Technology has played a pivotal role in the evolution of investment analysis. Where an analyst’s toolkit might have formerly only consisted of basic screens or linear regressions, enhancements to computing power and the application of machine learning have accentuated the predictive and explanatory reach of these models through time. Adoption has hinged on the need to quickly and efficiently evaluate large repositories of data, and AI architectures like deep learning have stepped in to help facilitate this process.

The Global X Investment Grade Corporate Bond ETF (GXIG) attempts to leverage this budding technology by bringing the power of AI into the fold. It does so by taking a multi-pronged approach to bond analysis, combining a quantitative factor model with a Deep Neural Network (DNN) to evaluate securities across the investment grade corporate bond universe. Human portfolio managers make the final decisions on GXIG’s portfolio construction, but leveraging AI helps to quickly and efficiently process mountains of data to help inform the managers’ decisions.

Key Takeaways

- Deep learning has transformed the way complex data relationships are analyzed. GXIG’s DNN aims to capture intricate, non-linear patterns within data to inform and guide its portfolio management team.

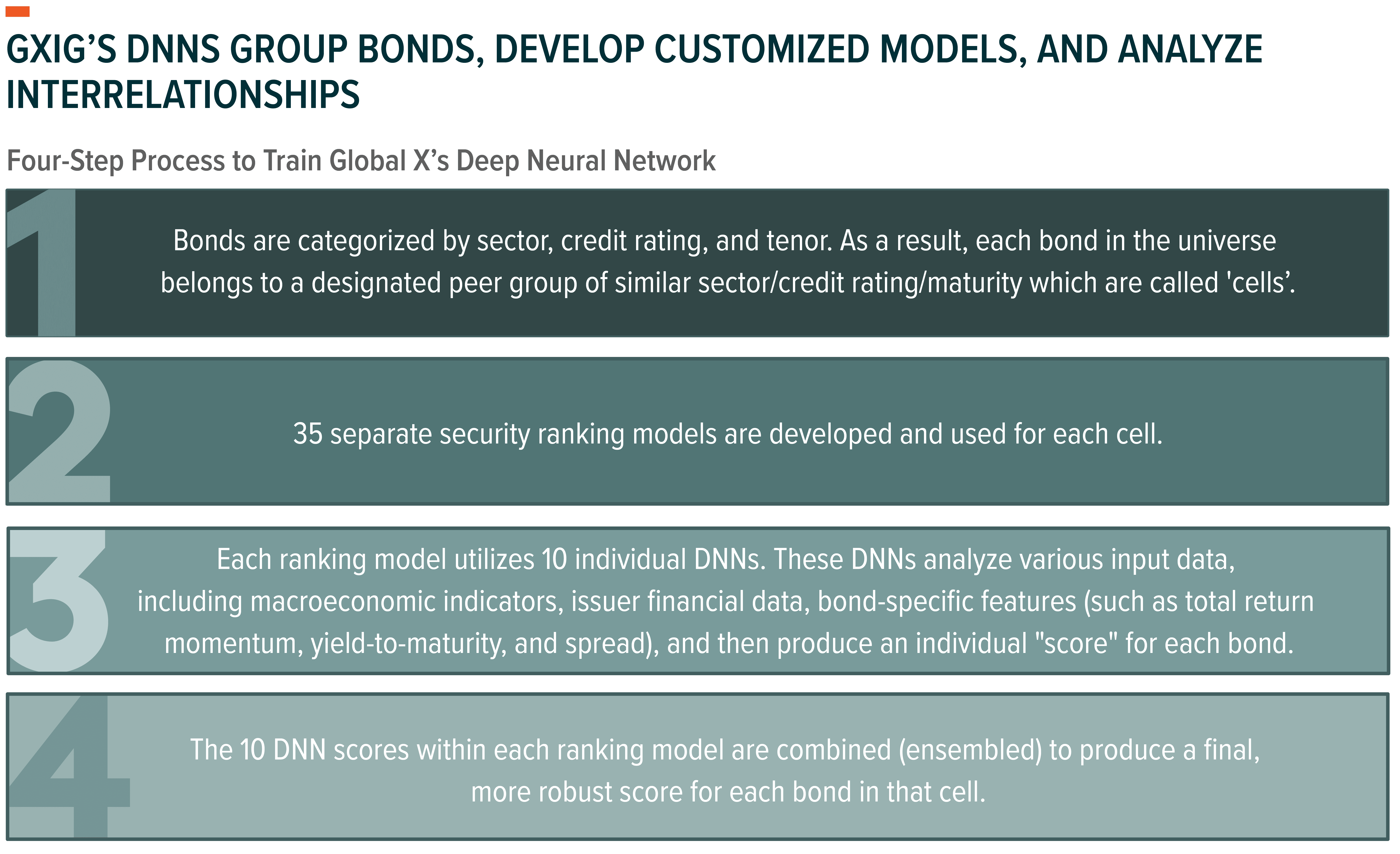

- GXIG’s deep learning model is trained through a four-step process designed to establish an optimal architecture for analysis and forecast expected security returns.

- The vast size and diversity of the corporate bond universe make it a potentially ideal candidate for utilization of a DNN to perform relative value analysis.

Investors Can Now Leverage Deep Learning Models for Quantitative Analysis

For decades, factor investing relied solely on corporate financial data and macroeconomic indicators to help develop stock selection models. In the 2010s, however, the training of machines with diverse algorithms helped push beyond the limitations of these conventions and added a new dimension to the investment analysis approach. Now, their application to artificial neural networks, which we now refer to as AI models, takes the process even one step further.

Unlike other generative models such as ChatGPT that have the potential to produce different results even when given the same input, a trained and “frozen” deep learning model, like that which is used in the Global X Investment Grade Corporate Bond ETF (GXIG), will always generate the same output. In fields like financial investment, where consistency and reliability are essential, this determinism is a critical factor. Once trained, a deep learning model functions much like a calculator. Regardless of who is using it or when, the same input will always yield the same output. This allows the deep learning model to uncover highly complex, non-linear relationships within data sets that are difficult for people to detect. With sufficient data and well-structured layers, neural networks can recognize high-dimensional patterns that cannot be neatly deciphered by conventional analytical or functional approaches.

GXIG Takes a Tactful Approach to Building its AI Architecture and Evaluating Potential Returns

The deep neural network employed by the Global X Investment Grade Corporate Bond ETF (GXIG) is designed to leverage the core competencies and strengths of deep learning technology. The model seeks to learn the relationships that exist between the key variables that it is fed to generate potentially reliable predictions of future returns of individual securities. These data sets include market data, economic indicators, and corporate financial data. With guidance from an experienced portfolio management team, a skilled model developer secures as much relevant data as possible, particularly amongst those variables that they believe best explains bond price movements. Through iterative testing, the developer then designed the neural network architecture that is deemed most suitable for this task. The GXIG model has been trained through repeated hypothesis testing and robustness checks to seek to be sure its performance is meaningful and reliable.

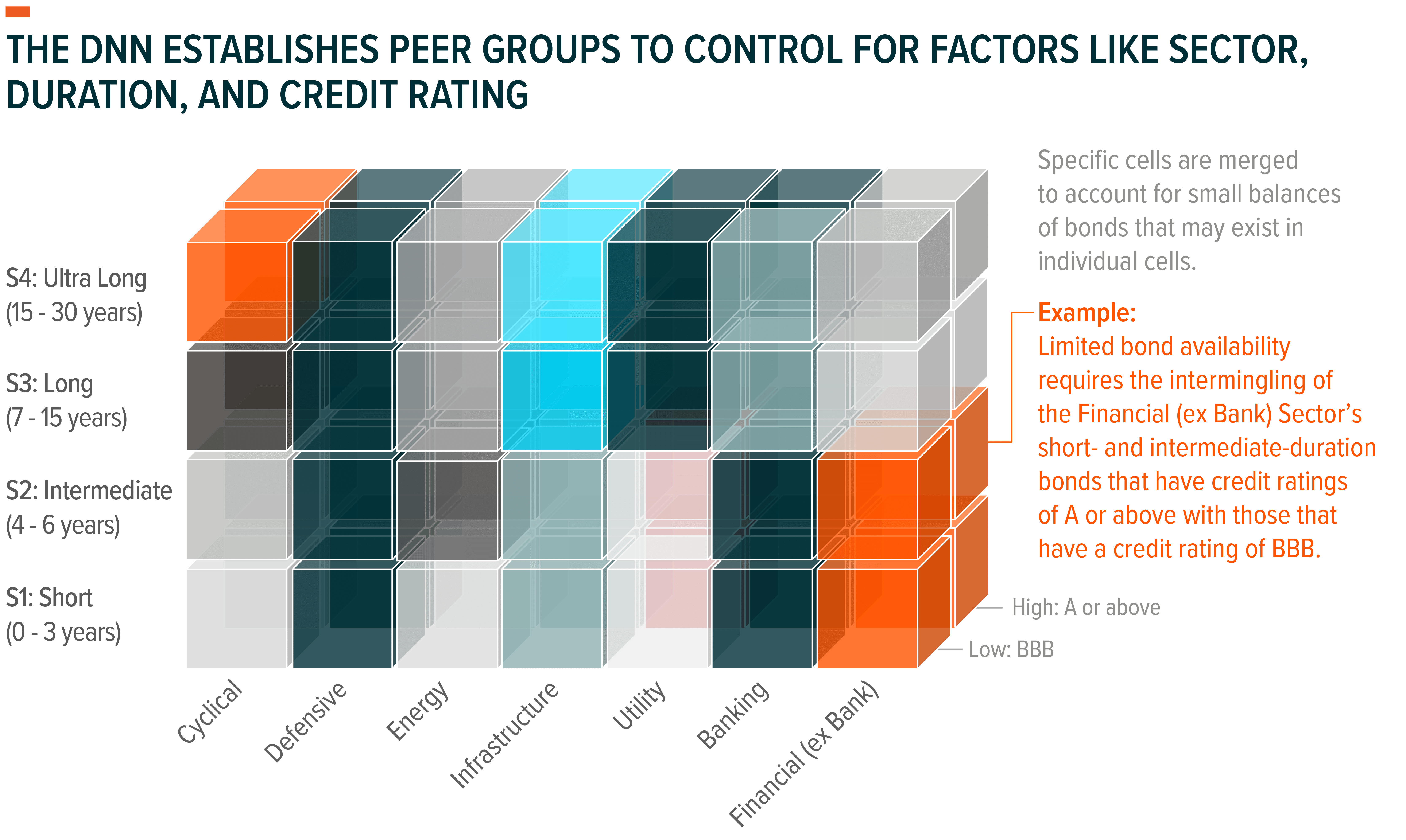

Step one of the training process is to classify the securities that exist in the investment grade corporate bond universe as dictated by the Bloomberg U.S. Corporate Index. This phase of the analysis is aimed at controlling for variables that fall outside the scope of security selection such as issuing sector, bond duration, and credit rating. Provided that enough of a constituency must be made available in order to train the model within each respective peer group, it breaks down the universe into 35 subgroups known as “cells”.

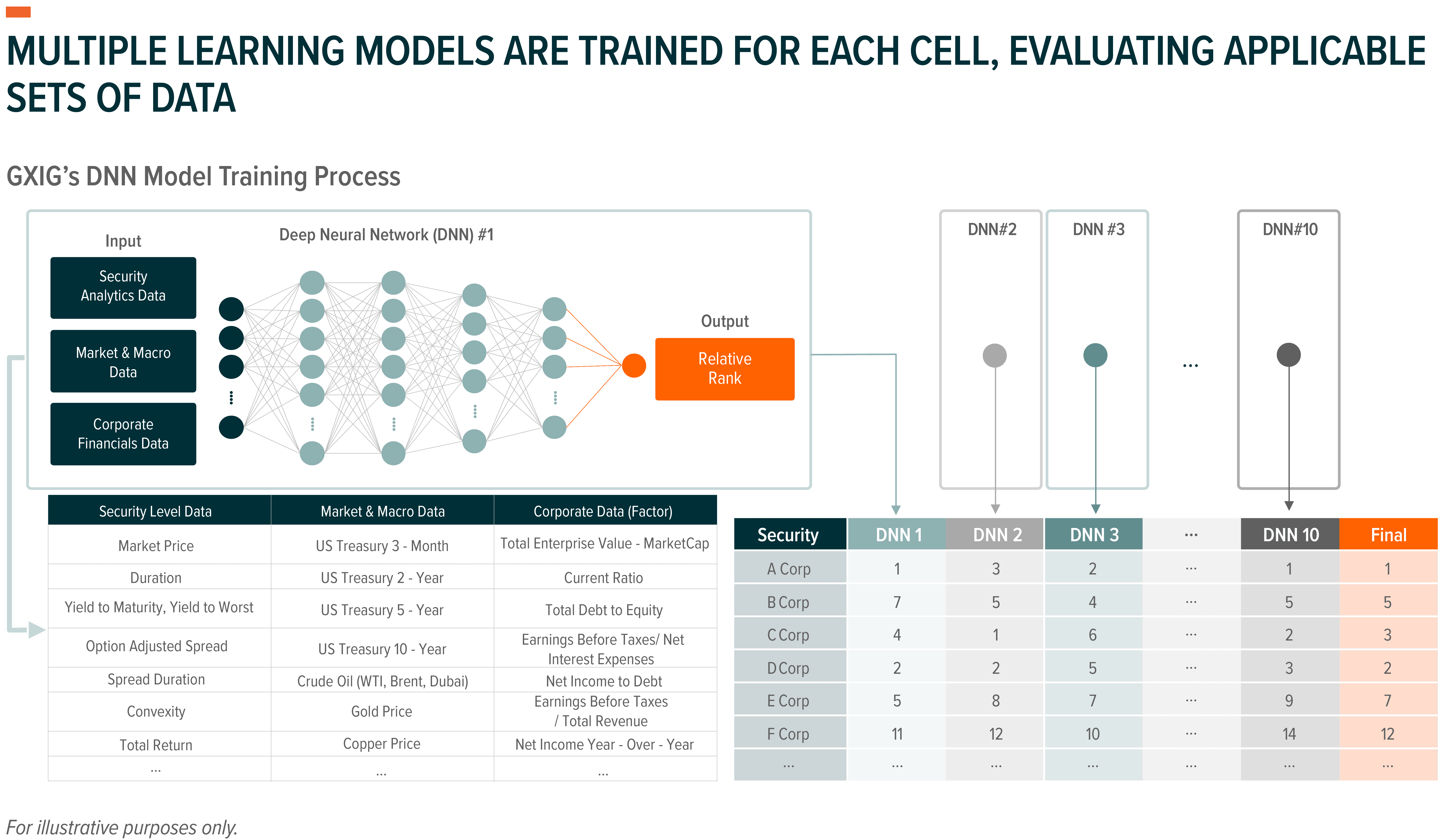

In the next phase of the process, separate deep learning models are trained for each of the 35 cells. Market data, economic data, and corporate financial data are all used as inputs and, for each cell, ten independent DNNs are trained to enhance robustness. Through extensive trial and error, combinations of the most representative financial statement items—such as cash flow, operating income, debt structure, interest expense, total assets, short-term investments, and revenue—are tested. Numerous experiments are also conducted on the overall architecture, including decisions about which data should feed into which layers of the neural network, requiring countless iterations to refine the design. The DNNs are aimed at addressing potential issues caused by random initialization in neural network training by being trained separately under the same methodology. Their results are then aggregated to enhance robustness. This ensemble approach can be likened to gathering the consensus of ten different research analysts, each bringing their own perspective to the same question.

Once the optimal architecture has been identified, it undergoes extensive validation, including backtesting from multiple perspectives, to assess generalization performance. From this process, the final models are selected. These models are stored and used solely for inference, with no further training applied. Based on inference results, ranking tables are created for the securities within each subgroup. The final stage involves verifying performance through backtests on hypothetical portfolios constructed according to these rankings. Ultimately, this step operates at the strategy level, where portfolio managers decide how best to apply the model’s outputs to real-world investment decisions. The trained model’s output, which forecasts the expected returns of individual securities over the near term, effectively provides a measure of investment attractiveness. Portfolio managers then combine these evaluation results—predicted returns and relative rankings across the entire investment universe—with their own insights and risk management considerations to make final investment decisions, including portfolio construction.

GXIG Offers an Active Optimization Approach to Investing in the Corporate Bond Universe

Application of a deep neural network to the bond analysis process requires elaborate model training and testing to evaluate reliability. To adequately evaluate the merits of bonds within the investment grade corporate bond space, however, this is a process that might be deemed worthwhile. Because the universe exhibits such depth, the incorporation of an AI model to evaluate the interrelationships between hundreds of factors across thousands of bonds can help save time and allow managers to be nimbler. It also helps address some of the more traditional shortcomings that come with pursuing exposure to this segment of the market in a passive fashion.

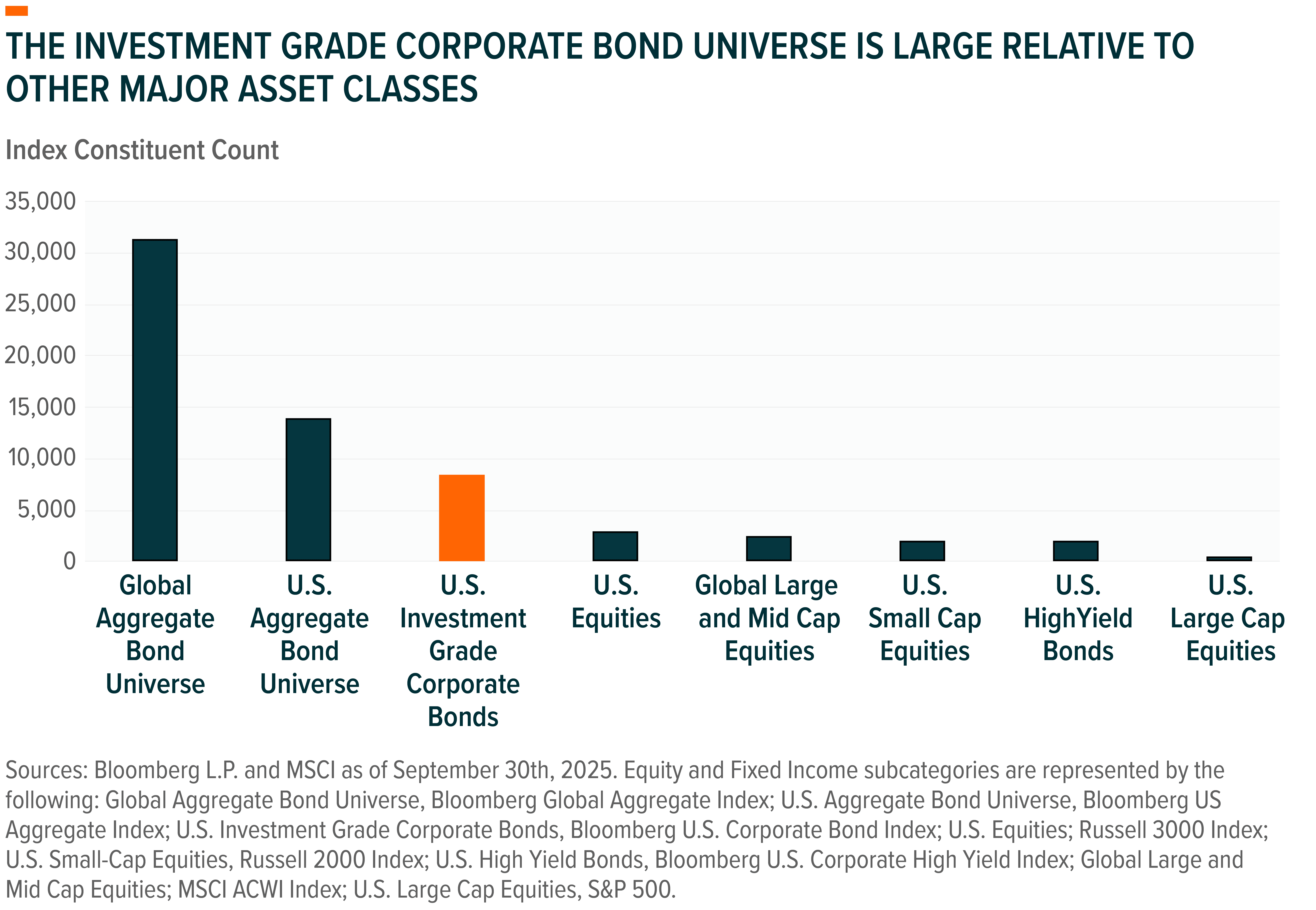

On September 30th, 2025, the Bloomberg U.S. Corporate Index consisted of roughly 8,500 bonds.1 And while some of these issues may fail to make the first cut for analysis even in traditionally screened portfolios, ranking investment opportunities across the balance of the securities that fall into this universe can still prove time consuming. Major equity indexes whose names bear their constituent count pale in comparison in virtually all instances relative to a group of this magnitude. Even High Yield Corporate Bonds consist of only about a quarter of the aforementioned total. Add in the wealth of factors that can be analyzed and applied to the right peer groups in the right market environments and the depth of analysis that must be performed can quickly become quite daunting.

Passive approaches have moved to tackle this challenge, but a potential shortcoming that arises is in gaining exposure using an index methodology that more heavily weights bonds that have the most debt, rather than a high quality of debt. Or, if utilizing a high-quality debt index, whether its constituents are still deemed to possess interesting capital appreciation potential. The passive route comes equipped with a variety of other potential pitfalls, as well, including less flexibility around rebalancing timing, requirements to hold securities that might be deemed of lesser quality, or the inability to address credit- or news-oriented events.

Conclusion: GXIG’s Cutting Edge DNN Transforms Bond Screening for its Fund Managers

There are many idiosyncratic factors that can influence the value of a bond. But before investors even approach that portion of their analysis, it can be helpful to have a screening process in place. The DNN utilized by GXIG is a fast and tested way for Global X’s management team to pursue this screening initiative, and it even has the potential to provide added value by recognizing patterns that might go otherwise unseen. Combined with GXIG’s experienced portfolio management, it strives to deliver stronger investment outcomes and more resilient strategies for clients in almost any market environment.

Related ETFs

GXIG – Global X Investment Grade Corporate Bond ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.