Market volatility has dominated the investment landscape in 2025, with both equity and bond markets experiencing significant turbulence. The second quarter proved particularly challenging as the VIX and MOVE indices—gauges of equity and bond volatility, respectively—surged following the Trump administration's tariff announcements. Ongoing uncertainty around U.S. economic indicators, Federal Reserve (Fed) monetary policy, and geopolitical developments has sustained this heightened angst across asset classes.

While such market conditions create considerable uncertainty, they can also generate meaningful dislocations, presenting compelling investment opportunities. In volatile environments, fundamental value often becomes disconnected from market pricing, creating entry points for discerning investors. We examine several of these emerging opportunities and their potential implications for portfolio positioning below, including short-term Treasuries, investment grade corporate bonds, and preferred securities.

Key Takeaways

- Short-term U.S. Treasuries can provide a compelling low-risk, potential high-yielding opportunity in today's environment should we continue to see interest rate volatility and an inverted yield curve. U.S. T-Bills can offer stable income generation while positioning investors to benefit from current rate dynamics with lower risk.

- Investment grade corporate bonds offer a balanced risk-return profile that may be particularly suited for portfolios targeting moderate risk exposure. As trade-related uncertainties may disproportionately impact speculative grade issuers, higher-quality corporate issuers can offer relative stability while relative risk premiums are compressed.

- Preferred securities distinguish themselves as potentially tax-advantaged income-producing investments, and with many preferred issues now trading at substantial discounts to par value this might represent a compelling entry point.

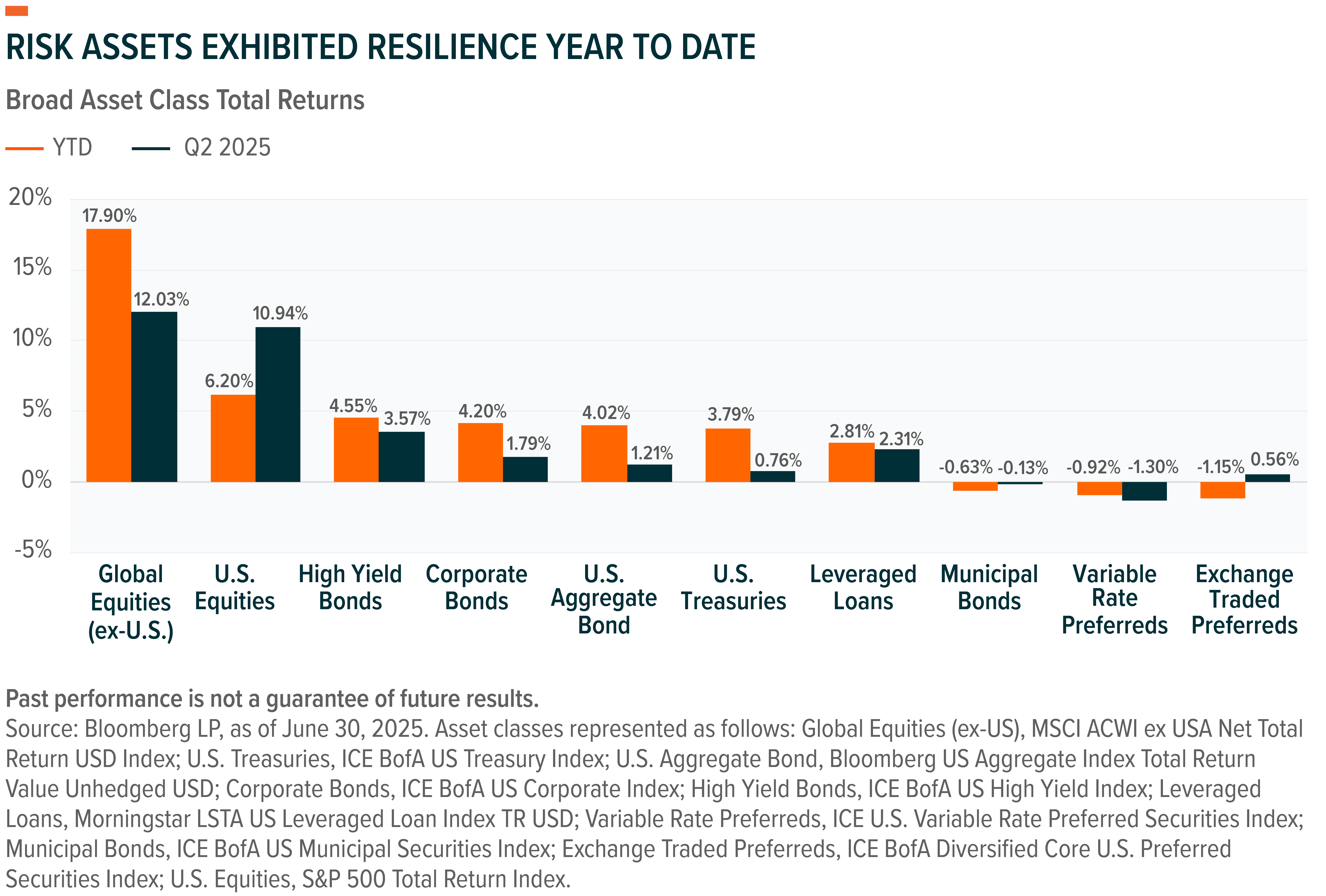

High Yield Has Led Through June, but U.S. Treasuries Proved Their Value

High yield bonds have represented the best performing fixed income asset class in 2025 due in part to their higher income levels. However, over the first four months of the year, U.S. Treasuries reigned supreme as investors sought out safety against a volatile backdrop. Indeed, U.S. tariff implications led anxious investors to more vehemently consider fixed income opportunities with defensive characteristics, and they acted as a “safe haven” in March and April, specifically, when credit spreads—the difference in yield between a corporate and government security—significantly widened.

Markets have remained on edge due to uncertainty about tariffs, with trade tensions between the U.S. and China, in particular, inciting wide price fluctuations. Until a recent trade agreement was reached between the two nations, retaliatory measures caused daily whipsaws in the rates market, mirroring volatility in equity markets and undermining much of the potential diversification benefit that fixed income traditionally provides.

Against this backdrop, and with the Fed maintaining its current stance, investors have increasingly turned to ultrashort bond funds that offer minimal duration risk. Year to date through May 31st, Ultrashort Bond and Short-Term Bond funds have collectively accounted for nearly 30% of net flows among the top 10 Open-End and Exchange-Traded Fund categories tracked by Morningstar.1 With yields at historically elevated levels, these strategies allow investors the potential to capture attractive income while maintaining the flexibility to adapt as trade dynamics continue to evolve.

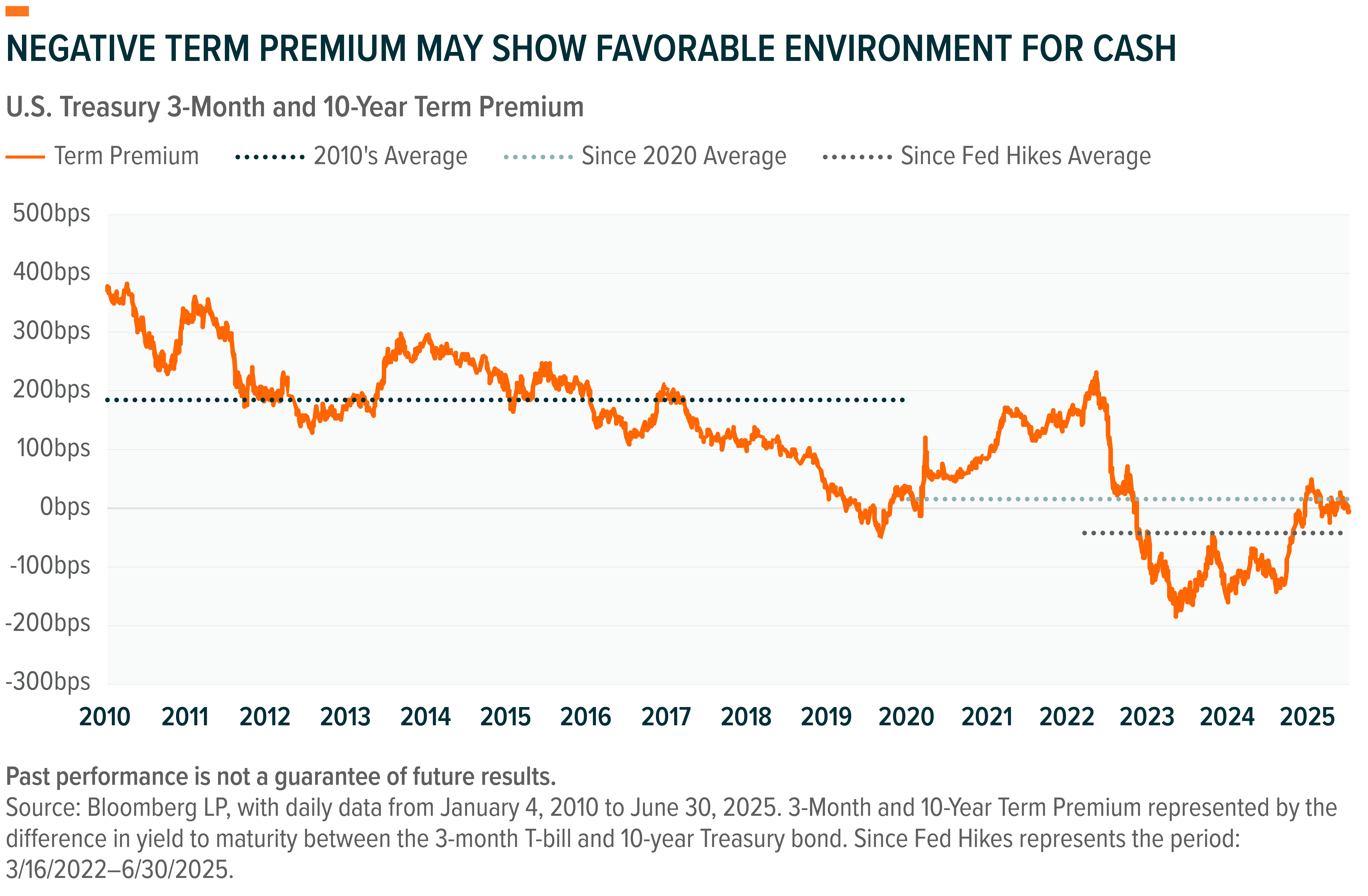

This preference for ultrashort strategies is supported by current yield curve dynamics. Investors are capitalizing on the negative term premium reflected by the current inversion of the yield curve across certain maturities. As of 6/30/2025, the term premium between the 3-month T-bill and 10-year Treasury bond stood at -6 basis points (bps).2 For perspective, the average term premium from 2010–2019 was 183 bps.3 A positive term premium typically compensates investors for extending duration, generally coinciding with pro-growth environments. This negative term premium implies that this compensation is not being provided. From the start of 2020 through June 30, 2025, the average term premium was just 15 bps. Since the Fed began its most recent hiking cycle in March 2022, the average term premium has sat at about -44 bps. With short-term rates near 0% for much of the 2010–2019 period, investors had little incentive to hold cash. However, with the term premium between the 3-month and 10-year tenors inverted, holding short-term T-bills now represents a potentially more attractive way to pursue income with lower risk.

At an expense ratio of 0.07%, the Global X 1-3 Month T-Bill ETF (CLIP) provides exposure to 1-3 Month T-Bills. We believe a high-quality short-term investment vehicle like CLIP can help to mitigate risk in today’s environment while potentially receiving elevated income relative to historical short-term rates.

Relative Valuations May Prove Supportive of Investment Grade Corporate Bonds

For investors allocating within credit, investment grade corporate bonds may represent an optimal risk-adjusted opportunity in the current environment. Yields are elevated across the credit spectrum, which might leave investors less inclined to take on incremental credit risk for not much more of a reward.

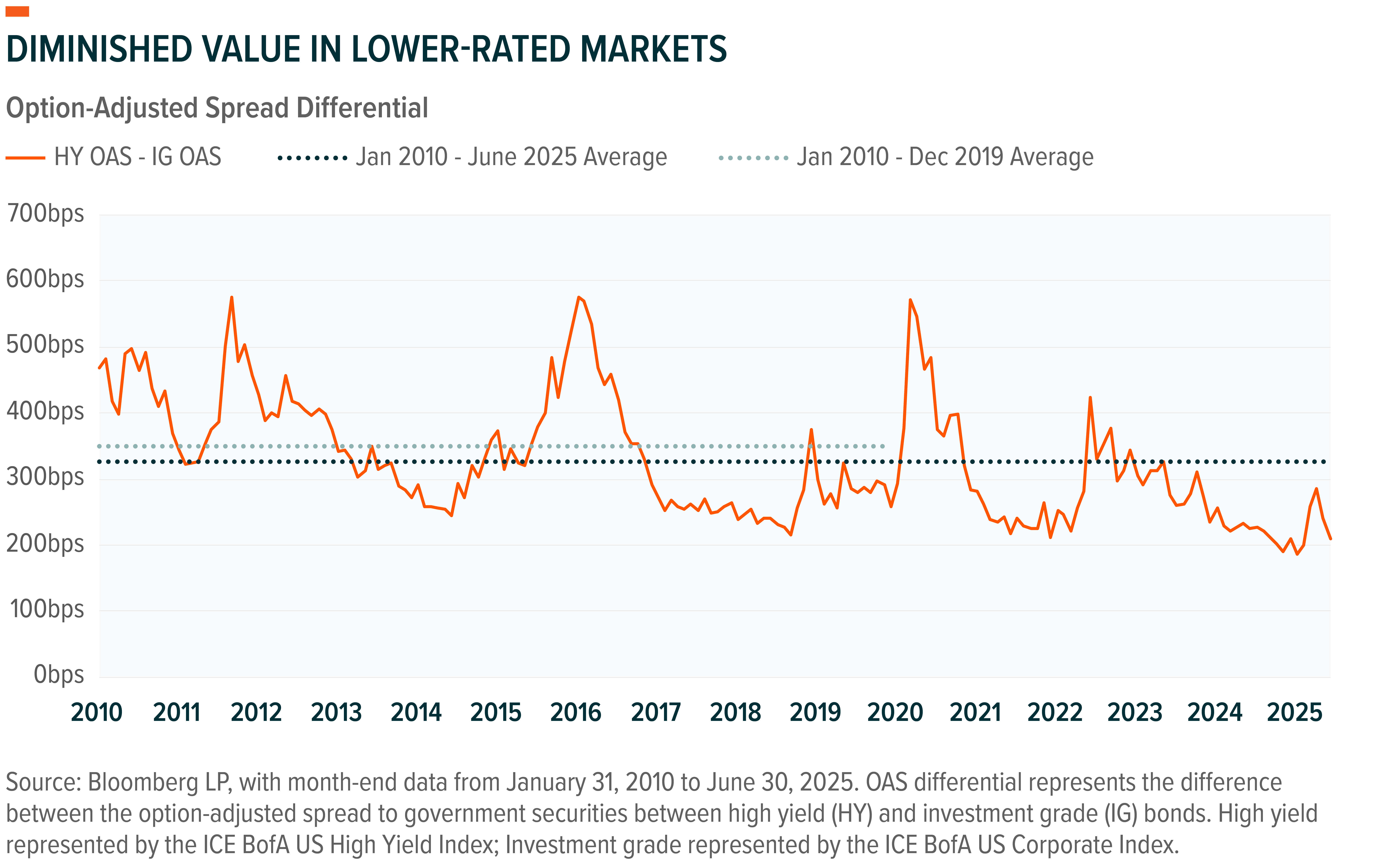

Spread measures between investment-grade (IG) and high-yield (HY) bonds help rationalize some of this relative value discussion, as they remain narrow relative to historic norms. Since recent highs in 2022—when investors sold riskier assets ahead of the Fed's hiking cycle—credit spreads over U.S. Treasuries have compressed by 247 bps for IG and 291 bps for HY. Though, the current spread of high yield over investment grade of 210 bps sits roughly 139 bps below the 2010-2019 average, suggesting investors aren’t getting paid quite as much to take on high-yield credit risk as they had been formerly.

Beyond the argument surrounding spreads, the market volatility that is created by tariff-related uncertainties is another factor worth consideration. Cyclical sectors, in particular, that more typically issue speculative-grade debt, have the potential to experience wide price oscillations as a product of rising import tariff implications. Consumer discretionary companies—the largest sector underweight in IG relative to HY—exemplify this dynamic.4 And despite underlying fundamentals denoted by consumer confidence and employment remaining favorable, conservative investors may not be inclined to take on this volatility risk.

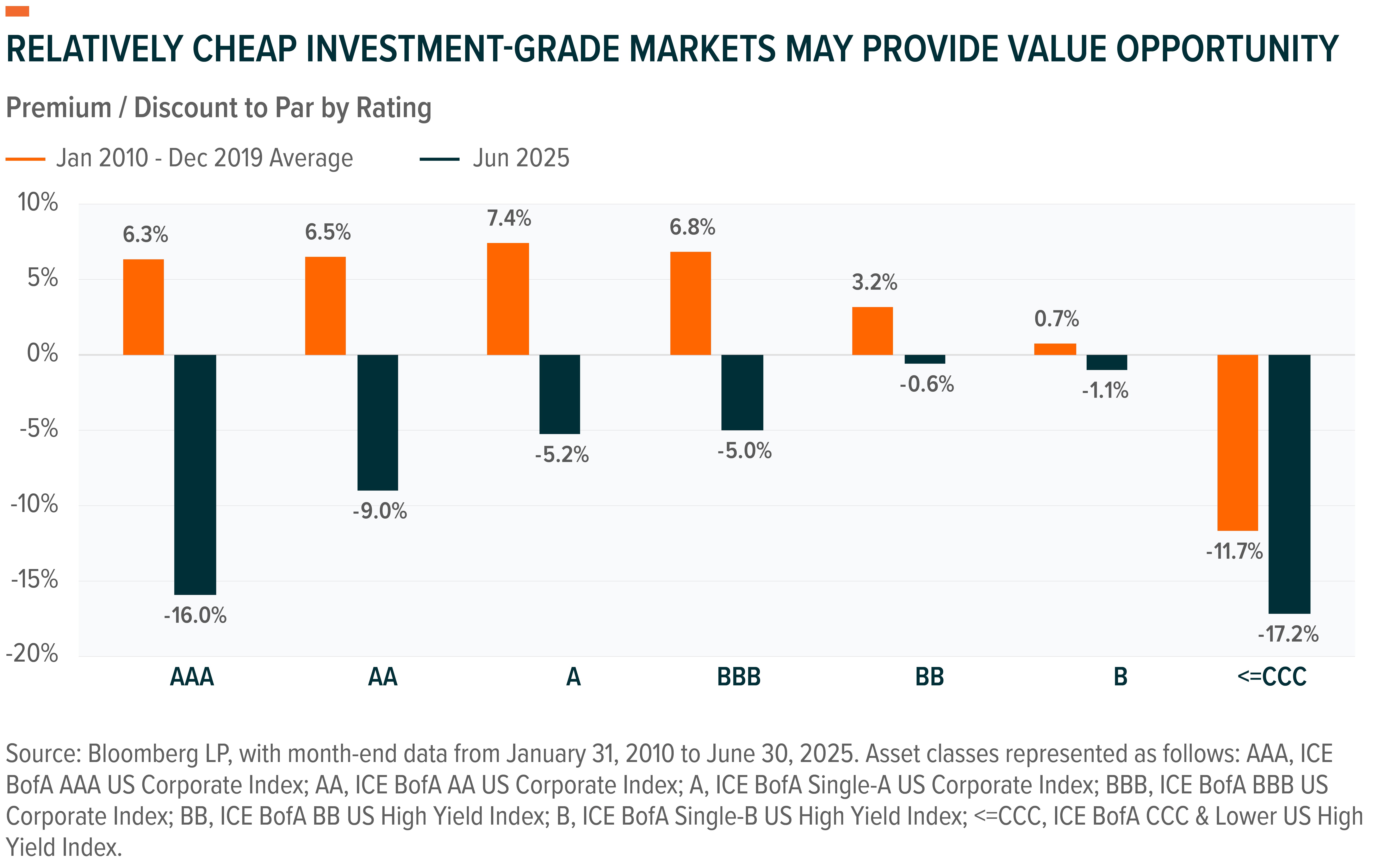

Within the context of investment grade corporate bonds, issues seem to be trading at relatively attractive discounts to par. Currently, ranging from 5% to 16%, they would appear significantly undervalued relative to the premiums that were quoted from 2010-2019.5 Moreover, the spread versus the 2010’s ten-year average is wider than that for high yield. To that end, investors today may not need to sacrifice quality for a worthwhile income incentive.

The recently launched Global Investment Grade Corporate Bond ETF (GXIG) may be an attractive way for investors to access the U.S. investment grade bond market. GXIG employs an actively managed strategy at an expense ratio of 0.14%, representing the lowest cost active U.S. investment grade bond ETF in the market.5 Global X’s portfolio management team applies a top-down analysis approach to the investment grade corporate bond market, assisted by a quantitative factor and deep neural network models to screen and evaluate potential opportunities.

Preferred Securities May Offer Tax Advantages and Currently Trade at Significant Discounts to Par

The same market dislocations that have resulted in investment grade corporate bonds trading at significant discounts to par make the case for preferred securities, as well. Characterized as hybrid instruments, preferreds take on features of both equity and debt, but they sit lower on companies’ capital structures relative to other forms of debt. Many fixed rate preferreds have been trading at these levels for some time, after the Fed’s rate hiking cycle of 2022 led prices to decline. However, they now bear much more generous yields to go along with these significant discounts to par, which may make them a suitable allocation for an income- and growth-oriented portfolio.

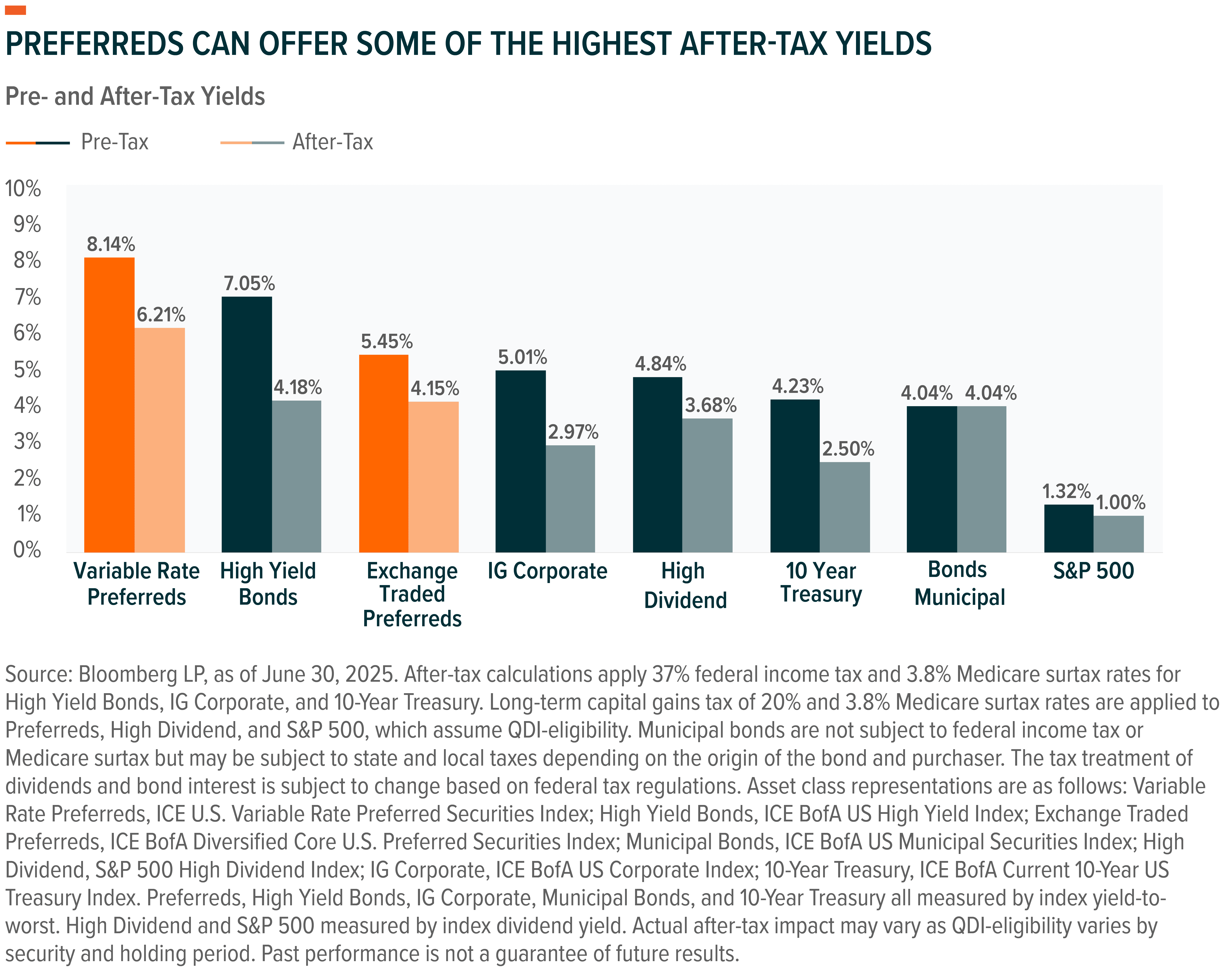

The ICE BofA Diversified Core U.S. Preferred Securities index recently showed a 5.5% pre-tax yield to worst, for example.6 And if we evaluate the implications associated with this yield further, we can glean that these instruments stand out from the perspective of taxation, as well, Preferreds securities often pay distributions in the form of qualified dividend income (QDI), which is taxed at more favorable long-term capital gains rates compared to bonds. Dividends from preferreds are taxed at 0%, 15%, or 20% rates, depending on an investor’s income tax bracket. Bond interest, on the other hand, is treated as ordinary income and taxed at an investor’s marginal income tax rate, which can be as high as 37%.

The chart below shows pre- and after-tax yields for asset classes as of June 30, 2025. Relative to other areas of the market, variable rate and exchange-traded preferreds currently offer some of the highest pre- and post-tax yields available.

Although preferreds are typically issued by investment grade companies, their lower placement in the capital structure, among other factors, is what typically enables them to yield more than their senior debt counterparts, irrespective of having the same underlying issuer fundamentals. In contrast to similarly yielding sectors, high yield bonds carry greater credit risk at the issuer and security level because the companies themselves are speculative grade and more susceptible to the business cycle.

Because prices move inversely to yields, today’s elevated yield levels are paired with many fixed income securities trading at steep discounts to par. For preferreds, this presents a potential opportunity as their discount to par stands at approximately 12% versus a 5% average over the last five years.7

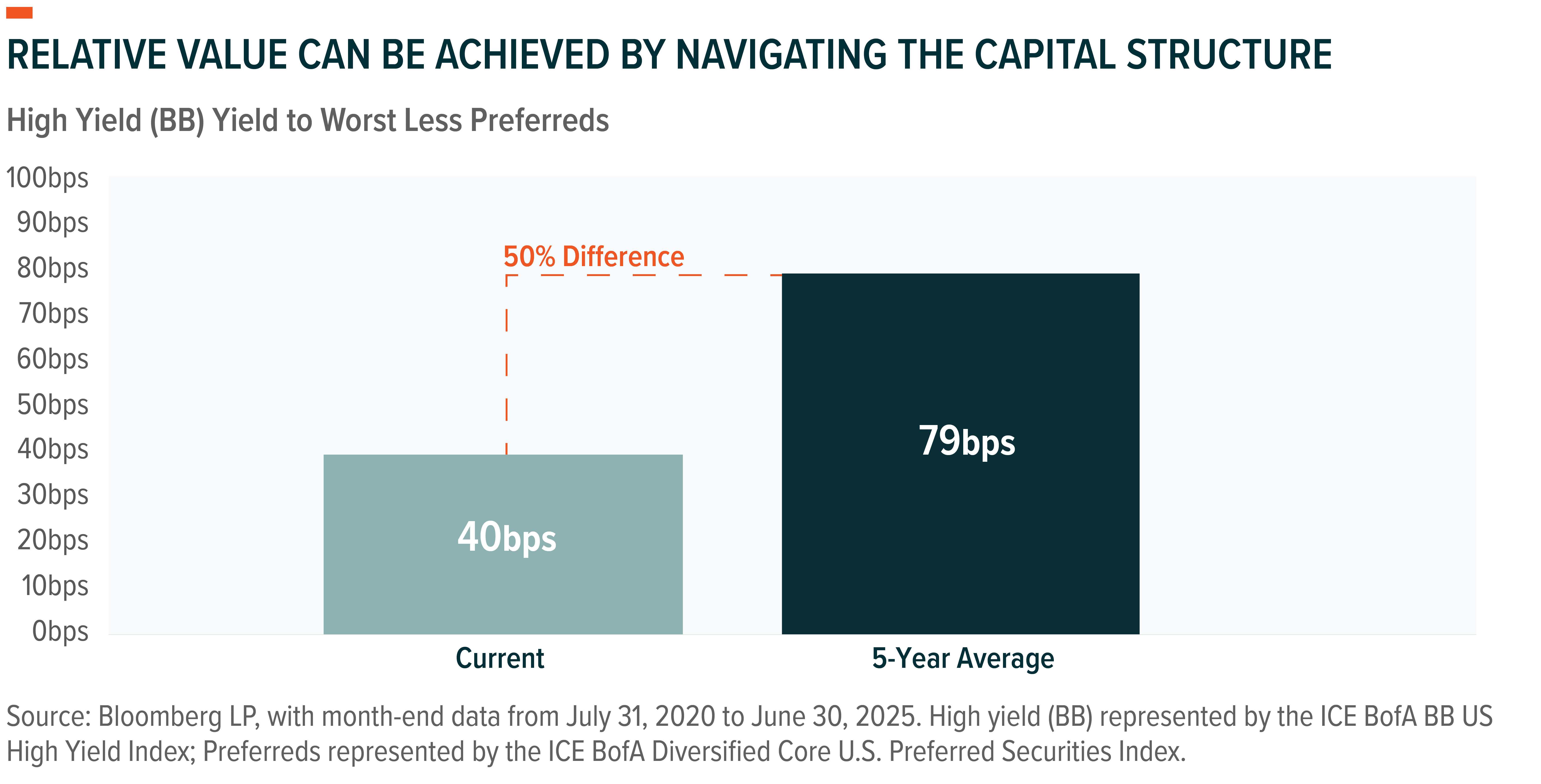

Furthermore, and akin to our former argument centered around whether or not the credit risk on high yield is worth taking right now, the yield premium of high yield over preferreds is also tighter these days than we have historically seen. In fact, over the past five years, high yield instruments have offered an average yield to worst advantage of about 79 bps over preferreds.8 Today, however, that spread is closer to 40 bps, a near 50% discount relative to history, indicating less value in high yield, especially when considering the additional credit risk.9

The Global X U.S. Preferred ETF (PFFD) can provide investors with benchmark-like exposure to the U.S. preferreds asset class. PFFD’s expense ratio of 0.23% is also less than half the competitor average.10

Conclusion: Volatility Has Accentuated the Potential Value of Bonds and Preferreds

Volatility can be difficult to digest, but we believe that investors have income options available to help them in this uncertain time. Short-term Treasuries—with their minimal duration and credit risk—offer a potentially stable and attractive current income source given current yield curve dynamics. For investors allocating within credit, investment grade corporates can benefit from relative value opportunities within the credit curve. Finally, preferreds combine elevated potential tax-advantaged income, discounted prices, and relative value opportunities. Taken together, these three assets can offer varying blends of quality, income, and relative risk exposure that may prove attractive should volatility remain intact over the balance of 2025.

Related ETFs

CLIP – Global X 1-3 Month T-Bill ETF

GXIG – Global X Investment Grade Corporate Bond ETF

PFFD – Global X U.S. Preferred ETF

Click the fund name above to view current performance and holdings. Holdings are subject to change. Current and future holdings are subject to risk.