heightened correlations between E&P and midstream entities. Despite a handful of bankruptcies, major E&P players tend to be surprisingly resilient, surviving oil crashes in 2008 and 2016. In addition, breakeven fixed costs for many E&Ps continue to fall lower driven by technological innovation, low interest rates/government loans, and the ability to renegotiate with suppliers. Capital discipline remains a critical focus to avoid further bankruptcies. Geopolitical implications make the Energy sector strategically important to the United States, meaning there could be further support from the government if oil prices become critically low again.

While there may be localized COVID-19 outbreaks for months to come, a gradual reopening across the global economy and a disciplined OPEC+ keeping supply constrained should be enough of a catalyst to support higher oil prices and reduce E&P risks. In this ideal scenario, midstream valuations look very appealing. Despite rallying almost 40% this past quarter, valuations remain near historic lows, while broader market indices are near recent valuation highs.

Outside of that ideal scenario, other catalysts may help spur a recovery in valuations, like institutional investors taking advantage of low valuations to make acquisitions. Berkshire Hathaway’s natural gas asset purchase for $9.7 billion is one such example that could instill greater confidence in midstream. There is a record amount of dry powder in infrastructure funds, totaling $212 billion, which could be deployed for further energy opportunities.13

For income investors, we believe the majority of distribution cuts in the midstream space already occurred in Q1 or the beginning of Q2. Yields still remain well above historical averages, but distribution coverage ratios are at 2.3x, up from 1.5x in Q4 2019.14 While these figures may come down as earnings reflect lower revenues, overall it signals strong support for distributions at these levels, even with MLPs yielding over 11%.

For valuation-conscious investors, few areas of the market appear as inexpensive as the Energy sector broadly, or midstream entities in particular. Such low valuations imply the market is pricing in widespread bankruptcies, which seem unlikely at this juncture. While the Energy sector will look different than in previous years, it remains a critical industry for the US economy and its geopolitical influence, giving it special implicit protections from the government. A renewed focus on the fundamentals and not the gloom and doom nature of Energy could improve share prices, particularly if institutional investors are at the forefront of this charge.

Related ETFs

MLPA: The Global X MLP ETF invests in some of the largest, most liquid midstream Master Limited Partnerships (MLPs).

MLPX: The Global X MLP & Energy Infrastructure ETF is a tax-efficient vehicle for gaining access to MLPs and similar entities, such as the General Partners of MLPs and energy infrastructure corporations.

Please click the fund names above for current fund holdings and important performance information. Holdings are subject to change.