Rohan Reddy

Rohan Reddy2020 is proving to be another challenging year for the midstream space, as MLPs and energy infrastructure companies seek to weather the storm of low oil prices, slowing US production, and election uncertainty that has weighed on the broader Energy sector. Looking forward, strong fundamentals and improving global growth could present opportunities within the midstream complex. In this quarter’s MLP Insights, we discuss key topics for this space, including:

- Range bound oil prices are pressuring US output

- Long term trends challenge the energy sector

- Midstream fundamentals remaining robust through tough macro environment

- An optimistic case for midstream

Range Bound Oil Prices Are Pressuring US Output

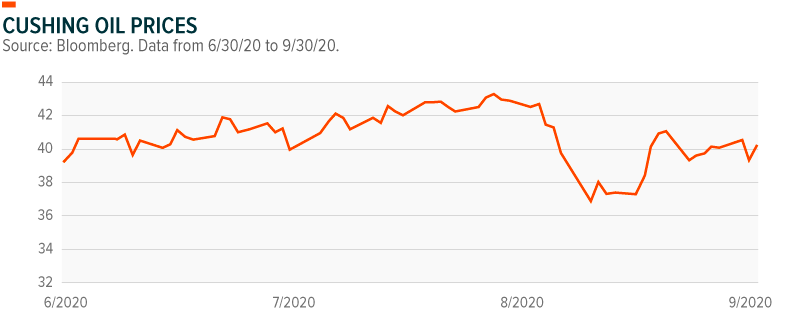

Amid a slow global economic recovery, oil demand has failed to return to pre-COVID-19 levels. Global oil & liquids demand in August stood at 94.3 million bp/d according to the Energy Information Administration (EIA). This represented an increase from the 85.1 million bp/d average in Q2, but still a full 8.2 million bp/d below last year’s August 2019 level. With demand only recovering about half of what it lost during worldwide shutdowns, there’s been few catalysts to push prices higher. The result is range-bound oil prices, zeroing in around the $40/barrel level.

Looking forward, prices could remain in this range well into 2021. Forecasts expect demand to increase by another 6.5 million bp/d next year, but much of this could be absorbed by the phasing-out of OPEC supply cuts.1 The Organization of Petroleum Exporting Countries (OPEC) and its allies cut output by 7.7 million bp/d beginning in August and is expected to keep the curbs in place through year end. Beginning in 2021, cuts are scheduled to taper down to 5.8 million bp/d to offset increases in demand. OPEC+ has recently been flexible on extending output cuts when needed, though.

The prolonged low oil price environment has forced US shale producers to reconsider their capital budgets and output targets. Oil production at its core is tied to the price of oil itself. Producers collect the difference between the market price for oil and the cost to extract it, hedging aside. With oil at $40/barrel, many US energy producers cannot profitability extract the commodity. The result is that US energy production declined from a peak of 13 million bp/d to under 10 million a day in August.

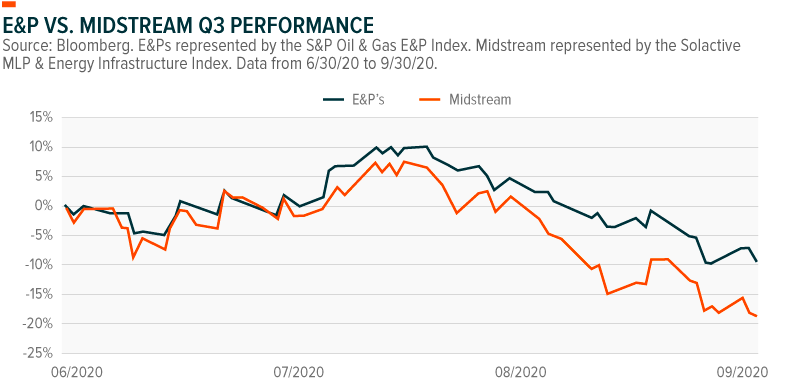

Midstream MLPs and energy infrastructure companies, which primarily benefit from the volume of oil and natural gas they transport and store, suffered amid fears that energy production would continue to decline. Midstream equities were down -9.4% in Q3 versus a -18.8% decline in the Exploration & Production segment. For the year, midstream is outperforming the E&P space by nearly 19% as less direct ties to commodity prices has helped somewhat insulate energy infrastructure.2 Midstream’s value proposition hinges in part on strong US energy production levels. The COVID-19 pandemic and consequent capital expenditure reduction by E&Ps reduced output as oil prices remained depressed.

Long Term Trends Challenge the Energy Sector

The broader Energy sector continues to suffer from short-term issues, like reduced demand from COVID-19, and long-term concerns, like peak oil and ESG divestiture. In addition to the COVID-19-related demand shock discussed above, major oil producers BP and Total suggested that oil demand may have peaked in 2019. With policies around the world to reduce carbon emissions, as well as advancements in alternative energy sources like batteries, total global output could be in a structural decline indefinitely.

Additional pressure on the Energy sector stems from changing preferences and considerations in investment criteria – namely the increased incorporation of ESG data into investment processes. Many ESG funds don’t explicitly divest from the Energy sector, but there is a growing microscope on the ‘E’ within ESG amid the climate change discussion. Estimated ESG investments hit $40 trillion in 2020, nearly doubling in the past four years, which has likely put further selling pressure on the Energy sector.3

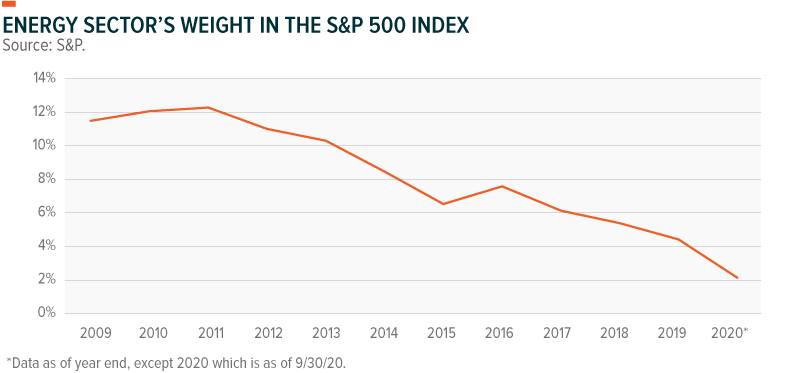

Another technical challenge includes the Energy sector’s shrinking weight in major benchmark indexes. Energy became the smallest weighted sector in the S&P 500 this summer, representing just 2% of the index.4 This means less direct investment from passive investors as well as from benchmark-aware active investors who can avoid the entire sector without risking major tracking error. Additionally, Utilities eclipsed Energy’s weight in the S&P 500 for the first time in history earlier this year. Further, ExxonMobil was removed from the Dow Jones Industrial Average Index this summer after 92 years of inclusion. These changes present a significant headwind for Energy investors due to the significant amount of assets either invested in or benchmarked to those major indexes. There are $11.2 trillion invested in or benchmarked to the S&P 500, for example, with $4.6 trillion directly tracking the index.5 Therefore, the falling relevance of the Energy sector has become a self-reinforcing cycle as investors can increasingly ignore the shrinking industry.

One method upstream exploration and production (E&P) companies are using to adapt to this challenging environment is through consolidation. M&A transactions can increase scale and reduce overhead, which can reduce breakeven prices for mega-producers. The low commodity prices are accelerating this trend. Chevron, for example, announced in July that they are buying Noble Energy, a mid-size shale operator, for a transaction value of $13 billion. In September, WPX Energy & Devon Energy announced they were combining their two entities in a $6 billion transaction. And in October, Pioneer Natural Resources announced it was acquiring Parsley Energy for $4.5 billion.

We believe consolidation will be the norm as E&Ps adapt to this new environment for several reasons. First, if oil demand is generally on the decline then the lowest cost producers globally will be the best positioned to profit. Mega-firms can trim redundant costs and wield greater negotiating power with partners. Second, while the Energy sector may remain much smaller in the aggregate, high concentration in a few names will likely garner more attention from investors. Third, consolidation helps energy producers mitigate certain risks by achieving greater geographic diversity.

Consolidation could have a modestly positive impact on midstream. Lower breakeven oil prices for mega-producers should be a positive for oil output and therefore help midstream volumes. In addition, mega producers have had better credit ratings and risk mitigation, improving counterparty risk for midstream. And while greater negotiating power from mega E&P firms might hurt in contract re-negotiations, midstream’s own consolidation efforts could counteract this force.

Midstream Fundamentals Remaining Robust Through Tough Macro Environment

The challenges facing the Energy sector have not left the midstream sub-segment unscathed, but overall the infrastructure segment has fared better than its Exploration & Production (E&P) counterparts. Despite low oil prices, the toll-road nature of the midstream business model insulated these companies against some of the downside in commodity prices, resulting in meaningful relative outperformance.

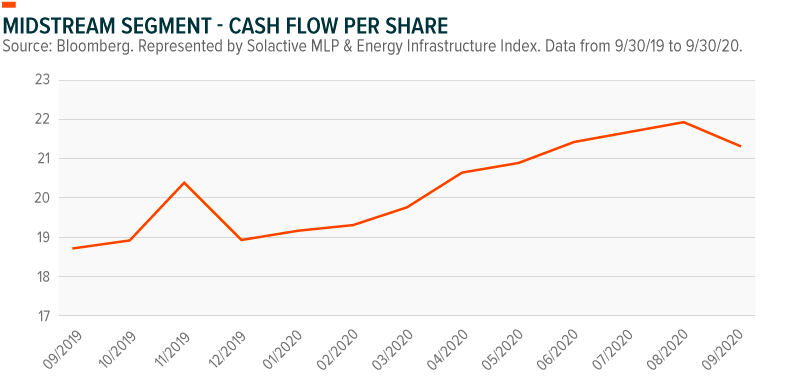

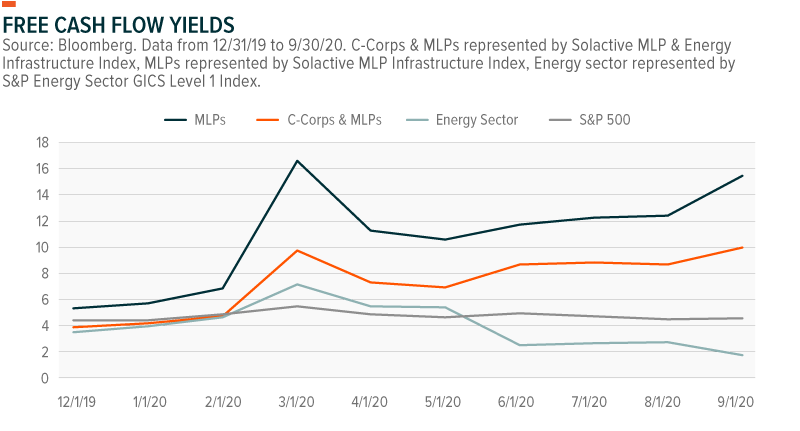

A bright spot among midstream entities was cash flow strength. Despite midstream equity prices falling amid weak Energy sector conditions, the long term nature of midstream companies’ contracts helped to protect the asset class’s cash flows. Midstream long-haul pipeline contracts tend to be protected by 5-10 year fee based commitments. It still gets paid for volumes transported, so midstream is not immune to all the challenges in the sector, but it tends to have more insulation than E&Ps to oil prices. We can see in the chart below that the midstream segment’s cash flows have proven to be fairly robust despite falling oil output.

In the past, many investors used distribution yields to value MLPs given that the structure distributed most cash flow to investors. Yet major portions of the MLP space have converted to the corporate structure and are retaining a much greater portion of their cash flow. Therefore, we believe cash flow yield may be more appropriate to value midstream equities today.

Free cash flow yields in midstream started the year at 3.96%, but rose to 9.98% at the end of Q3.6 Higher cash flow yields can indicate lower valuations and/or greater business model strength.

We can also evaluate midstream’s strength based on the market’s assessment of the segment’s debt versus the other Energy sub-sectors. Equity prices are closely scrutinized, but the credit markets may tell more about the stability of the overall business. With midstream focused on stable cash flows and de-leveraging their balance sheets, the segment’s debt has performed relatively well year to date, down just 3% while E&P debt is down almost 20%.

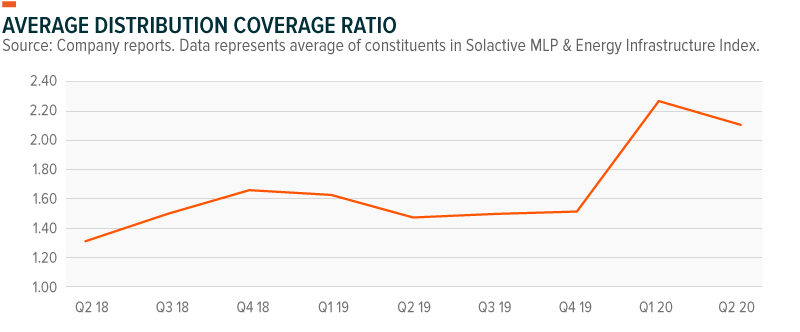

Another area to evaluate is the coverage ratios for midstream, or the ratio of cash flows to distributions. The higher the coverage ratio, the more insulated distributions will be from short term changes in the macro environment. With midstream retaining more cash flows (via aggressive distribution cuts) and cash flows remaining robust year to date, distribution coverage remains high.7

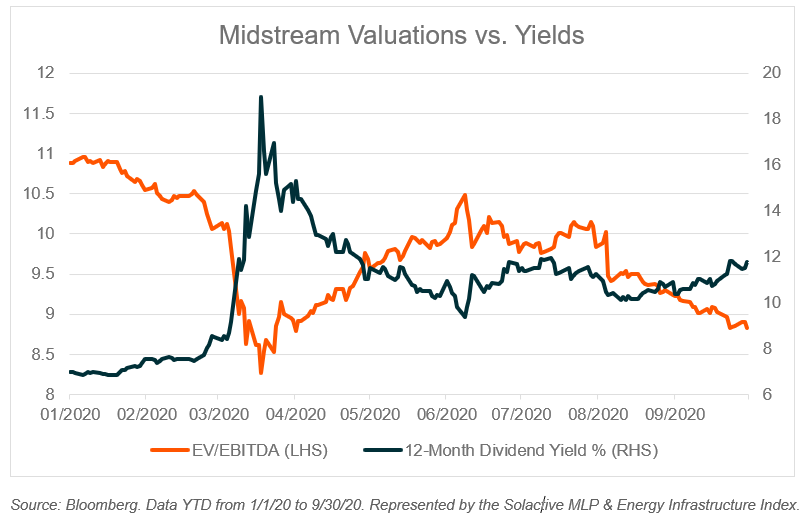

Despite fundamentals appearing relatively strong, midstream distribution yields are hovering well above 10% as equity performance has suffered.

An Optimistic Case for Midstream

Midstream’s low valuations and underperformance versus the broader markets this year reflects the negative headwinds and sentiment the segment faces. Yet there are cases for market enthusiasm towards the space to improve. First, institutional interest in the space remains meaningful as midstream’s long term assets and high yields are attractive characteristics amid a low yield environment. Should institutional investors acquire more midstream assets, it could provide a tailwind for prices across the space. Second, a lower for longer interest rate environment has multiple positive implications for the space including greater demand for high yield assets, lower borrowing costs for midstream entities to pursue capex or refinance, and cheaper financing for M&A deals. Last, the better than expected fundamentals show midstream’s business model robustness amid a challenging commodity price environment. Should oil price remain flat or improve, due to OPEC+’s continuation of output curbs or strengthening demand, the market may exhibit growing confidence in the business structure. Taken together, these optimistic views of the midstream space could reward investors with income in the near term and a rebound in valuations over the medium term.