Investment grade (IG) debt has long offered an interesting combination of income and capital preservation potential that’s promoted its stalwart position in diversified portfolios. In the right conditions, it has also served as a tactical allocation, potentially benefiting investors seeking both stability and opportunity. The recent environment has been characterized by falling interest rates and still-attractive yield potential, which has brought these instruments back to the forefront of investor conversations. To address the opportunity with thoughtful portfolio construction and risk management in mind, the Global X Investment Grade Corporate Bond ETF (GXIG) and the Global X Emerging Markets Bond ETF (EMBD) aim to provide disciplined exposure to U.S. and Emerging Market (EM) debts, respectively, leveraging the ETF wrapper for both tactical and income-oriented investors.

Key Takeaways

- Investment grade bonds can offer income, differentiation, and a portfolio ballast, with today’s yield environment potentially enhancing their appeal.

- Active management of IG bond positions can potentially prove important in navigating credit cycles, evaluating regional divergences, and identifying sector-specific opportunities.

- We believe the fixed income investment narrative still has legs, and GXIG and EMBD can deliver active exposure with the liquidity and transparency of ETFs.

The IG Investment Case is Multi-Layered

The core competencies behind why IG corporate bonds have staked a permanent place in balanced portfolios are unwavering. These securities have historically represented sources of ordinary income; their defensive features have been characterized by the very credit ratings with which they are attributed; and they tend to trade with lower correlations to U.S. equities, granting them the potential ability to cushion drawdowns in an overall portfolio in periods of equity market volatility.1

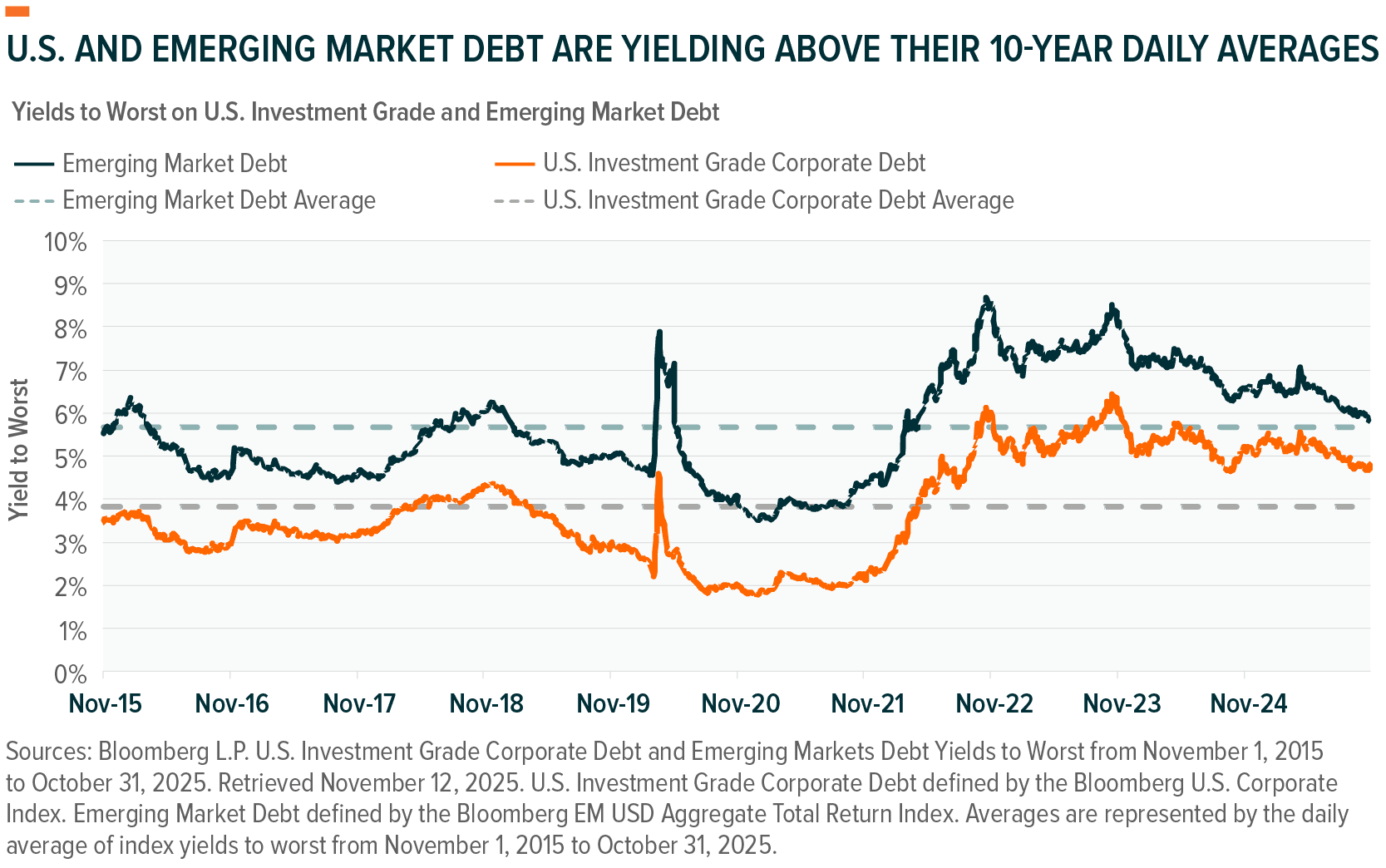

These traits have proven particularly evident within the U.S. corporate bond market, which has matured into one of the deepest and most liquid bond markets in the world. They’ve made domestic IG debt a potentially appealing allocation, with scalability across portfolios of all shapes and sizes. This appeal has been further accentuated in recent market dynamics, which have featured yields to worst that are elevated relative to the last decade.

Index results are for illustrative purposes only and do not represent actual Fund performance. Index data does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

The IG case isn’t just tethered to the U.S., either. Investors have seen meaningful development of Emerging Markets that have made them potentially more attractive allocations, as well. Sovereign and corporate issuers in these geographies, specifically, have gained recognition for their improving fiscal and monetary policies. This has led to enhanced credit quality and more options in EM’s investment grade securities. And with yields elevated in EMs, similar to that of the US, relative to the long term, these bonds provide additional opportunities in the forms of geographic diversification and exposure to potential growth dynamics not always available in developed markets.

The Dynamic IG Bond Market is Prime for Active Solutions

The fundamental characteristics of IG bond exposure have historically represented enough incentive for investors to get their foot in the door. However, the rapidly shifting fixed income landscape has highlighted the critical value that active management can provide. Credit spreads can widen and contract quickly, creating dislocations that can reward thoughtful allocation across issuers and sectors. Oversight may also add value when dealing with duration, particularly as rate paths remain uncertain. Beyond risk management, active selection may help avoid concentration in overleveraged issuers, while managers may be able to identify credits with improving fundamentals.

Looking to EM bonds, we think the active case is no less important. In fact, there are potentially even more variables to take into consideration. Country fundamentals can vary widely, and the dispersion between issuers might be better addressed through rigorous research. Currency risks, liquidity considerations, and geopolitical developments all call for careful navigation, and an active approach allows managers to potentially overweight countries with improving fiscal dynamics while seeking to avoid those facing structural challenges.

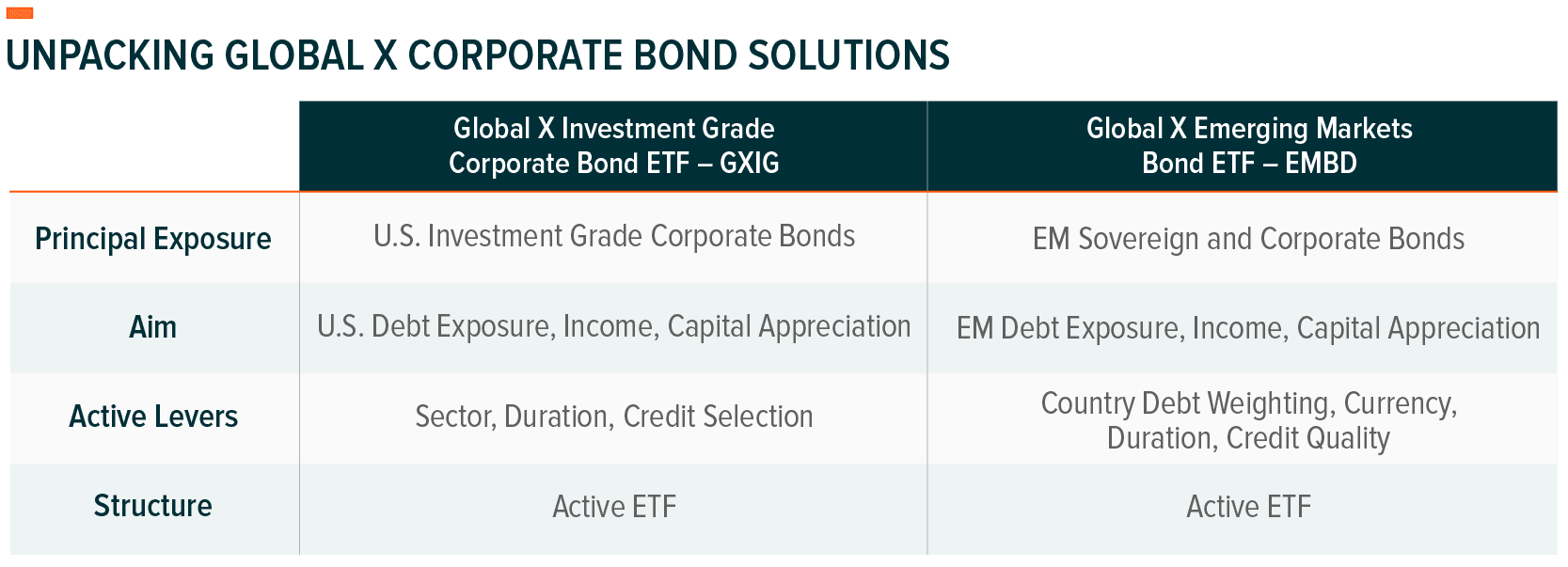

GXIG and EMBD were launched to help address these needs. The former provides exposure to investment grade corporates with an active investment team that considers liquidity, diversification, and risk-adjusted return potential when making allocations. Meanwhile, EMBD focuses on EM exposure, and similarly maintains the ability to dynamically adjust exposures to particular geographies, industries, and currencies. Through active oversight, these funds may provide a source of income while still preserving the flexibility to manage duration and credit exposure within the ETF structure.

The Runway for Corporate Bond Price Appreciation May Still Be Intact

The markets in which GXIG and EMBD participate have recently exhibited noteworthy gains. Over the first nine months of 2025, the Bloomberg US Corporate Index appreciated 6.88% in value, while the JPMorgan EMBI Global Core Index rose 10.47%.2 Their performances have been underpinned by strong credit fundamentals, attractive yields, and a stretch of declining interest rates that saw the yield to worst on the 10-Year U.S. Treasury instrument fall 42 basis points, to 4.15%, through the end of September.3 Investors allocated to bonds to reflect uncertainties around growth, expectations for inflation, and monetary policy that all highlighted the need for income streams. Now, with many of these forces still influential, we see further potential for these exposures to provide portfolio value.

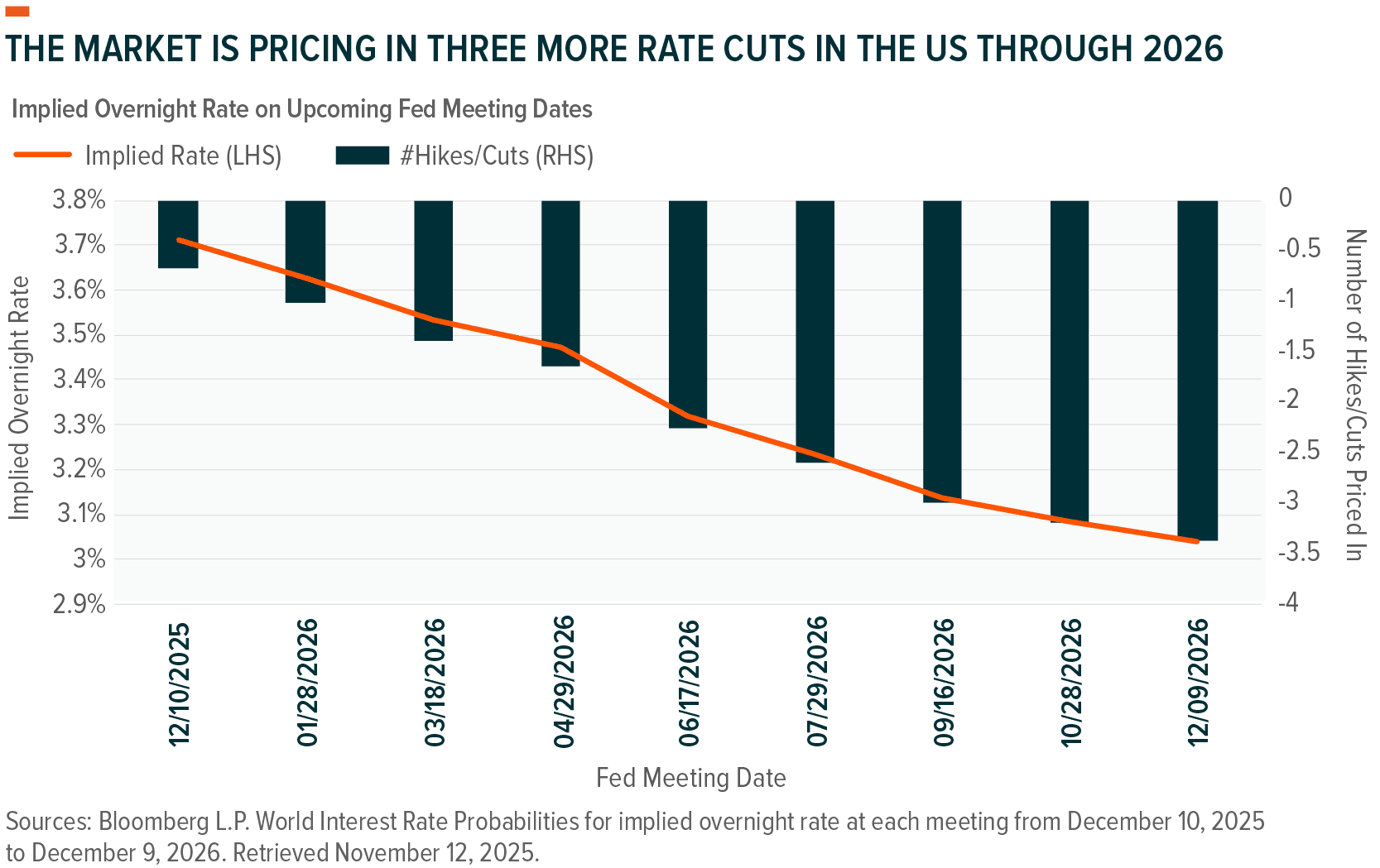

Perhaps the most important factor at present is the ongoing interest rate cutting narrative that’s taking place around the world. Within the U.S., rate cuts resumed this fall with 25 basis points of relief being etched in at both the Federal Reserve’s September and October meetings. A softening labor market and somewhat stubborn price inflation have given investors some pause since then. However, as of October 31st, World Interest Rate Probability metrics were still pricing in about three more cuts in the U.S. by the end of 2026.

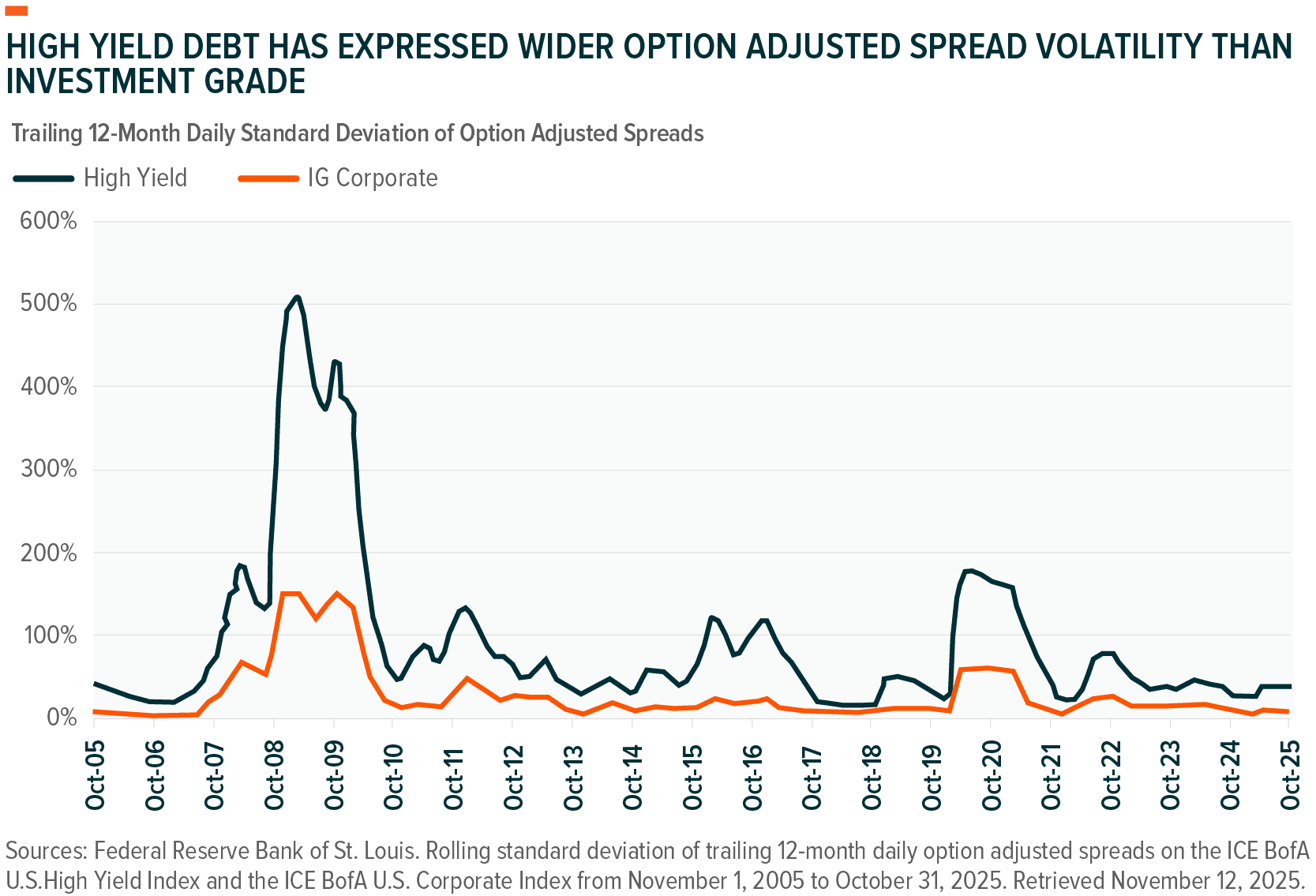

Spreads also remain rather tight across the domestic corporate bond space. And while this might result in less potential reward, on a relative basis, for taking on corporate credit risk, we believe IG bonds are positioned well compared to high-yield instruments, which may not be paying investors enough to consider such exposure. Option adjusted spreads expanded heading into late fall, but this served to exemplify the more volatile nature of high-yield spreads versus investment grade instruments. Should spreads continue to widen, GXIG maintains its active management approach to address exposures related to such risks.

In this environment, investors who are strictly looking for additional yield may be inclined to diversify internationally rather than by simply wading further out across the credit spectrum domestically. EM bond spreads are typically attractive relative to U.S. Treasuries and offer above-average compensation for the risk taken from a historical perspective. This reflects monetary tightening enacted by EM central banks well ahead of the Federal Reserve, which should leave them in good position to continue easing rates in the years ahead. These dynamics may provide tailwinds for both credit quality and returns. Additionally, we believe improving balance sheets, contained inflation, and higher commodity revenues in certain regions strengthen the case for EM allocations.

Conclusion

The global equity markets have experienced noteworthy price appreciation over the last few years. However, with bonds now offering solid yields and interest rates back on the decline, the moment may be right for more conventional forms of diversification. GXIG and EMBD are ETFs that can provide exposure to corporate fixed income instruments, and they are both managed by active investment management teams that can be nimble in the face of market disruptions. The active style may be helpful when dealing with an asset class that presents opportunities around liquidity, credit quality, and duration, and the ETF wrapper offers an element of accessibility that makes them potentially seamless portfolio additions.

Related ETFs

EMBD – Global X Emerging Market Bond ETF

GXIG – Global X Investment Grade Corporate Bond ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.