Rohan Reddy

Rohan ReddyA link to the latest Global X MLP Monthly can be found here.

The Energy sector carried its momentum from the end of 2020 into 2021 and ended Q2 as the S&P 500’s best performer after returning a staggering 45.61%.1 Importantly, oil and gas production stabilized after a tumultuous COVID-19-induced period for producers. Certain regions face a slowed reopening as they struggle to get ahead of the virus, but major consumption centers have the global economy moving in the right direction, which bodes well for the industry. For midstream companies, the unfolding recovery led to stronger Q1 earnings and sparked mergers and acquisitions (M&A). Also renewing investor interest in the segment was the rotation from Growth to Value stocks and rising bond yields. All told, we believe midstream’s multifaceted use cases make it particularly compelling in the current environment.

Key Takeaways

- Energy demand is rising as major economies around the world engage in the re-opening process, and significant improvements in economic data is now beginning to reflect that reality.

- US energy production is expected to increase going into 2022, led by natural gas production.

- Strong midstream earnings and a broader shift to cyclical assets creates an ideal outlook for midstream companies heading into the second half of 2021.

Oil & Gas Demand Expectations Rising with Re-opening On Track

Much of the global economy has turned the corner on the pandemic after vaccination rollouts, but secondary bouts of COVID-19 and its variants are concerns in parts of Asia and South America. India’s recent COVID spike is the most prominent example, being one of the top 10 largest economies in the world. However, the implications for the global re-opening timeline appear modest.

Setting the stage for a smoother re-opening in the second half of 2021 is the vaccination charge led by North America and developed Europe. As such, the International Energy Agency (IEA) now estimates that oil demand will reach pre-pandemic levels by the end of 2022. Demand in 2020 declined by 8.6 million barrels a day (mbpd), but a 5.4 mbpd recovery is expected for 2021 and another 3.1 mbpd increase for 2022.

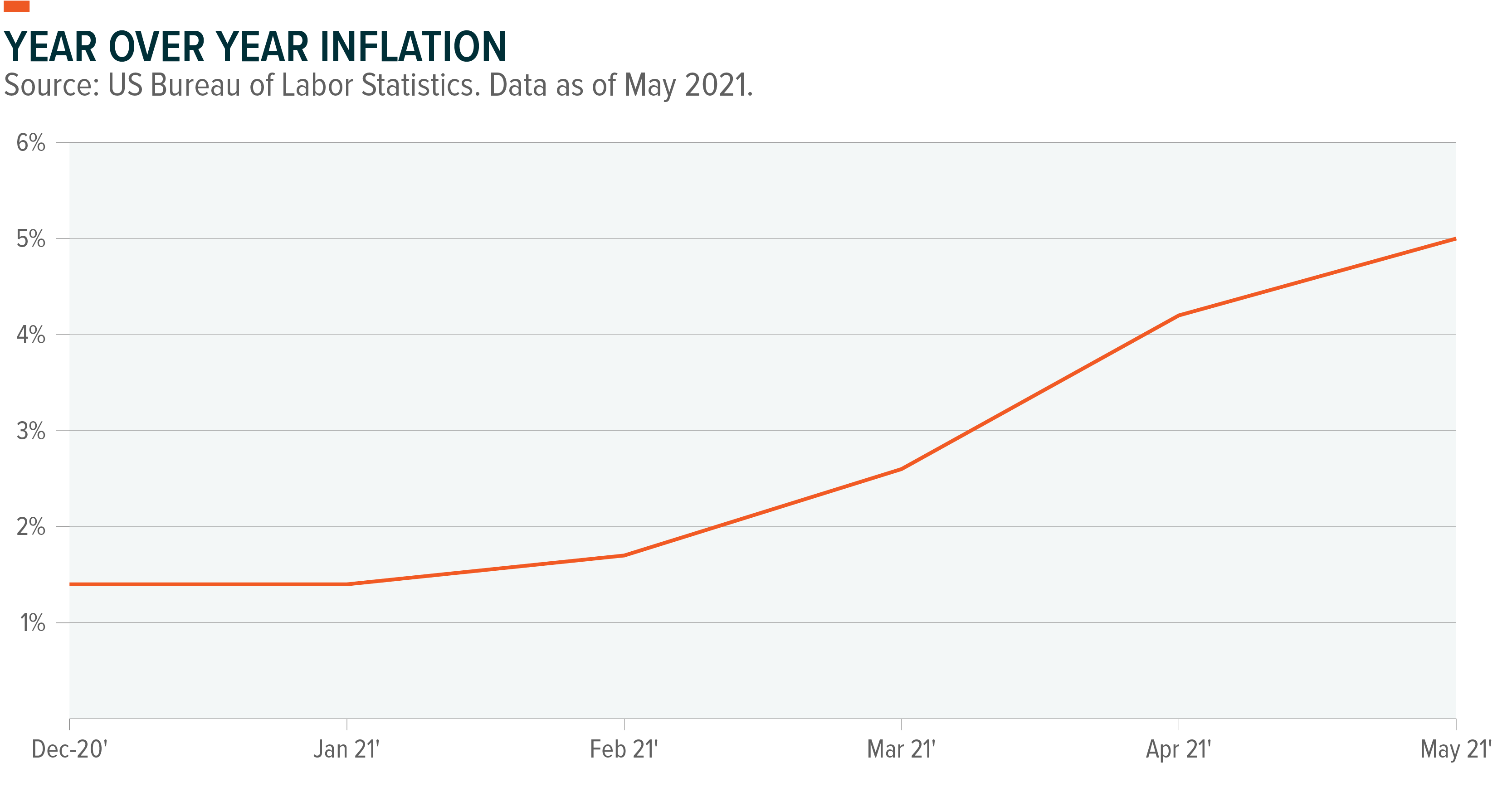

Most notably, the US is progressing towards a fully functioning economy with virtually every US state fully re-opened already or with plans to do so by July. Important for the US oil and gas industry is that demand expectations are rising and economic data is beginning to reflect this reality. In May, daily average gasoline prices crossed $3 and inflation hit 5.0%, peaking after persistent sub-2% levels.2

US Energy Production Expectations Higher

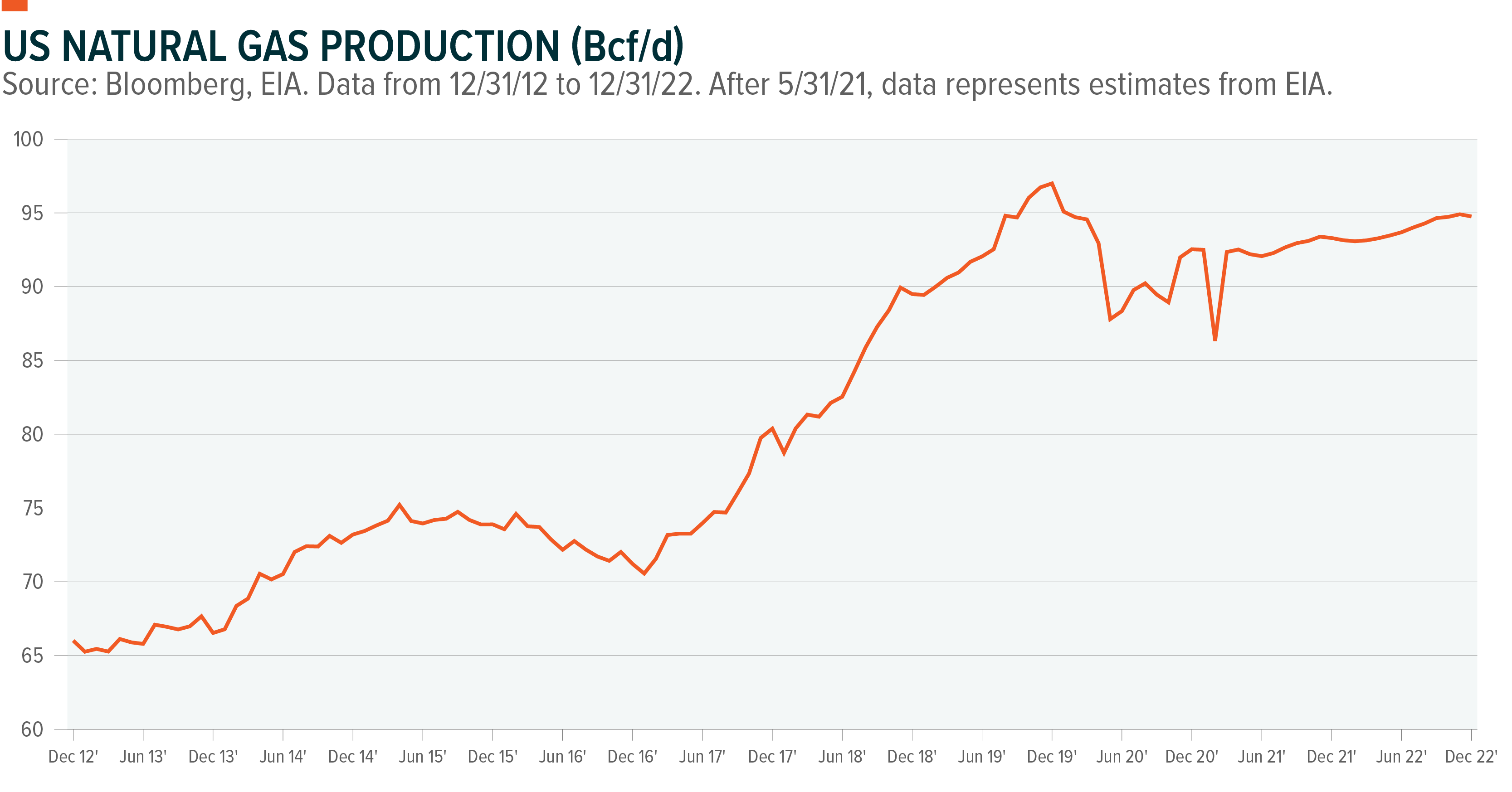

US oil production has been steady around 11 mbpd for most of 2021 given producers’ conservative capital allocation strategies towards new capital expenditure (CapEx) spending. However, amid higher prices and greater economic certainty, production is expected to increase steadily toward the end of 2021 and through 2022. Natural gas production growth is expected to outpace oil production, which is noteworthy because gas now accounts for 76% of the US midstream industry’s revenue.3 The Energy Information Administration (EIA) expects gas production to reach 93.1 bcf/d in the beginning of 2022, before hitting 94.8 bcf/d by year-end 2022.4 Such production would restart a trend, as production hit a record in December 2019 of 97.0 billion cubic feet per day (bcf/d), before dropping off in 2020 and into 2021 due to the pandemic.

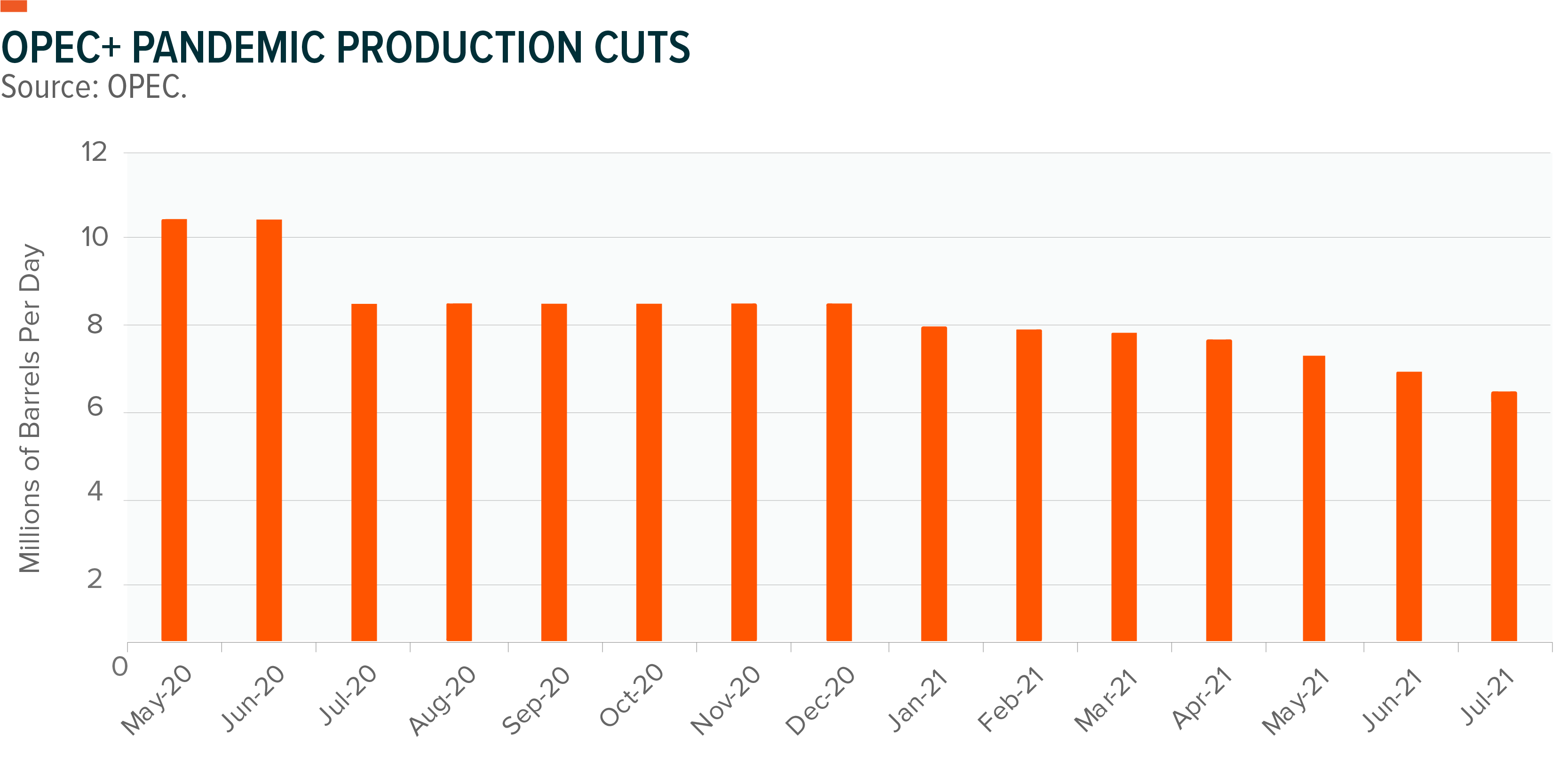

US energy production is important for midstream performance, but the Organization of Petroleum Exporting Countries (OPEC) still has massive influence. In Q2, the oil cartel took a measured approach to re-opening by adding 2 million barrels a day in additional supply to the market from May until July. In early June, the cartel reiterated its commitment to that plan, but the pace and current policies show that they understand how sensitive the market dynamics are and that they’re flexible. Even with the increased supply through July, overall supply is still restrained by 5.8 mbpd, compared to proposed cuts of 9.7 mbpd originally.

The US is not part of OPEC+’s production curbs, so domestic producers can still make market-driven production decisions. OPEC+’s approach isn’t likely to be permanent, but at a minimum it allows US producers to get comfortable with more aggressive production strategies at these higher commodity price levels.

Energy Sector Consolidation a Positive for Midstream

The commodity rally is accelerating at a faster-than-expected pace in 2021, particularly inflation-sensitive commodities like oil. A byproduct of the rally is that it’s accelerating M&A activity, which should be largely positive for midstream because it reduces the number of smaller junior producers and improves operational scale in a capital-intensive industry. Ultimately, M&A can also lead to value creation for shareholders. Most deals are now completed in share-for-share exchanges, allowing acquisition companies to retain upside potential.

Fewer smaller E&Ps after this consolidation wave likely means less associated higher yield credit risk compared to pre-consolidation efforts. Also, bankruptcy risk can be a challenge for smaller E&Ps during down periods, but consolidation improves the viability of these companies across economic cycles.

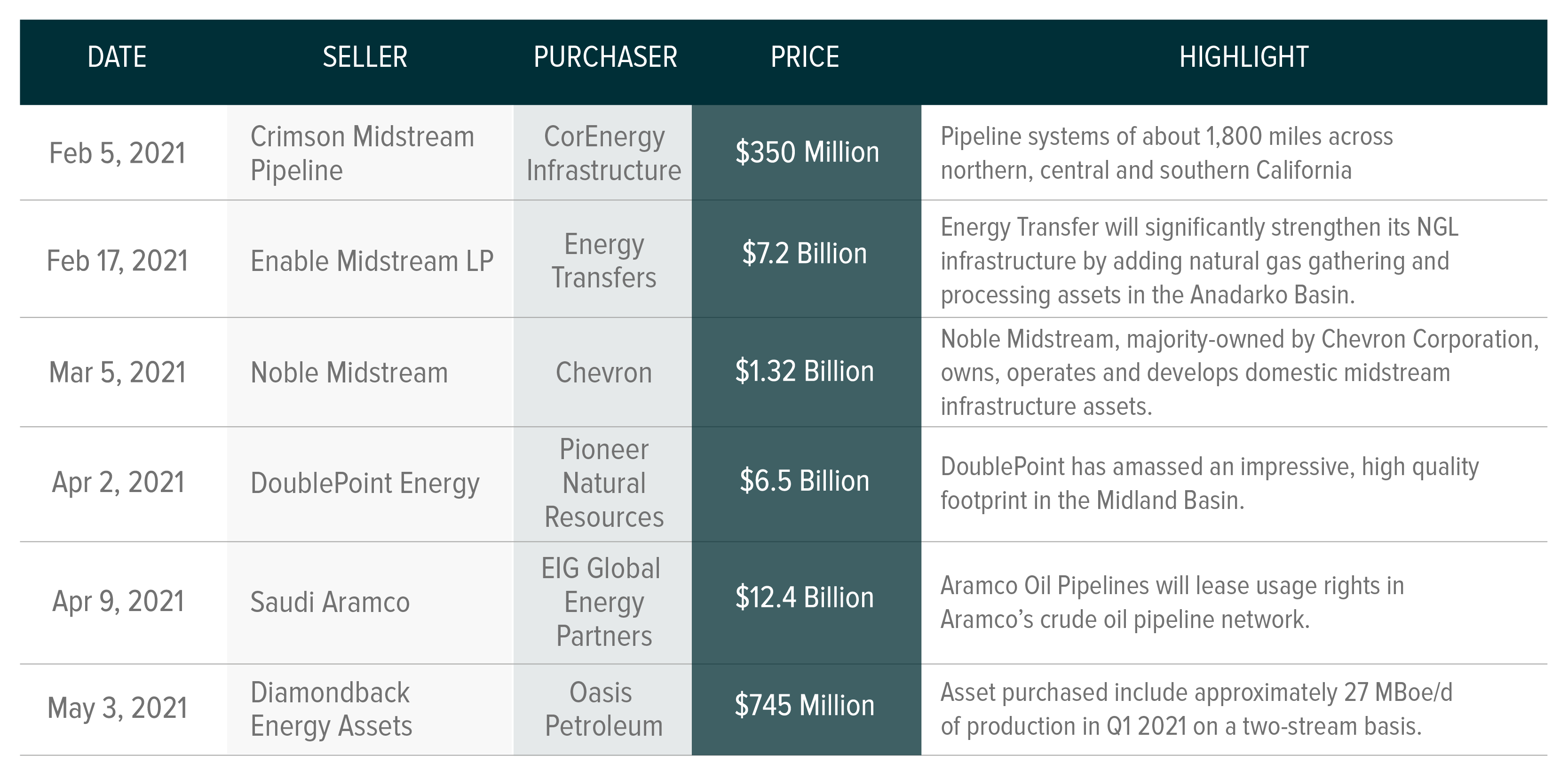

The table highlights major transactions completed so far this year, some of which are significant in value, illustrating deal confidence in this environment.

More Tailwinds for Midstream: Strong Earnings, Shift to Value, Rising Rates

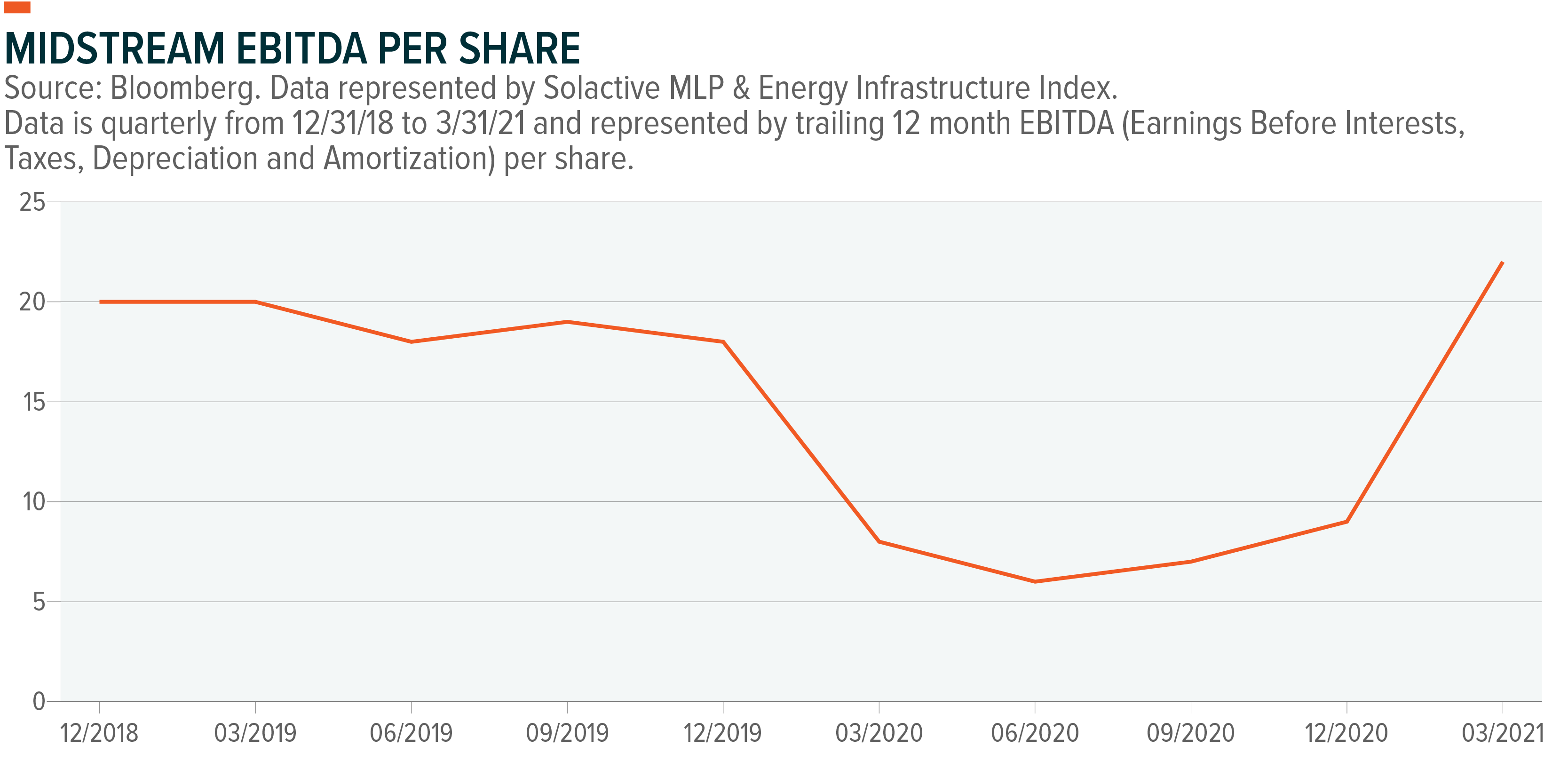

MLP & midstream earnings were strong in Q1 and many beat earnings estimates. Of the 24 midstream companies in the Solactive MLP & Energy Infrastructure Index, 16 beat estimates, 6 met them, and only 2 fell short.5 Earnings expectations for cyclical assets were naturally higher than last year, but midstream’s Q1 showing was impressive amid the global reopening.

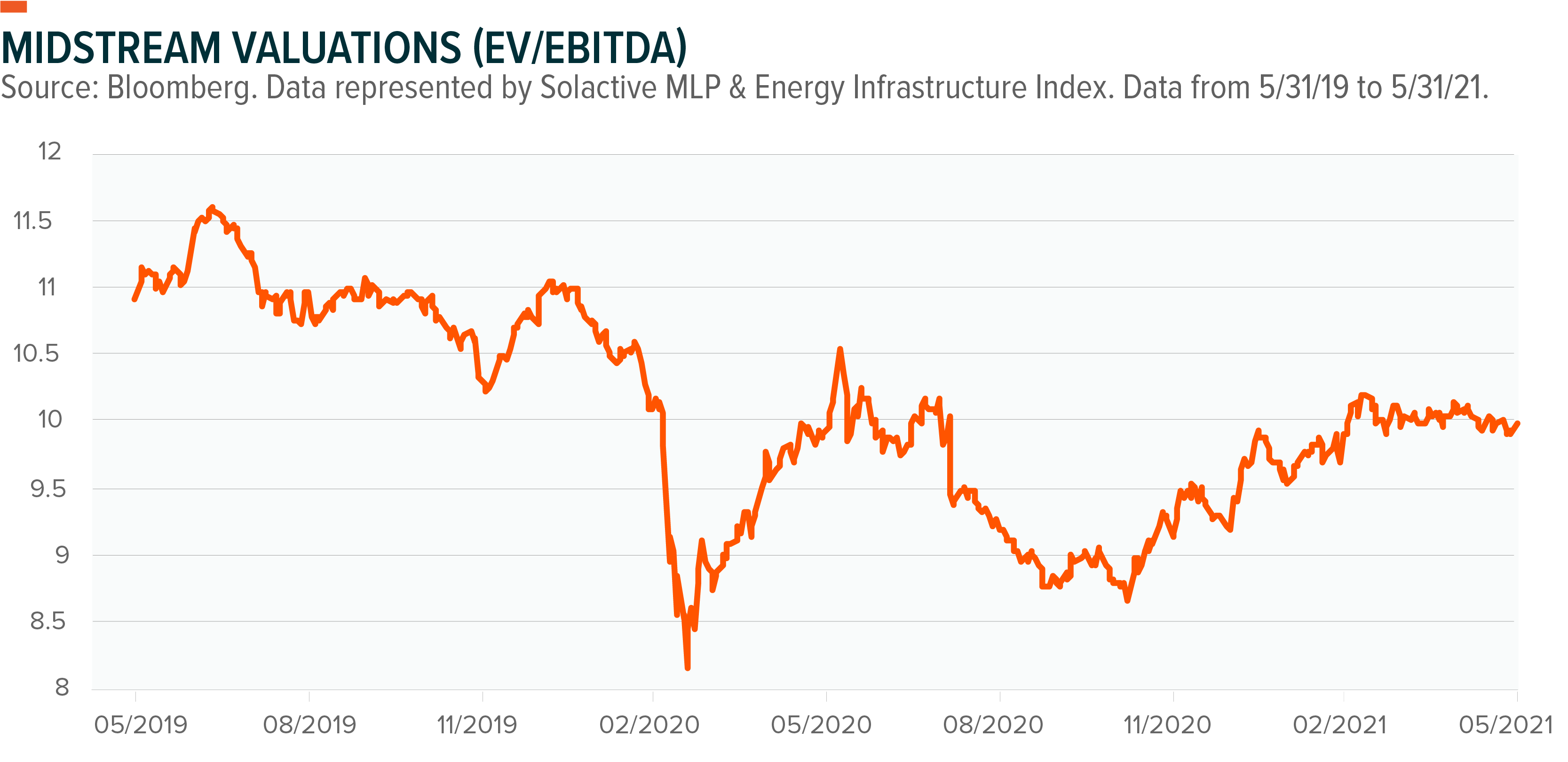

Even though midstream rallied 34.33% through end of May, the asset class still traded at just a 10.0x forward Enterprise Value (EV)/EBITDA compared to 9.2x multiple to start the year.6 For investors, we believe there is limited risk of excessive valuations because midstream hasn’t even reached pre-pandemic valuation levels yet that were in the 10.5-11.5x range.

The broader Energy sector often falls into value indexes, as the energy complex is capital intensive, cyclical, and relatively low growth. Therefore, the recent shift in leadership from Growth to Value has helped midstream companies. The Value index was up 17.44% this year through the end of May, compared to just 6.10% for Growth.7 The Value-to-Growth divergence has been significant, given that Value underperformed Growth by a cumulative -234.62% from 2011 to 2020, or by an annualized -7.12%. Value could remain in favor during the re-opening economy after cyclical equities were battered during the COVID-19 pandemic, potentially benefiting midstream.

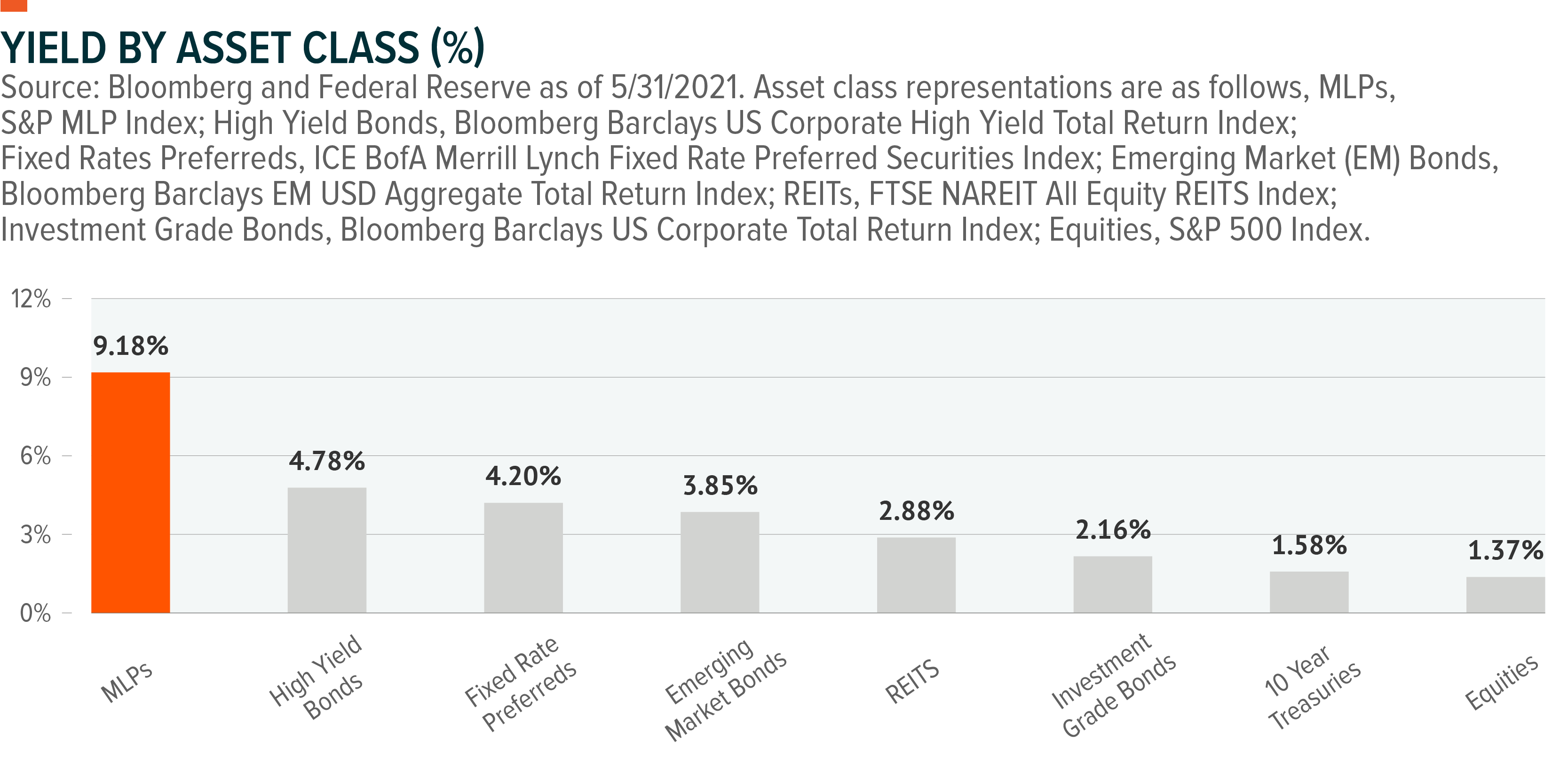

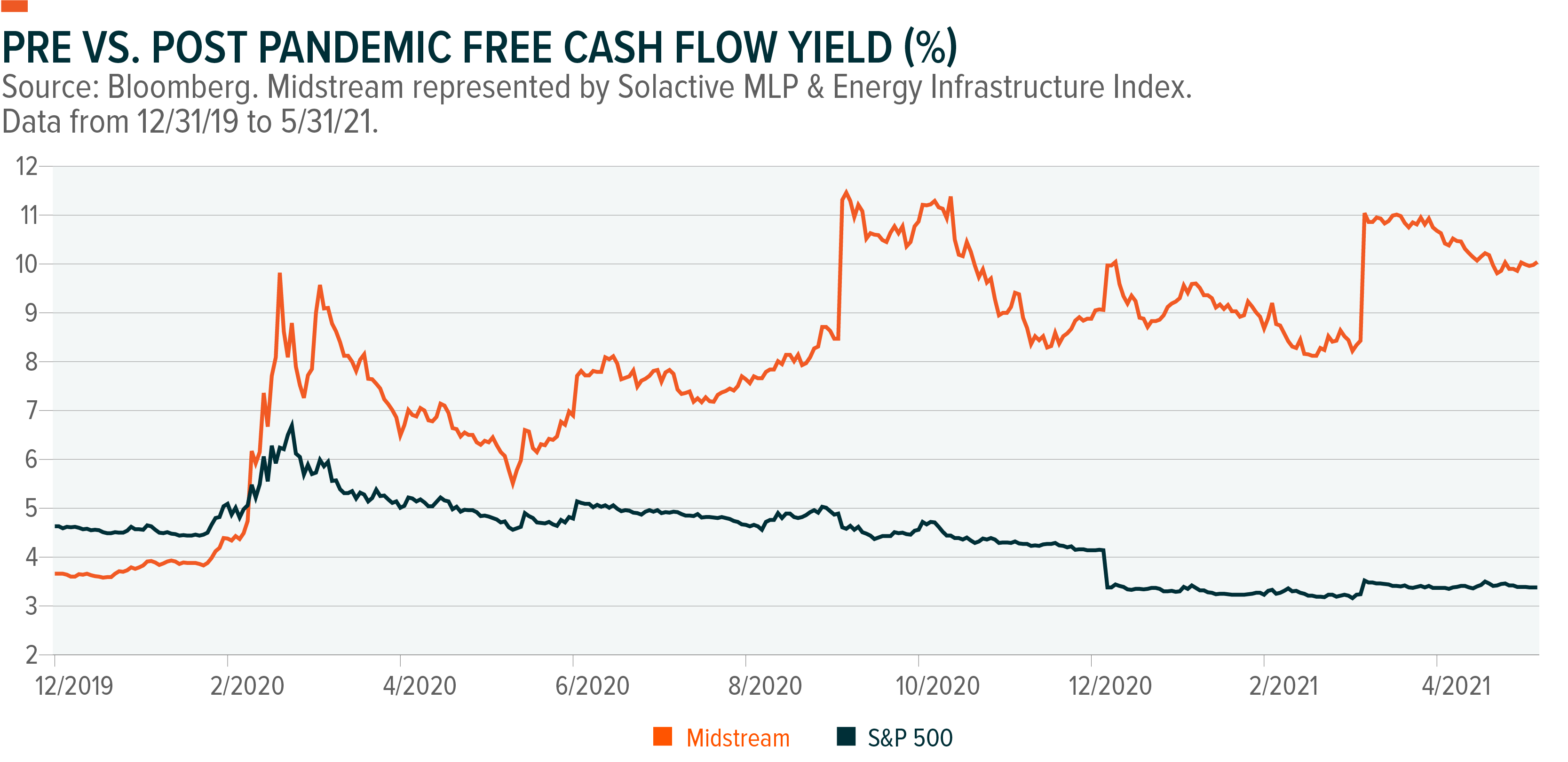

Asset Class Yield Comparison

Rising interest rates and tight credit spreads also strengthen the case for equity in midstream companies. Master limited partnerships (MLPs)’ 9% yield offers greater yield spreads than most other income-oriented asset classes, so even a 100- or 200-basis point rise in treasury bond yields should allow investors to comfortably collect real income. For traditional fixed income, such a rise in rates can potentially wipe out years of returns.

Tight credit spreads signal healthier economic conditions and lower borrowing rates for midstream companies, should they choose to take on additional debt financing or refinance existing debt.

Many investors came into the midstream asset class years ago for the high distributions, so a natural question is whether midstream companies are comfortable raising distributions at this stage. Distributions are still primarily flat after a volatile multi-year period, during which MLPs focused on improving balance sheet strength. Only 4 of the 24 midstream companies in the Solactive MLP & Energy Infrastructure raised their distribution last quarter.

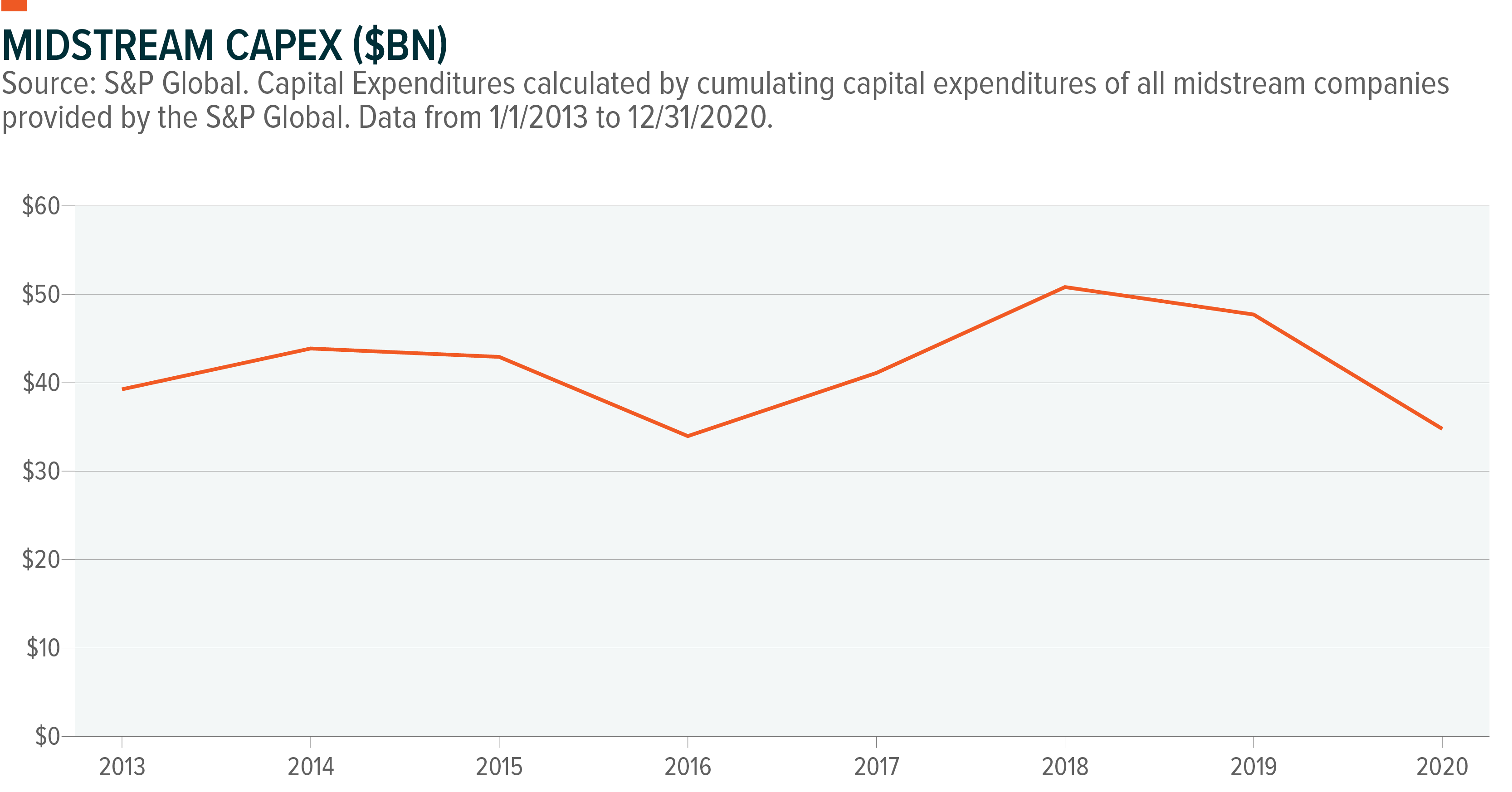

Capital allocation is heavily scrutinized by generalist investors today due to the shift to the self-funding model, meaning less reliance on the capital markets for financing. Unlike past down cycles where capex increased after an initial decline, in Q1 2021 midstream capex declined by -26% versus Q4 2020 levels.8

Capital expenditure (CapEx) reductions led to higher free cash flows as well. Considering midstream outperformed the S&P 500 by 31.40% Year to Date (YTD)9, we believe the broader investor base is also less likely to prioritize distribution growth than in the past.

Conclusion: Multiple Points of Attraction

Renewed demand for oil and gas, the rotation to Value stocks, and the M&A trend contribute to a positive outlook for the Energy sector broadly and midstream companies in particular. More earnings data like we saw in Q1 and significant earnings improvement versus last year should also continue to improve investor sentiment. Because fundamentals have supported the strong rally this year, not just multiple expansion, valuations do not appear excessive either. Also, we expect the portfolio applications that midstream provides to draw longer-term investor dollars in this environment. Specifically, MLPs offered a 9.18% 12-month yield at the end of May. MLP yields were higher than most asset classes and well above the 10-year Treasury’s 1.59%. More broadly, the Energy sector has historically been an attractive option for portfolios positioning for rising inflation.

Related ETFs

MLPA: The Global X MLP ETF invests in some of the largest, most liquid midstream Master Limited Partnerships (MLPs).

MLPX: The Global X MLP & Energy Infrastructure ETF is a tax-efficient vehicle for gaining access to MLPs and similar entities, such as the General Partners of MLPs and energy infrastructure corporations.

Please click the fund names above for current fund holdings and important performance information. Holdings are subject to change.