Global X ETF Model Portfolio Team

Global X ETF Model Portfolio TeamThe U.S. economy is primarily driven by consumers, who contribute to roughly 70% of its economic activity.1 The combination of fiscal stimulus and robust wage growth resulted in a remarkable surge in consumer spending. With the easing of these two factors and high inflation rates, the once robust U.S. consumer is showing signs of strain.

The state of the U.S. consumer most directly impacts the Consumer Discretionary and Consumer Staples sectors. In this piece, we analyzed the health of the U.S. consumer and how to position U.S. sector portfolios within this economic backdrop.

Key Takeaways:

- The state of the U.S. consumer is deteriorating as personal debt levels rise, interest rates remain high, and inflation is elevated.

- In 2023, growthier areas of the market have shined, leading to outperformance in the Consumer Discretionary sector.

- We favor the defensive nature of the Consumer Staples sector as we transition from a late-stage market to an anticipated recession.

Health of the U.S. Consumer

U.S. consumer health has steadily declined over the last few quarters as elevated inflation and high interest rates weighed on savings. Over this period, savings rates deteriorated from over 30% at the peak of the pandemic, to 4.6%, significantly below pre-pandemic levels.2 Spending increased and has remains slightly elevated.3 Household debt has continued to rise, reaching $16.9 trillion at the end of 2022 with non-housing balances hitting a record $4.64 trillion.4

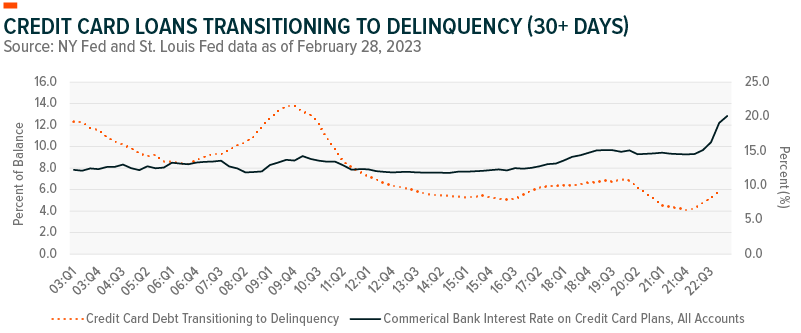

Credit card balances have surpassed the pre-pandemic high and stand at $986 billion, after declining to $770 billion in March of 2021.5 At the same time, credit card interest rates have risen to 20.09%, its highest historical level.6 This has led to a pickup in the credit card loan delinquencies, as seen below. If treasury rates remain higher for longer, we expect credit card rates to remain elevated, potentially increasing delinquencies as payments become larger and tougher to make.

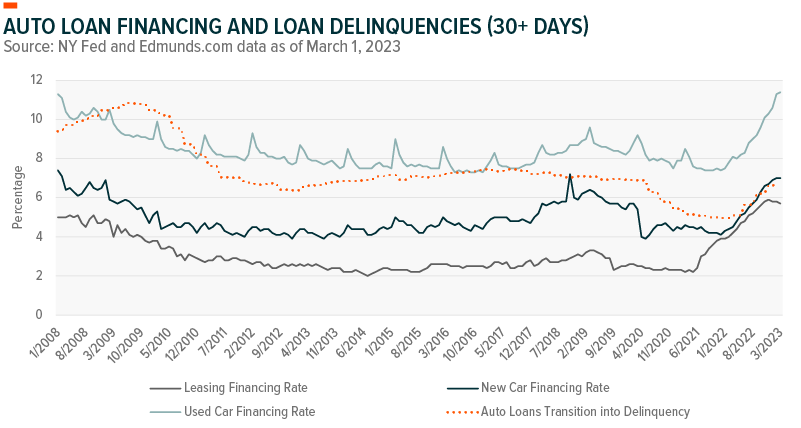

Total outstanding auto loans have also seen a surge, increasing nearly 15% over the past 2 years.7 Interest rates on auto loans, regardless of the type, have grown to levels not seen since 2008. As of recently, similar to credit card loans, there has been a tick up in the percentage of auto loans entering delinquency, as seen below. While this increase in loans is something to be mindful of, most auto loans have fixed rates as opposed to credit card variable rates, therefore the increase in interest rates affects current auto loans more than it would for legacy loans locked in at lower rates. Furthermore, auto demand has weakened, indicating that consumers may have already begun to shift purchasing patterns.

The rising delinquencies indicate that there are cracks forming. Consumers are facing increasing pressures. We expect delinquencies to rise as the ability to pay these large sums of debt becomes more difficult due to slowing wage growth, limited savings, and still high inflation.

Consumer Sectors – Tale of Two Stories

The impact of higher interest rates has begun to have an effect – starting with the collapse of Silicon Valley Bank and Signature Bank. Despite this, markets have rallied, with the S&P 500 up 7.5%.8 As with many of the previous late-stage cycles, growthier market segments have outperformed. This year’s rally has been driven by the hopes that the Fed rate hiking cycle is nearing an end.

The Consumer Discretionary sector benefitted from the rally within growth stocks, outperforming the S&P 500 by about 6.5%.9 The sector’s auto exposure has rebounded significantly this year after tumbling in 2022. On the other side, the Consumer Staples sector has underperformed the S&P 500 by about 5.8%.10 The sector tilts toward value, which has been out of favor.

Positioning in the Current Environment

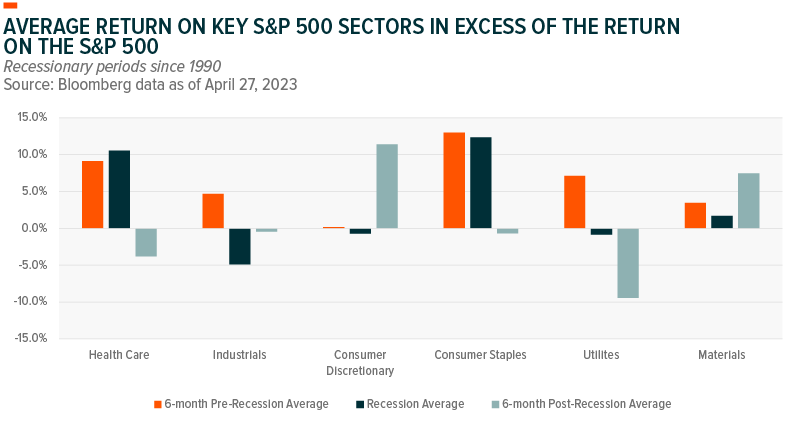

Markets have shifted the prioritization between interest rate sensitivity and economic growth sensitivity. As we shift from late cycle to recession, we favor the defensive nature of Consumer Staples over the cyclicality of Consumer Discretionary. Historically, in recessionary periods, the stability and defensive nature of the Consumer Staples sector outperformed. This was the case in both 2008 and Q4 2018.11

The tightness of the labor market remains at the crux of the consumer’s strength. With renewed focus on corporate efficiency and the rise in corporate bankruptcies, layoffs are on the rise.12 Continuing jobless claims remain low but are on an increasing trend.13 If unemployment continues to increase, this can create a more challenging environment for an already stretched consumer. Couple this with the likely resurgence of student loan payments later this year, the consumer would be forced to redistribute its spending. Spending would likely be limited to essentials, favoring Consumer Staples.

Despite the decline in consumer health, recent signs could point toward peak pessimism. Inflation has been steadily declining, as evidenced by the March CPI and PPI releases.14 The labor market remains tight, with more job openings than workers.15 If consumers are able to weather the tide, they could be better positioned than current expectations.

As illustrated in the chart below, certain sectors have historically been more sensitive to slower economic growth during the four U.S. recessions since 1990. Our sector views table below provides more detail on sector positioning.