Global X ETF Model Portfolio Team

Global X ETF Model Portfolio TeamWe are at a tricky place with fixed income. On October 30th, the Federal Reserve (Fed) reduced short-term interest rates for a third time this year, as expected. Fed Chairman Jay Powell characterized the 25bp move in the benchmark funds rate to 1.50% from 1.75% as a “midcycle adjustment” in a maturing economic expansion. He also indicated that there would be a higher bar for more easing in the future.

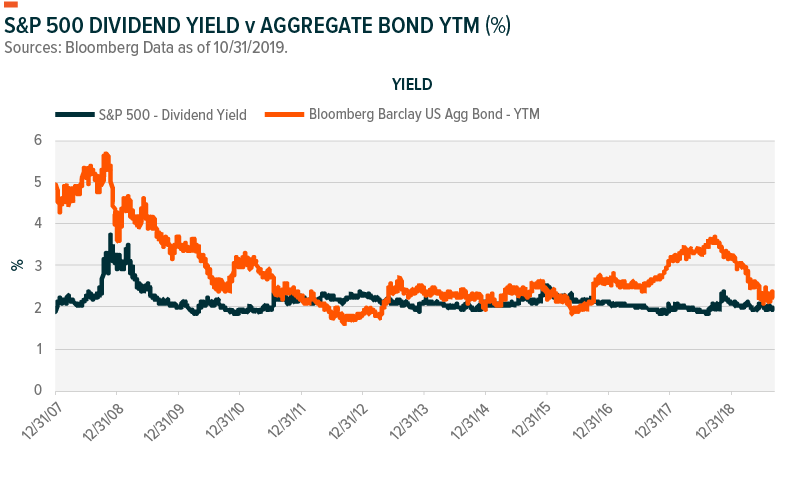

So that leaves us with super-low rates again. Complicating matters is that yields on equities and fixed income are quite close to one another. And when the yield on the S&P 500 Index (1.94%) and the Bloomberg Barclays U.S. Aggregate Bond Index (2.33%) meet, an important question surfaces: Where should investors allocate their “income” bucket?

Fixed income typically offers relative safety and diversification. But this environment’s a little different: yields are so low—almost historically low—and principal could be lost when yields eventually rise. In addition, with fixed income and equity yields so close, it’s reasonable to wonder if the value of equities and fixed income investments decline in tandem when yields turn higher. A breakdown in the historical relationship between fixed income and equity, and for how long that anomaly persists, could leave investors thirsty for yields.

In the equity world, bond proxies like REITS, MLPs and Utilities are among the higher-yielding strategies to consider, and could help income focused investors meet their mandates. But performance likely depends on where we are in the business cycle. Then again, the market remains resilient and risks appear to be softening, particularly with signs of a possible trade deal with China forming.